Types of marriage

Depending on the location of detection of the defect and the nature of the detected defects, the defect is divided into the following categories:

- external: correctable and incorrigible;

- internal: correctable and incorrigible.

The reasons for defects (both internal and external) for a trade organization are:

- receipt of defective goods from the supplier (manufacturer);

- defects made during pre-sale preparation of goods (for example, during packaging and packing). In this case, goods actually become damaged. For more information about accounting for damaged goods, see How to record shortages (damage) of goods.

If a defective product was sold to a buyer, then the organization suffers losses from external defects. Accounting for losses from external defects depends on what kind of defect is identified - correctable or irreparable.

External correctable marriage

If a correctable defect is discovered, the buyer has the right:

- demand a proportionate reduction in the price of a low-quality product (i.e., discount it);

- return the goods to the seller;

- demand elimination of defects;

- independently eliminate the defects, while demanding compensation from the seller for the costs of eliminating the defect.

This follows from Articles 475 and 482 of the Civil Code of the Russian Federation, Law of February 7, 1992 No. 2300-1.

If the buyer demands that the defect be corrected, the seller can:

- transfer the goods for correction to the organization from which such goods were previously purchased;

- correct the defect on your own (with or without compensation from the supplier for low-quality goods);

- correct the defect with the involvement of service centers (third party organizations).

Elimination of defects by the manufacturer

If an organization transfers the goods to its supplier (manufacturer of goods) for correction, then it will not incur losses from defects. This is because all costs for correction will be borne by the supplier (manufacturer).

Situation: how to reflect in accounting the goods accepted from the buyer to correct a defect (defect)? The organization transfers these goods for repair (elimination of defects) to its supplier (manufacturer).

Goods accepted from the buyer and transferred to the supplier (manufacturer) to eliminate defects are reflected in off-balance sheet account 002.

This is explained as follows. Firstly, the buyer, when transferring the goods to the seller to eliminate defects, remains the owner of this product (Article 218 of the Civil Code of the Russian Federation). Secondly, the purchase and sale agreement was concluded between the trading organization and the buyer (Article 454 of the Civil Code of the Russian Federation). The trading organization that accepted the goods from the buyer remains responsible to the buyer for eliminating defects, as well as for the safety of the goods. A trading organization, as a seller, is obliged to deliver goods of proper quality (Article 469 of the Civil Code of the Russian Federation). In case of transfer of a low-quality product, it is responsible for its shortcomings (it must eliminate, reimburse the buyer’s expenses for elimination, replace the product, etc.) (Articles 475 and 476 of the Civil Code of the Russian Federation).

The supplier (manufacturer) and the trading organization are bound by another supply agreement. If the buyer of a trade organization transfers the goods for correction to this organization, and not to the manufacturer, then the manufacturer does not bear any obligations to the buyer of the trade organization. He is responsible only to the trading organization (since the contract is concluded between them). This follows from Article 476 of the Civil Code of the Russian Federation.

Therefore, reflect the goods transferred to the supplier (manufacturer) to correct the defect on account 002. Documentary confirmation of the fact of transfer of the goods to the supplier (manufacturer) can be an acceptance certificate. It will be possible to write off such goods from off-balance sheet account 002 only at the moment when the organization returns the goods to its buyer (Instructions for the chart of accounts).

For the convenience of maintaining analytical accounting and reflecting the movement of goods received to account 002, you can open additional sub-accounts:

- “Goods accepted for elimination of defects in warehouse”;

- “Goods transferred to the supplier (manufacturer, service center) to eliminate defects.”

Marriage in 1C. Working with defective goods in ERP, KA 2, UT 11. Customer complaints

Content:

1. How to write off defects in 1C and keep records of defects

2. Claims in 1C

1. How to write off defects in 1C and keep records of defects

At any trading enterprise, a situation may arise when a defective product is discovered, and you need to determine what to do with this product, and how to keep records of defects in 1C

. Let us highlight several situations that typical configurations of the solution “1C: ERP 2”, “1C: Trade Management 11” or “1C: Integrated Automation 2” help to solve:

· Return to supplier

· Return of customer goods -> return to supplier

· Return of goods from the client -> Write-off for own needs

· Registration of a claim -> Consideration of a claim -> Return of goods

· Return of goods from the client -> Change in quality -> Markdown

The operating mechanisms in the above configurations are identical. And this article will discuss examples of work in “1C: Trade Management 11”.

o Return of defects

to the supplier - when we find a defective product at the warehouse after receiving the goods, we call the client and issue a return. It can also be noted that if a defective product was discovered at the time of acceptance, then such a product can not be accepted at all, an act can be drawn up, given to the forwarder, and the product goes back to the supplier.

o The next moment when a defect was discovered in the client. Here it is necessary to determine the culprit of the marriage, because The customer could have damaged the product and tried to return the defective product. At another point, a marriage could arise through our fault. For example, the product was in good condition, but during the loading process our employees scratched (damaged) it, so at this point there is no fault of either the client or the supplier.

o The third option is the supplier’s fault. In this case, during the process of negotiating the claim, it is decided whose fault it is. And if the supplier’s fault is determined, the goods are returned from the client and then returned to the supplier.

o If it is determined that the fault of the damage to the goods is not the supplier’s, but ours, then we issue a return of the goods from the client, and write off the defect in 1C

for our own needs (for expenses), thereby reducing the overall profit of our activities.

o If it turns out that the product is partially substandard. For example, we sold a refrigerator and it was scratched during loading. Those. by itself, like a refrigerator works, but there is a scratch. We can sell such goods at a discount, at a reduced price. For such a sold product, it is necessary to issue a return of the product from the client, change the quality of the product and make a markdown (set a new price).

o The system has the ability to register the complete document flow for defective goods, starting from registering a customer complaint. Those. We register a complaint and note in it what the problem is. Next, we note the fact of consideration of the claim and the result. If we determine that it is our fault, we arrange for the return of the goods from the client, and then further along the chain return to the supplier, etc.

Claim documents are located in the CRM and Marketing section:

2. Claims in 1C

In the 1C:UT

It is possible to enter

claims

based on shipping documents, which is logical.

Let's use this method. Based on the existing implementation of the TV, we will enter a claim, i.e. Let's look at how to reflect a claim in 1C, and how calculations for 1C claims are carried out.

In 1C, a claim to a supplier or a client’s claim is registered in the initial status “Registered”. Next, information on the claim, description, classification by reason of occurrence, and the person responsible for receiving the claim are indicated.

