In what cases is it necessary?

A covering letter is not a mandatory element when sending a document and its presence is not regulated by law. However, practice shows that the attached letter helps speed up and simplify the work of inspectors. If the information inspectors need or the note itself is missing, additional proceedings may follow.

You can attach a covering letter to the following types of declarations:

- Specified (submitted to the tax authorities before the deadline for filing a tax return, after the filing deadline, but before the end of the tax payment period, or after all deadlines have expired).

- Zero (submitted by the individual entrepreneur in the absence of activity; if there is no reporting, zero data must be provided).

- Lesnoy (contains data on the methods and timing of use of forest resources; the forest user is required to attach a report with actual data on deforestation).

- According to UTII (quarterly reporting in the tax return; submitted regardless of whether the activity was carried out or not, since tax is paid even in the absence of income).

- According to the simplified tax system (a declaration to the tax authorities with the reporting of an individual entrepreneur or LLC for the calendar year, also submitted regardless of the presence or absence of profit).

General rules for correcting the sales ledger and purchase ledger

It is also necessary to correct the data in these tax registers in cases where there is no obligation to submit an updated declaration and the taxpayer needs to correct technical errors. If errors are discovered after the end of the quarter in which they were made, corrective entries in the sales book or purchase book are made in additional sheets of the sales book (purchase book) in which the errors were made (clause 4 of the Rules for maintaining the purchase book, clause 3, 11 Rules for maintaining a sales book, approved by Resolution No. 1137)

To make an entry in the sales book or purchase book about invoices that were not previously included in them, you must register “forgotten” invoices in an additional sheet to the sales book or purchase book, respectively. And in order to remove the erroneous entry, in an additional sheet to the purchase book (sales book) it is necessary to repeat the “extra” entry on the invoice, indicating the numerical indicators of the invoice with a negative sign.

Let's take a closer look at the most common errors and options for correcting them.

Error 1. Forgot to register the issued invoice in the sales book

Invoices must be registered in the sales book in the period in which tax obligations arose (clause 2 of the Rules for maintaining the sales book). Accordingly, the “forgotten” invoice should be registered in an additional sheet of the sales book of the quarter in which the VAT tax base arose. It is also necessary to submit an updated VAT return, having previously paid the arrears and penalties.

Error 2. An “extra” invoice was issued

In many organizations, managers, rather than accounting employees, handle the preparation of primary documents and invoices. Therefore, after the end of the quarter, it sometimes turns out that the sale of goods (work, services) was registered, which did not exist.

Such situations are typical for organizations performing construction and installation work. On the last day of the quarter, the contractor drew up a work completion report and issued an invoice, but the customer refused to sign the report for objective reasons. In such a situation, there is no implementation of work, which means the invoice is issued prematurely. Accordingly, it must be cancelled.

The Federal Tax Service of the Russian Federation explains that if the seller did not register the issued invoice in the sales book, and the buyer in the purchase book, then no tax consequences arise for the parties to the transaction (Letter of the Federal Tax Service of the Russian Federation dated April 30, 2015 N BS-18-6 / [email protected] ). That is, in order to cancel an erroneously issued invoice, the seller must cancel the entry about it in the sales book.

If the buyer has registered an erroneously issued invoice in the purchase book, then he needs to cancel the entry about it in the purchase book. As already mentioned, if it is necessary to make changes to the sales book or purchase book after the end of the quarter, such corrections are made in additional sheets of the sales book (purchase book), i.e. records of “extra” invoices are canceled (numerical indicators are reflected with a negative value).

Error 3. Registered an invoice with incorrect numbers (overestimated or underestimated the amount of VAT payable)

When registering correctly completed invoices, you can make a mistake when filling out the purchase book (sales book) by entering incorrect data. In this case, to correct errors, incorrect invoice entries are canceled, i.e. in an additional sheet of the sales book (purchase book), they repeat erroneous entries, but indicate numerical indicators with a minus sign and make the correct entry.

In such a situation, regardless of the results of the recalculation, an updated VAT return must be submitted. If the taxpayer has underestimated the amount of VAT payable, then before submitting the “clarification” it is necessary to pay the arrears and the corresponding penalties.

Error 4. Forgot to declare VAT deduction

Practice shows that most often taxpayers forget to deduct VAT calculated upon receipt of an advance payment when reflecting the shipment of goods (works, services) (clause 8 of Article 171, clause 6 of Article 172 of the Tax Code of the Russian Federation). Many people forget to deduct VAT paid as tax agents. In these situations, if the taxpayer wishes to take advantage of “forgotten” deductions, an updated VAT return should be submitted, increasing the amount of deductions.

