Is it possible to charge penalties on penalties?

This article describes in detail whether it is possible to charge penalties on penalties, and everything you need to know about it. In Russia, many people have debts for utilities, loans, and fines. If they are not paid on time, a person may end up in a debt trap associated with the accrual of fines and penalties on the principal debt. To understand the legality of accruing these penalties to the debtor, it is necessary to fully understand this issue, study the civil code of the Russian Federation, as well as the relevant government regulations.

Rules for calculating penalties

The existing debt of a citizen of the Russian Federation is constantly increasing due to fines and penalties accrued to him. Is this legal? This question is relevant at all times. The rules for calculating penalties are stipulated in government decree number 1063, adopted in 2013. It talks about all the rules for calculating fines and penalties for failure to fulfill their financial obligations by the performer, recipient or organizer of services.

The amount of fines and penalties must be specified in the contract for the supply of services. If there is no such item, then they are calculated in accordance with government decree number 1063.

In accordance with it, the fine is calculated as follows:

- If the cost of the services provided is less than three million rubles, then the fine should be set at ten percent of the principal debt;

- If the cost of the services provided is more than 3 million rubles and borders on fifty million rubles, then the amount of the fine should be set at five percent of the principal debt;

- If the cost of the services provided is between fifty and one hundred million rubles, then the amount of the fine should be set at one percent of the principal debt;

- If the cost of the services provided is more than one hundred million rubles, then the fine should be set at half of one percent of the principal debt.

These fine rules apply throughout the Russian Federation. The amount of accrued penalties is also established by this provision. They are formed as follows:

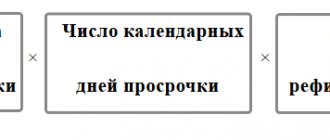

It is necessary to know the cost of services provided by the supplier, as well as the amount paid by the purchaser of services. In addition, you need to know the rate at which penalties are calculated. It is also not difficult to calculate; for this you need to know the refinancing rate of the central bank of the Russian Federation, as well as the total delay in days. Also, to determine how penalties should be calculated, for each day or for a certain period of time, you need to calculate the coefficient.

The bet size is calculated using the following formula:

- Rate = Cst * efficiency, where Cst is the rate of the central bank of the Russian Federation, and efficiency is the total number of days of delay.

- The amount of interest accrued is calculated according to the following formula:

Penalty = (C - IO)* Rate, where C is the entire amount payable, IO is the fulfillment of the obligation under the contract, Rate is the rate calculated above.

To determine the coefficient, you need to refer to the formula:

- Coefficient = (Days of delay/fulfillment of obligations) * 100%.

Penalties are calculated for each day of delay in the amount of:

- 0.01 refinancing rate if the coefficient is 0 and below 50;

- 0.02 refinancing rate if the coefficient is from 50 to one hundred;

- 0.03 refinancing rate if the coefficient is more than one hundred.

In what cases can penalties be avoided?

The accrual of penalties cannot be avoided. In any case, they will be charged on the principal amount of the debt. But it should be noted that penalties cannot be accrued on penalties under any circumstances.

In accordance with Article 404 of the Civil Code of the Russian Federation, the amount of the fine can be reduced in the following cases:

- If the debt occurred due to the fault of both parties to the contract;

- If the service provider intentionally increased the debt, which does not comply with legal requirements.

Also, in accordance with Article 333 of the Civil Code of the Russian Federation, the amount of penalties can be reduced:

- If the amount of the penalty is greater than or equal to the amount of the entire debt;

- If the claimant, with the help of these penalties, can obtain an unjustified benefit;

In accordance with the Civil Code of the Russian Federation, and in particular with Article 394, the amount of the penalty can be reduced if this is provided for in the contract, or the contract provides for the payment of only the debt or only the penalty.

To avoid falling into debt, you must make all payments on time. If the law does not provide for the accrual of penalties on penalties, then there is a law that allows the service provider to increase the amount of debt through fines and penalties for each day of delay. The debtor should begin paying the principal immediately. You can always agree with the creditor on the possibility of installments and suspension of the accrual of penalties. Therefore, there is no need to be afraid of him, but you need to make contact with him.

