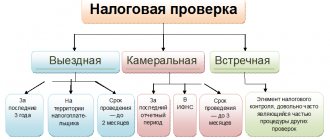

What is the procedure for conducting an on-site tax audit in 2017–2018

An on-site tax audit consists of the following stages:

- The decision by the head of the Federal Tax Service to conduct an on-site tax audit.

What this document is can be found in the publication .

- Implementation of measures to verify the compliance of accounting and tax records of the taxpayer with the norms of current legislation.

These actions are accompanied by:

- requesting the necessary documentation and explanations justifying a particular business transaction;

Details are in the articles:

- «What documents are tax authorities entitled to request during an on-site audit?»;

- «How tax authorities request clarifications from taxpayers».

However, in practice, the Federal Tax Service often requests documents that are not related to the subject of an on-site tax audit.

You will learn how to respond to such requests from the recommendations contained in the material “For an on-site inspection, the Federal Tax Service requires deciphering the accounting reporting lines. Should I comply with the requirement? .

- involving witnesses, specialists (including translators);

- inspection of premises; At the same time, it is possible that during the inspection tax authorities may conduct an inventory;

“The person being audited must assist tax authorities in taking inventory” will help to organize such a procedure correctly for the Federal Tax Service .

- carrying out examinations;

- seizure of documents.

- Completion of the procedure is accompanied by the preparation of a certificate that contains the substantive content of the on-site tax audit, as well as its period.

An example from judicial practice

I would like to confirm my thesis with reference to a specific arbitration dispute considered by the Arbitration Court of the Perm Territory, the Seventeenth Arbitration Court of Appeal, the Arbitration Court of the Ural District in case A50-36396/2019, where all three courts confirmed the legality of the actions of the tax authority, which handed the taxpayer a decision to conduct on-site tax audit one and a half months from the date of its issuance.

The factual circumstances of the case were that in the period from 09.09.2017 to 13.12.2018, the entrepreneur was registered for tax purposes with the territorial tax authority of the Perm Territory, and from 14.12.2018, due to a change of registration address, he was registered as tax accounting with a tax authority located on the territory of the Udmurt Republic.

On 02/05/2019, the entrepreneur receives by mail from the tax authority at the previous place of registration a decision to conduct an on-site tax audit, dated 12/13/2018, with which he does not agree, since, obviously, the tax authority at the previous place of registration made a decision not at all on December 13, 2018, but significantly later, putting on the decision a convenient date immediately preceding the day of changing the place of tax accounting, for the purposes of the possibility of conducting tax control.

In court, the tax authority referred to the lack of any contact information for the taxpayer, which made it impossible to issue a decision in a timely manner, but the taxpayer is an arbitration manager whose contact information is publicly available, and it is this tax authority that is the creditor of the debtors who are managed by the taxpayer. Therefore, the inspectorate employees know the taxpayer personally well, and even more so all his contact information.

However, the courts did not attach importance to these circumstances, pointing out only that, by virtue of paragraph 8 of Art. 89 of the Tax Code of the Russian Federation, the inspection begins on the day indicated in the decision to conduct it. The formal approach taken by the courts in a particular case led to the fact that the tax authority at the previous place of registration secured the right to conduct an audit, and also provided the opportunity to verify the tax obligations of the taxpayer for 2015.

Since if the decision was dated, for example, on the day when it was actually sent to the taxpayer (01/31/2019), then the inspection, by virtue of clause 4 of Art. 89 of the Tax Code of the Russian Federation would have the right to check a period not exceeding three calendar years preceding the year in which the decision to conduct the audit was made (that is, starting from 2016).

Consequently, the current content of Art. 89 of the Tax Code of the Russian Federation, which guides arbitration courts, indicating that there are no deadlines for serving decisions on conducting on-site inspections, leads to the fact that a situation may practically arise where tax authorities in 2021 can serve taxpayers with decisions on conducting on-site inspections, for example, for the period from 2014 -2016, dated any day of 2021, citing the fact that Art. 89 of the Tax Code of the Russian Federation does not contain a deadline for serving a decision, or even earlier periods should be subject to revision.

Thus, the uncertainty in Art. 89 of the Tax Code of the Russian Federation, the issue of the timing of delivery of decisions on conducting an on-site tax audit, legalizes potential abuses by tax officials when conducting on-site tax audits, makes tax control unlimited in terms of the depth of the audit period.