The fact is that, according to the Ministry of Finance of the Russian Federation, not all deductions can be transferred to a later period.

In accordance with clause 1.1 of Article 172 of the Tax Code of the Russian Federation, deduction of VAT on goods (work, services) specified in clause 2 of Article 171 of the Tax Code of the Russian Federation, i.e. VAT presented by sellers and “customs” VAT can be declared within three years after the goods (work, services) are reflected in accounting. Moreover, deductions can be claimed in parts in different quarters (Letter of the Ministry of Finance of Russia dated May 18, 2015 N 03-07-РЗ/28263).

Exceptions include fixed assets, equipment for installation and (or) intangible assets. VAT can be transferred on them, but it must be declared in full (that is, the deduction cannot be partially transferred) (Letter of the Ministry of Finance of Russia dated December 19, 2017 N 03-07-11/84699).

Deductions not specified in clause 1.1. Article 172 of the Tax Code of the Russian Federation cannot be transferred to a later period.

Accordingly, if the taxpayer discovered that he forgot to deduct VAT calculated upon receipt of an advance payment on the date of shipment of goods (works, services) or VAT paid by the tax agent, and does not want to argue with the tax authorities, such deductions should be declared in the quarter in which which the conditions for deduction are met, i.e. in the updated VAT return. These deductions should not be transferred to a later period (Letters of the Ministry of Finance dated 07/21/2015 N 03-07-11/41908, dated 04/09/2015 N 03-07-11/20290).

At the same time, the norms of Chapter 21 of the Tax Code of the Russian Federation may establish other deadlines for VAT deductions. For example, deduction of VAT when returning an advance payment or returning goods (work, services) is possible after the corresponding adjustment transactions in connection with the return of goods or refusal of goods (work, services) are reflected in the accounting records, but no later than one year from the date of return or refusal ( Clause 5 of Article 171 and Clause 4 of Article 172 of the Tax Code of the Russian Federation).

And deductions for adjustment invoices are made within three years from the date of issuance of the adjustment invoice (clause 13 of article 171 and clause 10 of article 172 of the Tax Code of the Russian Federation). Therefore, such deductions can be declared both in the current period and in an updated VAT return, if, of course, the deadlines for

VAT deductions are not omitted.

Thus, if a taxpayer discovers that he forgot to claim a VAT deduction that can be used at a later period, it is not necessary to submit an updated VAT return. It can be declared in the current period. If it is impossible to “carry forward” the deduction to a later period, in order to exercise the right to deduction, a “clarification” must be submitted. In this case, the forgotten invoice should be registered in an additional sheet of the purchase book of the quarter in which the right to deduction arose.

Error 5. An error was made when filling out the invoice

If an error was made when filling out the invoice, for example, the wrong price for the product was indicated, the tax rate was mixed up, etc., i.e. An error in the invoice prevents the tax authorities from identifying the seller, buyer, goods (work, services), their cost, amount and VAT rate; the invoice must be corrected (clause 2 of Article 169 of the Tax Code of the Russian Federation). Otherwise, the buyer cannot deduct VAT.

Invoices are corrected by issuing a corrected (correctly completed) invoice with the same number and date. In this case, line 1a indicates the number and date of correction of the invoice. The remaining invoice indicators are filled out as they should have been done initially (correctly).

Once the invoice is corrected, the seller must make the correction in the sales ledger for the period in which the original invoice was recorded. If an invoice is corrected after the end of the quarter in which it was registered in the sales book, then the sales book corrections are made in an additional sheet of the sales book for the quarter in which the invoice with an error was registered.

A record of an incorrectly completed invoice is cancelled, i.e. its numerical indicators are indicated with a negative value and the corrected invoice is recorded.

After compiling an additional sheet of the sales book, it is necessary to submit an updated VAT return, regardless of how the VAT tax base has changed, incl. to protect the buyer from unnecessary interactions with tax authorities.

If the buyer received a corrected invoice, he can deduct VAT in the period in which he claimed a deduction on the incorrectly completed invoice. Taxpayers officially received this right from October 1, 2017 (Resolution of the Government of the Russian Federation dated August 19, 2017 N 981), after amendments were made to the rules for filling out VAT documents approved by Decree of the Government of the Russian Federation dated December 26, 2011 N 1137 (hereinafter referred to as Resolution N 1137).

