We charge penalties in 2021 for a budgetary institution

Having considered the issue, we came to the following conclusion: Any penalties, fines and other sanctions transferred to budgets (extra-budgetary funds) can be taken into account by public sector organizations on account 0 303 05 000 “Settlements for other payments to the budget” with attribution to account 0 401 20 200 “Expenses of an economic entity.”

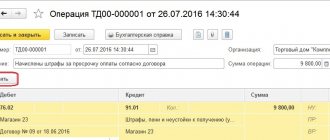

The amount of money reimbursed by the guilty person should be considered as compensation for the institution’s costs, to be reflected in account 0 209 34 000 “Calculations for compensation of costs.” Rationale for the conclusion: In accordance with paragraphs. 4 paragraphs 1 art. 23 of the Tax Code (hereinafter referred to as the Tax Code of the Russian Federation), taxpayers are required to submit tax returns (calculations) to the tax authority at their place of registration. According to Part 1 of Art. 119 of the Tax Code of the Russian Federation, failure to submit a declaration (calculation of insurance premiums) to the tax authority at the place of registration within the prescribed period entails a fine in the prescribed amount. In accordance with paragraph 1 of Art. 75 of the Tax Code of the Russian Federation, penalties are recognized as the amount of money established by this article, which the taxpayer must pay in the event of payment of due amounts of taxes or fees later than the deadlines established by the legislation on taxes and fees. Thus, the obligation to pay penalties and fines arises specifically from the taxpayer - the budgetary institution. Reflection in the accounting of transactions for the acceptance of such obligations, as well as their fulfillment, cannot be linked to the reimbursement of any funds from individuals or legal entities. In accordance with the Instructions approved by Order of the Ministry of Finance of Russia dated 01.07.2021 N 65n (hereinafter referred to as Instructions N 65n), expenses for payment of fines and penalties (including for late payment of taxes (contributions)) are reflected in CVR 853 “Payment of other payments” in connection with Article 290 “Other expenses” of KOSGU. From 01/01/2021, this article of KOSGU is detailed by subarticles of KOSGU 291-296. Thus, the costs of paying penalties, fines for violation of the legislation on taxes and fees, legislation on insurance premiums are included in subsection 292 of KOSGU * (1). Calculations for the transfer of penalties and fines to the budget can be taken into account by public sector organizations on account 0 303 05 000 “Settlements for other payments to the budget” * (2). Expenses associated with the payment of penalties and fines accounted for on account 0 303 05 000 are not included in the cost of products (works, services), but are charged to the financial result of the institution - to account 0 401 20 200 “Expenses of an economic entity” (paragraph 8 p 131 Instructions for the application of the chart of accounts for accounting of budgetary institutions, approved by Order of the Ministry of Finance of Russia dated December 16, 2021 N 174n, hereinafter referred to as Instruction N 174n). As a rule, judicial practice is based on the fact that payment of taxes and related penalties is the legal obligation of the organization and, accordingly, such expenses cannot be considered as direct actual damage. Therefore, making a decision to collect penalties from the guilty employees against the institution in the manner of holding them materially liable is inappropriate. However, this does not exclude the possibility of voluntary reimbursement by guilty persons of the institution’s expenses incurred in connection with the imposition of such penalties on the institution. We believe that in the situation under consideration, the amount of money reimbursed by the guilty person should be considered as compensation for the costs of the institution. Such revenues, according to Instructions No. 65n, must be reflected in accounting using subarticle 134 “Income from compensation of costs” of KOSGU. This KOSGU code corresponds to account 0 209 34 000 “Calculations for compensation of costs” (clauses 108, 109 of Instruction No. 174n). As a general rule, budgetary institutions reflect the accrual of any income on the debit of account 209 00 and the credit of account 401 10 only using the financial security code “2” - income-generating activity (letter of the Ministry of Finance of Russia dated November 9, 2021 N 02-06-10/65506). This accounting procedure does not prevent the organization from making an independent decision: - on the allocation of funds for expenses related to the implementation of government tasks; — on the transfer of received funds to budget revenues. Thus, in the situation under consideration, the following correspondence accounts can be reflected in the accounting of a budgetary institution: 1. Debit 4,401 20,292 Credit 4,303 05,730 - penalties and fines were accrued based on the request of the tax authority; 2. Debit 4,303 05,830 Credit 4,201 11,610 Increase in off-balance sheet account 18 (KVR 853, KOSGU 292) - penalties and fines paid; 3. Debit 2,209 34,560 Credit 2,401 10,134 - accrued income from compensation of expenses of the institution; 4. Debit 2,201 11,510 Credit 2,209 34,660 Increase in off-balance sheet account 17 (AnKVD 130, KOSGU 134) - funds voluntarily contributed by the guilty person were credited to the personal account.