Of course, arbitration courts are formally right in applying the current content of Art. 89 of the Tax Code of the Russian Federation, however, it is difficult to call this approach fair, since in relation to the previous editions of Art. 89 of the Tax Code of the Russian Federation (before the adoption of clause 8 of Article 89 of the Tax Code of the Russian Federation) the Constitutional Court of the Russian Federation in clause 3.1. Resolution No. 14-P of July 16, 2004 explained that, within the meaning of Parts 1 and 7 of Art. 89 of the Tax Code of the Russian Federation in conjunction with paragraph 1 of Art. 91 of the Tax Code of the Russian Federation, the start date of an on-site tax audit is the date of presentation to the taxpayer (his representative) of the decision of the head (his deputy) of the tax authority to conduct an on-site tax audit.

Heading:

Tax audits

on-site tax audit of the Tax Code of the Russian Federation

- Alexander Trapeznikov, lawyer at Invest-audit LLC

Sign up 8645

12350 ₽

–30%

How is the period for conducting an on-site tax audit calculated?

The period for conducting an on-site tax audit usually varies from 2 to 6 months. This depends on the following factors:

- whether the company is one of the largest taxpayers;

- does it have separate divisions;

- whether the taxpayer violated the deadlines for submitting the requested information;

- other factors.

They are described in detail in this material .

Please note that an on-site tax audit may be suspended for up to 6 months (or up to 9 months in case of waiting for information from foreign authorities within the framework of international contracts). Such suspension is carried out by transferring the relevant decision to the person being inspected. From the moment the on-site tax audit is “frozen,” its period ceases to be calculated and tax authorities no longer have the right to:

- be with the taxpayer;

- request documents;

- inspect the premises;

- carry out other activities.

You will learn about what these events are from the publication “What is the deadline for conducting an on-site tax audit?” .

Please note: if the tax authorities made a demand and then suspended the audit, the obligation to submit documents remains with the taxpayer.

Our article “Suspending the inspection will not extend the period for submitting the requested documents” .

The number of such “freezes”, according to clause 9 of Art. 89 of the Tax Code of the Russian Federation, may be equal to the number of counterparties of the taxpayer being audited. At the same time, the deadlines continue to be calculated after the resumption of the on-site tax audit, which is accompanied by the adoption of an appropriate decision.

Grounds for conducting a tax audit

To conduct an on-site tax audit, there must be a basis, which is in accordance with Art. 89 of the Tax Code of the Russian Federation, the decision of the head of the tax authority or his deputy.

The following may serve as a reason for making the above inspection decision:

- if the tax burden of the person subject to inspection is below the average level in a particular area;

- if the organization operates with losses for several years in a row and reflects the corresponding losses in tax reporting;

- if the reporting indicates significant amounts of tax deductions for a particular period;

- if employees are paid a salary that is below the industry average in a constituent entity of the Russian Federation;

- if the taxpayer has been repeatedly deregistered and registered with the tax authorities, changing locations;

- if the taxpayer did not provide an explanation in response to a notification from the tax authorities about the identification of discrepancies in business performance indicators, or did not submit to the tax authorities the documents that were requested;

- for other reasons.

USEFUL: watch a video about appealing a tax decision and the participation of a lawyer in a tax audit. Subscribe to the YouTube channel to receive free advice on taxes and other issues through comments on videos:

How to appeal an on-site tax audit report

The completion of the on-site tax audit is evidenced by a certificate drawn up by the tax authorities. After its registration, inspectors have 2 months to draw up and submit an act (Clause 1 of Article 100 of the Tax Code of the Russian Federation), which indicates:

- date of;

- details of the person being checked;

- Full name of inspectors from the Federal Tax Service;

- number of the decision to conduct the inspection;

- documents submitted by the taxpayer;

- review period;

- other important information.

This is discussed in more detail in the material . Here you can also find a sample act.

After receiving the report, the taxpayer has the opportunity to appeal within a month. “Objections to an on-site tax audit report - sample” will tell you how best to do this .

After considering the objections, the Federal Tax Service Inspectorate within 10 days (according to paragraph 1 of Article 101 of the Tax Code of the Russian Federation, this period can be extended by 1 month) makes a decision on whether or not to hold the person being inspected accountable.

Tax audit procedure

- The decision to leave is made by the head of the tax authority, so you should pay attention to the details of this decision (who signed it? Which person checks it?). If the decision is not properly formalized, then we have a chance to appeal it in our favor.

- It should be remembered that the audit covers only the last three years of activity, so the tax office has no right to take a longer period, in addition, the tax office cannot come to you twice in a calendar year to check on the same taxes. In addition, the tax office’s departure is preceded by a request for documents, to which the taxpayer sends a response to the tax office’s request. The inspection period is no more than 2 months (in exceptional cases up to three months). The procedure for on-site tax audits should not be violated.

