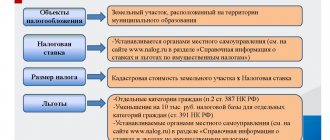

The tax base for calculating land tax is the cadastral value of the plot, established as of January 1 of the calendar year. However, during the tax period, the cadastral value may change due to the transfer of a plot from one category to another or due to the entry into force of a judicial act establishing the market value. The Russian Ministry of Finance spoke in a commentary letter about the procedure in which land tax is calculated when the cadastral value of a plot changes. (LETTER OF THE MINISTRY OF FINANCE OF THE RF dated 09/05/13 No. 03-05-05-02/36540)

Calculation features

According to the law, recalculation of land tax when the cadastral value changes is necessary when owning a plot of land does not last the entire tax period. That is, not a whole calendar year (clause 1 of Article 393 of the Tax Code of the Russian Federation). In such a situation, the cadastral valuation may change for three reasons. Due to:

- Changing the type of permitted use;

- Transfer of a plot from one category of land to another.

- Changes in site area.

Based on Articles 391 and 396 of the Tax Code of the Russian Federation, all this obliges the calculation of land tax when changing the cadastral value, taking into account two coefficients at once - Kv and Ki.

However, as noted by the Ministry of Finance and the Federal Tax Service, Chapter 31 of the Tax Code of the Russian Federation “Land Tax” does not stipulate the rules for calculating the tax and advance payment for it, when it is necessary to simultaneously apply both coefficients - Kv and Ki, the value of each of which is different from unity (it is possible that legislators will correct this situation in the near future).

The Federal Tax Service believes that the value of the Ki coefficient should take into account the period of ownership of the land plot in a given tax period.

REFERENCE

If ownership rights (permanent (perpetual) use/lifelong inheritable ownership) to a land plot (its share) arise/terminate during the tax/reporting period, the tax (advance payment) is calculated taking into account the coefficient Kv. It represents the ratio of full months of ownership of a plot to calendar months in the tax/reporting period (clause 7 of Article 396 of the Tax Code of the Russian Federation).

When changing the type of permitted use of a plot during the tax/reporting period, transferring it from one category of land to another and/or changing the area, the tax (advance payment) is calculated taking into account the Ki coefficient. It is defined similarly to paragraph 7 of Art. 396 of the Tax Code of the Russian Federation (clause 7.1 of Article 396 of the Code).

Recalculation of land tax

According to Art.

391 of the Tax Code of the Russian Federation, the cadastral value of real estate acts as a tax base for calculating land tax, and accordingly entails a revaluation of its value. There is no need to submit a written request to the Federal Tax Service, since the recalculation is carried out automatically. The amount of tax will change for the reporting period in which the owner filed an application with the court or collegial commission. The procedure is carried out from the moment of registration of changes in the state register.

Tax calculation example

In letter No. BS-4-21/11418 dated June 14, 2018, the Federal Tax Service gives the following example of calculating land tax when the cadastral value changes.

Situation

The cadastral value of a plot of land as of January 1, 2018 is 10 million rubles. Information serving as the basis for determining the cadastral value due to a change in the type of permitted use of the site was entered into the Unified State Register of Real Estate on February 16, 2021. The date of termination of ownership of the plot is March 23, 2018.

The changed cadastral value based on the change in the permitted use of the land plot amounted to 8 million rubles. The tax rate is 1.5%.

Solution

According to officials, the recalculation of land tax when the cadastral value changes for the tax period of 2021 should be done by summing up:

- the product of the cadastral value of the land plot as of 01/01/2018 (10 million rubles) by Kv (3 months/12 months), by Ki (2 months/3 months) and by the tax rate (1.5%)/100 ;

- the product of the new cadastral value of the site (due to a change in permitted use) (8 million rubles) by Kv (3 months/12 months), by Ki (1 month/3 months) and by the tax rate (1.5%) /100.

A similar calculation procedure should be applied when calculating advance payments for land tax if it is necessary to simultaneously apply the coefficients Kv and Ki, the value of each of which is different from unity.

Also see “New clarifications of the Federal Tax Service of Russia in the letter on land tax.”

