Account 68 “Calculations for taxes and fees”

The size and frequency of tax payments are established by the current fiscal legislation. Thus, the Tax Code of the Russian Federation provides for settlements with the budgets of the federal, regional and local levels. And in addition to tax obligations, companies are often required to pay specific fees. For example, state duty or local trade tax.

According to Order of the Ministry of Finance No. 94n, account 68 should be used in accounting to reflect calculations for state taxes and fees. Note that in addition to dividing fiscal obligations by level of the recipient budget, taxes are divided into:

- Property. This type of tax is paid for the use of a specific type of property. For example, if a company operates transport, land, buildings, etc., then the company is obliged to pay the state a certain amount of funds. The size of property tax return is determined based on the volume of the tax base multiplied by the rate.

- Indirect. BUT, which are included in the cost of goods, works or services, should be classified as indirect. For example, this type of non-compliance includes value added tax, excise taxes, customs duties and duties.

- According to the result. These NUTs are calculated from the specific result of the economic activity of the subject for a certain period of time (calculation period). For example, corporate income tax. Calculation indicators for this type of non-commercial entity must coincide with declarations and other reports submitted to the Federal Tax Service.

Indicators 68 of the accounting account reflect not only the amount of accrued debt to the state, but also the amount of funds transferred to the budget system of the Russian Federation, as well as the amount of tax liabilities subject to refund or deduction.

Features of account accounting 68

This accounting account belongs to the group of active-passive ones, that is, the balance of account 68 can be not only debit, but also credit. It all depends on whose benefit the debt is: in favor of the company or the state.

Transactions should be reflected by type of tax liability. To organize this detailing in the working PS, special sub-accounts are provided for account 68:

The final balance of account 68 in terms of tax obligations may be different. Consequently, an expanded balance is formed for the existing subaccounts. For example, a debt on one tax is reflected in credit 68 of account, and an overpayment on another is recorded as a debit. In this case, when including accounting indicators 68 in the annual balance sheet and other financial statements, make sure that debit balances are included in the balance sheet assets, and credit balances are included in liabilities.

Calculation of transport tax (accounting entries)

Every accountant accompanying the activities of a company for which a vehicle from the list of Article 358 of the Tax Code of the Russian Federation (motorcycles, cars, buses, airplanes and other vehicles) is registered, sooner or later faces the issue of reflecting the accrual of transport tax in transactions. After all, according to tax legislation, such a company is a transport tax payer.

General rules and norms for recognizing expenses when reflecting transport tax in accounting should be applied. Let us turn to the Chart of Accounts and PBU 10/99 “Organizational Expenses” in order to understand the issue from a practical perspective.

Tax base and calculation

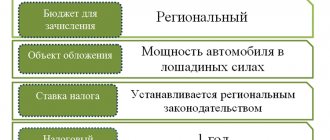

So, the objects of taxation are vehicles, regardless of whether they are land, water or air. Individuals must pay a fee for motorcycles, cars and other vehicles that are for personal use. We must not forget that the fee, among other things, also applies to boats, along with motor sledges, motor boats and jet skis. In this case, the tax base is very important for calculating the fee, on which the amount of payment received by the budget directly depends. The actual size of the base depends on the type of transport. The following factors are taken into account:

- If the vehicle is equipped with an engine, then the basis for the calculations is power, which is measured in horsepower.

- In the event that an air or water vehicle is not equipped with an engine, for example, floating cranes, landing stages, etc., then the fee is calculated based on the gross tonnage value. In this situation, the unit of measurement is registered tons.

- In exceptional situations, the base is taken as a vehicle unit for calculations.

Transport tax accounting

Account 68 “Calculations for taxes and fees”, provided for in the Chart of Accounts, is used, among other things, for reflecting and accounting for transport tax. You should create a subaccount to account 68 specifically for postings for calculating transport tax.

For each vehicle, the amount of transport tax payable to the budget at the end of the tax period, in accordance with clause 2 of Art. 362 of the Tax Code of the Russian Federation is calculated separately.

Therefore, it is advisable in accounting to reflect the accrued amounts in the accounts of the corresponding costs - either for production or as part of other expenses. The choice of a specific corresponding account will depend on where exactly the transport is used: in auxiliary or main production, in which particular division.