Reflection of fines and penalties

Reflecting transactions with penalty amounts in the accounting of government institutions has its own characteristics depending on their type and traditionally raises many questions among accountants.

No time to read? Cheat sheet on the contents of the article:

- What is the difference between the concepts of “forfeit”, “fine” and “penalty”

- What legislation regulates the payment of penalties?

- 3 ways to collect penalties

- What transactions should be used to charge penalties to state-owned, budgetary and autonomous institutions?

- What indicators are reflected in the reporting forms?

What is a penalty

In accordance with the Civil Code of the Russian Federation, a penalty is a sum of money that the debtor is obliged to pay to the creditor in the event of non-fulfillment or improper fulfillment of an obligation, in particular, for its delay (Article 330). Moreover, the agreement on the penalty must be made in writing, regardless of the form of the main obligation, otherwise it is declared invalid (Article 331).

There are two types of penalties: a fine or a penalty. The fine is a fixed payment and can either be specified as a fixed amount or calculated as a percentage of a particular amount. The penalty is a variable value, its size depends on the duration of the period of violation. The amount of the penalty is determined as a percentage of the amount of the obligation, the fulfillment of which it ensures.

The rules for calculating penalties are also determined by the Civil Code of the Russian Federation.

The first day of delay is the date following the day of fulfillment of the obligation in accordance with the contract. Last day is the date preceding the day of actual fulfillment of the obligation. Example.

According to the terms of the contract, the deadline for fulfillment of obligations by the supplier (contractor) is defined as follows: “no later than June 20, 2021.” The goods were actually delivered on July 20, 2021. The period of delay lasted from June 21 to July 19 and amounted to 29 days.

Penalty when purchasing services

In addition to the Civil Code of the Russian Federation, the concept of a penalty, the procedures for its calculation and collection when purchasing services for state (municipal) needs are defined in Art. 34 “Contract” of Federal Law No. 44-FZ (hereinafter referred to as the Law). According to clause

4 securing the responsibility of the customer and supplier (contractor, performer) for non-fulfillment or improper fulfillment of obligations stipulated by the contract are a mandatory condition of the contract. P.

6 contains requirements for the payment of penalties in case of delay in fulfilling obligations and in other cases of non-fulfillment (improper fulfillment) of obligations.

However, the Law also provides for a number of exceptions when the above requirements may not apply (Clause 15, Article 34). Exceptions include purchases from a single source, for example, for an amount not exceeding 100,000 rubles, or goods, works or services related to the scope of activity of natural monopolies.

According to the Law, in certain cases, in the manner prescribed by the Government of the Russian Federation, it is possible to grant a deferment in the payment of accrued amounts of penalties or to write them off. One of the criteria required for write-off is the size of the total amount of unpaid penalties. It should not exceed 5% of the contract price.

Methods for collecting penalties

In the terms of the contract (agreement), it is recommended to immediately specify the method of collecting the penalty. There are three ways:

Separately, it should be said about the right to dispose of received funds, which depends on the type of institution.

In paragraph 3 of Art. 41 of the Budget Code of the Russian Federation, a penalty is included in non-tax budget revenues from liability measures for violating the terms of a civil transaction. Amounts received by a government institution are accordingly subject to inclusion in budget revenues.

Budgetary or autonomous institutions have the right to spend the amounts received in accordance with the FCD Plan, since such receipts are their non-operating income. It is only necessary to make timely changes in the prescribed manner to the FCD Plan, increasing the total amounts of receipts and disposals and determining the directions of expenditure.

Reflection of transactions in accounting

The accrual of the presented amounts of penalties (fines, penalties) is documented by posting

D-t (KDB) X. 209.40. (560) or

(KDB) X. 205.41. (560)

Kit (KDB) X. 401.10. (140)

Where X is the source of financial support depending on the type of institution (1 – state-owned, 2 – budgetary, autonomous).

The program uses the document “Accounting operation (manual)”

.

Correspondence regarding the receipt of the collected penalty in accordance with Instructions No. 162n, No. 174n and No. 183n should be reflected in accounting depending on the type of institution.

Correspondence in a government agency

Upon receipt of payment of the penalty from the supplier of correspondence in a government institution, the following will occur:

To pay under the contract

In the case under consideration, the resulting counterclaim (penalty) presented to the supplier (contractor) is counted towards payment of the institution’s obligations under the contract.

When choosing this calculation method, a government institution must take into account several factors:

- It is advisable to include in the contract a condition that the fulfillment of obligations to transfer the penalty to budget revenue is assigned to the state customer;

- transfer the penalty yourself to budget revenue (the name of the counterparty for whom the penalty is transferred should be indicated in the payment document);

- make changes to the indicators of the budget obligation taken into account by the FC body.