In this article, you learned whether it is possible to charge penalties on penalties. If you have any questions or problems that require the participation of lawyers, then you can seek help from the specialists of the Sherlock information and legal portal. Just leave a request on our website and our lawyers will call you back.

Editor: Igor Reshetov

Contradictions in Resolution No. 424. How to still charge penalties in 2021?

On April 6, government decree No. 424 of 04/02/2020 was published. It suspended until January 1, 2021 the operation of a number of provisions of PP No. 354, contracts for the supply of utility resources, management contracts related to the decommissioning of the IPU, the limitation of utilities, the accrual and collection of penalties.

04/27/2020 Everything is clear with the limitation of services: in case of incomplete and late payment, utility services cannot be turned off or limited to debtors.

Regarding the verification of the IPU, everything is also clear: after the expiration of the verification interval, the consumer may not carry out verification of the IPU. He must do this before January 1, 2021. Until this moment, all accruals must continue to be made based on the fact that the IPU is in effect. But with penalties, it turns out, not everything is so simple.

This week it is necessary to close the billing period and deliver payment documents to consumers, but many still do not understand how to deal with penalties.

The following questions arise:

1. What to do with the fact that PP No. 424 contradicts paragraph 14 of Art. 155 Housing Code of the Russian Federation? 2. Is it possible to charge penalties for housing services during the moratorium period? 3. What to do with unpaid penalties as of April 6, 2021? 4. What to do with penalties for the moratorium period after its end if the consumer remains a debtor?

Let's deal with them.

What to do with the fact that PP No. 424 contradicts paragraph 14 of Art. 155 Housing Code of the Russian Federation?

PP No. 424 prohibits the contractor from demanding payment of a fine, and removes the obligation from the consumer to pay it. However, paragraph 14 of Art. 155 of the Housing Code of the Russian Federation, according to which debtors are obliged to pay penalties, has not been canceled. It turns out that the government decree contradicts the Housing Code, which is higher in the hierarchy of regulatory legal acts than the government decree. Formally, we are obliged to work according to the Housing Code of the Russian Federation. The resolution is the only way to quickly take the necessary measures. So, it is worthwhile to implement PP No. 424 despite the contradiction, because if you continue to accrue penalties during the moratorium period, there is a high probability of losing the case in the future: most likely, the courts themselves will be given the “correct” explanation of how to act in such situations.

Is it possible to charge penalties for housing services during the moratorium period?

If you carefully analyze PP No. 424, you will notice that clause 1 concerns the prohibition of the requirement to pay penalties only for utilities: the corresponding paragraphs of PP No. 354 are suspended. There is no talk about housing services in these paragraphs. Penalties for housing services are reflected in clauses 4 and 5 of PP No. 424. But they prohibit collecting a penalty, that is, forcing someone to pay, receiving it from someone by force, but it is not prohibited to charge and offer to pay. It would seem that this allows us to continue to charge penalties for housing services. But it is unlikely that this game with definitions will pass in court, since it is obvious that such a position does not correspond to the actual meaning of PP No. 424. Perhaps this omission with the terms in PP No. 424 is, again, due to the haste in its adoption. It will likely be amended accordingly soon. So, there is also no need to charge a penalty for housing services.

What to do with unpaid penalties as of April 6, 2020?

PP No. 424 prohibits during the moratorium period from demanding payment of penalties, regardless of the period for which they were accrued. If we interpret the resolution literally, then it is also impossible to demand a penalty for previous periods (before April 6, 2020). It must be excluded from the total amount payable. But at the same time, I recommend that you still leave the information about the amount of the penalty on the payment document with a note like “Fine as of 04/06/2020 (for reference)”, as a reminder to debtors that the penalty has not been written off, but simply the due date for its payment has been postponed. It will be possible to return this penalty to the amount payable after January 1, 2021, that is, in payment documents for December 2021. There is an option to continue to issue the penalty for payment on April 6, 2021, citing the fact that it was formed for the period before the moratorium. This will prevent debtors from relaxing too much. But in this case, you should accept the risk of inspections by supervisory authorities and be prepared to defend your position in court.

