Every business has assets. These are material assets and investments, money that allows the company to engage in core and auxiliary activities. Account 58. Financial investments is an item that is needed to reflect in the accounting records the enterprise’s financial investments in securities of various types, make contributions to the company’s capital, issue interest-bearing loans and carry out other operations.

More details about transactions using account 58 will be discussed in the article. A real example will be given for novice accountants.

Scope of application

To display information about which funds should be regarded as financial investments, account 58 is used in the chart of accounts.

Structure of Article 58

Through this PBU article you can display:

- government securities;

- municipal central banks;

- bills, bonds of other companies;

- investments in the authorized capital of other companies;

- interest-bearing loans provided to other companies;

- deposit investments;

- receivables received on the basis of assignment of claims.

Financial investments account 58, subaccounts and other items corresponding to the specified item are used.

Important! Investments in a company's own securities cannot be considered financial investments. This does not include bills issued for manufactured products, purchased “jewelry,” or objects of art.

Shares and shares

The management of an enterprise can invest in the authorized capital of various commercial organizations, purchase their shares, that is, invest in third-party companies. Such activities can be carried out:

- In the form of a cash contribution through the purchase of shares.

- By transferring various types of intangible and tangible assets.

- In the form of direct investment of funds into capital.

All these options significantly complicate the characteristics of subaccounts. 58.1. It can thus be called:

- Material account. In this case, the material assets contributed to the capital of a third-party company are taken into account.

- Money account. In this case, one should proceed from the position in which it is located by the developers of the Plan, as well as from the possibility of quick liquidity of securities.

- Current account. This is explained by the fact that in all cases there is a relationship between the entities providing capital and the entities receiving it.

As a result, in accordance with these interpretations, three versions of accounting arise. Let's look at them.

What are the subaccounts?

Account 58 is not used in accounting in its “pure” form. This article acts as the main one, which takes into account data from all existing sub-accounts.

Picture 4. Subaccounts

To separately account for amounts received in different currency units, an enterprise accountant can open sub-accounts:

- 58 1 - statutory contributions, contributions to joint-stock companies;

- 58 2 — investing in securities;

- account 58 3 - loans provided to citizens to companies in any form. It is 58 subaccount 03 that is often used in accounting;

- 58 4 - contributions to common property under a simple partnership agreement.

On a note! The number of subaccounts is not limited to those indicated, since it is necessary to maintain analytical accounting for each group of objects. An accountant can open additional sub-accounts if this is specified in the company's accounting policies. The most commonly used count is 58 03.

How does Article 58 correspond to other accounts?

In addition to the main characteristics of the article, it is worth having an idea of which accounting accounts it corresponds with.

There are several accounts that enter into a “relationship” with the 58th account in debit and credit. We are talking about the following articles.

| Debit | Credit |

| 50, 51, 52, 75, 76, 80, 91, 98 | 51, 52, 76, 80, 90, 91,99 |

The main purpose of account 58 is to collect and summarize data on invested funds and other assets of the company in profitable activities.

Accounting for loans from the lender - entries for issuing loans

If a company issues a loan to another organization, then the transactions will be as follows:

- Debit 58 Credit 51 (50, 52, 40 ...) – entry for the loan issued.

As can be seen from the posting, a loan can be provided not only in the form of a sum of money, but also in the form of property (materials, fixed assets, etc.). The amount that will be taken into account in this case is the value of goods/materials, etc.

When issuing an interest-free loan to a legal entity, the amount is taken into account in the debit of account 76 and the credit of the account for issuing funds or property (50, 51,10, 40, etc.).

Loan repayment is documented by posting:

- Debit 51 (50, 40...) Credit 58 (76).

Regarding the taxation of loans with VAT, there are two opposing points of view. The first is based on the fact that there is a transfer of ownership, which is an implementation (Article 39 of the Tax Code of the Russian Federation). Sales are subject to VAT. The opposite point of view: when receiving and returning a loan in the form of goods, there is no object of VAT taxation.