Next, the guilty unit and employee are indicated, but this must be done after analysis and identification.

You can also add the supplier and some of his contact persons as participants to the claim.

Next, we move the claim to the next step, the status is “Processing”. Next “Satisfied” or “Dissatisfied”

The last statuses must indicate the result of the review. Otherwise, the program will generate an error and the claim will not be recorded in 1C.

Therefore, we indicate the text of the review, for example, claims from the buyer

Accordingly, the claim was sorted out and a manufacturing defect was identified. Now we can process the return of defective goods from the buyer in 1C. We will do this not directly, but according to the return application, i.e. First let's fix that there will be a refund

The application is generated in the status “To be returned”

And now we can enter the document “return of goods from the client”, the document is filled out based on the application

We process the document and change the application to completed status.

Now that we have received the goods from the client, we can issue a document in 1C “return of goods to the supplier”, for example, based on the document of receipt of this goods from the supplier

The main mechanisms for working and managing defective goods are considered.

Sergey Omelchuk, 1C programmer, head of the implementation department of Coderline LLC

Eliminating defects on your own

If the organization eliminates the defect on its own (for example, the contract does not provide for the elimination of the defect by the supplier), then losses from the defect will be equal to the amount of expenses associated with eliminating the defect. Namely:

- the cost of materials used to correct the defect;

- salaries of employees involved in eliminating defects;

- accruals on the salaries of employees involved in repairing marriages (contributions to compulsory pension (social, medical) insurance, as well as insurance against accidents and occupational diseases);

- costs of shipping defective goods for correction from the buyer and back;

- other expenses for correcting the defect.

Reflect these expenses in the debit of account 44 “Sales expenses”. This is due to the fact that in sales organizations all costs can be taken into account as part of sales expenses. When reflecting expenses associated with eliminating defects, make the following entry in accounting:

Debit 44 Credit 10 (60, 69, 70…)

– the costs of correcting the defect are reflected.

Goods accepted from the buyer for correction of defects during the entire period of work to eliminate defects are recorded in off-balance sheet account 002 “Inventory assets accepted for safekeeping.” This is explained by the fact that the goods transferred for correction are the property of the buyer and remain so even when they are with the trade organization to eliminate defects (Clause 1 of Article 223 of the Civil Code of the Russian Federation).

Capitalize the goods received to correct a defect on the basis of the documents issued by the buyer when transferring the goods for correction. This could be, for example, an invoice drawn up by the buyer in any form (or an invoice in form No. TORG-12). The use in this case of an independently developed primary document is explained by the fact that there is no unified form for reflecting such an operation. This procedure follows from Article 9 of the Law of December 6, 2011 No. 402-FZ.

In accounting, reflect the receipt of defective goods for correction and its return to the buyer after eliminating the defects with the following entries:

Debit 002

– goods were received from the buyer to correct the defect;

Credit 002

– the product is returned to the buyer, the defects of which have been eliminated.

This procedure follows from the Instructions for the chart of accounts.

Accounting in wholesale trade: postings

Here are the basic accounting records in trade organizations. We will show transactions in trade when conducting wholesale sales.

| Operation | Account debit | Account credit |

| Products purchased | 41 | 60 “Settlements with suppliers and contractors” |

| VAT on purchased goods is reflected | 19 “VAT on purchased assets” | 60 |

| Reflects intermediary services for the purchase of goods, delivery costs, customs duties | 41 | 60, 76 “Settlements with various debtors and creditors” |

| Revenue from the sale of goods is reflected | 62 “Settlements with buyers and customers” | 90 “Sales”, sub-account “Revenue” |

| VAT charged on goods sold | 90, subaccount “VAT” | 68 “Calculations for taxes and fees” |

| Cost of goods sold written off | 90, subaccount “Cost of sales” | 41 |

| Costs associated with the sale of goods are reflected | 44 “Sales expenses” | 60, 10 “Materials”, 70 “Settlements with personnel for wages”, 69 “Calculations for social insurance and security”, etc. |

| Expenses associated with the sale of goods are written off | 90, subaccount “Sales expenses” | 44 |

| Payment received from customers for goods sold | 51 “Currency accounts”, 52 “Currency accounts”, etc. | 62 |

| Profit from the sale of goods at the end of the month was revealed | 90, subaccount “Profit/loss from sales” | 99 "Profits and losses" |

When writing off a defect in trade, the postings will be the following, if the defect is discovered after the goods have been posted and it is not the supplier’s fault:

| Operation | Account debit | Account credit |

| Defective goods in warehouse detected | 94 “Shortages and losses from damage to valuables” | 41 |

| The loss of goods was written off within the limits of natural loss | 44 | 94 |

| Losses in excess of natural loss norms are written off (in the absence of culprits) | 91 “Other income and expenses”, subaccount “Other expenses” | 94 |

| Losses from defective goods are attributed to the perpetrators | 73 “Settlements with personnel for other operations” | 94 |

Elimination of defects by a third party

If an organization eliminates defects with the involvement of service centers (other third-party organizations), then reflect the cost of their services in expenses using the following entry:

Debit 44 Credit 60

– expenses for the services of the service center (other third-party organizations) are reflected.

This procedure follows from paragraph 1 of Article 475, Article 477 of the Civil Code of the Russian Federation and the Instructions for the chart of accounts.

In accounting, reflect the movement of goods received from the buyer and transferred to a service center (third-party organization) to eliminate defects in the same way as in the case of transfer of goods to the supplier (manufacturer).

The defect was eliminated by the buyer

The buyer, having purchased a defective product, can independently eliminate the defects so that the product is suitable for use. In this case, he has the right to demand compensation from the seller organization for the costs of correcting the defect. This is provided for by paragraph 1 of Article 475 of the Civil Code of the Russian Federation and paragraphs 1 and 2 of Article 18 of Law No. 2300-1 of February 7, 1992. It is these costs that will be taken into account by the seller as expenses for eliminating defects (i.e., increasing losses from defects). To take into account such costs, require the buyer to provide documents confirming the presence of a defect and the costs of eliminating it. For example it could be:

- marriage certificate;

- conclusion of the service center;

- calculation of expenses incurred.

As a rule, the buyer attaches such documents to the claim that he submits to the organization when a defect is discovered and corrected.

In this case, when reflecting the costs of eliminating defects in accounting, make the following entry:

Debit 44 Credit 76 subaccount “Calculations for claims”

– reflects the amount of compensation for the costs of eliminating the defect presented by the buyer.