It should be noted that the Budget Code of the Russian Federation does not provide for the execution of the budget by income by offsetting expenditure obligations (Article 218 of the Budget Code of the Russian Federation). Let's consider a separate case when the contract is executed at the expense of subsidies allocated for other purposes (capital investments) and located in a separate personal account of the institution. Correspondence regarding the termination of the counterclaim is reflected (based on certificate f. 0504833). Writing off in accounting the amounts of penalties from funds in temporary disposal and reflecting them as income:

D-t (city of KBK) 3. 304.01 (830)

Accrual of penalties for transactions with a budgetary institution in 2021

If penalty payments are assessed by the company independently, then they must be reflected on the date of calculation and payment to the budget. When accruing based on the results of an audit, they should be reflected on the date the audit decision came into force. Accounting for settlements with the budget for taxes is organized, in accordance with the chart of accounts, on account 68. If penalties are accrued on contributions, accounting entries are reflected on account 69. For the convenience of monitoring the accrual and payment of penalties for tax payments, their analytical accounting should be organized in the context relevant taxes. For example, when calculating penalties for VAT, transactions must be reflected in the subaccount of account 68, opened to record the accrual of this tax.

We recommend reading: Liability of the founder of a municipal enterprise for damage

But this standard does not determine the procedure for displaying tax sanctions, including penalties. Some explanations from representatives of the Ministry of Finance of the Russian Federation boil down to the fact that penalties should be displayed on account 0.303.05.000, relating to settlements with the budget for other payments. This is explained by the fact that penalties cannot be considered taxes or other mandatory fees; they should be classified as other payments paid to the budget. In order to maintain separate accounting in relation to tax sanctions and other payments due for payment to the budget, it is rational to open a sub-account to account 0.303.05.000. Postings for accrual of penalties for taxes in budget accounting are made as follows: Dt 0.401.20.290 Kt 0.303.05.730 subaccount “Penies” Whatever method is chosen by the organization, it must be fixed in the accounting policy of the enterprise. As a rule, the choice of method is determined by the qualifications and experience of the accountant.

Accounting entries in government institutions penalties

The emergence of obligations to pay a penalty, its accrual, as well as the determination of the procedure for fulfilling the monetary obligation of an institution under a state contract can be made on the basis of an act of acceptance of goods, work, services or other document provided for by business customs, in which information about the fulfillment of the obligation by the contractor must be indicated , on the accepted results of contract execution, including the amount of penalties, fines Letter from the Ministry of Finance of the Russian Federation dated In this case, it is necessary to indicate the reason for making changes in text form and attach a document confirming the decision made in the form of an electronic copy created by scanning Letter from the Federal Treasury from Procedure for settlements with executor In this section we will consider the procedure for settlement of institutions with executors within the framework of concluded contacts of civil contracts.

Calculation of penalties in a government posting institution

My profile Favorites Billing Personal blog. OFD Opinions User Agreement Rules for the use of materials. Source: Journal » Institutions of physical culture and sports: accounting and taxation » State municipal contracts, as well as civil contracts, provide for conditions on the liability of the supplier of the contractor, the contractor for non-fulfillment or improper fulfillment of obligations and on the payment of penalties in favor of the institutions.

We recommend reading: Maternity Capital Transfer Deadline 2021

In accordance with the Chart of Accounts (Order of the Ministry of Finance dated October 31, 2000 No. 94n), the amounts of tax penalties due are reflected in the debit of account 99 “Profits and losses” in correspondence with the account for accounting settlements with the budget for taxes.

Accounting entries for accrual of penalties for taxes in 2021

If an organization has not paid taxes on time and there is not a sufficient amount of funds in its current account, then the tax authorities have the right to forcibly collect taxes and accrued penalties from the debtor’s property.

Otherwise, a penalty will be charged at the initiative of the Federal Tax Service. A fine is not a tax penalty, but is related to tax obligations. Therefore, accountants often have a question about how to correctly reflect penalties in accounting.

We take into account penalties and fines in tax accounting and prepare entries

Fines and penalties are what determine financial liability for failure to fulfill obligations. There are two types of liability that are different from each other. One of them relates to the contractual sphere and is regulated by civil law, and the second by tax law.

Having such documents is extremely important when you reflect penalties and interest in tax accounting. This becomes especially important at the turn of tax periods. For example, the debtor recognized a penalty in 2020, but paid only in 2021. The amount of the penalty must be included in the 2021 tax return.

