Penalties are fees for late payment. Such sanctions, like fines, are possible not only for taxes, but also for contracts. Basically, penalties are calculated manually in 1C 8.3. The accountant immediately has a question about which accounts to use when calculating penalties in 1C 8.3 postings.

But are all penalties accrued by an Operation entered manually? We hasten to please you - this is not so! For example, the accounting of penalties under a contract in 1C 8.3 to the buyer is automated. For this purpose, the program provides a special document Accrual of penalties.

Let's figure it out:

- what entries must be made in accounting and in 1C 8.3 in order to accrue penalties for taxes and fees;

- how to calculate a fine in 1C 8.3 - we will reflect the entries in the accounting of the seller and buyer in case of violation of obligations under the contract.

For more details, see the online course: “Accounting and tax accounting in 1C: Accounting 8th ed. 3 from A to Z"

Administrative fines

A special resolution is issued for an administrative fine for a company. In addition to standard information, it indicates

- Amount of fine;

- The article under which the company was fined;

- Required information about the payee.

To pay an administrative fine, an enterprise has 60 calendar days, which must be counted from the day the resolution came into force.

After receiving the resolution, the accountant is obliged to reflect the accrual of the fine in the accounting registers of the 1C 8.3 program.

Administrative fines are accounted for as part of other expenses. This procedure is prescribed in clause 11 of PBU 10/99.

The accounting entries will be as follows: Dt 91 subaccount Other expenses Kt 76 - the administrative fine is reflected in other expenses.

In 1C 8.3, the accrual of an administrative fine should be reflected as an Operation. Go to the Operations menu, select the type of operation Operations entered manually:

Open the selected operation:

Using the Create button, create a new operation and fill in:

- The date of the document and correspondence of accounts corresponding to the accounting entries;

- We recommend filling out the comments line;

- When filling out the analytics, you should use the previously created Miscellaneous Income and Expenses – Administrative Fines item or create a new one:

When choosing analytics for a cost item, you should take into account that the amount of the fine is accepted only for accounting purposes, so you should select the expense/income item “not accepted for accounting”, that is, with a “tick”. The cost should not be marked in the NU column in the cost directory:

Due to the fact that fines in tax accounting cannot be written off as expenses, therefore, a permanent tax liability of the PNO arises.

You should pay attention to the result of generating transactions in 1C 8.3. In the column “Dt NU” the amount of the fine is not reflected. The fine is reflected according to the rules of PBU 18/02:

After posting the document, you need to print the accounting certificate on the Accounting certificate tab. Sign and keep in the accounting documents in the original:

Small enterprises may not apply PBU 18/02 and permanent differences are not formed in accounting.

Description of the calculation of penalties in the 1C program: Accounting in housing and communal services management companies, HOAs and housing cooperatives

The organization began its activities in May 2021; it was decided to accrue penalties for the first time in September 2021 for all services. Our organization has a payment deadline of 15 days (this is the date of the next month by which the current month’s charges must be paid). Federal Law No. 307-FZ* dated November 3, 2015 (hereinafter referred to as Federal Law No. 307) amended the article of the Housing Code regulating the procedure for calculating the amount of penalties. These changes came into force on 01/01/2016. Now, in case of violation of the deadline for payment for residential premises and utilities or payment is not made in full, penalties are accrued in the following amounts:

| from 1 to 30 days | Penalties are not charged. |

| from 31 to 90 days | Penalties are charged at a rate of 1/300 of refinancing |

| from 91 to now | Penalties are charged at an increased rate - 1/130 of the refinancing rate |

Let's look at the algorithm for calculating penalties using an example (the amount of charges changes due to a change in the tariff in July). The debt begins to count from the moment when the due date for paying the accruals passes, in our case after 15 days.

Stages of calculating penalties:

- We charge services

- We close the month for housing and communal services accruals. This operation helps to distribute advances on debts within one agreement, personal account, service

- We create the document Calculation of penalties.

For example, let’s charge penalties to only 1 personal account.

