What is retained earnings of an enterprise

A company's retained earnings are its net profit (after tax), which has not yet been divided among the participants (shareholders) of the organization. How such profits will ultimately be distributed depends on the decision of shareholders at the annual meeting. Typically, funds are spent on the following purposes:

Take our proprietary course on choosing stocks on the stock market → training course

- payment of dividends to shareholders (participants) of the organization;

- formation or increase of reserve capital;

- fulfillment of remaining obligations;

- other goals chosen by the owners of the enterprise.

Retained earnings are a liability because they are, in fact, an unfulfilled obligation to the owners of the business. Ideally, the money should be paid as dividends to the owners and used to develop the business.

In the same way, a liability is an uncovered loss, which is indicated in parentheses due to its negative value.

Example of retained earnings and uncovered losses

Let's look at an example of what constitutes retained earnings and uncovered losses:

| Index | Definition | Example |

| retained earnings | The final income that was received by the enterprise as a result of business activities remained after taxation and has not yet been divided by the owners or spent on the needs of the business. | Pobeda LLC made a profit in the amount of 755 thousand rubles in 2021. Income tax amounted to 125 thousand rubles. The accountant calculates retained earnings: RUB 755,000 – 125,000 rub. = 630 tr. This amount will be reflected in line 1370 of the balance sheet. |

| Uncovered loss | The excess of an enterprise's expenses over its income at the end of the year. | In 2021, Dela Super LLC receives income from production and other non-operating income, in total - 367 thousand rubles. The cost of producing goods is 335 thousand rubles. Other expenses that are not taken into account when calculating income tax - 46 thousand rubles. Income tax – 7600 rubles. There is no reserve capital. Uncovered losses: RUB 367,000 – 335,000 rub. – 7600 rub. – 46,000 rub. = -21,600 rub. The value will be entered in line 1370: (21,600). |

The most common causes of uncovered losses are described in the diagram below:

What is contained in column 1370

The codes are indicated in the supplement to the orders regulating the preparation and entry of information into the reporting documentation. Retained earnings in the balance sheet are line 1370. The column also contains the amount of uncovered loss that has accumulated over a certain period of time at the time the balance sheet was written.

According to the Chart of Accounts, account 84 is intended for recording retained profits and losses. Profits and losses received as of December 31 are recorded in it. In column 1370 enter the amounts for the reporting years - both the current and the previous one. The loan balance is shown here. If the organization has suffered a loss, the account balance is entered in the line by debit.

When a document is written for the reporting period, the remainder of 84 and 99 “Profit and Loss” is entered into 1370. It is the latter that displays the result of accumulated profits or losses from usual activities, other operations, and the money that is directly related to this account. These are penalties for violation of the Tax Code of the Russian Federation.

If, as of the date of writing the report, losses were recorded at the enterprise, their amount is written without the minus sign, and in brackets: (2000).

Factors that can influence retained earnings (uncovered loss)

The amount of retained earnings may increase or decrease during the reporting period depending on what actions the managers and employees of the organization perform:

| Increase in uncovered loss | Reducing uncovered losses |

| Due to the reduction in the volume of authorized capital while bringing its value to the amount of net assets | In connection with the direction of retained earnings to the reserve fund |

| For the amount of additional capital arising during the revaluation of disposed non-current assets during the reporting period | Due to an increase in the size of the authorized capital due to retained earnings |

| For the amount of declared and unclaimed dividends for which the statute of limitations has expired | For the amount of accrued dividends (including interim) |

| On the amount of net profit of the reporting period | By the amount of net loss of the reporting period |

Profit and loss asset and liability

The Letter states, in part:

“the indicator “net profit (loss) of the reporting period” for reflection in the profit and loss statement is calculated based on the fact that the amount of the conditional income tax expense, deducted from the amount of profit before tax, should be the amount of the conditional income tax expense, adjusted for the amount of permanent tax liabilities. The specified amount of income tax expense is formed in the income statement as a set of amounts reflected under the items “deferred tax assets”, “deferred tax liabilities” and “current income tax” (clause 24 of PBU 18/02).