In all cases, make entries in account 44 related to the reflection of expenses for correcting defects on the basis of:

- primary documents confirming the detected defect. These documents must be drawn up by the buyer at the time of discovery of the defect (damage) and then handed over to the trading organization;

- documents confirming the costs incurred to eliminate defects (damage) and compensation for damage from the perpetrators (suppliers, manufacturer) (invoices, pay slips, work completion certificates, etc.).

This procedure is provided for in Article 9 of the Law of December 6, 2011 No. 402-FZ.

Writing off defects in 1C 8.3: step-by-step instructions

If a defect is detected, the accountant can document:

- returning defective goods to the supplier;

- write-off of manufacturing defects.

From 2021, return goods to the supplier in 1C only through the Receipt Adjustment . the document Return of goods to supplier anymore.

Let's take a closer look at writing off manufacturing defects.

During the production of 500 pairs of women's shoes "Megan" women's sandals, 10 defective products were discovered. The marriage was declared irreparable, and the perpetrators were not found.

Costs for the production of women's sandals "Megan" amounted to 140,000 rubles.

The accounting policy for NU establishes that losses from defects are recognized as direct expenses.

Output

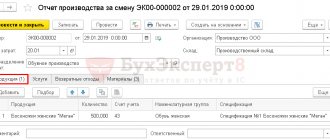

When registering product release and writing off materials, indicate material costs in full: for the entire production output, 500 pairs, including scrap.

But in the document Shift Production Report on the Products , indicate:

- Quantity - the number of products produced without defects.

- The planned amount (if you use it) is the total cost of production, taking into account defective products.

Writing off defects

Write off the defect using the document Transaction entered manually in the section Transactions - Accounting - Transactions entered manually.

In the document, indicate the posting:

- Dt of the account to which losses from defects are attributed, Kt,

and also fill out the analytics:

- Cost item - cost item with Expense Type NU Material costs ;

- Products - fill in only if you take into account product costs.

The cost of one unit of production can be determined based on the costs of account 20.

Cost of defective products = 140,000/500*10 = 2,800 rubles.

If costs are calculated without division by product, then take the total amount of costs by product group.

If losses from defects are recognized as direct expenses in the NU, then set the costs of correcting them in the settings of Methods for determining direct production costs in the NU section Main - Settings - Taxes and reports - Income Tax tab - link List of direct expenses.

If production output is accounted for at planned cost, then adjust the movements in the accumulation register Output of products and services at planned prices . To do this, check the box on the Accumulation registers and click the More button - Select registers.

In the movements indicate:

- Quantity - do not fill in, otherwise the cost calculation will incorrectly reflect the unit cost;

- Planned cost is the total planned cost of defective production.

After filling out this register at the end of the month, the costs of defects will be taken into account when calculating the cost.

If the planned cost price is not used, the posting Dt Kt 20.01 () is not generated when closing the month, and the account must be closed manually using the Transaction entered manually .

See also:

- Writing off materials in 1C 8.3: step-by-step instructions

- Cost calculation in 1C 8.3 Accounting 3.0

- Production accounting in 1C 8.3 Accounting

- Sales of finished products in 1C 8.3 Accounting 3.0

- Adjusting the implementation in 1C 8.3: step-by-step instructions

- Sales of goods and services in 1C 8.3: postings with examples

- Retail sales report in 1C 8.3: filling and postings

If you are a subscriber to the BukhExpert8: Rubricator 1C Accounting system, then read additional material on the topic:

- Product release options and their differences when calculating costs

- Release of finished products at planned prices using a new method: using the Products subconto. Materials are written off without specifications

- Release of finished products without planned prices using a new method: using the Products subconto. Materials are written off without specifications

- Release of finished products at planned prices using the old method: without using the Products subconto. Materials are written off according to specifications

If you haven't subscribed yet:

Activate demo access for free →

or

Subscribe to Rubricator →

After subscribing, you will have access to all materials on 1C Accounting, recordings of supporting broadcasts, and you will be able to ask any questions about 1C.

Did the article help?

Get another secret bonus and full access to the BukhExpert8 help system for 14 days free of charge

The supplier reimburses the costs

If the buyer returns a defective product, the trade organization may file a claim with its supplier for reimbursement of the costs of eliminating the defect (unless otherwise provided by the contract). This is explained by the fact that in relation to its supplier, the trading organization is the buyer. This means that she can present to the seller all claims related to inadequate quality of the goods, provided that the supplier is responsible for the defect, that is, the defect occurred before the goods were transferred to the trading organization. Such rules are established by Articles 475 and 476, paragraph 2 of Article 518 of the Civil Code of the Russian Federation. In this case, the trading organization does not experience losses from defects. The costs of eliminating defects reimbursed by the supplier (manufacturer of the goods) should be reflected by posting:

Debit 76 subaccount “Settlements on claims” Credit 44

– a claim was made to the supplier for compensation for losses due to defects.

How to write off a defective product from a buyer if the supplier refuses to accept it?

Our trade organization accepted a defective product from the buyer, but our supplier for some reason did not accept it. That is, this product is stuck in our warehouse

According to the norms of Russian legislation (clause 1 of Article 475 of the Civil Code of the Russian Federation), if the defects of the goods were not specified by the seller, the buyer to whom the goods of inadequate quality were transferred has the right, at his choice, to demand from the seller:

- A proportionate reduction in the purchase price;

- Free elimination of product defects within a reasonable time;

- Reimbursement of your expenses to eliminate product defects.

And in the event of a significant violation of the requirements for the quality of the goods, the buyer, on the basis of clause 2 of Art. 475 of the Civil Code of the Russian Federation also has the right to demand the replacement of goods of inadequate quality with goods that comply with the contract (clause 2 of Article 475, clause 1 of Article 476, clause 1 of Article 503 of the Civil Code of the Russian Federation, Article 12, clause 1 of Article 18 Law RF dated 02/07/1992 N 2300-1).

As follows from your comments, the retail trade did just that, completed all the necessary documents and returned the defective goods to the wholesale trade.

In turn, wholesale sellers have the right to make claims to their supplier - he is obliged to accept the defect and compensate for losses (i.e. return or offset funds against other supplies, as well as reimburse transportation costs, examination or disposal costs, if the agreement to dispose of or destroy the goods on site by the wholesaler).

Inspectors always pay attention to such moments during inspections. And if the organization received compensation for the defect, then the expenses do not raise questions for the tax authorities when checking the tax base for income tax.