Let's look at the report “Deciphering the fine”

Penalty base - accrual amount for a given month 150.55 - until July, 154.7 - starting from August Penalty rate - 10.5% (refinancing rate) * 1/300 = 0.035% Penalty rate - 10.5% (refinancing rate )*1/130=0.0807% We accrue penalties in September 2016, during which time the debt for May, June, July, and August was formed. The total amount of penalties accrued in September for debt from May to September =

= amount of penalties for May debt + penalties for June debt + penalties for July debt + penalties for August debt

Below in the table we will consider in more detail each component of the formula for calculating penalties in September:

| 1. Calculation of the amount of penalties for debt incurred since May 31, 2016 |

| Payment deadline is June 15, 2021. As of June 15, 2021, payment for May has not been made. From June 15, 2021, 30 days are counted (during this period from June 15 to July 15, 2021 inclusive, no penalties are accrued). From July 16, 2021 (from the 31st day to the 90th day), penalties are accrued in the amount of 1/300 of the refinancing rate (penalties in the specified amount are accrued from July 16 to September 13, 2016 inclusive). From September 14, 2021 (from the 91st day) and subsequent days until the day of actual payment, penalties are accrued in the amount of 1/130 of the refinancing rate. That is, the amount of penalties on the May debt, when accrued in September = = the amount of penalties on the May debt at a rate corresponding to the term (from 31 to 90 days) + the amount of penalties on the May debt at a rate corresponding to the term (over 91 days) = = ( debt for May * 1/300 of the refinancing rate * number of days from 01.09 to 13.09) + ((debt for May * 1/130 * number of days from 14.09 to 30.09 (date of accrual of penalties)) = = (150.55*(1/ 300*10.5)* 13) + (150.55*(1/300*10.5)* 17) = = 0.685+2.065=2.75 |

| 2. Calculation of the amount of penalties for debt incurred since June 31, 2016 |

| Payment deadline is July 15, 2021. As of July 15, 2021, payment for June has not been made. From July 15, 2021, 30 days are counted (during this period from July 15 to August 14, 2021 inclusive, no penalties are accrued). From August 15, 2021 (from the 31st day to the 90th day), penalties are accrued in the amount of 1/300 of the refinancing rate (penalties in the specified amount are accrued from August 15 to November 12, 2016 inclusive). That is, the amount of penalties on the June debt, when accrued in September = = the amount of penalties on the June debt at the rate corresponding to the period (from 31 to 90 days) = = (debt for June * 1/300 of the refinancing rate * number of days from 01.09 to 30.09 (date of accrual of penalties)) = = (150.55*(1/300*10.5)* 30) =1.58 |

| 3. Calculation of the amount of penalties for debt incurred since July 30, 2016 |

| Payment deadline is August 15, 2021. As of August 15, 2021, payment for July has not been made. From August 15, 2021, 30 days are counted (during this period from August 15 to September 14, 2021 inclusive, no penalties are accrued). From September 15, 2021 (from the 31st day to the 90th day), penalties are accrued in the amount of 1/300 of the refinancing rate (penalties in the specified amount are accrued from September 15 to December 13, 2021 inclusive). That is, the amount of penalties on the July debt, when accrued in September = = the amount of penalties on the July debt at the rate corresponding to the period (from 31 to 90 days) = = (debt for July * 1/300 of the refinancing rate * number of days from September 14 to September 30 (date of accrual of penalties)) = = (154.7*(1/300*10.5)* 16) =0.87 |

| 3. Calculation of the amount of penalties for debt incurred since August 31, 2021 |

| The payment deadline is September 15, 2021; as of September 15, 2021, payment for August has not been made. From September 15, 2016, 30 days are counted (during this period from September 15 to October 15, 2021 inclusive, no penalties are accrued). |

Total: Total amount of penalties accrued in September for debt from May to September = penalties for May debt + penalties for June debt + penalties for July debt + penalties for August debt = = 2.75 + 1.58 + 0.87 +0 = 5.2

If you still have questions about calculating the amount of the penalty, we can advise you in more detail.