We recommend reading: Types of annuity agreements

Calculation of penalties under a contract in a budgetary institution

According to paragraph 6 of Rules No. 1063, for each day of delay, the supplier (performer, contractor) is charged a penalty in the amount of at least 1/300 of the key rate of the contract price. The rate is taken on the date of payment of penalties (as in the case of the customer). And the contract price should be reduced by an amount proportional to the volume of obligations that the counterparty actually fulfilled. The amount of sanctions for the supplier is determined according to the Rules approved by Decree of the Government of the Russian Federation of November 25, 2021 No. 1063 (Rules No. 1063). To calculate the amount, formulas from Rules No. 1063 are used. In this case, it is necessary to take into account Decree of the Government of the Russian Federation of December 8, 2021 No. 1340 (hereinafter referred to as Resolution No. 1340). It says that for relations regulated by acts of the Government of the Russian Federation in which the refinancing rate of the Central Bank of the Russian Federation is used, from January 1, 2021 it is necessary to apply not it, but the key rate, unless otherwise provided by federal law.

For a long time, the refinancing rate remained at 8.25 percent per annum (Instruction of the Central Bank of the Russian Federation dated September 13, 2021 No. 2873-U). However, starting from 2021, it has been equated to a key one. As a result, the refinancing rate has lost its former meaning and is now only a formal value that appears in many legislative acts. Let's find out how the accrual of penalties will change in connection with these innovations. The contract system is based on the provisions of the Civil Code of the Russian Federation. This is stated in Part 1 of Article 2 of Federal Law No. 44-FZ of April 5, 2021 (hereinafter referred to as Law No. 44-FZ). Thus, a contract is understood as a civil agreement, which can be concluded, among other things, by a budgetary institution in accordance with parts 1, 4 and 5 of Article 15 of Law No. 44-FZ. And one of the mandatory conditions of contractual relations is the liability of counterparties for non-fulfillment or improper fulfillment of obligations (Part 4, Article 34 of Law No. 44-FZ).

Postings in the budget for penalties under the contract

If the contract is not fulfilled in full If the supplier (contractor, performer) has not completed the work provided for by the contract in full, the customer has the right to terminate such a contract unilaterally or judicially, as well as to collect a penalty for improper fulfillment of obligations under the contract, or has the right to return the security for the performance of the contract, reduced by the amount of accrued fines and penalties (letter of the Ministry of Economic Development of Russia dated April 10, 2021 N D28i-1555). If, however, there was a delay in fulfilling obligations (including guarantees) due to the fault of the supplier, then the customer sends to the supplier ( contractor, performer) requirement to pay penalties (fines, penalties) (Part 6, Article 34 of Law No. 44-FZ).

Thus, submitting a demand for payment of penalties is an obligation and not a right of the customer institution. The penalty is divided into fines and penalties. Fines If the contract is not fulfilled in full In the event that the supplier (contractor, performer) performed the work provided for by the contract not in full , the customer has the right to terminate such a contract unilaterally or in court, as well as to collect a penalty for improper fulfillment of obligations under the contract, or has the right to return the security for the performance of the contract, reduced by the amount of accrued fines and penalties (letter of the Ministry of Economic Development of Russia dated April 10, 2021 No. D28i-1555 ).

How will the accrual of penalties for late utility payments change in 2021?

For an individual - that is, for the majority of consumers of utility services - the amount of the penalty will depend on exactly how many days the payment was not made. Previously, it was like this: penalties were accrued if you did not pay by the 10th day of the month following the month of accrual. Now the following scheme applies:

We recommend reading: Property at FSSP auction

As is known, in addition to penalties, resource supply organizations have the right to limit or completely stop the supply of electricity, heat, water and gas. Of course, before cutting off a consumer from an energy resource, there will be several warnings.

Calculation of Penalties Budgetary Institution 2021

PBU 9/99, Order of the Ministry of Finance dated October 31, 2021 No. 94n): Debit account 76 “Settlements with various debtors and creditors”, subaccount “Settlements on claims” - Credit account 91 “Other income and expenses” Administrative fine: accounting entries Thus, the accrued fine for violating traffic rules will correspond to the following accounting entry: Debit account 91 – Credit account 76 A similar entry will reflect the accrual of a fine by the labor inspectorate and other similar authorities. Consequently, payment of an administrative fine will be reflected as follows: Debit of account 76 – Credit of accounts 50 “Cash”, 51 “Cash accounts”, etc. A separate sub-account “Administrative fines” can be opened for account 76.

Having considered the issue, we came to the following conclusion: Any penalties, fines and other sanctions transferred to budgets (extra-budgetary funds) can be taken into account by public sector organizations on account 0 303 05 000 “Settlements for other payments to the budget” with attribution to account 0 401 20 200 “Expenses of an economic entity.” The amount of money reimbursed by the guilty person should be considered as compensation for the institution’s costs, to be reflected in account 0 209 34 000 “Calculations for compensation of costs.”

Penalty: how to calculate, demand and reflect in accounting

Accounting A penalty is a payment for violation or non-fulfillment of the terms of an agreement or government contract. Moreover, the size of the fee is determined according to a certain algorithm. In the article we will talk about the concept of a penalty, how to calculate the amount, and also determine how to reflect it in the accounting of a budgetary institution.