If a defect was identified by the buyer of a product after its receipt, in order to document the fact of an external defect, the following must be received from the buyer:

- An act on identified defects in the quality of the goods, drawn up in any form, indicating all mandatory details in accordance with Part 2 of Art. 9 of Law N 402-FZ;

- Examination report (if necessary);

- A claim with requirements regarding defective products (return, replacement, discount) and with reference to a clause of the contract or a rule of law regarding the violation;

- An invoice for the release of materials to the party, in the “grounds” column of which should be written: “return of defects according to act N ___ dated ____.” In this case, the name of the product must be that which was indicated upon shipment to the buyer;

- An act of destruction of defective products, or documents confirming the costs of correcting the defect;

- Documents confirming transportation costs, etc.

If the supplier does not voluntarily agree to admit his guilt regarding defective products, then there is a judicial option. On the other hand, the Tax Code of the Russian Federation does not contain a direct condition for recognizing losses from defects in expenses only if there is compensation from the supplier (manufacturer) who is responsible for the defect (see, for example, paragraph 47, paragraph 1, Article 264 of the Tax Code of the Russian Federation).

In some cases, the Russian Ministry of Finance allows the recognition as expenses of costs associated with the disposal and destruction of goods that have become unusable due to the expiration of the shelf life for those goods, the taxpayer’s obligation to destroy or dispose of which is provided for by law (see, for example, the letter of the Ministry of Finance of the Russian Federation dated May 26 .2016 N 03-03-06/1/30409, dated September 15, 2011 N 03-03-06/1/553).

The Law “On Protection of Consumer Rights” does not provide for establishing an expiration date for shoes. Thus, the issue is controversial and contains tax risks.

Due to the ambiguity of tax consequences, it is advisable for an organization to distribute the defect, for which the supplier refused to reimburse expenses, into those subject to sale at a reduced price and subject to destruction. Selling defects at a reduced price will generate income, and documents for returning defects from retail will be the justification for the reduced price.

The assessment must be documented. The costs of destroying defective items unsuitable for sale can be economically justified by calculations confirming that this event provides savings on storage (i.e., economic benefits not only in generating income, but also in reducing costs - freeing up warehouse space, for example.) Such calculations will increase the organization’s chances of defending its position in a tax dispute.

In addition, an important circumstance is the proportionality of the costs of defects in the total cost of purchased shoes. The fact is that reject amounts exceeding “usual” amounts for the industry are an additional tax risk factor.

Losses from external irreparable marriage

If the buyer returns a product with an irreparable defect, the organization, in turn, can also return it to its supplier (manufacturer of the product). This is explained by the fact that in relation to its supplier, the organization is a buyer. This means that he has the right to make demands related to low-quality goods (Article 475 of the Civil Code of the Russian Federation). In this case, the organization does not experience losses from defects.

If the organization cannot return it to its supplier (Article 477 of the Civil Code of the Russian Federation), it has the right:

- discount this product and resell it in the future;

- use in your activities;

- write off (if the goods are not subject to further sale or use).

When calculating losses from external irreparable defects, determine the cost of the defective product as the cost at which the buyer returns it. It will be equal to the purchase price of the goods excluding VAT. This is explained by the fact that, as a rule, at the time of return the goods are already the property of the buyer, and therefore, when they are returned, a “reverse sale” occurs, where the buyer is the seller, and the seller is the buyer (Article 218, paragraph 1 of Article 223 Civil Code of the Russian Federation).

The cost of the returned (defective (damaged)) goods should be recorded on account 10 “Materials” or on account 41 “Goods”, depending on further use. So, if an organization wants to use defective goods in its own activities (for example, office supplies), then use count 10.

An irreparable marriage

Example 2

Upon receipt of the products at the warehouse, a manufacturing defect was discovered. The commission determined that the defect could not be corrected. It was decided to dismantle the defective products and produce new products.

Sequence of reflection in accounting (see Fig. 2):

- We draw up the “Product Release” document. In the “Quantity” column we indicate the total number of products produced, in the “Number of defective products” column - the number of defective products out of the total number of products produced. If only defective products were produced, then the values in the “Quantity” and “Quantity of defective products” columns should be equal.

- We draw up the document “Write-off of defective goods and materials”. The document indicates defective products that cannot be corrected. The cost of this product will be written off as losses from defects to account 28 “Defects in production”.

- We draw up the document “Capitalization of goods from defects in production.” In the document we indicate the materials at the price of possible use, which were received after disassembling the defective products. The indicated cost of materials will be written off from account 28 “Defects in production”.

- We draw up the “Product Release” document, in which we indicate the new products released.

Rice. 2

When posting the document “Closing the month”, the cost of defective products written off as losses from defects, minus the cost of materials obtained from defects in production, will be written off to account 20 “Main production” and taken into account in the cost of manufactured products for the current month. Sequence of reflection in accounting (see Fig. 2):

Debit 28 “Defects in production” Credit 43 “Finished products” - 2000 rubles. - writing off defective products as losses from defects Debit 10.1 “Raw materials and materials” Credit 28 “Defects in production” - 800 rubles. - capitalization of materials from defects in production at the price of possible use Debit 20 “Main production” Credit 28 “Defects in production” - 1200 rubles. - end of the month.

After all operations have been completed, account 28 “Defects in production” will be closed.

Markdown of goods

If you return a defective product, reflect it on account 41 (10) depending on further use.

Debit 41 (10) Credit 60 (76)

– defective goods were capitalized as part of the goods.

This procedure follows from the Instructions for the chart of accounts (accounts 10 and 41).

In this case, estimate the cost of the defective product as the cost at which the buyer returns it. It will be equal to the purchase price of the goods excluding VAT.

In the future, the organization can use the returned goods at its discretion (for example, sell or use in activities). If necessary, it is necessary to mark down (for example, for further sale) the cost of the returned goods due to defects.

Write-off of goods

A document for writing off goods can be created either from the “Warehouse” menu, indicating the inventory in its card, or from the inventory itself. We will use the second method, since it is more convenient.

On the document form “Inventory of goods”, in the “Create based on” menu, select “Write-off of goods”. If an excess of goods is detected in the warehouse, a posting is created, but this is not what our article is about.

The program will open the form of a new document, where everything is already filled out automatically. The tabular part includes only those rows for which a shortage was detected in the inventory. The accounting account was also set up automatically based on the settings of this item item (included in the item group “Materials”).

We won't change anything here. All data was filled in based on what we ourselves indicated in the inventory. Now you can post the document.