Based on the above, “deferred tax liabilities (assets)” are taken into account when calculating net profit, which is the source of dividend payments.”

Let’s assume that in the first quarter, according to accounting data, the organization made a profit of 90,000 rubles.

Line 1370 “Retained earnings (uncovered loss)”: how to fill out

First of all, it is necessary to understand several points that are directly related to entering information in line 1370:

- The amount of the enterprise's net profit for the reporting period should be reflected according to the CT account. 99 “Profits and losses” in accounting, and the amount of net loss - according to Dt account. 99.

- If, after approval of the financial statements for the current period, significant errors from the previous period were identified, they must be corrected. Corrections are made by making entries in the relevant accounting accounts in the current reporting period. Account 84 is corresponding. That is, if the company corrected significant flaws in 2014 or earlier periods by making entries in the financial statements in 2015, despite the fact that the 2014 financial statements had already been approved, the indicator on line 1370 of the balance sheet for the reporting period of 2015 containing corrective entries should be formed taking into account the correctional entry.

- The accountant must reflect the accrual of dividends according to Dt account. 84 in correspondence with account. 70 and count. 75, sub-account 75-2. This applies to both interim dividends and year-end dividends. If dividends are declared but not claimed, and their statute of limitations has expired, a reverse entry is made for their amount.

- By the final turnover of December, the amount of retained earnings should be taken into account according to the CT account. 84, the amount of uncovered loss - according to Dt account. 84. The amount of net profit or loss of the reporting period should be written off to the account. 84.

Important! The distribution of profit at the end of the period is an event after the reporting date, which indicates that after the reporting date conditions have arisen in which the enterprise carries out its business activities. In the reporting period for which profit should be distributed, no entries are made in accounting (neither in analytical nor in synthetic accounting). But in the next period, the accountant will already make an entry to properly reflect the event. This means that information on the account. 84 “Retained earnings (uncovered loss)” in the reporting period will be formed taking into account the decision made in the reporting year on the distribution of profits identified based on the results of the previous year.

Using the resulting retained earnings to modernize and improve the company's production will not lead to either a change in the indicator of line 1370 or changes in the balance of account 84. Let's find out why. The fact is that the formation in accounting of information about the purposes for which funds of retained earnings will be directed is carried out through the organization of analytical accounting for accounts. 84. In it, money from retained earnings that has not yet been used, and which it was decided to use to subsidize the modernization of production and any other events for the purchase or creation of new assets, can be divided. Costs incurred by an enterprise must be recognized in the reporting period in which they occurred, regardless of:

- time of their formation;

- presence/absence of a source of funds (various funds).

When preparing interim reporting, information from accounts 84 and 99 is used to fill out line 1370 for the reporting period. If the value that needs to be entered on line 1370 appears with a minus sign, it should be placed in parentheses to avoid confusion.

Definition

Retained earnings on the balance sheet are the portion of certain profits that remains with an organization after it has paid all taxes, salaries, dividends and other payment obligations.

To assess the company's performance, the most important indicator in the report is profit for a certain period of time.

Based on its positive or negative dynamics, one can understand how effectively the organization operated in a given period of time.

In order to increase productivity, and as a result, the growth of income received, it is necessary to correctly direct funds from retained earnings.

The allocation of these resources is influenced by the decisions of the firm's management. They will be jealous of where the retained earnings will be directed:

- employee bonuses;

- dividend payment;

- increase in the amount of authorized capital;

- increasing the reserve fund;

- distribution of funds for other purposes aimed at the development of the organization.

Important: retained earnings cannot be accumulated until the organization fulfills all monetary obligations for a certain period of time.

The concept of retained earnings closely intersects with the concept of net profit.

However, their difference is that retained earnings are primarily a performance indicator for a period of one calendar year or for the period from the start of the organization’s work to the present.

Net profit is necessary for reconciliation of indicators for the reporting period.

It should be taken into account that retained earnings in the organization are interpreted differently.

The accountant evaluates such profit as the result of the final work for the year and reflects its indicator in the 84th account.