What to do with penalties for the moratorium period after its end if the consumer remains a debtor?

Despite the moratorium on penalties, the consumer remains obligated to pay utility bills on time. Whoever does not do this will be a violator. PP No. 424 only exempts violators from punishment in the period until January 1, 2021, but does not justify the violation. That is, the violator remains a violator. But it is not clear from the resolution whether after January 1, 2021, it will be possible to “remember” the facts of violations committed during the moratorium period. There are three options for how the resolution in this part can be interpreted.

Penalties for violations committed during the moratorium period after January 1, 2021: 1. Cannot be accrued under any circumstances; 2. Charges can be made only if, as of January 1, 2021, the consumer is still a violator (debtor); 3. You can accrue in any case - in fact, there were violations.

When adopting the resolution, the Government of the Russian Federation most likely had in mind an interpretation similar to the first paragraph. But if we interpret the resolution literally, we get the third paragraph, which means that after January 1, 2021, it will be possible to “remember” everything and charge a penalty for late payment during the moratorium period. However, such an interpretation is unlikely to pass in the courts. There will probably be a public clarification later. Or, closed explanations will be given within the judicial system regarding the fact of the trials in 2021. But interpretation No. 2 looks quite viable and has a high chance of being accepted by the courts.

Thus, if a consumer actually committed violations during the moratorium period, but paid off all debts as of January 1, 2021, then he cannot be charged a penalty for the moratorium period. If the consumer remains a debtor as of January 1, 2021, then in the payment document for December 2020 it is advisable to charge him a penalty for the moratorium period for the amount of debt outstanding as of 01/01/2021.

Later, if the courts still do not accept this position (it will be necessary to observe actual judicial practice), it will be possible to recalculate based on interpretation No. 1. But for now it is better to adhere to the second interpretation in order to prevent a critical drop in the level of payment collection.

In order to maintain payment discipline among consumers, I propose to rely on interpretation No. 2 and convey it to consumers.

Here’s what your message to consumers might look like:

“Please note that Government Decree No. 424 of 04/02/2020 did not relieve consumers of housing and communal services from the obligation to pay in full and on time, but only postponed the calculation of penalties until January 1, 2021. In order for us to fulfill our obligations to you, we ask you to pay the issued payment documents on time. This can be done using numerous contactless and remote payment methods. This way you will not violate the self-isolation regime. Those who do not pay for services on time and in full will be charged a penalty on January 1, 2021 for violations of deadlines and complete payment for the entire established period.”

If your organization is a user of Kvartplata 24 services, then we have already done the following:

1. The dates for verification of IPU falling during the moratorium period have been changed to 01/01/2021. The original verification date is available for viewing in the field of the same name. If the consumer does not verify by 01/01/2021, then we will return the original verification date to the IPU and it will automatically be recalculated for the period after the decommissioning date. 2. The penalty as of 04/06/2020 is excluded from the amount payable, but is given in the PD for reference. The amount payable is also transferred to online payment collectors without taking into account any penalties. The penalty for 04/06/2020 will be returned to the amount due from 01/01/2021 in payment documents for December 2021. 3. For the period from 04/06/2020 to 01/01/2021, the “Period without penalty” property is set. From 01/01/2021, all debtors will automatically be charged a penalty for the moratorium period for the amount of debt outstanding as of 01/01/2021.

If you have questions about these settings, or you adhere to other interpretations of PP No. 424, then contact our expert support service and we will offer you other available options.

We know that the energy community is currently negotiating with the Government, and we are likely to expect clarifications or changes in PP No. 424. We’ll find out which ones specifically soon.

ASK A QUESTION

Share

What formula can you use to calculate tax penalties?

To calculate penalties for late transfers of payments to the budget, you must use the following formula:

Penalties = Amount of arrears × Number of days of delay × 1/300 of the refinancing rate

When calculating penalties for payment, the accountant in this formula must use the actual values of the refinancing rate that were in effect during the period of late payment of taxes (clause 4 of Article 75 of the Tax Code of the Russian Federation). That is, if the refinancing rate changes during this period, you need to calculate penalties separately for the periods of validity of each refinancing rate, and then add up the resulting amounts.