Let's look at the formed wiring. Here everything is filled out correctly. The goods were written off from account 10.01 “Raw materials and materials” to account 94 “Shortages and losses from damage to valuables”.

See also video instructions for writing off:

To account for defective inventories, the concept of “Quality” is used.

“Quality” in documents can take on two meanings:

- New - new MPZs

- Defect - defective MPZ

Defective materials are identified separately in both warehouse and batch accounting. The cost of writing off defective goods from the warehouse is calculated separately from the cost of writing off new ones.

To register transactions with defective inventories in a configuration depending on the business transaction, you can use the following documents (see table).

Name of business transaction

Document used to conduct a business transaction

Reimbursement of other expenses

If the organization, in addition to the cost of the defective (damaged) product, reimburses the buyer for other expenses (for example, transport), they should also be attributed to:

- to increase the actual cost of materials accepted for accounting if the returned goods will be used in the organization’s activities (clause 6 of PBU 5/01);

- sales expenses if the returned goods are resold after markdown (Instructions for the chart of accounts, clause 13 of PBU 5/01).

In all cases, make entries in the accounting accounts (accounts 10, 41, 44) based on:

- primary documents confirming the detected defect (damage) and the buyer’s costs, which are reimbursed by the organization (for example, invoices, claim certificate, etc.);

- primary documents confirming the attribution of losses from defects to the perpetrators (supplier, manufacturer) or the organization’s use of part of the defective goods (for example, a write-off act, an internal movement act, etc.).

These documents must contain the mandatory details specified in paragraph 2 of Article 9 of the Law of December 6, 2011 No. 402-FZ.

BASIC

When calculating income tax, losses from marriage are taken into account in full as part of other expenses (subclause 47, clause 1, article 264 of the Tax Code of the Russian Federation).

It does not matter at whose expense the defect is written off - the supplier (manufacturer) or the organization. Losses from a correctable defect will be equal to the cost of eliminating it, from an irreparable defect - the amount of the returned payment (excluding VAT), as well as the buyer's costs, which the organization reimburses in case of returning the goods.

If an organization uses the accrual method, take such losses into account in full when calculating income tax in the period to which they relate (Articles 272 and 318 of the Tax Code of the Russian Federation). For example, take into account the cost of materials transferred to eliminate repairable defects at the time of their transfer from the warehouse (i.e., at the time of filling out the demand invoice in Form No. M-11).

If an organization uses the cash method, all losses for which the conditions for their recognition during taxation are met will reduce the tax base for income tax (clause 3 of Article 273 of the Tax Code of the Russian Federation). For example, losses from a correctable defect, equal to the cost of purchased materials spent on its elimination, should be included in the tax base in the period in which these materials were used (subclause 1, clause 3, article 273 of the Tax Code of the Russian Federation). At the same time, they must be paid to the supplier (clause 3 of Article 273 of the Tax Code of the Russian Federation).

The cost of the goods returned by the buyer should be taken into account in the income of the period in which the return occurs (Article 250 of the Tax Code of the Russian Federation). Include in income the cost of the product at which it was accounted for on the date of sale (i.e., the amount of actual costs associated with its acquisition or creation). Accept the goods returned by the buyer for tax accounting at the same cost. In the future, the organization can use the returned goods at its own discretion (for example, sell or use in activities).

To learn how to take into account the costs of selling a product when calculating income tax if it was sold at a price significantly lower than the purchase price (for example, as a result of a defect), see How to record shortages (damage) of goods.

Amounts received from suppliers (manufacturers) through whose fault the defect occurred should be included in non-operating income (clause 3 of Article 250 of the Tax Code of the Russian Federation).

Under the cash method, recognize non-operating income at the time of receipt of money (to the cash register, to the current account) for damages (clause 2 of Article 273 of the Tax Code of the Russian Federation).

When using the accrual method, determine income as the amount of compensation for damage on the date it was recognized by the guilty party (for example, at the time when the supplier signed the claim made against him). If the organization seeks compensation for damage through the court, the date of recognition of income is the day the court decision enters into force. This is stated in subparagraph 4 of paragraph 4 of Article 271 of the Tax Code of the Russian Federation.

When returning a defective product, VAT previously charged to the buyer can be deducted.

An example of how losses from external correctable defects are reflected in accounting and when calculating income tax

LLC "Torgovaya" is engaged in the sale of furniture. The organization applies a general taxation system (accrual method). The organization pays income tax quarterly. The organization maintains accounting for purchased goods at purchase prices.

In March, Hermes sold a furniture set to a citizen in the amount of 236,000 rubles. (including VAT – 36,000 rubles). The cost of goods sold was 150,000 rubles. In April, the buyer discovered that some of the goods were defective (the covering of the wooden tables was uneven). The purchase price of the defective goods was RUB 70,800. (including VAT – 10,800 rubles). The buyer handed over the defective goods to Hermes to eliminate the defects (polishing and varnishing).

In the same month (April), the defect was eliminated by Hermes and the product was returned to the buyer. The cost of correcting it amounted to 25,300 rubles, including:

- cost of materials used (excluding VAT) – 8,000 rubles;

- salary (including salary accruals) of the employee who corrected the defect - 17,300 rubles.

In April, Hermes submitted demands to its supplier for reimbursement of costs to eliminate deficiencies. In the same month, the “Master” fully compensated for the losses from the marriage.

Postings were made in accounting.

In March:

Debit 62 Credit 90-1 – 236,000 rubles. – revenue from the sale of goods is reflected;

Debit 90-2 Credit 41 – 150,000 rub. – the cost of goods sold is taken into account in expenses;

Debit 90-3 Credit 68 subaccount “Calculations for VAT” – 36,000 rubles. – VAT has been charged.

In April:

Debit 002 – 70,800 rub. – goods were received from the buyer to correct the defect;

Debit 44 Credit 10 – 8000 rub. – the cost of materials used to correct the defect has been written off;

Debit 44 Credit 70 (69) – 17,300 rub. – the salary (including salary accruals) was accrued to the employee who corrected the marriage;

Debit 76 subaccount “Calculations for claims” Credit 44 – 25,300 rub. – expenses for correcting defects are attributed to the manufacturer of the goods;

Debit 51 Credit 76 subaccount “Settlements on claims” – 25,300 rubles. – losses from the marriage are compensated by the “Master”;

Loan 002 – 70,800 rub. – the corrected product is returned to the buyer.