The profit itself is distributed by the owners of the organization in the person of its owners.

They distribute it for the next year starting from March 1 and until June 30 of the current year.

The economic meaning of retained earnings will be that its indicators will be considered the next year after the date of its actual calculation and distribution by the accountant, based on the decision of the enterprise management.

back to menu ↑

Line 1370, annual and interim reporting (balance sheet formula)

On page 1370, enterprise accountants reflect the amount of retained earnings or uncovered losses. The formulas by which the values to be entered in the line can be found differ depending on whether we are talking about interim or annual reporting.

Balance sheet formula for filling out line 1370 for annual reporting:

Balance sheet formula for calculating the value of line 1370 for interim reporting:

To fill in line 1370, you can use the formula

if the following statements are true for the enterprise under study:

- at the beginning of the reporting period there is no retained profit (uncovered loss) from previous periods;

- During the current period, there were no disposals of previously overvalued fixed assets;

- There have been no distributions of interim dividends during the current year.

This is explained by the fact that the amount of retained earnings of the reporting period is equal to the amount of net profit of the reporting period (profit after deduction of tax payments). And the amount of the uncovered loss of the reporting period is the same as the amount of the net loss of the reporting period (loss after taxes). So, if the company does not have retained earnings or uncovered losses from previous periods, and no distribution of interim dividends was made during the reporting period, the indicator on line 1370 will be the same as the value on line 2400 (form No. 2).

Retained earnings as a source of production development

Of great interest is the fact that the Ministry of Finance, as a recommendation, proposes, within the framework of analytical accounting, to separately reflect that part of the net profit that is allocated to the development of the enterprise. As is known, the acquisition of fixed assets is carried out at the expense of property (cash), and there are no mandatory entries indicating the source. This entry does not lead to a decrease in retained earnings and the size of the enterprise’s net assets. An enterprise can easily prove that fixed assets were acquired solely through profits and not in any other way. Sources of financing can also be identified based on an analysis of the balance sheet structure. This analysis assumes that investments are made primarily from net profit, secondly from long-term loans, and thirdly from other accounts payable.

Clarifications on filling out line 1370

In order to correctly reflect retained earnings and uncovered losses, the following rules must be observed:

- Indicators on line 1370 as of December 31 of the previous and previous periods must, in general, be transferred from the balance sheet for the previous year.

- The Ministry of Finance of the Russian Federation recommends that interim dividends that were paid during the year for which reporting is prepared be reflected separately in section 3 of the annual balance sheet in parentheses - for this purpose, a separate line 1371 “Including interim dividends” should be entered in the mentioned section.

- The order in which interim dividends are reflected should be the same for the current, previous and previous periods (if you decide to enter line 1371, it should be everywhere).

- The accountant is obliged to ensure comparability of information on the amount of retained earnings as of the reporting date and as of December 31 of the previous and previous periods. If the enterprise's accounting policies changed in year n+1, the consequences of the changes must be reflected retrospectively. Those. comparative indicators from the columns “as of 31.12 n-1 year” and “as of 31.12 n-1 year” on page 1370 and for related items must be adjusted as if the new accounting policy was taken into account from the time facts of activity of this type appeared.

- If the enterprise was correcting significant errors of the previous year in the reporting period, and the reporting of the previous year had already been approved, a retrospective recalculation is carried out. This means that the indicator of uncovered loss or retained earnings for 31.12 years n and n-1 are subject to recalculation as if the error had never occurred.

- If the company was correcting errors of those years that preceded the previous period, it will also be necessary to recalculate the uncovered loss or retained earnings for 31.12 years n-1. But not when it is impossible to understand what the impact of the found error is cumulatively in relation to all previous years, or what is the connection between the error made and a specific period of activity.

What is included in retained earnings on the balance sheet: calculation using the formula

So, summarizing the accounting data, the accountant calculates the amount of retained earnings in the balance sheet (line 1370), which the owners of the company have the right to distribute. Taking into account the previous values of this indicator, already appearing in the balance sheet, it can be calculated using the formula:

- NPk = NPn + PP – D, where:

- NPn and NPk – NP at the beginning and end of the reporting period;

- PE – net profit, ;

- D – dividends due to owners, paid from NP of previous periods in the reporting year.