Until October 1, 2017, this calculation formula was used by all taxpayers without reference to the length of the period of delay.

But from October 1, 2017, for legal entities that allow a delay in payment for a period of more than 30 calendar days, this calculation has changed. The change applies to a period of delay beyond 30 calendar days, concerns arrears that arose only after September 30, 2017, and is expressed in doubling the amount used in the calculation of the rate (subclause “b”, clause 13, article 1, clause 9, art. 13 of the Law “On Amendments...” dated November 30, 2016 No. 401-FZ). That is, the calculation formula additionally used in the event of a long delay in payment by legal entities looks like this:

Penalties = Amount of arrears × Number of days of delay × 1/150 of the refinancing rate.

If tax authorities decide to round up the interest rate for accrual of penalties, for example, to whole values, which will lead to an increase in payment, then such actions of inspectors can be appealed either to a higher tax authority or in court (Article 137, paragraph 1 of Article 138 of the Tax Code of the Russian Federation) . Moreover, the courts often take the side of taxpayers, as, for example, in the resolution of the Federal Antimonopoly Service of the North-Western District dated November 9, 2005 No. A42-5178/04-29 or the resolution of the 14th Arbitration Court of Appeal dated January 21, 2011 No. A05-9658/2010. This is due to the fact that the text of Art. 75 of the Tax Code of the Russian Federation does not provide for rounding of interest rates.

To calculate penalties, we recommend that you use our Penalty Calculator service.

Calculation of the amount of penalties

Of course, penalties can be calculated in a couple of minutes using special calculators, of which there are many on the Internet. However, it is still necessary to know the basic calculation rules and formulas.

The following indicators are used to calculate penalties :

- the amount of unpaid tax or fee on which they are accrued;

- billing period, that is, the number of days of accrual;

- key rate of the Central Bank of the Russian Federation (currently the refinancing rate).

Note! If during the period of delay the rate of the Central Bank of the Russian Federation changed, this must be taken into account.

The calculation formula will be different for individual entrepreneurs and organizations.

Calculation for the company

For the first 30 days of delay, penalties are calculated using the formula:

Amount of arrears * (Key rate of the Central Bank of the Russian Federation / 300) * 30

Starting from the 31st day of delay, the following formula applies:

Amount of arrears * (Key rate of the Central Bank of the Russian Federation / 150) * Number of days of delay from 31 days

The resulting values are then added together.

Example. Romashka LLC had to pay tax in the amount of 30,000 rubles by April 25, 2018. However, in fact, the debt was repaid only on August 1. Let's calculate the penalties.

The total period of delay, taking into account the date of payment, is 98 days . During this time, the rate of the Central Bank of the Russian Federation was 7.25% and did not change.

For the first 30 days of delay, penalties will be: 30,000 * 30 * 7.25% / 300 = 217.50 rubles.

For the period from the 31st to the 98th day of delay, that is, 68 days, penalties will be: 30,000 * 68 * 7.25% / 150 = 986 rubles.

The total amount of the penalty is: 217.50 + 986 = 1203.50 rubles.

Note! The current procedure for calculating penalties for organizations (with an increase in the rate from the 31st day of delay) applies to arrears that arose after October 1, 2017 . If an underpayment is revealed that arose before this date, then penalties are calculated in the same way as for entrepreneurs.

Calculation for individual entrepreneurs

For individual entrepreneurs, penalties are calculated regardless of the period of delay according to the formula:

Amount of arrears * (Key rate of the Central Bank of the Russian Federation / 300) * Number of days of delay

If we assume that in the example above the person involved is not a company, but an individual entrepreneur, then the amount of penalties will change: 30,000 * 98 * 7.25% / 300 = 710.50 rubles.

Results

Calculation of penalties for taxes is done according to the formula given in paragraph 4 of Art. 75 of the Tax Code of the Russian Federation. It involves the amount of tax not paid on time, the number of days of delay and the rate, determined as a share of the refinancing rate in force during the period of delay. This share in the general case is 1/300. From 10/01/2017, for legal entities that allow a delay of more than 30 calendar days, another value of this share is applied - 1/150.