September 4, 2021 Evdokimova Natalya

The basis of the relationship between business partners is an agreement or government contract. If one of the parties, the customer or the contractor, violated the terms of this agreement, then the other party has the right to demand compensation. This monetary compensation is called a penalty.

In some cases, penalties are applied in the form of fines or penalties.

Article 330 of the Civil Code of the Russian Federation establishes that compensation can be obtained under the conditions stipulated in the contract itself, or according to legislative norms. However, in both cases it will be necessary to prove that the defendant party actually violated the obligations.

In addition to compensation, the injured party has the right to demand compensation for losses or other expenses that were aimed at eliminating the adverse consequences. However, these expenses will also have to be proven. And in most cases through the courts.

How to calculate

Calculate the amount of the penalty, guided by the provisions of the contract. If the agreement does not contain conditions for the application of penalties to the guilty party, then make calculations based on Decree of the Government of the Russian Federation No. 1042 of August 30, 2017.

It is worth noting that for some areas, for example, in the gas supply or electricity sectors, penalties will have to be calculated individually, since officials have provided exceptional requirements for these areas of activity.

When calculating penalties, consider the following indicators:

- The amount of the unfulfilled obligation. It is important to note that only that part of the contract that was not fulfilled on time should be accepted for calculation, unless otherwise provided by the rules of the contract.

- The system of taxation of the culprit. If the company is the defendant on OSNO, then calculate the amount of compensation and fines taking into account VAT. For companies that have chosen simplified systems, calculate the amount without VAT.

- Duration of breach of obligation. Calculate the period of delay from the next day after the day on which the obligations under the contract should have been fulfilled. For example, the delivery date is July 20, therefore, consider the delay from July 21.

- The refinancing rate set by the Central Bank of Russia at the time of imposing penalties on the guilty party.

If the obligations were fulfilled the next day, then there are no grounds for imposing penalties and fines. For example, the contract deadline is August 10, but if the obligations are fulfilled on August 11, then penalties cannot be imposed.

Having determined the main indicators for calculation, calculate the amount using the formula:

Can the penalty exceed the amount of the principal debt? Maybe, for example, if the deadline for fulfilling obligations is delayed for a long time. However, the court may decide to reduce the amount of the fine taking into account its disproportionate nature. The court also has the right to reduce accrued penalties if payment was not made due to disputes between the parties. Or due to the inability to make calculations.

How to claim

The procedure for issuing a penalty has its own characteristics. Follow the following algorithm:

- Record the violation in a special act or other document. For example, draw up a separate act in which you indicate in detail all types of violations identified. Or record the circumstances in the transfer documents (certificate of completed work, delivery note).

- Calculate the amount of compensation. Determine the amount of penalties according to the rules indicated above. Count the fee not from the entire contract amount, but only from the amount of unfulfilled obligations. Before calculating, check the refinancing rate of the Central Bank of Russia.

- Prepare a claim against the violator. Indicate the norms and clauses of the agreement that were not fulfilled on time. Describe the entire essence of the complaint, provide links to regulatory legislation. Record demands for payment of penalties.

- Go to court. If it is not possible to reach an agreement with the counterparty, then it is permissible to withhold compensation from the amounts to be transferred, if this is stipulated in the agreement. Otherwise, prepare a statement of claim and go to court.

If it is not possible to get the culprit to pay off the fine, then the amount of the debt can be put up for auction. This procedure is called redemption of the penalty. The debt can be purchased by a third party, for example, debt collectors.

How to reflect in accounting

The way transactions are recorded in an institution's accounting records depends on the type of organization. Let's look at how to make entries for each type of institution:

OperationDebitCredit

| State institution | ||

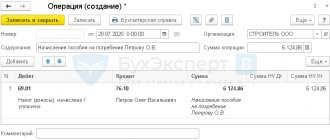

| The imposed penalty is reflected in budget accounting | 1 209 41 560 | 1 401 10 141 |

| Payment of compensation was transferred to the account of the budget revenue administrator (if the CU has administrator powers) | 1 210 02 140 | 1 209 41 660 |

| If a government agency does not have administrator powers | ||

| Calculations for non-tax revenues have been submitted to the revenue administrator (notification f. 0504805 has been completed) | 1 304 04 140 | 1 303 05 730 |

| Confirmation received from the revenue administrator (f. 0504805) | 1 303 05 830 | 1 209 41 660 |

| Budgetary or autonomous institution | ||

| Penalties imposed on the supplier are reflected | 2 209 41 560 | 2 401 10 141 |

| The amount was credited to the bank account | 2 201 11 510Record the transaction on the balance sheet of account 17 | 2 209 41 660 |

The article was prepared using materials from ConsultantPlus. Get access

How to assess an administrative fine on transactions of a budgetary institution in 2021

Having considered the issue, we came to the following conclusion: Any penalties, fines and other sanctions transferred to budgets (extra-budgetary funds) can be taken into account by public sector organizations on account 0 303 05 000 “Settlements for other payments to the budget” with attribution to account 0 401 20 200 “Expenses of an economic entity.”