Review of the report from the Unified Seminar

Order a consultation

To which account in the postings should penalties and fines for taxes be attributed in 1C 8.3

In accounting, the amounts of fines and penalties for property tax, VAT, income tax, etc. are reflected by the entry: Dt 99 Kt 68 subaccount Calculations for fines and penalties - tax penalties and fines for property and profit taxes are accrued or other taxes:

Reflecting an operation in accounting is similar to accounting for administrative fines, only the accounting analytics changes. The registration is carried out based on the requirements of the Federal Tax Service. We recommend opening separate sub-accounts for account 68, where the amounts of penalties and fines for taxes will be shown.

When transferring amounts to the budget: Dt 68 subaccount Calculations of fines and penalties Kt 51 - penalties and fines for tax are transferred to the budget, the balance on account 68 will be closed.

If an organization plans to challenge fines in court or in a higher authority, penalties and fines should still be accrued in accounting by posting: on the debit of account 99 and the credit of account 68. If the court decides positively in favor of the organization, make a reversing entry.

Due to the fact that in accounting all fines are written off to the financial result, no differences arise according to PBU 18/02.

Register of accounting for settlements of penalties

The register is formed to summarize information about agreements containing conditions for the accrual of penalties due to the taxpayer or payable to the counterparty in the form of fines, penalties and other sanctions for violation of contractual obligations, accrued under the terms of the agreement with the counterparty or by court decision, as well as information on accounting for tax purposes of the amounts of accrued sanctions.

The procedure for register formation

To create this register, you need to open the submenu “Registers of the status of a tax accounting unit” from the “Tax Accounting” menu and select the “Register for accounting for settlements of penalties” item.

This register is formed based on the data entered in the “Accrual of Penalties” documents for the selected counterparty and agreement.

Composition of register indicators

Rice. 2. “Register of accounting for settlements of penalties”

Contract details

— filled in based on information about the counterparty and contract details.

Income or expense indicator

— determines the accounting of the amounts of accrued sanctions as part of income or other expenses of the current period. Determined by the terms of the contract.

Start date for accrual of penalties

— determined by the terms of the agreement and filled in based on the relevant details of the selected agreement.

Procedure for calculating sanctions (base)

- indicates the basic cost or quantitative indicator, which, in accordance with the terms of the contract or a court decision, is the starting point for calculating penalties under the contract (amount, products not delivered on time in physical terms, etc.).

Procedure for calculating sanctions (rate)

— the amount of charges per unit of measurement of the base is indicated (in monetary terms or as a percentage) in accordance with the terms of the agreement or a court decision.

Procedure for calculating sanctions (temporary unit of calculation)

— a time indicator is indicated, per unit value of which, in accordance with the terms of the contract or a court decision, the amount of penalties increases.

Amount of sanctions

accrued under the agreement - indicates the amount of penalties accrued under the agreement for each period of accrual of penalties. The total amount in the column is reflected as the amount of income or expense.

Sanction termination date

— indicates the moment of termination of accrual of penalties upon fulfillment of the terms of the contract or for other reasons. Filled out based on the relevant details of the selected contract.

Fines, penalties, penalties under business contracts

The most common fines in the activities of an enterprise are fines, penalties, and penalties under business contracts.

In more detail, how to keep records of fines and penalties under contracts with counterparties in the 1C 8.3 Accounting program is discussed in our article.

In accounting, fines, penalties, and penalties for violation of contractual obligations are included in non-operating expenses. The amounts awarded by the court are accepted for accounting purposes in the period when the court decision on their collection was made. Reflected in accounting by postings:

- Dt 91.2 Other expenses Kt 76 Settlements with various debtors and creditors for the amount of accrued fines awarded by the court;

- Dt 76 Settlements with various debtors and creditors Kt 51 Current account for the amount of transfers, that is, payments.

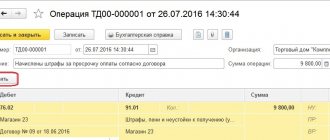

The operation for reflecting a fine in accounting is the same as for reflecting administrative fines - an operation entered manually, only the corresponding account and analytics change:

Since fines and penalties under business contracts are accepted for tax accounting, when posting the document, the amount will be reflected in both accounting and tax accounting.

How to calculate a fine if contractual obligations are not fulfilled

Penalties are assessed if the supplier has not fulfilled contractual obligations.