The need to calculate penalties for tax payments arises when accrued amounts of taxes, as well as mandatory insurance payments to the state treasury, are paid later than the deadlines established in the relevant legislation.

It is important to know that the payment of taxes and contributions is considered completed only after presenting the corresponding order to the bank. It confirms the transfer of funds to the state treasury account.

At the same time, there must be a sufficient balance in the bank account of the person who submits the order at the time of making the payment. If all these criteria are not met, then additional, mandatory payments in the form of penalties are charged.

What is a tax penalty?

The definition of penalties is provided in the Tax Code of the Russian Federation. Penalty – represents the amount of money that the payer is obliged to pay in the event that fees and taxes were repaid by him later than within the time limits established by law.

The penalty must be paid in addition to the tax amount, and is calculated daily throughout the period of late payment. It begins to accrue immediately after the expiration of the tax or insurance payment period.

There is only one exception for the unified agricultural tax, for which the penalty is calculated in accordance with Chapter 26.1 of the Tax Code of the Russian Federation.

Penalties also play the role of a government instrument that ensures timely payment of taxes and fees. Because its accrual stops only on the day when the overdue payment was repaid. It is always calculated as a percentage of the unpaid amount for one type of payment.

The tightening of penalties for late payment of taxes in 2021 is described in the following video:

For what period is the penalty accrued?

Part 3 of Article 75 of the Tax Code:

3. A fine is accrued for each calendar day of delay in fulfilling the obligation to pay tax, starting from the day following the tax payment established by the legislation on taxes and fees, unless otherwise provided by this article and Chapters 25 and 261 of this Code.

A penalty is charged for each day of delay.

For example, if the transport tax for 2021 was paid on December 5, 2017, then the penalty will be charged within 4 days, because payment deadline is December 1.

Accrual of penalties

The accrual and calculation of tax penalties is regulated by the state Tax Code.

There are several main reasons for charging penalties:

- the most common is when the taxpayer did not pay the monetary obligation within the prescribed period;

- when the tax control authority has identified an understatement of the tax payment amount;

- there is a circumstance when the accrual of penalties may apply to the tax agent if he transferred the amount of the payer’s tax payment later than the required deadlines (that is, when the delay occurred due to the fault of tax inspectors);

- The accrual of penalties can be carried out not only on the market within the state, but also on transactions of import and export of goods across the border (customs duty).

There are also cases when a tax penalty is not charged:

- is not accrued on the amounts of arrears incurred by the payer of taxes and fees, due to his provision of explanations in writing about the procedure for accrual and payment of payments, or due to his solution of other tasks related to the current legislation of the Tax Code of the Russian Federation, given to the payer by the local tax authority. In order for such circumstances to be taken into account when deciding on the calculation of penalties, they must be confirmed by an appropriate document. It can be obtained from the tax office. The above exception also applies to tax agents (when they are obligated to pay a fine, this clause may exempt them from payment);

- if the taxpayer has an overpayment for the relevant types of payments;

- if the amount of the overpayment completely covers the penalty;

- is not accrued in full if the amount of overpayments is less than the amount of arrears by type of tax, in which case the penalty is reduced in proportion to the amount of the missing arrears.

Overpayment is money that includes surpluses resulting from the payment of taxes, penalties, and fines. It can be used to pay off debts if the following conditions are met:

- the overpayment is transferred to cover the arrears by the tax authorities;

- transfer of overpayments can only be carried out to pay off local, regional and federal taxes.

The Supreme Court clarified when penalties for one tax are not accrued if there is an overpayment for another

The Supreme Court published Ruling No. 305-ES20-2879 of November 23 in the case of a taxpayer challenging the tax inspectorate’s demand to pay VAT penalties in the event of an overpayment of income tax.

In July 2021, Borets LLC submitted to the MIFTS for the largest taxpayers No. 2 an updated income tax return for the first half of the year, which stated the amount of tax to be reduced in the amount of 328 million rubles. A month later, the tax authority received an application from the company to offset the overpaid income tax against upcoming VAT payments in the amount of 150 million rubles. Subsequently, the company submitted a VAT return for the third quarter of 2021 with the amount of tax payable in the amount of 89 million rubles.