The tax authority imposed penalties on the budgetary institution for late payment of taxes (contributions, fees) and fines for failure to comply with deadlines for submitting tax returns (calculation of insurance premiums). Payment of the specified penalties and fines was carried out under subsection 292 of KOSGU at the expense of a subsidy for the state task. The violation of deadlines was due to the fault of the accounting employee, and he agrees to voluntarily reimburse the expenses incurred. How to reflect in accounting transactions for the payment of penalties and fines and their compensation by the guilty party?

Budget accounting entries with examples of basic transactions

Accounting in budgetary organizations has a number of features that differ from the accounting procedure in industrial and commercial enterprises. These include the availability of approved cost estimates and control of their execution, and the use of budget classification, which is the basis for organizing accounting in the institution.

The accounting procedure in budgetary institutions has its own characteristics and specifics. In this article we will introduce you to the main accounting operations of budgetary institutions and the mechanism for reflecting them.

Payment order for penalties in 2021 - 2021

So, the first difference is KBK (field 104). For tax penalties, there is always a budget classification code, in the 14th–17th digits of which the income subtype code is indicated - 2100. This code is associated with a significant change in filling out payment orders: from 2021, we no longer fill out field 110 “Payment Type” .

However, these changes did not affect accident insurance contributions, and penalties for them, as well as these contributions themselves, are still paid to social insurance. When paying both contributions and penalties to the Social Insurance Fund in fields 106 “Basis of payment”, 107 “Tax period”, 108 “Document number” and 109 “Date of document”, enter 0 (clauses 5, 6 of Appendix 4 to the order of the Ministry of Finance of Russia dated November 12, 2021 No. 107n). And if penalties are paid at the request of the fund and according to the inspection report, their details are given in the purpose of payment.

Postings when accruing penalties under the contract

Contributions for penalties under an employment contract are generally always accrued (letter of the Ministry of Labor of Russia dated April 27, 2016 No. 17-4-OOG-701). Although in judicial practice there are also opposing positions (for example, Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated December 10, 2013 No. 11031/13). But strictly speaking, according to the letter of the law, contributions must be calculated and, in order to avoid legal disputes, it is recommended.

- in accordance with the agreement of the parties or a unilateral notification from the counterparty (which become supporting documents when recording transactions in accounting);

- by law - as in the case of writing off penalties for state construction contracts in accordance with Decree of the Government of the Russian Federation dated March 14, 2016 No. 190.

What are the fines for non-payment of personal income tax in 2021?

If tax inspectors reveal violations, the employer will have to pay 40% of the debt. But violators are often not afraid of this. Therefore, the issue of not only increasing penalties, but also other countermeasures is being resolved by law.

After committing an offense, the employer will need to pay a fine. It is calculated depending on certain circumstances. It is important to know the situations when additional funds cannot be withheld, as well as the powers of tax authorities in calculating such payments.

Postings for penalties for electricity in 2021 budgetary organization

Until 2021, control over the calculation of insurance premiums was carried out directly by extra-budgetary funds, and starting from January 1, 2021, these powers were transferred to the tax authorities. Now the transfer of contributions, as well as reporting on them, must be sent to the Federal Tax Service at the place of registration of the company. However, this in no way affects the accounting and postings that are compiled in the organization, and, therefore, the correspondence and rules for calculating contributions remain the same.

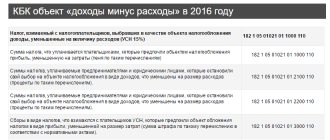

In accordance with the Instructions on the procedure for applying the budget classification of the Russian Federation, approved by Order of the Ministry of Finance of Russia dated December 21, 2021 N 180n, the costs of paying insurance contributions to the Pension Fund of the Russian Federation are included in subarticle 213 “Accruals for wage payments” of the KOSGU, the cost of paying penalties for late payment of insurance premiums are reflected by the budgetary institution under Article 290 “Other expenses” of KOSGU.

Postings for wages in budget accounting

Every month, each organization pays insurance contributions to the Pension Fund, mandatory social contributions to the Social Insurance Fund and the Federal Compulsory Medical Insurance Fund.

The object of taxation is payments and other remuneration accrued by employers in favor of employees. In the budgetary sphere, to detail the flow of funds, a classification of operations of the general government sector (abbreviated as KOSGU) has been developed. In this case, when generating transactions, a code should be added to the accounting account that determines the type of receipt or disposal of an accounting object in accordance with this classification.