Read also

06.07.2018

In accordance with current legislation, organizations that own land plots are required to calculate and pay land tax based on the cadastral value of the plot they own. Moreover, by virtue of the direct instructions of the law, the cadastral value should be determined not on an arbitrary date or the date of tax calculation, but on January 1 of the year, which is the tax period. This calculation procedure is convenient if the value of the land and its purpose do not change during the year. However, in practice, there are often cases when, for one reason or another, the cadastral value of a plot and (or) the tax rate is revised. Is it necessary to recalculate the land tax? The answer to this question depends on a number of factors. The cadastral value of a land plot may change as a result of the transfer of land from one category to another or a change in the type of permitted use of the land plot, as a result of the court establishing the market value of the land plot and entering such value into the state real estate cadastre as the cadastral value, as well as as a result of correcting technical errors made when entering information into the state cadastre. In this case, the adjustment of the price of a land plot can be established on January 1 of the reporting year, that is, be retrospective in nature, or on some other date during the reporting year. Changes in value can occur either upward or downward. If the cadastral value changes upward, regardless of the reasons for such a change, the Ministry of Finance of Russia, in letter dated September 5, 2013 No. 03-05-05-02/36540, recommends using the new cadastral value in order to determine the tax base for land tax as of January 1 the year following the tax period in which such changes were made to the cadastre. Thus, if the increase in cadastral value is not associated with a change in the category of land or type of permitted use (that is, the tax rate did not change during the tax period), then the land tax should not be recalculated in the current tax period, since this would lead to a worsening of the taxpayer’s situation . An exception is the situation in which the increase in cadastral value occurred as a result of the correction of technical errors made when entering information into the state cadastre, which was recorded by a court decision. In this case, even if the cadastral value of the land plot was changed as of January 1 of the year (retrospectively), the land tax must be calculated based on the new value of the land plot, adjusting tax liabilities. Arbitration courts and the Federal Tax Service of Russia adhere to this position.

Example 1. Based on a court decision made on July 1, 2013, a technical error made by the cadastral registration authorities in relation to a land plot classified as land within agricultural use zones in the city of Moscow, owned by Alfa LLC, was corrected in connection with incorrect application of the specific indicator of cadastral value of land per unit area. The cadastral value of the land plot was increased from 10,000,000 rubles. up to 20,000,000 rubles, while, due to the direct indication in the text of the court decision, changes to the cadastre were made from January 1, 2013. Calculation procedure: Before the court decision entered into force, advance payments for land tax were calculated by Alpha LLC in the amount of 7,500 rub. for the quarter (RUB 10,000,000 x 0.3% x 0.25). After the court decision comes into force, the taxpayer should recalculate tax liabilities at the rate of 20,000,000 rubles. x 0.3% x 0.25 and pay the difference in the amount of 7,500 rubles for the 1st and 2nd quarters of 2013 to the budget. Advance payments for the 3rd quarter of 2013 and for the tax period of 2013 to Alpha LLC should be calculated based on the cadastral value in the amount of 20,000,000 rubles. and count in the amount of 15,000 rubles. for the quarter.

If the cadastral value of a land plot has decreased, when calculating land tax from the moment when supporting documents are drawn up, the use of a different cadastral value is possible provided that it corresponds to the indicator established at the beginning of the year by local authorities. A similar point of view was expressed in the resolutions of the Presidium of the Supreme Arbitration Court of the Russian Federation dated November 6, 2012 No. 7701/12, dated June 28, 2011 No. 913/11, and the resolution of the Seventh Arbitration Court of Appeal dated December 6, 2013. In addition, if a change in the category of land or the type of permitted use led to a change in the tax rate, when calculating the tax from the moment of such change (regardless of whether the cadastral value of the land or the tax rate itself increased or decreased), the new rate must be applied. In letter dated 04/13/2013 No. 03-05-04-02/7507, the Russian Ministry of Finance recommends calculating land tax or an advance payment thereon taking into account a coefficient defined as the ratio of the number of full months during which the land plot was assessed at one or another cadastral value , to their full number in the tax or reporting period. In this case, a month in which a particular cadastral value (tax rate) was applied for more than fifteen days is equated to a full month. In the reporting period when changes occurred, as well as when calculating tax for the year, different cadastral values and different coefficients are involved in the calculation; in the reporting periods remaining after the changes until the end of the calendar year, advance tax payments are calculated based on the new value and new rate. To calculate land tax taking into account the correction factor, the following formula can be applied:

N = Ks x Ct x Kf, where N is the amount of tax; Kc - cadastral value; St - tax rate; Kf - coefficient. To calculate the coefficient, the numerator is substituted with the number of full months remaining until the end of the quarter (when calculating the advance payment) or year (when calculating the tax) after the change in the value of land or the tax rate, and the denominator is the number 3 (for the reporting period) or 12 (for tax period).

Example 2. On June 12, 2013, Omega LLC received documents on the basis of which the category of land plot No. 1 owned by it, located on the territory of the city of Moscow, changed. Until June 12, 2013, this land plot belonged to the category of agricultural land and was valued at 10,000,000 rubles; after this date, the plot was transferred to the category of other land with a cadastral value of 15,000,000 rubles. On July 17, 2013, the category of land plot No. 2 owned by Omega LLC, located on the territory of the city of Moscow, changed - from the category of land used for the operation of sports facilities, it was transferred to the category of other land, the cadastral value of the plot did not change and amounted to 2,000,000 rubles. On October 20, 2013, Omega LLC transferred land plot No. 3, located in the city of Moscow, from the category of other land to the category of agricultural land. At the same time, the cadastral value of the land plot decreased from 10,000,000 rubles. up to 5,000,000 rub.