Adjustments to balance sheets during the inter-reporting period

In some situations, an enterprise is obliged to make adjustments to balance sheet indicators during the inter-reporting period as of 01.01 of the reporting period. Such cases are described in the table below:

| The essence of adjusting balance sheet indicators | Details |

| Assignment of the results of restatement of deferred tax assets and liabilities to retained earnings or uncovered loss | The recalculation is caused by a change in tax rates for income tax in accordance with the laws of the Russian Federation. |

| Adjustment of the amount of retained earnings or uncovered loss when there is a change in accounting policy (not required when the financial implications of the change in accounting policy for earlier periods cannot be estimated with reasonable accuracy) | – When an entity's accounting policies are subject to changes due to legal or regulatory requirements. accounting acts; – in any other cases of revision of accounting policies. |

| Attribution of the results of revaluation of fixed assets to retained earnings or uncovered loss | – When a previously undervalued fixed asset item is discounted; – if the amount of depreciation of a fixed asset turns out to be greater than the amount of its revaluation, credited to the additional capital of the enterprise due to revaluation, which took place in earlier periods; – when an additional valuation of a fixed asset that was previously discounted is made (in this case, the amount of the write-down for earlier years was attributed to retained earnings or uncovered losses in earlier periods). |

| Adjustment of the amount of retained earnings (uncovered loss) when the estimated values of intangible assets (their residual value) change | – If the method of calculating depreciation for intangible assets has been clarified; – when the useful life of intangible assets was clarified. |

| Attribution of the results of revaluation of intangible assets to retained earnings or uncovered loss | – If an intangible asset that was previously discounted is revalued (and the amount of the writedown for earlier years was allocated to retained earnings in earlier periods); – when it is decided to discount an intangible asset that was not previously undervalued; – if the amount of the write-down of intangible assets turns out to be greater than the amount of its revaluation, credited to the company’s additional capital due to the revaluation carried out in earlier years. |

Indicator for investors

Retained earnings are a very convenient indicator for investors of the success of an enterprise. There may be several options, and from each a certain conclusion is drawn. Here are some examples:

- A situation when a company accumulates retained earnings without launching development projects. If the business is stable and does not require further progress, this is a good option that allows you to receive dividends.

- If modernization or further advancement in the market is needed, such conservatism can lead to stagnation and then a drop in income.

***

Retained earnings in the balance sheet are determined according to an established formula and show how much business owners can distribute in different directions. In addition, this indicator gives investors an idea of the company's success.

Similar articles

- How to calculate income tax on an accrual basis?

- What is book profit?

- How to calculate income tax: example

- The ratio of penalties and losses

- How to show a loss on the balance sheet

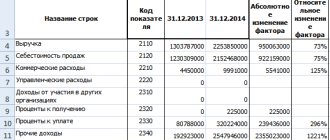

An example of filling out line 1370 when preparing annual reports

Let's imagine a hypothetical Do-It-Yourself limited liability company whose accountant prepares annual reports. The company does not keep records of special funds on the account. 84.

Indicators for account 84:

Fragment of the Balance Sheet for 2013:

Solution:

Fragment of the Balance Sheet of Do It Yourself LLC:

Answers to frequently asked questions on the topic “Retained earnings (uncovered loss)”

Question: How to reflect retained earnings from previous years?

Answer: It is accumulated on account 84. Balance on Kt account. 84 should be transferred to line 1370 of the balance sheet. Since the distribution of profits is usually made at the end of the year at a meeting of owners, there is no movement in account 84 during the year.

Question: What situation with retained earnings at the enterprise will suit potential investors?

Answer: The ideal option for investors is a company that pays dividends to participants and then invests the remaining funds in business development. Investors may also be interested in the option of waiving dividends in favor of improving and modernizing production.