If transport is used in the main production, then the transport tax is classified as ordinary expenses and its accrual is reflected in correspondence with accounts for accounting for ordinary expenses 20 (23, 25, 26, 44 ...).

Let's look at the accounting entries for transport tax:

| Debit | Credit | Posting Contents |

| 20 (23, 25, 26, 44…) | 68 (separate subaccount) | The amount of accrued transport tax is reflected |

| 68 (separate subaccount) | 51 | The debiting of money from the current account for the transfer of transport tax to the budget is reflected |

Now let’s look at the accounting entries for transport tax in a situation where the vehicle is not used in the main activity, but, for example, is leased (in this case, rental of transport is not the main activity of the company).

In this case, it is necessary to reflect the accrual of transport tax in correspondence with the account of other expenses and make the following entries:

| Debit | Credit | Posting Contents |

| 91 (other expenses) | 68 (separate subaccount) | The amount of accrued transport tax is reflected |

According to Art. 362 of the Tax Code of the Russian Federation, advance payments for transport tax are quarterly, therefore the accrual and payment of transport tax are made quarterly.

According to clause 18 of PBU 10/99, accrued amounts of advance payments for transport tax are accepted as corresponding expenses of the quarter for which the advance payment is accrued.

How to reflect transport tax in accounting and tax accounting

Accounting

In accounting, transport tax calculations are reflected in account 68 “Calculations for taxes and fees”. To do this, open a subaccount for account 68 “Calculations for transport tax” (Instructions for the chart of accounts).

As a rule, transport tax relates to expenses for ordinary activities (clause 5 of PBU 10/99).

The procedure for its reflection in accounting depends on the production or division of the organization in which the vehicle on which the tax is calculated is used. Also read how to calculate property taxes in accounting.

When calculating and paying transport tax, make the following entries:

Debit 20 (23, 25, 26, 44...) Credit 68 subaccount “Calculations for transport tax” – transport tax has been accrued (advance tax payment);

Debit 68 subaccount “Calculations for transport tax” Credit 51 – transport tax has been paid (advance tax payment).

If the vehicle is not used in the main activity of the organization, for example, transferred under a lease agreement (provided that this type of activity is not the main one), consider transport tax as part of other expenses (clause 11 of PBU 10/99):

Debit 91-2 Credit 68 subaccount “Calculations for transport tax” – transport tax has been accrued.

Calculate the amount of transport tax (advance payments for transport tax) in the accounting statement. This document is the basis for including transport tax (advance payments) as expenses (Article 9 of the Law of December 6, 2011 No. 402-FZ).

The tax accounting procedure for transport tax depends on the taxation system that the organization uses.

BASIC

When calculating income tax, include the amount of transport tax (advance payments for transport tax) among other expenses associated with production and sales (subclause 1, clause 1, article 264 of the Tax Code of the Russian Federation). This must be done in the same period for which the advance payments are calculated. This should be done despite the fact that since 2011, organizations have been exempt from calculating advance payments for transport tax. Similar clarifications are contained in letters of the Ministry of Finance of Russia dated June 7, 2011 No. 03-03-06/1/333 and dated April 20, 2011 No. 03-03-06/1/254.

You can confirm costs in the form of accrued amounts of advance payments for transport tax with primary documents drawn up in accordance with current legislation and containing all the necessary details. Such documents, for example, could be:

- certificate from an accountant;

— calculation of the amount of advance payment for transport tax;

— tax accounting registers, etc.

The title of the document in this case does not matter. Similar clarifications are contained in the letter of the Federal Tax Service of Russia dated June 9, 2011 No. ED-4-3/9163.

If the organization uses the accrual method, include the amount of transport tax (advance payments) as expenses at the time of accrual - on the last day of the reporting (tax) period (subclause 1, clause 7, article 272 of the Tax Code of the Russian Federation). That is, on the date of drawing up the accounting certificate with the calculation of tax (advance payment). If the organization uses the cash method, include the amount of transport tax (advance payments) as expenses on the date of transfer to the budget (subclause 3, clause 3, article 273 of the Tax Code of the Russian Federation).

Situation: when calculating income tax, is it possible to take into account the amount of transport tax on a car that is not used in the production process (idled, leased, etc.)?

Answer: yes, it is possible, provided that the car is used in activities aimed at generating income.