From October 1, 2021, a corrected invoice received after the end of the tax period is registered in an additional sheet of the purchase book for the quarter in which the invoice was registered before the corrections were made to it (clause 4. and clause 9 of the Bookkeeping Rules purchases used in calculations of value added tax, approved by Resolution No. 1137). In this case, the entry about the incorrectly completed invoice is canceled (clause 3 and clause 5 of the Rules for filling out an additional sheet of the purchase book used in calculations of value added tax, approved by Resolution No. 1137).

For example, a buyer accepted VAT on an incorrectly completed invoice in the third quarter of 2021, and received a corrected invoice in the second quarter of 2021. In this case, in the additional sheet of the purchase book for the 3rd quarter of 2017, he will cancel the entry about the incorrectly completed invoice and register the corrected invoice.

And here the question may arise: does the buyer need to submit an updated VAT return if the amount of deductions has not changed? For example, in the 3rd quarter of 2021, the buyer accepted VAT on goods for deduction based on an invoice in the amount of 118,000 rubles, i.e. 18,000 VAT, and in the 2nd quarter of 2021 received a corrected invoice in the amount of RUB 236,000, incl. VAT 36,000 rub.

To ensure that the amount of deductions in the amended VAT return does not increase, the taxpayer decided to declare the deduction on the amended invoice in parts, i.e. he canceled the entry about the incorrectly completed invoice in the amount of RUB 118,000. and registered the corrected invoice in an additional sheet of the purchase book for the 3rd quarter of 2021, indicating in column 15 of the additional sheet of the purchase book the cost of goods (work, services) indicated in column 9 on the line “Total payable” of the corrected invoice (in our example - 236,000 rubles), and in column 16 - the amount of VAT accepted for deduction - 18,000 rubles. He reflected the remaining part of the deduction (RUB 18,000) on the corrected invoice in the purchase books of the current period. Accordingly, the amount of VAT deductions based on the results of the 3rd quarter of 2021 did not change.

According to the author, even if the buyer has deducted VAT in an amount less than indicated in the corrected invoice, he should submit an updated VAT return.

The fact is that significant errors in the invoice, in particular errors in the cost of goods and the amount of VAT claimed, deprive the buyer of the right to deduct VAT (clause 2 of Article 169 of the Tax Code of the Russian Federation). Accordingly, regardless of whether the buyer received a corrected invoice or not, a deduction for an incorrectly completed invoice is not possible. This means that by deducting VAT, the buyer overestimated the amount of deductions, i.e. made a mistake that led to non-payment of tax and is obliged to correct it (clause 1 of Article 81 of the Tax Code of the Russian Federation). The deduction of VAT on the corrected invoice is a right of the taxpayer and this right should be declared in the VAT return.

In addition, if the buyer does not have an updated VAT return, the data from the seller’s updated VAT return will not “collapse” with the buyer’s return data. Therefore, there is a risk that if an updated VAT return is not submitted, the tax authority, during an on-site audit, will “withdraw” from deductions the entire amount of VAT on an incorrectly completed invoice, while the tax authority will not “impose” the right to a deduction on the corrected invoice on the taxpayer .

Purpose of provision

The covering letter contains a list of the materials sent and explanations for them. These additions greatly facilitate interactions between tax authorities and taxpayers.

If there is a written listing of the submitted documents, the risk of additional questions from the inspectorate regarding the completeness of the reporting provided is minimized. The second reason why it is worth attaching an explanatory note to reporting to the inspectorate is to simplify the registration of incoming correspondence.

Note! The tax authorities will not ask the taxpayer for the purpose of filing a return (for example, an updated one) if a letter is attached with the reason for sending the documents.

A cover letter has no meaning, but its presence:

- is a confirmation of the fact of sending;

- contains a list of attached documents and instructions for handling them;

- allows you to determine the deadline due to the specified departure times.

Updated declaration sample of filling out 3 personal income tax

- A certificate in form 2-NDFL, confirmed by the seal or signature of the director, chief accountant, containing information on taxes withheld for the past year.

- If the reason for filing a declaration is the sale of property, then documents confirming ownership rights are required (transfer and acceptance certificate, registration certificate, purchase and sale agreement).

- Payment documents confirming the amount of expenses for the acquisition of property, construction or other action (receipts, payment orders, checks).

- Original passport or its copy certified by a notary.

- Details of the bank from which the loan was taken to purchase real estate.

- A certified copy of the loan agreement.

You will also need to file an income tax return if you decide to take advantage of deductions for social or property issues: for example, to return the amount of tax from the budget if you bought a home or spent some money on treatment or education.

Who writes?

Covering letters are written by persons who are required to declare their income. These include:

- individual entrepreneurs (IP);

- legal entities;

- limited liability company (LLC).

