Home • Blog • Blog for entrepreneurs • Tax holidays for individual entrepreneurs in 2020

Tax holidays for individual entrepreneurs in 2021 continue. For the first time, registered entrepreneurs using the simplified tax system and special tax system can use a 0% rate until 2024. This is indicated in Federal Law-266 dated July 31, 2020.

Reasons for extending tax holidays

Tax holidays have been in effect since 2015. They were originally planned until 2021. But due to economic fluctuations in the country, they were repeatedly extended. In 2021, the reason for extending tax holidays has again appeared - the spread of coronavirus infection, as a result of which a pandemic was declared throughout the world. Entrepreneurs in many areas of activity temporarily stopped working, which could not but affect the economic situation.

“Panic sentiment” among entrepreneurs further worsened the situation. Many began to be afraid to open their own business so as not to incur losses. To support “young” entrepreneurs and attract new taxpayers, the Government decided to extend the tax holiday. They are focused primarily on small businesses.

New tax payment deadlines

Small and medium-sized businesses that are included in the Register of SMEs and operate in affected industries/areas (the list is determined by the Government of the Russian Federation) have had tax payment deadlines postponed. They are presented in the table below.

Also see “Companies from which industries will receive help due to coronavirus: official list.”

| WHAT IS THE TAX/FEES? | PAYMENT DURATION |

| Income tax for 2021 Unified agricultural tax (UST) for 2019 Tax according to the simplified tax system for 2019 Taxes (advance payments) for March and 1st quarter. 2020 EXCEPTIONS:

| For 6 months |

Taxes (advance payments) for:

Patent tax (PSN), the payment deadline for which falls on the 2nd quarter. 2020 | For 4 months |

| Personal income tax on individual entrepreneur income for 2019 | For 3 months |

Also, for SMEs included in the Register as of 03/01/2020, due to the coronavirus, a deferment of taxes (advance tax payments) has been made: transport, land and corporate property taxes:

- for the 1st quarter of 2021 – until October 30, 2020 inclusive;

- for the 2nd quarter of 2021 – until December 30, 2021 inclusive.

Extension of deadlines for payment of advances on property taxes, as well as postponement of deadlines for their payment for organizations of other categories, is possible on the basis of regulations of the highest executive bodies of state power in the regions.

The following table shows all the new tax payment deadlines for 2021, taking into account Resolution No. 409.

Below are the typical tax payment deadlines and tax deferrals due to the coronavirus in 2021 for small and medium-sized businesses in affected industries.

Conditions for using the grace period

Tax holidays are a period during which entrepreneurs have the right to work with zero tax rates.

Preferential conditions are provided for “simplified” entrepreneurs and individual entrepreneurs with a patent who registered as entrepreneurs for the first time. There are requirements regarding the type of activity:

- Production of goods;

- work in the field of science;

- social sphere;

- provision of household services to the population;

- Providing the population with places of temporary residence (hotels, hotels).

It is worth noting that types of activities can be established on an individual basis. You need to check with local authorities about which ones operate in a particular region.

These categories of taxpayers are allowed to use zero rates if they register as individual entrepreneurs before January 1, 2024. The right to provide benefits has been transferred to regional authorities.

Another condition for using tax holidays for individual entrepreneurs in 2020 is that the share from the sale of goods, services or work is 70% or more of total income. That is, profit from preferential activities should prevail in the total profitability.

Tax holidays for individual entrepreneurs are valid for two tax periods.

Results

Tax holidays for individual entrepreneurs are valid in 2021, and will continue to be valid in 2021-2023.

They allow entrepreneurs on a simplified basis or a patent to apply a zero rate for the simplified tax system or PSN if a number of conditions are met: registration as an individual entrepreneur occurred for the first time after the regional authorities adopted the law on tax holidays, the share of income from preferential activities is at least 70%, and the types of activities themselves are listed in the regional law. The same law may establish additional restrictions on the average number and maximum allowable income. You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Restrictions

Local authorities have the right to independently determine restrictions that apply to the activities of entrepreneurs using tax holidays:

- the number of employees;

- profitability.

Important! Tax holidays apply only to the simplified taxation system and special taxation system. If an entrepreneur works on several taxation systems, according to others he pays the tax in full.

Despite the temporary exemption from tax, insurance premiums must be paid throughout the tax holiday period - contributions are made to the Pension Fund for yourself and for employees. It is also important to understand that at the end of the year a declaration is submitted indicating a 0% tariff. Tax holidays are valid until 01/01/2024.

“Young” entrepreneurs have enough time to register with the Federal Tax Service and save money.

A little history

Tax holidays are not a new concept. They began to be introduced in 2015. At first there was an assumption that they would be in force until 2021, that is, until the country recovered from the crisis, but for various reasons the validity of the bill was extended. 2021 provides a good reason to take advantage of this privilege again.

Representatives of Russian business, in particular young entrepreneurs, no longer look to the future with optimism. Many people are in a pessimistic mood, to put it mildly. And in such a situation, a tax break is simply necessary, because this is the only way to support small businesses, which means tax holidays for LLCs will come in handy.