- Based on the results of the inspection, a report is drawn up. It must contain violations identified during the inspection, conclusions regarding these violations, and references to specific norms of the Tax Code of the Russian Federation. These points are important, since based on them a decision will be made that can be appealed.

- But the act itself can also be checked; the Tax Code of the Russian Federation gives a two-week period for submitting objections, which are considered in the presence of the taxpayer (violation of this procedure can also serve as grounds for canceling the decision). Based on the results of this procedure, an additional check may be ordered. Her appointment will indicate insufficient information to bring to justice.

Where can I get a plan for on-site tax audits for 2021?

The plan for on-site tax audits is annually posted on the Federal Tax Service website until December 31 of the year preceding the year of control activities. Therefore, 2021 has already shown who will face an on-site tax audit in 2021.

Taking into account clause 4 of Art. 89 of the Tax Code of the Russian Federation in 2021, tax authorities can conduct an on-site tax audit in relation to 2015, 2021, 2021. At the same time, the arbitrators admit that during an on-site tax audit, regulatory authorities have the right to request documents from the current year, i.e., in addition to the previously indicated years, you must be prepared to submit documentation relating to 2021.

Details are in our materials:

- “The RF Armed Forces recognized that an on-site inspection of the current calendar year is legal”;

- “Does the tax authority have the right to check the current year?”.

Blog about taxes by Vladimir Turov

Especially for the Financial Director magazine, legal tax specialist Natalya Bryleva described a step-by-step methodology for preparing for tax audits in 2021. What will tax officials look for during a tax audit in 2021? A checklist to help you prepare for business audits.

The priority directions of the tax policy of the Russian Federation for 2021 and the planning period of 2021 and 2021 are to prevent an increase in the tax burden and to simultaneously increase tax revenues to the budget. In this regard, tax audits will not only become less frequent - they will be comprehensive and meticulous. Moreover, inspectors now have even more tools for collecting reasons for conducting tax audits. So, what will tax authorities look for in 2021 during business tax audits?

Are all enterprises registered and registered with the funds?

The first thing they check during a tax audit is whether all enterprises are registered. If stamps, forms, or forms of non-existent companies are used, this will be qualified under Article 171 of the Criminal Code of the Russian Federation as “Illegal entrepreneurship”, the maximum penalty is 5 years in prison. From January 1, 2021, tax officials will take over the functions of monitoring the correct calculation and timely payment of insurance contributions to the Pension Fund of the Russian Federation, the Social Insurance Fund and the Federal Compulsory Medical Insurance Fund. Now such control will be carried out according to the general rules for conducting tax audits and regulated by the Tax Code of the Russian Federation. But periods that expired before 2021 will be checked according to the old rules by the Pension Fund of the Russian Federation and the Federal Social Insurance Fund of the Russian Federation. As part of on-site inspections, tax officials will check both the payment of taxes and insurance premiums. It is expected that insurance premium collections will increase due to the transfer of such powers to the Federal Tax Service, since tax authorities have long developed a method for collecting tax arrears, including through intimidation (see how to prepare for a tax audit).

Have you or your employees created “leftist” companies in the last ten years?

During a tax audit in 2021, there are risks of applying Article 173.1 “Illegal formation (creation, reorganization) of a legal entity” and 173.2 “Illegal use of documents for the formation (creation, reorganization) of a legal entity” of the Criminal Code of the Russian Federation. The maximum penalty under 173.1 is up to 5 years in prison.

During tax audits, inspectors will look for signs of cashing out through shell companies

Cash withdrawal, in addition to charges of tax evasion under Articles 198, 199, falls under Article 3 of Law 115-FZ. This is fraught with careful scrutiny for involvement in extremism and terrorist financing. And here they will probably begin to apply Articles 174 and 174.1 of the Criminal Code of the Russian Federation “Legalization of funds ... obtained by criminal means”, the maximum penalty is up to 7 years in prison. And here the tax authorities will be helped by the ASK VAT-2 system, which has already been in use for a year.

Please note that companies that are required to submit VAT returns in electronic form will be able to provide explanations to the tax authorities only in electronic form during a desk audit (clause 3 of Article 88 of the Tax Code of the Russian Federation). If explanations are provided on paper, they will not be considered submitted. Another mechanism for tax officials to take advantage of the inattention of businessmen and failures in computer technology to collect a fine for unlawful failure to report information to the tax authority in the absence of signs of a tax offense under Art. 126 of the Tax Code of the Russian Federation. Fine in the amount of 5 thousand rubles. recovered in case of failure to submit (untimely submission) explanations to the tax authority when the updated tax return is not submitted on time (clause 1 of Article 129.1 of the Tax Code of the Russian Federation).