When taxing profits, taxes accrued in accordance with current legislation (except for taxes mentioned in Article 270 of the Tax Code of the Russian Federation) are considered as other expenses associated with production and sales. The organization has the right to recognize such expenses on the basis of subparagraph 1 of paragraph 1 of Article 264 of the Tax Code of the Russian Federation.

However, when writing off certain expenses as a reduction in taxable profit, you need to take into account that all of them must be economically justified, documented and related to activities aimed at generating income. Such restrictions are established by paragraph 1 of Article 252 of the Tax Code of the Russian Federation. These restrictions also apply to taxes paid by the organization.

The economic basis for paying transport tax is the requirement of Chapter 28 of the Tax Code of the Russian Federation.

Documentary evidence of expenses can be a transport tax declaration and payment documents for the transfer of tax to the budget.

As for the connection between expenses and activities aimed at generating income, in relation to the transport tax on a car that is not used in the production process, such a connection is not obvious. The obligation to pay transport tax, provided for in Article 357 of the Tax Code of the Russian Federation, in itself does not confirm this connection.

Using a car for income-generating activities does not imply its daily operation. It is enough that the organization’s activities imply the presence of situations in which a car is necessary (transportation of goods, passengers, business trips of employees, etc.). Therefore, if for some time the car is idle, expenses in the form of transport tax on this car can be considered related to activities aimed at generating income.

The existence of such a connection can also be recognized if the car is leased. The rent received by the organization is income, therefore, paying transport tax for a rented car can be considered as one of the conditions for receiving this income.

Another thing is the transfer of a car for free use under a loan agreement (Article 689 of the Civil Code of the Russian Federation). Since in this case the vehicle is not used in activities aimed at generating income, during the audit the tax office may exclude transport tax from expenses for those periods when the car was used by the borrower.

In some cases, it is possible to expense the transport tax on a car that the organization does not own, but which has not been deregistered with the traffic police. For example, if the former owner contributed a car to the authorized capital of another organization and entered into an agreement with the new owner to lease this vehicle. Since the car was used in the production activities of the tenant, the FAS of the North-Western District recognized that the transport tax paid by him may reduce taxable profit, since in this case the criteria of paragraph 1 of Article 252 of the Tax Code of the Russian Federation are met (resolution of the FAS of the North-Western District of December 15, 2011 No. A66-5535/2011).

A stable arbitration practice on the issue under consideration has not developed. Thus, in each specific situation when the car is not used in the production process, the organization must independently decide whether to include transport tax as an expense. Moreover, if the tax inspectorate does not agree with the decision made, the organization will have to defend its position in court.

simplified tax system

If an organization applies a simplified tax system and pays a single tax on income, then when calculating the tax base, do not take into account the amount of transport tax (clause 1 of Article 346.18 of the Tax Code of the Russian Federation).

If an organization pays a single tax on the difference between income and expenses, include transport tax in expenses (subclause 22, clause 1, article 346.16 of the Tax Code of the Russian Federation). These payments will reduce the tax base on the day they are transferred to the budget (clause 2 of Article 346.17 of the Tax Code of the Russian Federation).

Do not take into account unpaid transport tax when calculating the single tax.

UTII

The object of UTII taxation is imputed income (clause 1 of Article 346.29 of the Tax Code of the Russian Federation). Therefore, expenses in the form of transport tax do not affect the formation of the tax base for UTII.

OSNO and UTII

If an organization combines a general taxation system and UTII, then the vehicle can be used in both types of activities simultaneously. In this case, the amount of transport tax must be distributed (clause 9 of Article 274 of the Tax Code of the Russian Federation).

If the vehicle is used in one of the types of activities, then the transport tax does not need to be distributed.

The amount of transport tax related to the activities of the organization on the general taxation system can be taken into account when calculating income tax. The amount of transport tax related to the activities of the organization on UTII cannot be taken into account for tax purposes.

An example of the distribution of transport tax expenses. The organization applies a general taxation system and pays UTII

LLC "Trading Company Hermes" (Elektrostal, Moscow region) sells goods wholesale and retail. For wholesale transactions, the organization applies a general taxation system. Retail trade has been transferred to UTII.

Hermes accrues income tax on a monthly basis. The accounting policy of the organization states that general business expenses are distributed in proportion to income for each month of the reporting (tax) period.

In March, the income received by Hermes from various activities amounted to:

— for wholesale trade (excluding VAT) – 12,000,000 rubles; — for retail trade – 4,000,000 rubles.