Entries for VAT accounting on loans in kind:

- Debit 91.2 Credit 68 VAT – when issuing a loan

- Debit 19 Credit 58 (76) – accounting for input VAT when repaying the loan.

The issuance of a loan to an employee of an organization is documented by posting:

- Debit 73 Credit 50 (51).

The return is processed by return posting.

Example:

The organization issued an interest-free loan to a legal entity in the amount of 320,000 rubles.

Postings for issuing a loan:

| Account Dt | Kt account | Wiring Description | Transaction amount | A document base |

| 76 | 51 | Issuing an interest-free loan | 320 000 | Payment order ref. |

| 51 | 76 | Loan repayment | 320 000 | Bank statement |

Posting account 58 in accounting

The PUB also shows the transactions used to display all operations using account 58. Let's look at the transactions for account 58 in more detail in the table:

| Operation description | Debit | Credit |

| The securities were purchased for foreign currency. | 58-1 | 52 |

| The bonds were paid from a current ruble account. | 58-2 | 51 |

| The loan was issued to another company with materials. | 58-3 | 10 |

| Under a simple partnership agreement, the fixed asset was transferred as a contribution to the management company. | 58-4 | 1 |

| The difference between the initial cost of the bond and the current market price was included in the financial results. | 58-2 | 91 |

| Revaluation of shares at market value as of the current date. | 91 | 58-1 |

| Payment on a bill. | 51 | 58-2 |

| The previously issued loan was returned by bank transfer. | 51 | 58-3 |

| The intangible asset transferred under a simple partnership agreement was returned. | 4 | 58-4 |

The presented entries were compiled using not the main financial investment account, but sub-accounts opened in the accounting of the enterprise. In the table presented, the debit of account 58 shows that the assets of the enterprise were transferred to another organization, and the passive position of the sub-accounts reflects the assets received by the company.

On a note! Every accountant must know that account 58 in the balance sheet is indicated on lines 1170 and 1240.

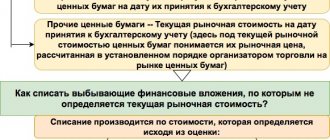

Write off account 58 postings

In the first case, we are talking about documents based on the property right to a certain asset.

If we are talking about derivatives, then in this case we are talking about a non-documentary form of right to property that appears due to a change in the value of the financial instrument that underlies it.

If we take the form of issue as a basis, then we can distinguish issue-grade securities, for example, shares, and non-issue securities, for example, checks and bills. If we classify documents according to the order of ownership, then we should distinguish registered, order and bearer papers.

In practice, there are a lot of other criteria by which designated monetary settlement documents can be classified. The designated account is designed to provide detailed accounting of the company’s cash investments. Analytics for this account is carried out in separate sub-accounts, including: 1 – accounting for investments in shares and shares; 2 – investing in debt instruments.

Account 58 “Financial investments” of the new chart of accounts

Sub-accounts can be opened to account 58 “Financial investments”: 58-1 “Units and shares”, 58-2 “Debt securities”, 58-3 “Loans provided”, 58-4 “Deposits under a simple partnership agreement”, etc. Subaccount 58-1 “Shares and shares” takes into account the presence and movement of investments in shares of joint-stock companies, authorized (share) capitals of other organizations, etc.

Subaccount 58-2 “Debt securities” takes into account the presence and movement of investments in government and private debt securities (bonds, etc.). At

RUB 132,457 Loan agreement 5,158.3 Funds credited from Etude LLC to repay the debt on a previously provided loan RUB 1,415,300.

Bank statement 5176 Funds have been credited from Etude LLC to pay off interest debt 132.457 rubles. Bank statement About account 51 (current account) it is written in detail in the article: ““.

(understand how to do accounting in 72 hours) > 8000 books purchasedHidden text

- purchase price – 1315 rubles.