When calculating income tax for the first half of the year, the accountant included in other expenses the cost of the correctable defect - 25,300 rubles, and reflected the amount of compensation in income - 25,300 rubles.

Write-off of defective goods

No production organization is insured against the appearance of defective products. Defects can be detected not only at the stage of production (internal defects), but also after shipment of finished products to customers (external defects). In this article we will consider what is called an external defect, the reasons for the occurrence of an external defect, its types, as well as the procedure for its reflection in the accounting and tax records of an organization.

External is a defect that is detected after the finished product has been shipped to the buyer. The reasons for the formation of external defects can be, for example, the use of low-quality raw materials, employee errors, technology deficiencies, and others. Clause 1 of Art. 475 of the Civil Code of the Russian Federation (hereinafter referred to as the Civil Code of the Russian Federation) it is established that if the defects of the goods were not specified by the seller, the buyer to whom the goods of inadequate quality were transferred has the right, at his own discretion, to demand from the seller: - a proportionate reduction in the purchase price; — free elimination of product defects within a reasonable time; - reimbursement of your expenses for eliminating defects in the goods. In the event of a significant violation of the requirements for the quality of the goods (detection of irreparable defects, defects that cannot be eliminated without disproportionate costs or time, or are identified repeatedly or appear again after their elimination, and other similar defects), the buyer has the right, at his choice: - to refuse execution of the purchase and sale agreement and demand the return of the amount of money paid for the goods; - demand the replacement of goods of inadequate quality with goods that comply with the contract (clause 2 of Article 475 of the Civil Code of the Russian Federation). External marriage, just like internal marriage, is divided into correctable and incorrigible. We will sequentially consider the procedure for its reflection in the accounting and tax accounting of the organization. The cost of irreparable external defects includes: - production cost of products (products) that were finally rejected by the consumer; - reimbursement to the buyer of expenses incurred in connection with the purchase of these products; — transportation costs for returning defective products; — other costs associated with the manufacture of defective products. To ensure that the return of products is not qualified as its resale to the manufacturing organization, it is important to correctly draw up documents confirming the nature of the transaction. According to paragraph 1 of Art. 9 of the Federal Law of December 6, 2011 N 402-FZ “On Accounting” (hereinafter referred to as Law N 402-FZ), each fact of the economic life of a commercial organization is subject to registration as a primary accounting document. Forms of primary documents can be developed by an economic entity independently, but they must be approved by the head of the organization upon the recommendation of the official responsible for accounting, and must contain the mandatory details established by clause 2 of Art. 9 of Law No. 402-FZ. A commercial organization has the right to use unified forms of primary documents, having approved their use in its accounting policies. As a unified document for identifying and returning defective products, you can use the TORG-2 form “Act on Identification of Defects” from the Album of unified forms of primary accounting documentation for recording trade operations, approved by Resolution of the State Statistics Committee of Russia dated December 25, 1998 N 132. To the act of If a defect is identified (form TORG-2), you must attach a claim that reflects the fact of delivery of low-quality products and indicates whether the supplier should transfer money to the buyer for defective products or pay off the debt incurred after the return of the defect by shipping similar products of proper quality. As a rule, external defects are detected not in the month when the products were manufactured, but later, when the rejected products are already included in the sales volume. In the event of returning defective products, the supplier must reverse accounting transactions for sales in the share attributable to the defect, including the amount of accrued taxes. The chart of accounts for accounting of financial and economic activities of organizations and the Instructions for its application, approved by Order of the Ministry of Finance of Russia dated October 31, 2000 N 94n, account 28 “Defects in production” is used to account for defects in production. It is intended to summarize information about losses from defects in production. In the debit of account 28 “Defects in production,” costs are collected for identified internal and external defects (cost of irreparable, that is, final, defects, costs of correction, etc.). The credit of account 28 “Defects in production” reflects the amounts attributable to reducing losses from defects (the cost of rejected products at the price of possible use, amounts to be withheld from those responsible for the defects, amounts to be recovered from suppliers for the supply of substandard materials or semi-finished products, as a result the use of which was defective, etc.), as well as amounts written off to production costs as losses from defects. Analytical accounting for account 28 “Defects in production” is carried out for individual divisions of the organization, types of products, expense items, causes and culprits of defects. The procedure for writing off external defects depends on the period when they were identified and on whether the organization creates a reserve for warranty repairs or not. If the organization has not created a reserve for warranty repairs, then losses from external defects are reflected as part of the costs of the month in which claims from customers are received and accepted. Losses from defects that relate to products manufactured in previous periods are included in the cost of similar products produced in the current period. If such products are not produced in the current period, then these costs are distributed by type of product as general production costs. Losses from defective products sold in previous periods must be included in non-operating expenses as losses from previous years identified in the reporting year. If an organization has created a reserve for warranty repairs, then the amount of losses from defects in accounting is written off against the reserve, regardless of when the defective products were sold. In the organization’s accounting records, this is reflected by the following entry: Debit account 96 “Reserves for future expenses” Credit account 28 “Defects in production” - the amount of losses from defects is written off from the reserve for warranty repairs. If the same reserve is created in tax accounting, then losses from marriage are also written off at its expense. When using the reserve, it should be taken into account that these funds are used to write off the costs of performing warranty work only within the warranty period. Note that the creation of a reserve for warranty repairs is typical for the shoe and fur industries, for industries producing consumer goods such as household appliances, watches, cars, small-scale mechanization, musical instruments, mechanical toys, hunting and sports weapons, and so on. .

Accounting for external correctable defects

The cost of external correctable defects includes: - costs of correcting defective products from the consumer; — transportation costs for transporting products from the buyer to the manufacturer and back; — other costs to reimburse the buyer’s expenses for purchasing products. In the event that the manufacturing organization corrects a detected defect and delivers products with corrected defects to the buyer, you should pay attention to the following: since the ownership of the specified products belongs not to the manufacturer, but to the buyer, the manufacturing organization, during the period for correcting the detected defects, must reflect it on off-balance sheet account 002 “Inventory assets in safekeeping.”