The organization uses several trucks to deliver goods to wholesale and retail customers. In March, an advance payment of transport tax for the first quarter in the amount of 10,300 rubles was charged from these vehicles.

Transport tax expenses relate to both types of activities of the organization. To distribute them, the Hermes accountant compared the income from wholesale trade with the total income.

The share of income from wholesale trade in total income for March is: RUB 12,000,000. : (RUB 12,000,000 + RUB 4,000,000) = 0.75.

The amount of the advance payment for transport tax, which can be taken into account when calculating income tax, is equal to: 10,300 rubles. × 0.75 = 7725 rub.

The amount of the advance payment for transport tax, which relates to the organization’s activities on UTII, is equal to: 10,300 rubles. – 7725 rub. = 2575 rub.

This amount (RUB 2,575) is not taken into account for tax purposes.

Calculation of transport tax under different taxation systems

Organizations using the simplified taxation system are not exempt from paying transport tax. Therefore, companies that have chosen the simplified tax system as a taxation regime calculate and pay transport tax in a similar manner to those companies that apply the general taxation regime in their activities.

Since at the moment they are not exempt from accounting, the transactions for calculating transport tax under the simplified tax system will be the same.

The basis confirming the calculation of the transport tax and its specific amount will be a certificate from an accountant.

Transport tax and its components

To correctly distribute the transport tax between the two regimes, you need to calculate what part is the income for each type of activity. To calculate the portion of income under OSNO, you must do the following: divide the amount of income under OSNO by income from all types of activities. The transport tax related to OSNO is determined by multiplying the amount of transport tax and the share of income received from OSNO. Transport tax related to activities on UTII is calculated in the same manner, using in this calculation the amount of income received on UTII. The sum of the results obtained from both calculations should give the total amount of accrued tax. About the division of expenses when simultaneously applying the simplified tax system and UTII, read the material “The procedure for separate accounting for the simplified tax system and UTII.” Results Independent calculation of transport tax is the prerogative of legal entities. The amount of transport tax related to the activities of the organization on UTII cannot be taken into account for tax purposes. To distribute the transport tax, it is necessary to determine the share of income received from different types of activities. In this case, the share of income from the activities of the organization on the general taxation system is calculated using the formula: Income from the activities of the organization on the general taxation system is divided into Income from all types of activities. Transport tax, which relates to the activities of an organization on the general taxation system, is calculated as follows: Transport tax is multiplied by the share of income from the activities of the organization on the general taxation system.

Account 68 in accounting

Account 68 is credited for amounts according to tax returns or calculations in correspondence:

- Account 99 - for the amount of accrued income tax;

- Invoice 70 - for the amount of personal income tax;

- Accounts 20, 25, 26, 44 - for the amount of local taxes, transport tax, property tax, etc.;

- Accounts 90.3, 91.2, 76.AV - when calculating VAT for the reporting quarter;

- Invoice 51 - upon receipt of overpaid tax from the budget.

The debit of the account records the amounts of taxes actually transferred to the budget, including the amounts of VAT written off from account 19.

Features of accounting

Like every tax, transport has its own accounting features. For example, a vehicle that is under repair and has not been used for some time is not exempt from taxation. It is subject to taxation for the entire period of repair.

If the tax is calculated for less than a month?

Transport tax is calculated from the moment, based on the full month of ownership of the vehicle.

Even if an organization registered a vehicle in the middle of the month, the tax must be paid for the full month.

For example, the company registered ownership of the bus on May 19. Tax will need to be paid for the full month of May. That is, the annual tax will be calculated based on 8 full months of bus ownership.

What are the postings under the simplified tax system?

Among the list of taxes from which enterprises using the simplified tax system are exempted, there is no transport tax. Therefore, “simplified” companies pay this tax on the same basis as enterprises under the general regime.

Subaccounts 68 “Calculations for taxes and fees”

Subaccounts under account 68 are used for taxes and fees paid by the company, depending on its chosen field of activity and tax regime. In this case, a separate sub-account is opened for each type of tax:

Additional sub-accounts can also be opened under account 68:

- 68.11 - UTII;

- 68.12 – simplified tax system;

- 68.13 – Trade fee.