Is there a benefit for re-registered individual entrepreneurs?

Consider the following situation. The entrepreneur stopped his activities, and then decided to register as an individual entrepreneur again. Moreover, he did this after the law on tax holidays was approved. Is it possible to take advantage of the benefit in this case or does it not apply to those who register again?

Initially, Letter No. 03-11-11/40882 dated July 12, 2021 stated that tax holidays cannot be used by individual entrepreneurs who suspended their activities and then re-registered as individual entrepreneurs.

But the Supreme Court refutes these data. According to his decision, entrepreneurs who were previously registered as individual entrepreneurs, then ceased their activities, then resumed them after the approval of tax holidays, are not excluded from the list of “beneficiaries”. Each case is considered individually.

Of course, all individual entrepreneurs receive the right to tax holidays in 2021 and beyond only if they meet the stated requirements.

Tax holidays in the Krasnoyarsk Territory

Any person who decides to open his own business is faced with the question of choosing a legal form and tax system.

The advantage of registering as an individual entrepreneur is tax holidays.

Tax holidays mean the ability to apply a tax rate of 0 percent for up to two tax periods in a row when using simplified or patent taxation systems.

In the Krasnoyarsk Territory, a tax holiday regime for individual entrepreneurs has been in effect since July 1, 2015.

A zero tax rate is established for individual entrepreneurs operating in the production, social and scientific spheres, as well as in the provision of consumer services to the population. First-time registered individual entrepreneurs can take advantage of the benefit. If an individual entrepreneur is deregistered and re-registered, he is not subject to the law on tax holidays. Specific types of activities can be viewed in the Regional Law dated June 25, 2015 No. 8-3530 by following the link https://zakon.krskstate.ru/0/doc/25468.

The validity period of tax holidays is limited by federal law dated December 29, 2014 No. 477-FZ. Therefore, you can use this regime until January 1, 2021.

Let us remind you that, subject to the simultaneous observance of what conditions, an individual entrepreneur in the Krasnoyarsk Territory can take advantage of the preferential treatment.

- If an individual entrepreneur was first registered no earlier than January 1, 2021 in the field of providing household services to the population and no earlier than July 1, 2015 for other preferential activities;

- Applies a simplified and (or) patent taxation system;

- Activities are carried out in the production, social and scientific spheres or in the provision of consumer services to the population;

- The share of services, works or goods subject to a 0% tax rate in this area is at least 70% of total income.

There is no special procedure for switching to tax holidays for start-up entrepreneurs. Those who have chosen the simplified tax system simply do not pay advance payments and taxes at the end of the year, and indicate a zero rate when filing a tax return. Those who have chosen the patent system must indicate the applicable tax rate (0 percent) in the application for a patent with reference to the norm of Regional Law No. 8-3530, which will be stated in the issued patent.

It is important to remember that if an individual entrepreneur receives the right to apply a zero tax rate, this does not exempt him from paying other mandatory payments: transport tax; fixed insurance premiums for yourself; personal income tax and insurance premiums for employees.

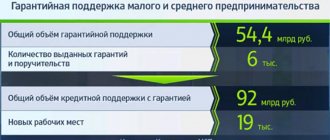

Tax holidays in the Krasnoyarsk Territory are gaining popularity. So in 2021, for the first time, registered individual entrepreneurs received 766 patents with a zero tax rate, which is 1.8 times more than in 2021. In addition, about 400 individual entrepreneurs using the simplified taxation system took advantage of the tax holiday.

The majority of zero-rate entrepreneurs who use a simplified taxation system choose manufacturing (85 individual entrepreneurs), construction (62 individual entrepreneurs), transport and communications (53 individual entrepreneurs), and agriculture (49 individual entrepreneurs).

Among individual entrepreneurs in the patent taxation system, welding and electrical installation work; home repair; tutoring and conducting classes in physical education and sports.

The estimated amount of tax under the patent and simplified taxation system for 2021 was 92 million rubles. These funds would have to go to the treasury, but within the framework of the law on tax holidays, individual entrepreneurs will be able to use them to develop their own business.

How to take advantage of tax holidays

In order to join the ranks of “beneficiaries” and pay tax at a 0% rate, individual entrepreneurs using the simplified tax system or PSN do not have to submit any special documents. Immediately after registration with the Federal Tax Service or within 30 days after registration, a standard application is submitted according to f. 26.2-1 or 26.5-1 (depending on which taxation regime is planned to be used). The 0% tax rate is indicated when submitting the declaration.

Note! If you make advance payments during the year, even if the individual entrepreneur had the right to a tax holiday, it will not be possible to return the funds spent. You will have to file a tax return showing the interest rate at which the payments were made.

What taxes will companies be able to defer due to the pandemic?

Representatives of sectors of the economy affected by the pandemic will be able to defer the payment of statutory taxes and advance payments of taxes for March and the first quarter of 2021. Also this:

- deadlines for payment of insurance premiums calculated from payments and other remuneration in favor of individuals for March 2021;

- deadlines for payment of insurance contributions for compulsory social insurance against industrial accidents and occupational diseases accrued from payments and other remuneration in favor of individuals for March 2021;

- deadlines for payment of advance payments for transport tax, corporate property tax and land tax for the first quarter of 2020 (if the laws of the constituent entities of the country, regulatory legal acts of representative bodies of municipalities provide for the payment of advance payments for such taxes).