How are penalties for non-payment of utility bills calculated and how to avoid them?

- From the 31st to the 90th day of non-payment of receipts, the fine will be 1/300 of the refinancing rate of the Central Bank of the Russian Federation (per day).

- From 91 days onwards, the penalty amount will increase to 1/130 of the refinancing rate of the Central Bank of the Russian Federation (per day).

We recommend reading: Sample application for a passport after obtaining citizenship

Another method, which is not officially established and does not always lead to the cancellation of penalties, is a personal appeal to the management company with a request to defer payments. Unfortunately, not all management companies do this for the sake of the residents.

New procedure for calculating penalties in 2021 using examples

It should be noted that this procedure for calculating penalties applies to arrears arising after October 1, 2021 (Clause 9, Article 13 of Federal Law No. 401-FZ of November 30, 2021). For debt that was formed earlier (before October 1, 2021), a different, “old” rule is provided. Penalties for companies are calculated based on 1/300 of the refinancing rate for each day of delay, regardless of its duration (Letter of the Ministry of Finance of Russia dated September 21, 2021 No. 03-02-07/1/60904).

If tax inspectors made a mistake in calculating penalties, then you should not remain silent. File a complaint. After all, tax inspectors do not have the right to charge penalties at a rate of 1/150 for debts that arose before October 1, 2021. The Federal Tax Service agrees with this (Decision on complaint dated 10/05/2021 No. SA-4-9/ [email protected] ).

How to calculate penalties on contributions in 2021 postings

Where to pay Insurance premiums, including penalties, are paid to the territorial tax office using the established details before the 15th day (inclusive) of the month following the reporting month. The exception is those months when the 15th of the calendar falls on a weekend, then the deadline will be the next working day.

We will talk about such a budget instrument as penalties for taxes and fees. Let's consider the concept of this term, let's name its main difference from a fine. The formula for calculating the amount of penalties for their independent calculation and current changes that came into force on October 1, 2021 will also be considered. Let's look at examples of calculating penalties for taxes and contributions, methods for accounting for penalties, as well as the nuances of tax accounting for penalties related to corporate income tax in 2021. In the article we will also talk about accounting entries when calculating penalties for taxes, and provide examples of calculations. The concept of a penalty, what is the difference from a fine Before starting a discussion of the entries and nuances of accounting and tax accounting for penalties, it is important to understand their semantic meaning.

Tax penalties: accounting entries

When calculating penalties in accounting, the entries may be different if we are not talking about a violation of tax laws, but about non-fulfillment of the terms of business agreements concluded between counterparties.

If an organization or individual entrepreneur does not pay its taxes on time, in addition to the overdue amount of debt, such taxpayers will have to pay penalties. A penalty is an amount of money that must be paid in excess of the amount of overdue taxes (Clause 1, Article 75 of the Tax Code of the Russian Federation). But it happens that the payment of penalties is also provided for in business contracts (for example, a purchase and sale agreement). We will tell you in our consultation what kind of entries are formed in accounting when calculating penalties.

Which postings should be used to reflect penalties?

According to the current tax legislation, penalties are understood as payments that an institution must pay as security in the event of a delay in payment of its obligations (Clause 1, Article 72 of the Tax Code of the Russian Federation). Such a penalty is accrued if the organization has violated the deadline for paying a tax (including advance) payment, contribution, fee (clause 1 of Article 75 of the Tax Code of the Russian Federation).

Collections can also be carried out using account 91. However, when accounting through account 91 “Other income and expenses”, the enterprise will have tax obligations, since such expenses are not accepted for taxation (clauses 4, 7 of PBU 18/02).

We charge penalties in 2021 for a budgetary institution

Svetlana, according to Instructions No. 65n, expenses associated with the payment of penalties for late payment for services provided are reflected in article 290 “Other expenses” of KOSGU. To account for settlements with suppliers for the amount of penalties, account 302.91 “Settlements for other expenses” is used. Moreover, in a situation where penalties under agreements (contracts) are accrued as the execution of judicial acts of the Russian Federation, settlement agreements, CVR 831 “Execution of judicial acts of the Russian Federation and settlement agreements on compensation for harm caused” is used to pay them. In case of voluntary payment of penalties under agreements (contracts) with suppliers, KVR 853 “Payment of other payments” is applied. It is advisable to write off such expenses immediately to the debit of account 401.20 “Other expenses”.

It is advisable to pay penalties and fines to budgetary institutions using funds from income-generating activities (KVD 2). However, current legislation does not directly prohibit the payment of economic sanctions using budget subsidies. At the same time, it should be understood that when such expenses are accrued and paid from subsidies, during control measures they can be classified, at a minimum, as ineffective.