Similarly to accounting for administrative fines, we fill out the Transaction entered manually:

- We indicate the name, debit and credit accounts;

- Amount for the transaction and subaccount;

- The subconto debit indicates the counterparty;

- Document on debiting from a bank account, on the basis of which penalties are calculated, agreement;

- In the loan subconto we indicate the item of other income and expenses from the directory Directory of Items of Income and Expenses, where we select the income item Fines, penalties and penalties for receipt (payment):

For the amount of the fine, use the document Receipt to current account with the transaction type Other receipt. Type of current account - account 76.02 Calculations for claims, since the amount of the fine is accepted to the NU, the same type of entries are generated in both the BU and the NU.

If you need help in mastering a wider range of operations in the 1C program, then we suggest you take our professional course “ 1C Accounting 3.0 on the TAXI interface ”. For more information about the course, watch the following video:

Please rate this article:

( 10 ratings, average: 4.70 out of 5)

Registered users have access to more than 300 video lessons on working in 1C: Accounting 8, 1C: ZUP

Registered users have access to more than 300 video lessons on working in 1C: Accounting 8, 1C: ZUP

I am already registered

After registering, you will receive a link to the specified address to watch more than 300 video lessons on working in 1C: Accounting 8, 1C: ZUP 8 (free)

By submitting this form, you agree to the Privacy Policy and consent to the processing of personal data

Login to your account

Forgot your password?

How to reflect fines in 1c

The 1C program provides mechanical performance of many often repetitive operations. Payment and accrual of a fine is a one-time situation. Consequently, for reflection in 1C, manual processing of documents is required.

Instructions

1. Payment of an administrative fine from a current account in the 1C program is reflected in the “Documents” section, then “Cash control” and “Bank documents”. Due to the fact that the company does not pay fines all day, there may not be standard settings for processing such one-time documents. 2. To process a payment order to pay a fine in the 1C program after downloading it, open the document by double-clicking the left mouse button. On the toolbar, click Operation. From the list of transactions that opens, select “Other withdrawal of funds” if your company does not provide another processing option. 3. Next, in the “Account” window, call up the directory of accounting accounts and select account 91.02 “Other expenses”. This account is analytical, so a window for selecting analytics will immediately open. In the list that opens, select “Penalties”. After that, click OK in the lower right corner of the window. The document has been submitted. 4. Check the accuracy of the accounting entries. An entry should occur: Debit account 91.02, analytics “Penalties” - Loan account 51 “Current account”. 5. Payment of tax fines is made either at the request of the tax inspectorate, or independently by the enterprise according to an updated tax calculation. When processing a bank document for payment of a fine, the program will prefer the “Tax Transfer” operation and, depending on the settings, may prefer a specific tax for which the fine was paid. It is possible that the tax will have to be entered manually. 6. Accounting 68 “Calculations with the budget” analytical. In the “Account” window, on the pivot tab of the banking document, call up the list of accounting accounts and select the tax for which the fine was paid. Under the “Account” window, in the “Payment Type” window that appears, select the required line: “Tax (accrued/additional accrued), penalties, penalties.” Click OK in the lower right corner of the document. The document has been submitted. 7. Check whether the accounting entry occurred according to the fine payment document: Debit account 68 “Calculations with the budget” – Loan account 51 “Current account”. 8. The accrual of a tax penalty is recorded in the debit of account 91.02 “Other expenses”, subaccount “Penalties” in correspondence with the credit of account 68 “Settlements with the budget”.

Most people use a current account to pay fines However, the lack of a current account is not a reason for avoiding paying a fine, because Russian law provides for other options.

You will need

- – receipt form PD-4;

- - computer;

- – documents for opening a current account.