Some are lucky, some are not. Where is it good to live in Russia during a crisis? More details

An exception will be taxes on value added, on professional income and taxes paid as a tax agent. They will have to be paid on time.

List of subjects of the Russian Federation

Currently, only a few regions have extended the preferential rate until 2024. For others, this issue is under active discussion. In Moscow itself and the Moscow region there is still no accurate information about the extension of tax holidays. According to official data, the preferential treatment in the capital and district ends on December 31, 2020.

Detailed information is in the table. Of course, this is not final data. The list will be updated as new information becomes available.

Regions that have decided not to introduce preferential treatment on their territory have the right to do so legally. In this case, entrepreneurs are deprived of the opportunity to apply a 0% rate, even if all conditions are met.

| Read and ask questions: What taxes does an individual entrepreneur pay on the simplified tax system? |

What laws are established

In 2021, a decision was made to extend tax holidays for small businesses until December 31, 2023. They have been used for individual entrepreneurs since 2015 and were introduced by Federal Law-477 of December 29, 2014. All subjects of the Russian Federation were authorized to independently decide on the introduction, set their own restrictions when applying a 0% rate and use their own in the region:

- income limit;

- indicator of the average number of employees for individual entrepreneurs;

- updated list of preferential OKVED classes.

IMPORTANT!

The following sections and classes will definitely not be included in the list of fiscal relaxations:

- G, 45–47 - wholesale trade;

- G, 46–47 - retail trade;

- F, 41–43 - construction;

- H, 49–53 - transportation and storage.

Please note that insurance premiums to extra-budgetary funds are paid as usual, payments to the Pension Fund and Social Insurance Fund are made in accordance with the established procedure. Currently, what tax holidays for individual entrepreneurs are in 2021 is enshrined in Federal Law No. 266 dated July 31, 2020.

How to support business during coronavirus

ConsultantPlus has collected all the current rules in one review: what is prohibited and what is allowed, whether it is mandatory to wear masks, what support measures are still in effect, and what monetary payments individuals and organizations can still receive. Convenient to keep track of changes. Free access for 2 days.

Accounting for income and expenses during tax holidays

Despite the tax rate being calculated at 0%, entrepreneurs are required to keep records of income and expenses in a special journal (KUDiR). According to Order of the Ministry of Finance No. 135n, a businessman reflects in this document the reliability, continuity and completeness of his activities. The tax base is determined from the accounting log, which in this case is necessary for calculating insurance premiums.

The advantages of KUDiR are obvious even during the grace period:

- the procedure for filling out the KUDiR involves the daily recording of monetary amounts, which is not directly related to the calculation of tax (for example, this helps to determine the revenue limits allowed for the simplified tax system);

- if KUDiR is absent from the workplace, the entrepreneur faces penalties of 10,000 rubles.

Data from KUDiR, first of all, is required by the entrepreneur himself.

Is it possible to save on insurance premiums?

Taxes carry a serious financial burden for any businessman. However, during the tax holiday for individual entrepreneurs for 2021 and subsequent years, insurance premiums will have to be paid. The benefit does not apply to them. This means that during the year you will have to make insurance contributions according to the same scheme as before. This applies equally to payments for yourself and employees.

The government explains this as follows: individual entrepreneurship is not only a way to make money, but also involves certain risks. In particular, employees of an enterprise should not lose contributions to the Pension Fund and other contributions if the employer temporarily works at a preferential rate.

Examples of calculations

Let's look at how to calculate tax for different types of activities.

Example 1

The individual entrepreneur is registered in a region in which tax holidays apply. “Simpler” chose “Income minus expenses” as the object of taxation, but is engaged in different types of activities. Some qualify for preferential treatment, others do not.

Based on the results of work for the calendar year, the profit amounted to 9,890,000 rubles. By type of activity, “net” income was distributed as follows:

- 7,500,500 rubles (preferential type of activity).

- 1,078,540 rubles.

- 1,310,960 rubles.

First, let's calculate the share of profit from preferential activities:

7,500,500 / 9,890,000 = 0.758. That is, 75.8%.

This figure exceeds the maximum norm of 70%, so the entrepreneur has the right to count on benefits. He does not calculate tax on the first type of activity, since the rate on it is 0%.

Example 2

An entrepreneur earned 10 million rubles during the tax period (calendar year). "net" profit. Of this, earnings from preferential activities amounted to 6,500,000 rubles.

Calculation of the percentage of profit on the benefit:

6,500,000 / 10,000,000 = 0.65 or 65%.

This is less than the established minimum, so the individual entrepreneur is not entitled to a 0% rate. The entrepreneur calculates the tax amount according to the standard tariff.

Need help with your taxes?

Don’t waste time, we will provide a free consultation and help with financial reporting for individual entrepreneurs.