Individuals may also need to submit reports to the tax authorities with an explanatory note. These cases include the sale of property, receipt of income from sources abroad, and the use of inherited intellectual property. Lottery winnings are also taxable.

You can submit documents to the inspectorate and write an appendix with an explanation to them yourself, but it is better to entrust this to a lawyer. The specialist will draw up a note for the documents according to all the rules and take into account all the necessary nuances.

Reasons for submitting an updated calculation in Form 6 of personal income tax

- The form of presentation of the updated calculation is the same as that of the primary document;

- Correct information is provided;

- the procedure for filling out the 6 personal income tax clarification report is the same as when drawing up the initial declaration;

- is handed over, like the first document;

- Along with the correct information, an explanatory letter is sent to the tax authorities, which will indicate which line the error was made on.

The law does not limit the number of adjustment reports submitted to the main one. Therefore, you can take it as many times as you like. Also, the Tax Code of the Russian Federation does not specify the exact deadline for submission. But to avoid fines, you must report before the deadline. For example, when submitting personal income tax for six months, you can submit an adjustment within the deadline, until July 31.

General drafting rules

There is no statutory form for writing a cover letter, but there are rules for its composition that have been developed in practice. The annex to the reporting before the inspection must include:

- name of the tax office (if necessary, indicate the full name of the employee to whom the documents are sent);

- name of the tax organization and address of the sender;

- number and date of the request in response to which an explanation is sent;

- contacting an employee or tax authority;

- a list of documents and other materials indicating the number of sheets and copies;

- Full name and position of the sender, his signature and contact information (phone number, email).

General recommendations for filling out a cover letter to the tax authorities

Before starting the procedure for drawing up the type of letter in question, the manager must decide on the format. There are two options: electronic or on paper. Based on this, the further course of action will be determined. However, regardless of the chosen format, the certificate must be drawn up in accordance with the rules for drawing up official documents, and also contain the following details:

- information about the taxpayer who is drawing up the letter. This means indicating the organizational and legal form, legal address of the company, checkpoint, as well as contact information (based on the company’s Charter). When the letter is drawn up on company letterhead, the main details will include the personal account number, the name of the servicing bank, BIC;

- information about the addressee of the letter. It is assumed that it is necessary to enter the name of the local branch of the Federal Tax Service of the Russian Federation and its legal address;

- date and number of the document compiled. It is also necessary to indicate a link to the requirement from the Federal Tax Service of the Russian Federation to send specific papers to the structure, if the document is drawn up for the corresponding purpose;

- main text, compiled in free form. When writing it, it is necessary to maintain a business style of communication with legal structures;

- After the main text, a list of attached documents is provided in the form of a regular bulleted list. When it is too large, it is necessary to refer to the inventory compiled in a separate document and also attach it to the package of papers;

- signature of the manager or his authorized representative;

- information about the performer. This implies indicating the full name of the subject who compiled the document, his contact details and other details relevant in each specific case. Practice demonstrates that when the document was drawn up by the manager himself, this note can be omitted, since the director endorses the document in any case.

The electronic version of the document in question is regulated by the Federal Tax Service of the Russian Federation. This form can be found on the official portal of the service.

How is it prepared for certain types of reporting?

In addition to the general rules for writing appendices to documents in the inspection, there are also additional requirements that must be taken into account when writing a particular declaration.

Zero

When sending a zero declaration, the accompanying note must explain why the reporting is zero. In the wording of the letter, it is enough to indicate that no activity was carried out in the quarter/year.

Lesnaya

When drawing up an annex to the forest declaration, it is necessary to indicate in it the volume of wood cut down and the time frame during which the forest was cut down. In addition, information about the intended purpose of forests and the form of felling should be contained.

According to the simplified tax system

In the accompanying letter to the reporting under the simplified taxation system, it is necessary to clarify the indicators from the declaration : the amount of income (even if there was none - indicate zero), expenses, as well as the amount of taxes paid for the calendar year. If an individual entrepreneur is on the PSN (patent taxation system), he does not need to submit a declaration annually.

In this case, taxes are paid in advance at the time of purchase of the patent, which has a certain validity period that can be extended.

Reference! When paying, the individual entrepreneur can also attach a letter indicating the date of payment and the validity period of the patent.

According to UTII

The appendix to the quarterly tax reporting must also list the income and expenses of an individual entrepreneur or LLC for a certain period, or the reason for the lack of income and the purpose of the expenses.

Refined

The annex to the updated declaration must contain:

- the reason for adjusting the amount of tax liabilities;

- amended declaration deadlines;

- details of the previously listed advances and penalties.