Instructions

1. If you need to pay a fine without a current account , contact Sberbank and ask for a receipt in form PD-4. After filling it out, pay here. However, remember that if you use the PD-4 receipt to pay the fine, the bank’s commission will be quite large - up to fifteen percent. Therefore, if you need to pay a huge fine, use a different method. 2. If you want to pay a fine using the Internet, say, through the WebMoney or Yandex money service, visit the formal website of the tax service: https://www.nalog.ru/ and go to the taxpayer’s individual account (or immediately follow the link https: //service.nalog.ru/debt/). Provide your personal information and follow the instructions. In your personal account, enter your TIN (you can find it on the same website here: https://service.nalog.ru/inn.do) or the TIN of your organization. Now you will see all your debts and fines (or fines and debts of your organization). Select the one you want to pay and follow the instructions. 3. If for some reason you cannot pay a fine via the Internet, open a current account. To do this, contact the tax office at your place of residence and explain the situation. Collect all the documents you are asked to provide and provide them to the tax office. After this, contact your nearest bank and state that you would like to open a current account. 4. Also notify the Social Insurance Fund and the Pension Fund about opening a current account . Later, find out what the bank’s commission will be for paying the fine. Top up your current account with an amount equal to the amount of the fine and commission and pay the fine. Later, if you do not want to leave your current account open, tell the bank representatives that you want to close it. Don't forget to notify the tax service, Social Insurance Fund and Pension Fund about closing your current account . Note! If you need to pay a fine as a legal entity, do not do this on behalf of an individual, because in this case the payment will go directly to the individual’s account, and there are no methods to transfer it to the legal entity’s account. Helpful advice: Before you pay the PD-4 receipt, check with the tax service for all the necessary details, because bank employees may provide incorrect data, and you will have to pay the fine again.

Currently, virtually all organizations use personal computers and various specialized software. Particularly famous among them is the 1C: Enterprise program, which facilitates the process of accounting. However, many encounter difficulties in reflecting the process of obtaining and listing computer programs in accounting and tax accounting.

Instructions

1. Recognize the costs of obtaining the 1C: Enterprise program as expenses for ordinary activities. In some cases, which are associated with the receipt of a product under a copyright agreement, according to which exclusive rights to software are transferred, these costs are accounted for as intangible assets of the enterprise and are carried out in accordance with PBU 14/2000. However, this case cannot be attributed to the use of 1C, because it is purchased on the basis of a purchase and sale agreement or an agreement on the transfer of non-exclusive rights. 2. Determine the accounting procedure for the 1C program based on the terms of the payment agreement. If the program is received as a one-time payment, then the costs are reflected in the expenses of future periods and are written off in parts during each period of use of the application. To do this, a loan is formed on account 51 “Current accounts” and a debit on account 97 “Expenses for future periods.” 1C company specifies the service life of the program in the contract. You need to divide the total cost of the application by the number of specified months. The resulting value is written off on the debit of account 26 “General business expenses” or 20 “Main production” in correspondence with account 97. 3. Reflect in accounting the costs of updating the 1C program. Expenses for this operation are recognized in the reporting period in which they are incurred. To do this, a loan is formed on account 60 “Settlements with contractors and subcontractors” and a debit on account 26 or 20. If the software shell has been updated, for example, an additional network version of the 1C program has been purchased, then the costs for this operation are charged to account 97 and written off monthly on account 26. 4. Take for deduction the amount of VAT that the company paid after receiving the 1C program for the reporting period when the purchase was reflected on account 97. In this case, you need to submit an invoice with the amount of accrued VAT and the fact of using the program for carrying out transactions that are subject to VAT.

Any economic activity requires a fast business cycle, one that is accompanied by high competition. Unfortunately, this entails various kinds of situations, such as the accrual of fines. They can arise either as a result of an on-site audit, or for late payment of taxes, or for late submission of reports. Many fines are calculated and assessed using 1C.

Instructions

1. This operation is carried out by an accountant of one or another enterprise. If a notice from the tax authorities indicating the accrued fines has not been received, then contact the tax office assigned to your company. The state tax inspector will notify you of all the exact and complete amounts of fines, and for each tax at once, if any. 2. If the management of your company agrees with all the indicated amounts, then you, as an accountant, begin the procedure for reflecting all these penalties. Based on the rules of accounting, those amounts that are accrued in settlements with the budget must be strictly taken into account. Under no circumstances should there be unaccounted amounts on the balance sheet. Reflect all fines exactly in the reporting period in which the corresponding decision was made. 3. The main thing to take into account is that, according to article number two hundred and seventy of the Tax Code, those fines that are subject to payment to extra-budgetary funds, as well as to the state budget, are not reflected in the taxation of revenue in any way. 4. Now it’s easy to talk about the 1C program. Calculate fines manually using accounting entries. If we are talking about tax penalties, then these amounts go through the debit cycle of account 99. The correspondence account in this case will be “Calculations for taxes and fees.” 5. Postings for other fines are also made according to this scheme. In order to avoid daring violations in reporting, use the latest Chart of Accounts when preparing accounting documents. This document can be downloaded, say, on the website of the Ministry of Finance, or you can develop a personal one based on a standard example.