Reflection of penalties for violation of contract in the budget posting organization

To do this, in the same reporting period, they make an entry for the corresponding amount: - debit 91-2 “Other expenses” credit 76-2: penalties for violation of contractual obligations awarded by the court or recognized by the organization are reflected.

According to the law, for citizens no penalties will be charged during the first month of delay. From 31 to 90 days of delay, the amount of the penalty is set at 1/300 of the rate of the amount not paid on time for each day of delay, from 91 days - 1/130 of the rate.

Postings in the budget for penalties under the contract

Read about the features of reflecting penalties on social contributions in accounting here. Results Changes in the accounting of social contributions are more related to innovations in the procedures for calculating and transferring these payments than to changes in the methodology for displaying them in accounting.

At the same time, timely signing of the new version of the order on the accounting policy for separate accounting of old and new contributions will help you avoid possible troubles associated with incorrectly reflecting the amount of contributions in the reporting or paying incorrect amounts.

If, in the event of a violation of contractual obligations, the violating party pays a fixed fine or an estimated amount of penalties, then in case of non-payment of taxes (contributions, fees) or parts thereof, the tax authorities will oblige the taxpayer to pay both the arrears, the fine, and the penalty.

Postings for penalties in a budgetary institution

Debit KDB.1.205.41.560 Credit KDB.1.303.05.730 – reflects the debt of the supplier (performer, contractor) to the budget to pay a penalty (fine, penalty) for violation of obligations under the contract;

The amount of the penalty (fine, penalties) in case of violation of the terms of the state contract relates to non-tax budget revenues and is credited in the amount of 100 percent to the income of the corresponding budget (paragraph 5, paragraph 3, article 41, subparagraph

6 clause 1 art. 46 of the Budget Code of the Russian Federation). Therefore, the supplier (performer, contractor) must transfer the penalty (fine, penalty) directly to budget revenue without being reflected in the personal account of the customer - the recipient of budget funds.

Penalty for late repayment of debt and other violations of contract terms

Reflection in accounting of a claim brought by a foreign organization against a Russian organization for late payment for goods in the form of penalties. The Russian Federation does not have an agreement on the avoidance of double taxation with the foreign state in which the representative office of this foreign organization is located.

We recommend reading: Number of immigrants to Russia 2020

Reflection in accounting of the payment of a fine by a Russian organization to a foreign organization for violation of customer requirements during the execution of a contract. According to the terms of the agreement, in case of failure to pay the fine on time, penalties will be charged for each day of delay in payment of the fine.

Accounting and taxation of fines, penalties, penalties under business contracts for an organization

For organizations that determine income and expenses on a cash basis, expenses in the form of fines, penalties and (or) other sanctions for profit tax purposes are recognized after their actual payment (clause 3 of Article 273 of the Tax Code of the Russian Federation).

According to paragraph 2 of Article 171 of the Tax Code of the Russian Federation, tax amounts presented to an organization for goods, work, services, property rights acquired for the implementation of transactions recognized as objects of taxation and for goods (work, services) acquired for resale are subject to deduction.

Accrual of penalties for postings in budget accounting

If payment under the contract was made by a federal budgetary institution at the expense of targeted subsidies in the amount of payment to the supplier (performer) of the amount reduced by the amount of the penalty, the amount of the penalty reflected on the personal account with code 21 shall be reflected on the personal account with code 20. The basis document for transferring these funds from one personal account to another is an application for cash expenses (f. 0531801) (hereinafter referred to as the application).

As a general rule, the size of the refinancing rate is determined on the day of fulfillment of the monetary obligation or its corresponding part, unless otherwise established by law or agreement of the parties (clause 1 of Article 395 of the Civil Code of the Russian Federation).

The rates are set by instructions of the Bank of Russia for a certain period and are published on its official website (https://www.cbr.ru).

At the time of writing, the refinancing rate is 8.25% per annum (Instruction of the Bank of Russia dated September 13, 2012 N 2873-u).

In cases provided for by law, when making settlements with an individual, not only the penalties paid - fines (penalties) are reflected in the accounting records, but also the taxes and contributions accrued on them. So, if the recipient of the penalty is an individual who is not registered as an individual entrepreneur, then the following correspondence may additionally be drawn up:

According to one opinion, a penalty cannot be attributed to tax sanctions for non-compliance with taxation rules. Concept, essence and reflection of a penalty in accounting, postings First of all, let's look at the definition.

A penalty is a type of penalty, which is determined for failure to fulfill or improper fulfillment by participants in legal relations of their obligations under contracts and other civil legal acts. This includes fines and penalties. Such a material sanction is other income for the receiving participant (clause

7 PBU 9/99) and other expenses - for the obligated participant (clause 11 PBU 10/99). The account on which the main accounting actions for accounting for sanctions are reflected is 76 “Settlements with various debtors and creditors.”