We divide last year's profit correctly | Book Magazine | No. 2 for 2013

The article from the magazine “MAIN BOOK” is current as of January 11, 2013.

magazine No. 2 for 2013

The year's results are of interest primarily to the company's owners, who expect to either receive dividends or otherwise dispose of net profit. But this profit is determined according to accounting data. And who else, if not an accountant, best imagines the situation of the organization? We will look at how to correctly calculate the amount that owners can distribute as dividends.

Closing the year - identifying current profit

The balance sheet reform must be carried out as of December 31. It represents the closure of financial performance accounts.

But before we talk about this, remember that at the end of each month, accounts 90 and 91 have a zero balance. The financial result for the month for these accounts is transferred from subaccount 90-9 “Profit/loss from sales” (91-9 “Balance of other income and expenses”) to account 99 “Profit and loss”. To account 99, some organizations open subaccounts 99-1-1 “Profit/loss from ordinary activities” and 99-1-2 “Balance of other income and expenses.”

However, during the year the subaccounts to accounts 90 and 91 have balances. And only when the balance sheet is reformed they are reset to zero. Thus, the debit of subaccount 90-1 “Revenue” is closed to the credit of subaccount 90-9 “Profit (loss) from sales”, and from the credit of subaccount 90-2 “Cost of sales” (90-3, 90-4...) the amounts are written off to debit subaccount 90-9. Subaccounts to account 91 “Other income and expenses” are closed in the same way.

Often, a subaccount 99-9 “Profit and Loss Balance” is opened to account 99 “Profit and Loss”, on which the amount of net profit/loss for the year will be formed. At the end of the year, all other sub-accounts opened to account 99 are closed to it. In this case, at the end of the year, the balance of other sub-accounts opened to account 99 is transferred:

- at the end of the year these subaccounts have a credit balance, then it is written off to the credit of subaccount 99-9;

- At the end of the year, these subaccounts have a debit balance, then it is written off as the debit of subaccount 99-9.

After this, the balance of subaccount 99-9 is transferred to account 84.

The distribution of profit for dividends is reflected on the date of the decision by the participants.

It may happen that when you prepare your annual financial statements, the approximate amount of dividends will already be known - for example, it is recommended by the board of directors based on preliminary data on financial results. Please note that there is no need to make entries to account 84 based on this with 2012 entries.

Entries for the distribution of actual dividend amounts should be reflected in 2013. However, the announcement of their recommended amount may be considered an event after the reporting date. 3, 5, 10 PBU 7/98. And the Ministry of Finance advises to indicate in the explanations to the financial statements how profits will be distributed in the future. Recommendations, approved. By letter of the Ministry of Finance dated December 19.

2006 № 07-05-06/302.

We study the net profit indicators in the reporting

In accounting, data on the amount of final profit occurs in two forms:

About in what situations during the year you can reflect postings on account 84, read: 2013, No. 3, p. 26

- in the balance sheet - line 1370 “Retained earnings (uncovered loss)”, it reflects the total balance of account 84 in terms of retained earnings (uncovered loss). The formation of this indicator, as a rule, is influenced by all changes in account 84 that occurred during the reporting year. Moreover, they can affect both the retained earnings of the current year and the profits of previous years.

When forming the indicator for line 1370, of all transactions reflected in account 84, only transactions for the expenditure of special funds are not taken into account, which some organizations keep in separate sub-accounts to account 84;

For many owners, accounting is like a Chinese charter. Only with the help of an accountant can hieroglyphs turn into real money

- in the income statement (in the financial performance statement) - line 2400 “Net profit (loss)”, this shows the amount of net profit (loss) that was received specifically for 2012. 23 PBU 4/99 It is defined as the amount that, during the reformation of the balance sheet, was written off from account 99 to account 84. Thus, in the income statement we see profit/loss that is not calculated on an accrual basis for all previous years, but only identified during the reporting year.

If in the annual reporting the value of line 1370 of the balance sheet is equal to the value of line 2400 of the income statement, there are no special difficulties: most likely, this is the amount of net profit that the owners can claim for distribution.

But this rarely happens. Moreover, often neither line of the financial statements gives an idea of how much profit the owners can distribute among themselves.