After conducting a desk audit on income tax, the tax office confirmed the presence of an overpayment. Based on the application submitted by the payer, the tax authorities decided to offset the overpayment of income tax in the amount of 150 million rubles. against current VAT payments. The test took place on October 29. At the same time, since the tax accrued according to the VAT return for the third quarter of 2018 is in the amount of 89 million rubles. was not paid on time by October 25, the inspection assessed penalties for late payment for the period of delay from October 26 to October 28 in the amount of over 66 thousand rubles.

Since the Federal Tax Service in Moscow did not satisfy the taxpayer’s complaint about the actions of the inspectorate in calculating penalties and the demand made, the company challenged it in the arbitration court.

Three authorities refused to satisfy the applicant’s demands, agreeing with the additional accrual of the disputed VAT penalties for the period when the deadline established by law for paying the tax had expired, but the decision to offset the overpayment generated by another tax had not yet been made. They noted that the tax inspectorate could confirm the formation of an overpayment of income tax only after the end of the audit or the expiration of the period for its conduct (in the case under consideration - October 26, 2021), and the decision to offset the overpayment had to be made within 10 days after the expiration such a period. The courts added that the decision to offset the confirmed overpayment of income tax against current VAT payments in the amount of 150 million rubles. was issued by the inspection on October 29, 2021, i.e. within 10 working days after the expiration of the desk audit period.

In its cassation appeal to the Supreme Court, the company referred to significant violations of substantive and procedural law committed by lower courts.

After studying the materials of case No. A40-86746/2019, the Judicial Collegium for Economic Disputes of the Supreme Court of the Russian Federation recalled the established judicial practice that there is objectively no debt to the budget for a specific type of tax if the accumulated amounts of overpayments for this tax exceed the amount of the newly assessed tax. In the case under consideration, the Court noted, the overpayment arose under the income tax credited to the budget of the constituent entity of the Russian Federation, while the tax liability arose under the VAT paid to the federal budget. Thus, the taxpayer was required to take actions aimed at paying the tax independently (in particular, submitting an application to the tax authority to offset the overpayment against the upcoming obligation to pay another tax).

At the same time, the accrual of penalties for the period of organizational registration of the decision on offset by officials of the tax authority in a situation where the overpayment is confirmed (a tax audit has been completed or the deadline for its implementation has expired) and the taxpayer has submitted an application for offset in advance (before the deadline for paying the tax), would mean the application measures of state coercion against a person who has taken the necessary actions to fulfill his tax obligation, and in the absence of illegal use of treasury funds on his part, which contradicts the relevant provisions of current legislation.

“In this regard, the exercise by tax authorities of their powers, including in cases where the Tax Code provides tax officials with significant time limits for carrying out legally significant actions, should not be opposed to the rights and legitimate interests of taxpayers, including interests related to fulfillment of the obligation to pay taxes in the most convenient way both for the treasury and for the payer himself, keeping in mind the preservation of the amount of overpayment in the budget system and freeing the taxpayer from the need to attract funds from third parties to fulfill the tax obligation, their diversion from their own economic turnover.” , – noted in the Court’s ruling.

In the case under consideration, the Supreme Court emphasized, the Borets company announced in advance (more than two months before the deadline for paying VAT for the third quarter of 2021) its intention to use the overpayment of income tax to fulfill the upcoming obligation to pay VAT. According to the inspection notification dated August 27, 2021, sent to the company, the issue of making a decision on offset of amounts of overpaid tax was subject to consideration after the completion of the desk tax audit or from the moment when such an audit should be completed.

“Thus, the will of the taxpayer to fulfill the upcoming obligation to pay VAT for the third quarter of 2021 through an overpayment of corporate income tax was expressed in due time and was known to the tax authority in advance. The taxpayer has an overpayment of income tax in the amount of 150 million rubles. confirmed on October 26, 2021 upon the filing of an updated tax return by the company and the expiration of the audit period. The inspectorate did not raise any objections regarding the existence of an overpayment during the consideration of the case. The inspectorate’s further postponement of the decision on offset between October 26 and October 29, 2021 was caused by organizational issues of tax administration, and not by the actions of the taxpayer,” the Court concluded.