- nominal value - 1241 rubles;

The issuer of the bond is Megapolis JSC. For this bond, you must receive two coupon payments, each of which is 15% of the bond's par value (1,240 rubles * 15% = 186 rubles).

The accountant of Stolitsa JSC carried out the following accounting transactions: DebitCreditDescriptionAmountDocument 58.251 Funds were transferred as payment for the purchased bond. The receipt of the purchased bond1 is taken into account.

315 RUR Payment

Accounting account 58

In addition, in analytical accounting, financial investments should be divided into short-term and long-term.

58-2 “Debt securities” Investments in government and private debt securities (bonds, bills, etc.) 58-3 “Loans provided” Cash and other loans provided to legal entities and individuals 58-4 “Deposits under agreement simple partnership" Contributions to common property under a simple partnership agreement Let us present in the table some standard accounting

Wiring Dt 58 and Kt 58 (nuances)

The organization also has the right to open its own sub-accounts to account 58 for the financial instruments it uses, which must be reflected in the working chart of accounts. Dt 58 - Kt 58 are used in conjunction with the following accounts:

- 76 “Settlements with various debtors and creditors”;

- “Other income and expenses”, etc.

- 52 “Currency accounts”;

- 51 “Current accounts”;

- 80 “Authorized capital”,

Let's look at several examples of using accounts Dt 58 - Kt 58.

Example 1 Zarya LLC issued a loan to another organization. At the same time, Zarya LLC will reflect the entries: Dt 58.03 Kt 51 - loan issued.

Account 58 in accounting. financial investments. postings

According to subaccount.

58.2 is the movement of deposits in private and government debt securities.

These include, in particular, bonds. In the course of its activities, an enterprise can invest in various assets.

All these investments go to account 58. In accounting, these investments are debited.

76 and Kd sch. 58 and 91. The debit is the amount of income due to be received. The loan reflects the difference between the funds allocated to the account.

76, recording settlements with debtors and creditors, and account.

Accounting: account 58 “Financial investments”

The debit displays financial investments in securities in correspondence with the corresponding accounts for recording valuables transferred as investments (for example, money from accounts 50,51,52). Repayment or sale is carried out in accounting according to Kt58 in correspondence with the account.

91 (90). Investments in securities, the current value of which is determined, are subject to monthly or quarterly revaluation in order to include assets in the annual financial statements. The adjustment amount is applied to the company’s financial results (91.01, 91.

02) For debt securities that are not traded on the market, the difference between the original price and the nominal price is applied to the financial results of the organization’s activities evenly over the period of their circulation and receipt of income. 58.

3 – mutual settlements for borrowed amounts presented to legal entities and individuals are displayed.

Source: https://KonsulAN.ru/spisanie-scheta-58-provodki-34341/

Posting examples

The final paragraph provides a specific example of using postings with subaccounts 58 accounts for beginners. The Cactus company sells exotic plants.

Example of a balance sheet for account 58

During the first quarter of this year, the company bought shares for 10 thousand dollars and issued a loan to another company that supplies them with turf for infrastructure development in the amount of 200 thousand rubles. At the end of the reporting period, the loan was returned to the current account. The accountant revalued the shares, with an increase of 10% at the market rate. Let's create the entries that the accountant of the Cactus company must make.

- Dt. 58-1 - Kt.52 - $10,000 - shares purchased for foreign currency.

- Dt. 58-3 - Kt.51 - 200,000 rubles - loan to another company engaged in the supply of turf.

- Dt. 91—Kt. 58-1 - $1000 - revaluation of shares with an increase of 10%.

- Dt. 51—Kt. 58-3 - 220,000 rubles - loan repayment with interest.

In conclusion, Article 58 is used mainly by companies that work closely with third parties and often make various financial investments. The accounting department keeps records of open sub-accounts, and the final indicators are formed on the main account - 58.

https://www.youtube.com/watch?v=eRVeCaNt6hs