What does it depend on

The tax is paid on a vehicle that is equipped with an engine. In this case, the calculation occurs for each horsepower. To get acquainted with the amount required to be paid, you need to know the following information

:

- tax rate in a specific region;

- number of horsepower;

- service life in months;

- multiplying factor for .

The tax rate is set in a specific region and depends on the engine size, environmental class and year of manufacture of the vehicle.

The tax base is established depending on the type of car. You can find this information in the vehicle passport or STS.

Paying transport tax is the responsibility of every person

. Therefore, it is worthwhile to independently calculate the amount to be paid annually, rather than wait for a notification from the Tax Service. It is necessary to pay the tax on time, otherwise, according to the law, penalties will follow with daily accrual on the principal amount of the debt. You can pay through the State Services portal and in the Sberbank terminal.

Every operation that occurs in the economic life of an organization must be recorded. The calculation of taxes is no exception. The presence of transport in an organization provides the basis for calculating transport tax, accruing and paying tax payments to the budget, as well as reflecting the transactions carried out in accounting entries.

Typical wiring

The main transactions for this account are presented in the table:

Get 267 video lessons on 1C for free:

- Free video tutorial on 1C Accounting 8.3 and 8.2;

- Tutorial on the new version of 1C ZUP 3.0;

- Good course on 1C Trade Management 11.

| Account Dt | Kt account | Wiring Description | A document base |

| 68 | 19 | Amounts of taxes actually transferred to the budget + VAT | Payment order |

| 68 | 50/51,52,55 | Payment of tax debts in cash or through a bank | Payment order |

| 70/75 | 68 | Personal income tax withheld from the income of employees or founders | Payslip |

| Based on settlement amounts for contributions to budgets | |||

| 99 | 68 | Income tax is reflected | Help-calculation |

| 70 | 68 | We reflect the amount of accrued personal income tax | Payslip |

| 90 | 68 | We reflect VAT, excise taxes, indirect taxes | Accounting information |

| 91 | 68 | We reflect financial results (operating expenses) | Certificate of calculation/Acceptance and transfer certificate |

Example 1. Postings to subaccount 68.01 “NDFL”

Postings for calculating personal income tax on account 68:

Example 2. Postings to subaccount 68.02 “VAT”

At Leto LLC based on the results of the 2nd quarter (core activities):

- VAT was charged in the amount of RUB 78,958;

- VAT accepted for deduction (advance) in the previous quarter in the amount of RUB 36,695 was restored;

- VAT on the sale of fixed assets amounted to RUB 7,959.

The accountant of Leto LLC reflected the accrual of VAT with the following entries:

Example 3. Postings to subaccount 68.04 “Income Tax”

To account for income tax calculations with the budget, subaccount 68.04.01 is used, and for tax calculations, a balance-free subaccount 68.04.02 is used, which is closed on account 68.04.01 at the end of the period.

Income tax is calculated on an accrual basis, taking into account advances of the reporting periods: quarter, 06 and 09 months and based on the results of the tax period - calendar year.

The accountant of Vesna LLC generated the following entries for subaccount 68.04 “Income Tax”:

Add a comment Cancel reply

You must be logged in to post a comment.

This site uses Akismet to reduce spam. Find out how your comment data is processed.

Postings for taxes

Entering account balances in the “Settlements” section

Account 68 “Calculations for taxes and fees”

Account purpose.

The account is intended to summarize information on settlements with budgets for taxes and fees paid by an organization, and taxes with employees of this organization.

Account 68 “Calculations for taxes and fees” is credited for the amounts due on tax returns (calculations) for contributions to budgets (in correspondence with account 99 “Profits and losses”, - for the amount of income tax, with account 70 “Settlements with personnel for wages” – for the amount of income tax, etc.).

The debit of account 68 “Calculations for taxes and fees” reflects the amounts actually transferred to the budget, as well as the amounts of value added tax written off from account 19 “Value added tax on acquired assets.”

Analytical accounting for account 68 “Calculations for taxes and fees” is carried out by type of tax.

Data input.

The account is a group account (yellow icon) and contains subaccounts that can only be used in transactions:

- 68.1 “Income tax for individuals”;

- 68.2 “VAT”;

- 68.3 “Excise duties”;

- 68.4.1 “Calculations with the budget”;

- 68.4.2 “Calculation of income tax”;

- 68.5 “Sales tax”;

- 68.7 “Tax on vehicle owners”;

- 68.8 “Property tax”;

- 68.10 “Other taxes and fees.”