We invite you to read other equally useful and interesting articles that will help you understand the following issues:

- What is a cover letter for a declaration?

- What are the features of drawing up such a document in the INFS, for personal income tax and for VAT?

Letter to clarify 2-NDFL certificates

When submitting an updated 2-NDFL certificate, the tax agent indicates the serial number of such adjustment in the “Adjustment Number” field. For example, “01”, if this is the first clarification of the 2-NDFL certificate for a specific individual, or “02”, if this is an adjustment to a previously submitted clarification (Procedure for filling out, approved by Order of the Federal Tax Service dated October 30, 2021 No. ММВ-7-11/) . The legislation does not require submitting any explanations along with updated 2-NDFL information.

If the tax inspectorate or the tax agent itself finds errors or inaccuracies in the submitted certificates, you will need to submit updated certificates. How to write a letter about clarification of 2-NDFL certificates?

Submission rules

A covering letter is sent to the tax office along with the declaration . You can submit the application along with a package of documents to the organization in person. It is also possible to send reports with an explanatory note by mail.

Covering letters are not mandatory elements when sending reports to the tax authorities, but their presence helps to avoid a number of problems and questions. The main thing is to correctly compose the application and clearly indicate your requests and explanations in it.

General writing rules

At the moment , there is no approved form for a cover letter, so it can be compiled in any form . The main thing is that it contains the information necessary for tax officials to work with declarations.

The document must indicate:

- In the “header” on the right are the necessary details of the company (TIN, KPP, OGRN, address and telephone) or an individual (TIN, passport, telephone).

- Document's name. Examples: “On the provision of documents”, “Clarifying note” or simply “Application”.

- The main part, which includes the main content of the letter. For example, in the case of filing an updated declaration, it is necessary to note the date and number of the updated certificate, as well as the date and number of the certificate in which the company discovered an error. You should also provide a description of what the error was and how it affected the tax calculation.

- Signature of the manager (seal if necessary) and contact details of the person in charge.

Important! A cover letter is a formal document. Although it assumes a free form, it is necessary to take a responsible approach to its compilation.

How to fill out the updated 3-NDFL declaration

- A certificate in form 2-NDFL, confirmed by the seal or signature of the director, chief accountant, containing information on taxes withheld for the past year.

- If the reason for filing a declaration is the sale of property, then documents confirming ownership rights are required (transfer and acceptance certificate, registration certificate, purchase and sale agreement).

- Payment documents confirming the amount of expenses for the acquisition of property, construction or other action (receipts, payment orders, checks).

- Original passport or its copy certified by a notary.

- Details of the bank from which the loan was taken to purchase real estate.

- A certified copy of the loan agreement.

We recommend reading: Preliminary Pledge Agreement

It is submitted by the payer himself and serves for reporting his income and subsequent payment of personal income tax. The peculiarity of this declaration is that it is compiled and executed by the taxpayer independently.

Letter about zero 6-NDFL: sample

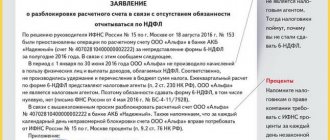

All tax agents must submit calculations using Form 6-NDFL (clause 2 of Article 230 of the Tax Code of the Russian Federation). Tax agents are, as a rule, employers or customers under civil contracts under which individuals receive income.

Unfortunately, there is a possibility of such a development of events. And in order to protect the business, it makes sense to submit a free-form letter to the tax office, in which it is reported that the organization or individual entrepreneur has neither employees nor contractors and therefore 6-NDFL is not submitted.

We recommend reading: Help 2 Personal Income Tax How to Fill out Child Benefits

Is it possible to submit an adjustment using Form 6-NDFL?

Thus, it is not only possible, but also necessary, to submit the calculation in question to the Federal Tax Service as soon as possible (or at the request of the Federal Tax Service). At the same time, there are a number of features that characterize the preparation of the 6-NDFL adjustment form. Let's study how to submit an update on 6-NDFL, taking into account these nuances.

In the first case, the clarification must be submitted as soon as possible: before the error is discovered by the Federal Tax Service. From the moment the calculation is received, the tax authorities do not have much time to check it - no more than 3 months (clause 2 of Article 88 of the Tax Code of the Russian Federation).

27 Jul 2021 jurist7sib 126

Share this post

- Related Posts

- Work Producer Foreman What are the Benefits in the Process of Labor Activities

- Gifts from Social Security

- Where on the State Services Website to View Tax Refund

- What benefits does a certificate of a person living in a residence zone with preferential economic status for an indefinite period provide?