Example. The Omega LLC organization sold a batch of 10 products in March 2014. The selling price of one product is 11,800 rubles. (including VAT 18% - 1800 rubles). The cost of one product is 8,000 rubles. During the use of the products, the buyer discovered defects in three products; the defects can be eliminated. The manufacturer paid transportation costs for the delivery of defective products in the amount of 2,360 rubles. (including VAT 18% - 360 rubles). The cost of materials and parts used to correct the defect is 3,000 rubles. Workers' wages for correcting defects were accrued - 5,000 rubles. Insurance premiums charged - 1500 rubles. The amount presented for recovery from the culprits is 8,000 rubles. In the accounting records of Omega LLC, the specified business transactions will be reflected as follows using the following accounts and subaccounts: account 10 “Materials”; account 19 “VAT on purchased inventories”; account 20 “Main production”; account 28 “Defects in production”; account 43 “Finished products”; account 51 “Current accounts”; account 60 Settlements with suppliers and contractors; account 62 “Settlements with buyers and customers”; account 68-1 “Calculations for VAT”; account 69 “Calculations for social insurance and security”; account 70 “Settlements with personnel for wages”; account 73 “Settlements with personnel for other operations”; account 90-1 “Revenue”; account 90-2 “Cost of sales”; account 90-3 “Value added tax”; account 90-9 “Profit/loss from sales”; account 99 “Profits and losses”; off-balance sheet account 002 “Inventory assets in safekeeping.” Before the defect was discovered: Debit 62 Credit 90-1 - 118,000 rubles.

(RUB 11,800 x 10 products) - revenue from the sale of products is reflected; Debit 90-3 Credit 68-1 - 18,000 rubles. (RUB 1,800 x 10 products) — VAT added; Debit 90-2 Credit 43 - 80,000 rub. (RUB 8,000 x 10 products) - the cost of products sold is written off; Debit 90-9 Credit 99 - 20,000 rub. (118,000 rubles - 18,000 rubles - 80,000 rubles) - profit from the sale of products is reflected; Debit 51 Credit 62 - 118,000 rub. — payment received for sold products. After detecting a defect and filing a claim: Debit 60 Credit account 51 - 2360 rubles.

— transportation costs for the delivery of defective products from the buyer are paid; Debit 28 Credit 60 - 2000 rub. — transportation costs are included in losses from defects; Debit 19 Credit 60 - 360 rub. — VAT on transport costs is reflected; Debit 68-1 Credit 19 - 360 rub. - submitted for VAT deduction; Debit 002 - 30,000 rub. (RUB 10,000 x 3 products) - defective products are recorded on an off-balance sheet account; Debit 28 Credit 10 - 3000 rub. — the cost of materials and parts used to correct defective products has been written off; Debit 28 Credit 70 - 5000 rub. - wages were accrued for correcting the defect; Debit 28 Credit 69 - 1500 rub. — insurance premiums are calculated; Debit 73 Credit 28 - 8000 rub. - an amount has been presented for recovery from those responsible for the marriage; Debit 70 Credit 73 - 8000 rub. — the amount collected is withheld from wages; Debit 20 Credit 28 - 3500 rub. (2000 rubles + 3000 rubles + 5000 rubles + 1500 rubles - 8000 rubles) - losses from defects are included in the cost of production of the current period; Loan 002 - 30,000 rub. — corrected items are withdrawn from the off-balance sheet account. End of the example.

Tax accounting

When returning low-quality goods from the seller, the obligation to pay income tax arises only if the payer has an object of taxation. In accordance with Art. 38 of the Tax Code of the Russian Federation (hereinafter referred to as the Tax Code of the Russian Federation), the object of taxation is the sale of goods (work, services), property, profit, income, expense or other circumstance that has a cost, quantitative or physical characteristic, with the presence of which the legislation on taxes and fees relates the taxpayer becomes obligated to pay tax. According to paragraph 1 of Art. 39 of the Tax Code of the Russian Federation, the sale of goods (work, services) recognizes the transfer on a reimbursable basis of ownership of goods, the results of work performed, the provision of services, and in cases provided for by the Tax Code of the Russian Federation - also on a gratuitous basis. When returning low-quality goods, there is no object of taxation, since the parties return to their original position: the returned goods cannot be recognized as sold, since the buyer’s obligation to accept the goods is considered unfulfilled. In addition, there is no mandatory sales criterion - consideration of the transfer, since the amounts paid are returned to the buyer. In connection with the above, there is no obligation to pay taxes in accordance with paragraph 1 of Art. 248 of the Tax Code of the Russian Federation, in particular corporate income tax. However, at the time of sale of the goods, the seller still does not know whether the goods will be returned or not, therefore, on the basis of clause 1 of Art. 271 of the Tax Code of the Russian Federation (accrual method) recognizes the amount of income from the sale of goods in the reporting (tax) period in which it occurred. The amount of income from the sale of goods is entered by the seller into a special tax register “Income from the sale of goods.” At the same time, expenses associated with the sale of goods are recognized (Articles 268 and 272 of the Tax Code of the Russian Federation), reflected in the tax register “Cost of goods sold”. Chapter 25 of the Tax Code of the Russian Federation does not contain direct instructions on how to reflect the return of goods in tax accounting and how to take it into account when calculating the tax base for income tax. Tax accounting for the return of defective goods will depend on the period in which it is carried out. If the return of low-quality goods occurred in the same tax period as the sale, then the seller must reduce the amount of income from the sale calculated in accordance with Art. Art. 249 and 316 of the Tax Code of the Russian Federation, for the amount of the refund received by the seller for this product. And the amount of expenses of the current tax period should be reduced by the cost of the returned products. If the sale was made in one tax period (for example, in November 2013), and the defective products were returned by the buyer in another (for example, in April 2014), then the loss incurred due to the return of low-quality products can be included in non-operating expenses as losses from previous years identified in the current year, based on paragraphs. 1 item 2 art. 265 of the Tax Code of the Russian Federation (Letter of the Ministry of Finance of Russia dated June 3, 2010 N 03-03-06/1/378, Resolution of the Federal Antimonopoly Service of the West Siberian District dated January 24, 2007 N F04-9244/2006 (30394-A67-40) on case No. A67-4678/06). In addition, in tax accounting, losses from marriage based on paragraphs. 47 clause 1 art. 264 of the Tax Code of the Russian Federation are included in other expenses associated with production and sales. The specified expenses, in accordance with clause 2 of Art. 318 of the Tax Code of the Russian Federation are indirect and are taken into account as part of the expenses of the reporting period in full. At the same time, among other expenses associated with production and sales, taken into account for the purpose of determining the tax base for corporate income tax, taxpayers have the right to include only those losses from defects in production that are not subject to recovery (withholding) from those responsible for the defects, in compliance with the requirements of Art. . 252 of the Tax Code of the Russian Federation.

simplified tax system

If an organization applies a simplification and pays a single tax on the difference between income and expenses, expenses in the form of amounts of damage from an external irreparable defect do not reduce the tax base for the single tax. This is explained by the fact that such costs are not in the list of expenses that can be taken into account when calculating the single tax (clause 1 of Article 346.16 of the Tax Code of the Russian Federation). But take into account the costs of eliminating a correctable defect (material costs, salaries of employees involved in correcting the defect, etc.) when calculating the single tax in the general manner (clause 2 of Article 346.16 and Article 346.17 of the Tax Code of the Russian Federation). But only if they are provided for in paragraph 1 of Article 346.16 of the Tax Code of the Russian Federation (Clause 1 of Article 346.16 of the Tax Code of the Russian Federation).