Instead of subaccount 68.5 “Sales Tax”, you can enter several subaccounts for taxes and fees, the payers of which are your organization, for example, UTII - a single tax on imputed income, etc.

To do this, do the following:

- Exit the program;

- Enter the “Configurator” ;

- In the menu at the top of the screen, select the Configuration , and in it the line “Open configuration” . When you press “Enter” at this position, the system configuration will be displayed on the screen;

- In the configuration, select the “Chart of Accounts” and click on the “+” of this position. Sub-items of the chart of accounts will open. Select the line “Main” , click the mouse (or press the “Enter” ) and the configuration of the chart of accounts will be displayed on the screen;

- Move along the chart of accounts to line 68.5. Click the right mouse button. The menu will appear: “New line” “Delete line” “Copy” ;

- Go to the “Copy” and click;

- A copy of line 68.5 will be displayed at the bottom of the screen, available for editing;

- Correct 68.5 to 68.11, instead of “Other taxes” enter the name of the tax and fee for which this subaccount is entered (for example, UTII), and press “Enter” ;

- The screen will display the question “Will the account have subaccounts?” .

How is tax reflected when using two types of accounting?

In situations where UTII (single tax on imputed income) and simplified tax system (simplified taxation system) are simultaneously applied for different vehicles, the final payment amount must be divided. The division is made in proportion to income by type of activity, i.e. profit under the simplified tax system and profit under UTII are calculated separately.

For example, an organization sells goods at wholesale and retail prices. UTII is paid on income from retail sales, while wholesale sales are subject to VAT. The distribution of expenses depending on monthly revenue is as follows: wholesale trade brought the company 600 thousand rubles, retail – 200 thousand rubles. For transportation, 5 units of equipment are used, the tax on which is charged in the amount of 20 thousand rubles.

The calculation algorithm looks like this:

- 600 / (600 + 200) = 0.75 (75%) – income under the simplified tax system is divided by the amount received from all activities.

- 20 * 0.75 = 15 thousand rubles - the tax on cars according to the simplified tax system is equal to the product of the total tax amount and the part of the profit according to the simplified tax system.

- 20 – 15 = 5 thousand rubles - advance payment for UTII (payment under the simplified tax system is subtracted from the total tax amount).

Thus, when sharing regimes, tax distribution is mandatory. The final payment amount depends on the vehicle model, engine power and available benefits.

If an enterprise transfers automobile equipment under a free use agreement, then it does not receive income from the property. In such a situation, the law allows not to charge tax for the period when the movable property is in operation of a third-party enterprise.

Elizarov Artem

lawyer, specialist in automobile law

Articles and answers written

The owner of a vehicle always bears financial responsibility, and it does not matter whether he has one personal vehicle or an entire fleet serving a large business or a small business. All the same, reporting documents for the calendar year are submitted, rates for the income received are determined, and not only the company’s turnover, but also finances are monitored

Account 68 in accounting: postings, subaccounts, examples for dummies

Click on the answer “No” ;

- The new subaccount 68.11 will be displayed in the configurator's chart of accounts. Go to the right along the line of subaccount 68.11 to the subaccount1 column of this subaccount and press “Enter” ;

- A window with all possible subcontos will appear on the screen. Select a subaccount from this list with the name Types of payments to the budget and press “Enter” .

- tax accrued/paid;

- additional tax accrued/paid (independently);

- tax: additionally accrued/paid (according to the inspection report);

- fine: accrued/paid;

- penalties: accrued/paid.

You see that a new subaccount has appeared in the configurator's chart of accounts. Open the File (in the upper left corner of the screen), go to the “Save” , press “Enter” . Answer “Yes” and “Accept” to the questions that appear on the screen when saving the information. Enter program mode again. Open the chart of accounts and make sure that the subaccount you entered is in the chart of accounts. These subaccounts can only be used in journal entries.

For all subaccounts of account 68, except for subaccounts 68.4.1 and 68.4.2, single-level analytical accounting is provided: by types of payments to the budget - subconto1, which corresponds to a fixed set of types of payments (transfer):

Subaccount 68.4.1 provides for two-level analytical accounting:

- by types of payments to the budget - subconto1, which corresponds to the above fixed set of types of payments (transfer);

- for budgets – subconto2, which corresponds to a fixed set of payment types (transfer):

- federal;

- republican;

- local.