In this regard, the Supreme Court of the Russian Federation canceled the judicial acts of lower authorities, declared the decision of the tax authority illegal and ordered the latter to eliminate the violations of the taxpayer's rights.

Moscow AP lawyer Vyacheslav Golenev noted that essentially the whole problem of the controversial situation boils down to only two questions: can a taxpayer be considered a debtor to the budget if he has an overpayment that exceeds the amount of the debt, and if so, then perhaps in debt account, for example for penalties, to take into account overpayment of taxes?

According to the expert, there is no objective debt if the overpayment covers it. “Judicial practice has been moving toward this simple idea for decades, but local tax inspectorates continue to charge additional amounts “formally.” This approach of the tax authorities does not correspond to the principle of a real tax liability - if the amount of overpayment exceeds the amount of the imputed tax liability, the real tax liabilities of the taxpayer are negative, i.e. The budget must return the money to the taxpayer. This means that the amount of debt must be reduced by the amount of the existing overpayment,” the lawyer is convinced.

Vyacheslav Golenev added that the rigidity of the rules on the admissibility of offsetting tax amounts in the 2000s. was caused by procedural and administrative difficulties, as well as a lack of technological progress. “Currently, tax authorities have all the technical capabilities to see in real time both the amounts of overpayment and the amount of underpayment to the budget, which allows the necessary offsets to be made automatically. Unfortunately, tax authorities do not always do this,” he emphasized.

Senior lawyer of Personal Tax Management LLC Yulia Kuznetsova believes that the Supreme Court has once again demonstrated a legal approach based on the primacy of the economic essence of the tax: “Actually, the Tax Code provides for the possibility of offsetting the amount of overpaid tax against upcoming payments for another tax, regardless of the budget to which these taxes are to be credited.”

According to the expert, in this case, the Supreme Court proceeded from the fact that the taxpayer had completed in advance all the necessary actions to carry out such an offset and quite rightly noted that the accrual of penalties for the period of organizational registration of the decision on offset by tax authority officials in such a situation would mean an unreasonable application of the measure state coercion in the absence of illegal use of treasury funds on the part of the taxpayer. “The definition is quite logical in the light of judicial practice on the issue of offset for the same tax and can become a significant support for taxpayers in similar situations,” concluded Yulia Kuznetsova.

Calculation procedure

Penalties are calculated for each calendar day of the current delay in payment of the insurance payment or tax.

For example, the tax must be paid by March 30, but the taxpayer was unable to deposit the required amount to pay off the tax debt until the 30th inclusive. This means that penalties begin to accrue from March 31st. It will be accrued until the day the tax debt is paid in full. But there is one peculiarity when determining the timing of the accrual of penalties. The period of its accumulation is not precisely defined in the Tax Code of the Russian Federation, so it needs to be clarified with the regulatory tax authorities.

The amount of the penalty is calculated as a percentage in relation to the amounts of overdue tax payments. The percentage is equal to 1/300 of the established refinancing rate of the Central Bank of the country.

The current formula for calculating penalties for the current year:

Penalty = (overdue tax obligations * refinancing rate / 300) * duration of delay in calendar days

The refinancing rate is a constantly changing value, therefore, in the process of calculating penalties, the rate that is current on the day the penalty is calculated is taken.

Peculiarities of accrual for late tax advances

In addition to all of the above, the current Tax Code of the Russian Federation specifies specifics when calculating penalties for certain types of tax advances.

Transport tax

It is a mandatory tax payment collected from all vehicle owners (both individuals and legal entities). Paid to local tax authorities once a year. The penalty for this type of tax begins to accrue 3 months after non-payment of payment.

Its size is calculated by the formula:

P = refinancing rate (%) * amount of overdue payment * number of days of non-payment / 300

That is, the formula is the same as when calculating other types of taxes. In addition, if the delay was made deliberately, then the person who failed to pay the tax will be required to pay a fine, the size of which is on average 30% of the amount of all overdue payments.

Property

If property tax payments are late, owners are subject to penalties in the form of penalties, accrued every day of late payment. In order to determine the amount of the penalty, the refinancing rate of the Central Bank of the Russian Federation is used.