If a simplified organization has chosen income as the object of taxation, do not take into account expenses in the form of losses from marriage when calculating the single tax. This is due to the fact that organizations that pay tax on income do not take into account any expenses at all when calculating the single tax. This follows from paragraph 1 of Article 346.18 of the Tax Code of the Russian Federation.

Regardless of the chosen object of taxation, take into account the cost of the goods returned by the buyer in the income of the period in which the return occurs (clause 1 of Article 346.15, Article 250 of the Tax Code of the Russian Federation). Include in income the cost of the product at which it was accounted for on the date of sale (i.e., the amount of actual costs associated with its acquisition or creation). Accept the goods returned by the buyer for accounting at the same cost. In the future, the organization can use the returned goods at its own discretion (for example, sell or use in activities).

The tax base of the single tax also increases the cost of defects, which are repaid by the supplier (manufacturer) (clause 1 of Article 346.15, clause 3 of Article 250 of the Tax Code of the Russian Federation).

In this case, include the amount of compensation for damage as income at the time the debt is repaid by the guilty party (clause 1 of Article 346.17 of the Tax Code of the Russian Federation).

Tax accounting of shortages of goods

According to the provisions of Art. 252 of the Tax Code of the Russian Federation, when determining the tax base for income tax, organizations reduce the income received by the amount of expenses incurred, with the exception of expenses not taken into account for tax purposes on the basis of Art. 270 Tax Code of the Russian Federation.

Expenses are recognized as justified and documented expenses (and in cases provided for in Article 265 of the Tax Code of the Russian Federation, losses) incurred (incurred) by the taxpayer.

Justified expenses mean economically justified expenses, the assessment of which is expressed in monetary form.

Documented expenses mean expenses supported by documents drawn up in accordance with the legislation of the Russian Federation.

Subclause 2, clause 7, art. 254 of the Tax Code of the Russian Federation provides that losses from shortages and (or) damage during storage and transportation of inventories within the limits of natural loss norms approved in the manner established by Decree of the Government of the Russian Federation of November 12, 2002 N 814 are equated to material costs.

However, if the identified shortage cannot be qualified as a natural loss of goods, the norms of paragraphs. 2 clause 7 art. 254 of the Tax Code of the Russian Federation do not apply (see also Resolution of the Ninth Arbitration Court of Appeal dated November 21, 2012 N 09AP-26757/12).

According to paragraphs. 5 p. 2 art. 265 of the Tax Code of the Russian Federation, losses received by a taxpayer in the reporting (tax) period in the form of a shortage of material assets in production and warehouses, at trading enterprises in the absence of perpetrators, as well as losses from theft, the perpetrators of which have not been identified, are equated to non-operating expenses. The fact that there are no guilty persons must be documented by an authorized government body (see letters from the Ministry of Finance of Russia dated December 16, 2011 N 03-03-06/4/149, dated August 3, 2011 N 03-03-06/1/448, dated June 20. 2011 N 03-03-06/1/365, dated 04/28/2010 N 03-03-06/1/300, dated 09/11/2007 N 03-03-06/1/658, resolution of the Seventeenth Arbitration Court of Appeal dated 18.01. 2012 N 17AP-13188/11).

At the same time, specialists from the financial department explain that the fact that the perpetrators are absent is confirmed by a copy of the resolution to suspend the preliminary investigation (clause 2 of Article 208, clause 13 of clause 2 of Article 42 of the Criminal Procedure Code of the Russian Federation).

The date of recognition of a loss from a shortage of material assets in the absence of perpetrators is the date the investigator issues the corresponding resolution (letter from the Ministry of Finance of Russia dated 03.08.2011 N 03-03-06/1/448, dated 20.06.2011 N 03-03-06/1/ 365, dated 08/27/2010 N 03-03-06/4/81, dated 06/08/2009 N 03-03-05/103, dated 05/02/2006 N 03-03-04/1/412, Ministry of Taxes of Russia dated 06/08. 2004 N 02-5-10/37).

Taking into account the position of the Ministry of Finance of Russia, it can be assumed that the tax authorities may not accept for tax purposes losses from a shortage of material assets in the absence of such a resolution, if the organization did not take any measures to identify the perpetrators (resolution of the Federal Antimonopoly Service of the Moscow District dated March 11, 2009 N KA- A40/1255-09).

If the organization did not contact the authorized government bodies regarding the fact of theft, then in order to avoid disputes with the tax authorities, it is advisable not to take into account the shortage of goods for profit tax purposes.

At the same time, there are examples of court decisions, according to which it is possible to confirm the absence of those responsible for the shortage with other documents containing the necessary information, in particular a certificate or letter from the Internal Affairs Directorate (resolutions of the Ninth Arbitration Court of Appeal dated July 3, 2012 N 09AP-15010/12, N 09AP-15430 /2012, FAS Moscow District dated November 9, 2007 N KA-A40/10001-07, FAS West Siberian District dated August 7, 2007 N F04-5161/2007(36812-A46-15)).

Therefore, if the organization did not contact the authorized government bodies regarding the fact of theft, then in order to avoid disputes with the tax authorities, it is advisable not to take into account the shortage of goods for profit tax purposes.

OSNO and UTII

As a rule, it is always possible to determine which type of activity the losses from marriage relate to. Therefore, if an organization applies a general taxation system and pays UTII, losses from defective products used in activities transferred to UTII and activities on the general taxation system must be taken into account separately for income tax and VAT (clause 9, article 274, clause 4 Article 170 of the Tax Code of the Russian Federation).

Losses from marriage, which relate to activities on the general taxation system, will increase other income tax expenses (subclause 47, clause 1, article 264 of the Tax Code of the Russian Federation). Do not take into account losses from marriage that relate to activities on UTII for tax purposes (clause 1 of Article 346.29 of the Tax Code of the Russian Federation).