Accounting

In accounting, take into account the water tax on account 68 “Calculations for taxes and fees.” To do this, open a subaccount for it “Calculations for water tax” (Instructions for the chart of accounts).

The costs of paying the water tax are classified as expenses for ordinary activities (clause 5 of PBU 10/99). Therefore, reflect the water tax on the last day of the quarter (clauses 16 and 18 of PBU 10/99). In this case, make the following entries:

Debit 20 (21, 23, 25) Credit 68 subaccount “Calculations for water tax”

– water tax is charged;

Debit 68 subaccount “Calculation of water tax” Credit 51

– water tax has been paid.

This order follows from the Instructions for the chart of accounts (accounts 20, 21, 23, 25 and 68).

The procedure for reflecting water tax when calculating taxes depends on what taxation system the organization uses.

BASIC

When calculating income tax, include the amount of water tax among other expenses associated with production and sales (subclause 1, clause 1, article 264 of the Tax Code of the Russian Federation). These expenses are taken into account for profit tax purposes in full.

When expenses for paying water tax are taken into account when calculating income tax depends on how the organization recognizes expenses.

When using the accrual method, include the amount of water tax in expenses on the last day of the quarter for which the tax was accrued (subclause 1, clause 7, article 272 of the Tax Code of the Russian Federation).

If an organization uses the cash method, then the tax paid must be recognized as expenses on the day it is transferred to the budget (subclause 3, clause 3, article 273 of the Tax Code of the Russian Federation).

An example of how expenses for paying water tax are reflected in accounting and taxation. The organization applies a general taxation system

In accounting, the Alpha accountant reflected the accrual and payment of water tax as follows.

In tax accounting, the Alpha accountant included the amount of accrued water tax among other expenses in September and reflected it in the income tax return for nine months.

Is it possible to sell a car if the transport tax has not been paid?

You can sell a car with a transport tax debt in any case - debts do not affect the ability to draw up a purchase and sale agreement. But the question of whether the new owner will be able to register such a car in his own name is not so clear-cut.

1When will it be impossible to re-register a car with transport tax debts?

The buyer will not be able to register a car if it has restrictions on registration actions. Bailiffs have the right to impose such a ban if the owner has evaded paying taxes for a long time and enforcement proceedings have been initiated against him.

You can see if a car has a registration restriction on the official website of the State Traffic Safety Inspectorate. To do this, go to the “Car Check” service in the “Services” section on traffic police.rf and enter the car’s VIN code in a special form.

If there is such a restriction, you should first pay off your debts, wait until the enforcement proceedings are closed, and only then sell the car.

2When can you sell a car?

If you have a small debt to the tax office and no enforcement proceedings have been initiated, you can sell the car. However, you will still have to pay off the debt and also pay a new tax for the year in which you sold the car.

The tax amount in this case will be calculated taking into account the number of full months of car ownership (calculated from January to the month of registration of the car for the new owner). For example, if you sold a car and the new owner registered it in his name on March 20, 2021, in 2021 you will have to pay 3 months of car tax.

Remember that the tax for a sold car ceases to be calculated not from the date of drawing up the purchase and sale agreement, but from the date of registration of the car with the traffic police. Until the new owner registers the car in his name, you will pay for it.

Taxes 2017 for dummies. A short excursion.

Much has been written and said on this topic. That's why we offer you a short “2021 Tax Summary” to help you cover the whole picture.

The state has two news for you: good and “as usual.”

The good news is that there are tax breaks.

Oil tycoons who love to change currency and sell scrap metal will be in seventh heaven:

- now they will not have to pay a 2% tax on foreign exchange transactions;

- rent rates for oil production fell by half: from 45% to 29%;

- The tax on the delivery of scrap metal has been eliminated.

As you can see, these are very useful and necessary concessions.

The news “as usual” is the essence of our entire subsequent article.

Without going into heartbreaking details, we will briefly describe the situation using current interest rates as an example:

- Excise taxes:

- The excise tax on gasoline increased by 42 €/1000 l;

- Excise taxes on fortified and sparkling wines - by 12%;

- Excise taxes on other alcohol - by 20%;

- Excise tax on tobacco products is 40%.

- Rent rate:

- for the use of radio frequencies has increased (incl.

500 times for 4G frequencies);