A fine is assessed by local tax authorities that have identified a payment violation. They issue a notification document for the payer indicating the amount of tax. At the beginning of the tax period, each owner of taxable property is sent a notice of his tax obligations and the deadlines for their payment. When the notification does not arrive, you must contact the tax administration. The calculation formula is standard.

Land

In cases of arrears of land tax, it is calculated on the same principle as for other types of taxes. But there is also a kind of fine for late payment of tax - 20%, for legal entities and individuals, of the unpaid tax amount, and in the amount of 40% if the non-payment was intentional.

The tax authority must send a tax notice to the individual with a requirement to pay the tax and the penalty accrued on it.

Income tax

For advance payments of income tax, it begins to accrue after the expiration of a period equal to one month from the date of non-payment. The accrual occurs in accordance with Article 75 of the Tax Code of the Russian Federation. That is, the rest of the calculation procedure is standard.

The rules for calculating penalties for advances under the simplified tax system are discussed in this video:

Fresh materials

- Clarification on 4 FSS When it is necessary to adjust 4-FSS The calculation presented in the FSS in form 4-FSS does not need adjustments if...

- Social tax 2021 Tax accrualIn accounting, the amounts of advance tax payments are reflected in the credit of account 69 (68)…

- Tax planning Tax planning in an organization Tax planning can significantly affect the formation of the financial results of an organization,…

- Why do they buy gold? Selling gold competently is a process that will require you to spend some free time. It will be necessary to find out...

The amount of penalties for transport tax for individuals

4. The penalty for each calendar day of delay in fulfilling the obligation to pay tax is determined as a percentage of the unpaid tax amount.

The interest rate of the penalty is assumed to be equal to:

- for individuals, including individual entrepreneurs, one three hundredth of the refinancing rate of the Central Bank of the Russian Federation in force at that time;

Let's look at the details of this point:

- The amount of the penalty depends on the amount of tax. Those. if a large amount is not paid, then the penalty will be greater, if it is small, then less.

- The size of the penalty depends on the key refinancing rate of the Central Bank. This point complicates the calculation, because the key rate changes regularly. And for the calculation you need to use exactly the rate that was in effect on the current day.

- For each day of delay, a penalty is charged in the amount of 1/300 of the key rate.

First, a few words about the key rate. You can find out the current value of this value on the website of the Central Bank.

The history of changes in the key rate is shown in the following table:

| Date of change | New rate |

| 27.07.2020 | 4,25 |

| 22.06.2020 | 4,5 |

| 27.04.2020 | 5,5 |

| 10.02.2020 | 6 |

| 16.12.2019 | 6,25 |

| 28.10.2019 | 6,5 |

| 09.09.2019 | 7 |

| 29.07.2019 | 7,25 |

| 17.06.2019 | 7,5 |

| 17.12.2018 | 7,75 |

| 17.09.2018 | 7,5 |

| 23.03.2018 | 7,25 |

| 12.02.2018 | 7,5 |

| 18.12.2017 | 7,75 |

| 30.10.2017 | 8,25 |

| 18.09.2017 | 8,5 |

| 19.06.2017 | 9 |

| 02.05.2017 | 9,25 |

| 27.03.2017 | 9,75 |

| 19.09.2016 | 10 |

| 14.06.2016 | 10,5 |

| 03.08.2015 | 11 |

Note. The table shows values starting from 08/03/2015, which can be used to calculate penalties for transport tax starting from 2014. As for taxes for previous years, they must be written off by the tax office as uncollectible.

Let's look at an example of calculating penalties:

Let's assume that Ivan did not manage to pay the transport tax for 2021 on time. He did this only on December 25, 2021. The tax amount is 3,000 rubles.

Thus, the delay was 24 days. Moreover, during this time the key rate of the Central Bank has changed (12/18/2017). Therefore, the first 16 days must be calculated in accordance with the rate of 8.25, and the remaining 8 - 7.75.

The amount of the penalty will be: 3,000 * (16 * 0.0825 + 8 * 0.0775) / 300 = 19 rubles 40 kopecks.