The 1C program can do a lot, but it reflects already accomplished facts and is not capable of changing them. It is important, at the time of purchasing the application itself, to provide for all the tight spots at the stage of completing the contract and clearly write down each clause of the agreement. Then entering this transaction into 1C will not be difficult.

Instructions

1. Carefully study the contract for the purchase of the 1C program. To reflect the process of obtaining it in accounting, it is important to know the stages and timing of implementation, the payment procedure and the rules for acceptance/delivery of work accepted by the parties. 2. The progress of the execution and acceptance into operation of individual program blocks is monitored by experts in the relevant areas of production: warehouse, accounting, etc. After the receipt documents are completed, it is possible to begin recording the accepted material and reflecting it in 1C. 3. Essentially, all receipts within the boundaries of the contract for receiving the 1C program are divided into physical and intangible. Accordingly, accounts in the 1C program also differ. 4. Receipts of goods and materials (1C writing, installation disks, etc.) are recorded as unprofitable receipts. If you have correctly executed and signed unprofitable ones, reflect the receipt of inventory and materials in the 1C program. 5. In the full interface, select “Documents” from the main menu. Submenu “Procurement Management”, then “Receipt of Goods and Services”. On the toolbar, click the Add icon. In the document that opens, select the counterparty, check the boxes “Accounting control”, “Tax control” and, if necessary, “Management control”. Inventory items are entered in the “Products” tab. Post the completed document. 6. Each block of work on setting up and debugging the program, loading data from an old database, etc. are essentially services and are entered into 1C on the basis of acts of completed work signed by the parties. The act for services received is reflected in a difference from the document in the section “Receipt of goods and services”. 7. Payment for work performed is reflected in the “Bank Documents” section of the “Documents” item in the main menu, submenu “Cash Management”. Video on the topic

Register-calculation of the amounts of accrued penalties

The register is formed to summarize information on the amounts of penalties due to the taxpayer or payable to the counterparty in the form of fines, penalties and other sanctions for violation of contractual obligations, accrued under the terms of the agreement with the counterparty or by court decision.

The procedure for register formation

To create this register, you need to open the submenu “Tax Transaction Accounting Registers” from the “Tax Accounting” menu and select the “Register-calculation of amounts of accrued penalties” item.

The register reflects entries for each accrual of penalties entered in the document “Accrual of penalties” for the specified period. The value of all register indicators is taken from the tabular part of the document.

Composition of register indicators

Rice. 3 “Register-calculation of the amounts of accrued penalties for the reporting period”

Contract details

— name of the counterparty and number of the agreement under which penalties were accrued.

Income or expense indicator

— determines the accounting of the amounts of accrued sanctions as part of income or other expenses of the current period.

The period for which penalties are calculated

— the time period for calculating sanctions is indicated.

Procedure for calculating sanctions (base)

- indicates the basic cost or quantitative indicator, which, in accordance with the terms of the contract or a court decision, is the starting point for calculating penalties for the current period (amount, products not delivered on time in physical terms, etc.).

Procedure for calculating sanctions (rate)

— the amount of charges per unit of measurement of the base is indicated (in monetary terms or as a percentage) in accordance with the terms of the agreement or a court decision.

Procedure for calculating sanctions (temporary unit of calculation)

— a time indicator is indicated, per unit value of which, in accordance with the terms of the contract or a court decision, the amount of penalties increases.

Amount of sanctions accrued for the current period

— the amount of penalties calculated in accordance with the terms of the agreement or a court decision when entering this entry into the register is indicated. This amount is also reflected in the income register of the current period or the non-operating expenses register of the current period.