In addition, now, if the taxpayer has not connected to electronic document management, banks are allowed to suspend an organization’s operations on its bank accounts and transfers of its electronic funds.

Are there any facts of artificially inflated purchase prices (inflated costs) of products (raw materials, materials)

It is difficult to detect artificially inflated purchase prices during the 2021 tax audit, but if the tax authorities succeed, the company will at least face liability under the Tax Code. The rest will depend on the amount of unpaid taxes. An increased tax penalty for non-payment of taxes as a result of the use of non-market prices between related parties begins to apply when checking controlled transactions only for tax periods starting from 2021 (more information about related parties in tax legal relations).

Are all your wages, the wages of your employees, and other income of you and your employees legal, and are taxes and insurance premiums paid on them in full?

A difficult violation to prove. Since when resolving cases of payment of envelope salaries to employees in court, arbitrators take into account only specific amounts of “gray” salaries, from which additional contributions can be calculated. If an employee says that his employer once paid him about 3,000 rubles. cash, then such testimony will not be accepted in court. However, tax authorities will try to bring the company to justice under Article 199.1 of the Criminal Code “Failure to fulfill the duty of a tax agent” with up to 6 years of imprisonment and, of course, arrears, penalties, and fines.

Illegal unlicensed programs

A favorite topic of operatives and investigators during tax audits both this year and in 2021. Article 146 of the Criminal Code – up to 6 years with a fine of half a million.

How to prepare for a tax audit 2021. Checklist

I advise businessmen to independently assess the risks of bringing their company to tax liability before a tax audit.

The minimum checklist should contain:

- Check the presence of folders and documents in them using the following blocks:

- bank documents;

- cash documents;

- contracts;

- personnel documents;

- general documents (constituent documents, rent, utilities, others);

- documents for fixed assets and intangible assets;

- Books and magazines.

- Take all bank statements.

- Take any bank statement for any day.

- Take any transaction shown on your bank statement.

- Request all documents for this operation. Go through the entire chain of movement of documents and money related to this operation: agreement, invoice, invoice, delivery notes, sales receipts, and so on - look at absolutely all the primary documents along this chain.

- If this was an operation for the purchase of office equipment, check the physical presence of office equipment, passports for it, invoices or sales receipts, invoices, invoices, commissioning certificates, accounting entries, depreciation, and so on.

- Then check the statements. I recommend checking your reporting to the state for the last three years.

- Make sure that the reports are physically available, that they are connected to each other, and that there are documents confirming payments to the state.

- Check other documents: move around the office from one workplace to another, take the first document you come across on the table, ask: “what is this?”, “Where should it be?”, and have the employee name it, put it in its place or throw it away trash can if not needed.

- Write down all the shortcomings so that you can later create a program to eliminate them. Additionally, invite an experienced accountant (not an auditor, there are reasons for this) and let him check the reporting and maintenance of registers.

Be sure to check that each enterprise (IP) you use in business meets the criteria of integrity and independence. Collect a basic package of documents to confirm the verification of the counterparty: request copies of constituent documents, passports of the company's top officials, seal impressions and sample signatures, etc.

By conducting a legal diagnosis of the company, you will be ready for a real tax audit in 2021 and at any time.

Especially for:

(Visited 114 times, 1 visits today)

Victor Khanzhin

PR specialist legal

Can an on-site audit be carried out on taxpayers who are not included in the audit plan?

Current legislation does not contain such a thing as an unscheduled on-site tax audit, although in practice this happens.

Let's consider the most common situations when the Federal Tax Service can conduct such an on-site tax audit:

- Liquidation or reorganization of a taxpayer. In this case, the verification period is also 3 years, which precede the year of the event.

- Carrying out a repeat inspection, the grounds for which are:

- decision of a higher tax authority - such an audit is carried out in order to control the activities of the subordinate Federal Tax Service;

- submitted updated declaration.

Read about the specifics of the inspection as part of submitting an update in the material “ When submitting a decreasing update, a repeated on-site inspection of periods “over 3 years” is possible . ”

- Upon receipt of information about a taxpayer’s violation of current legislation. However, such information can be obtained from individuals, organizations or law enforcement agencies.

Thus, on-site tax audits in 2017–2018 may not have been included in the Federal Tax Service’s plan, but in the presence of the above circumstances, they can still be carried out.

An on-site tax audit, taking into account the specifics of its implementation, is always a labor-intensive and lengthy process. What characterizes an on-site tax audit, what is the procedure for conducting it and other features of this control event, you can always find out from the publications in our “ On-site tax audit ” section.