Calculation procedure: In relation to land plot No. 1, there was both an increase in the cadastral value and an increase in the tax rate. To calculate land tax when the cadastral value of a plot increases during the tax period, the cadastral value established on January 1 of the year is used, that is, in the case under consideration - 10,000,000 rubles. The tax rate is determined depending on the category of land on the date of calculation of the advance payment or tax , thus, when changing the category of land, it is necessary to apply a new tax rate taking into account the correction factor. In the case under consideration, the changes occurred on June 12, 2013 (before the 15th day of the month), therefore the number of full months of application of the rate of 0.3% (for agricultural land) will be 5 months, the coefficient for calculating the tax for the year will be 0.42 ( 5/12); for the second quarter – 0.67 (2/3). The new rate of 1.5% (for other lands) will be applied for 7 full months, the coefficient for calculating the tax for the year will be 0.58 (7/12), for the second quarter - 0.33 (1/3). Therefore, for the first 5 months, the amount of tax in relation to land plot No. 1 will be 12,600 rubles. (10,000,000 rubles x 0.3% x 0.42), and for the subsequent period – 87,000 rubles. (RUB 10,000,000 x 1.5% x 0.58). The total tax amount for the year will be 99,600 rubles. For quarterly advance payments, the calculation is carried out as follows: - for the first quarter - 7,500 rubles. (RUB 10,000,000 x 0.3% x 0.25); - for the second quarter - 17,400 rubles. (RUB 10,000,000 x 0.3% x 0.67 x 0.25) + (RUB 10,000,000 x 1.5% x 0.33 x 0.25); - for the third quarter - 37,500 rubles. (RUB 10,000,000 x 1.5% x 0.25).

For land plot No. 2, only the tax rate has increased. When calculating the adjustment coefficient, the month of the rate change refers to the full month of application of the 0.3% rate, since the change occurred after the 15th day. Thus, for a rate of 0.3%, the coefficients will be: 0.58 (7/12) for the year and 0.33 (1/3) for the third quarter. For a rate of 1.5%, the odds will be: 0.42 (5/12) for the year and 0.67 (2/3) for the third quarter. For the first 7 months, the tax amount in respect of land plot No. 2 will be 3,480 rubles. (2,000,000 rubles x 0.3% x 0.58), and for the subsequent period – 12,600 rubles. (RUB 2,000,000 x 1.5% x 0.42). The total tax amount for the year will be 16,080 rubles. For quarterly advance payments, the calculation is carried out as follows: - for the first quarter - 1,500 rubles. (RUB 2,000,000 x 0.3% x 0.25); - for the second quarter - 5,520 rubles. (RUB 2,000,000 x 0.3% x 0.33 x 0.25) + (RUB 2,000,000 x 1.5% x 0.67 x 0.25); - for the third quarter - 7,500 rubles. (RUB 2,000,000 x 1.5% x 0.25).

In relation to land plot No. 3, there was a decrease in cadastral value and tax rate. Starting from October 20, 2013, Omega LLC has the right to use both a reduced rate and a new cadastral value when calculating tax. The correction factor in relation to the previously established cadastral value for tax calculation will be 0.83 (10/12); in relation to the new cadastral value – 0.17 (2/12). For the first 10 months, the tax amount in respect of land plot No. 3 will be 124,500 rubles. (RUB 10,000,000 x 1.5% x 0.83), and for the subsequent period – RUB 2,550. (RUB 5,000,000 x 0.3% x 0.17). The total tax amount for the year will be 127,050 rubles. At the same time, advance payments for the 1st, 2nd, and 3rd quarters are calculated based on the previous cost and tax rate - in the amount of 37,500 rubles. (RUB 10,000,000 x 1.5% x 0.25).

Bibliography 1.. Tax Code of the Russian Federation (part two) dated 08/05/2000 No. 117-FZ (as amended on 04/20/2014 [Electronic resource]. – Access mode: https://www.consultant.ru. 2. Law of Moscow dated November 24, 2004 No. 74 “On land tax” [Electronic resource]. – Access mode: https://base.garant.ru/12137774/#ixzz2yNJJEokW3. 3. Letters of the Ministry of Finance of Russia dated September 5, 2013 No. 03-05-05-02/36540; 07/16/2013 No. 03-08-04-02/27809; 03/15/2012 No. 03-05-05-02/15; 03/13/2013 No. 03-05-04-02/ 7507 [Electronic resource]. – Access mode: https://www.consultant.ru. 4. Determination of the Constitutional Court of the Russian Federation dated 02/03/2010 No. 165-О-О [Electronic resource]. – Access mode: https: //www.consultant.ru 5. Resolution of the Thirteenth Arbitration Court of Appeal dated 06/09/2009 in case No. A56-54160/2008 [Electronic resource]. – Access mode: https://www.consultant.ru 6. Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated November 6, 2012 No. 7701/12 [Electronic resource] – Access mode: https://www.consultant.ru 7. Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated June 28, 2011 No. 913/11 [Electronic resource]. resource]. – Access mode: https://www.consultant.ru. 8. Resolution of the Seventh Arbitration Court of Appeal dated December 6, 2013 [Electronic. resource]. – Access mode: https://www.consultant.ru. 9. Letter of the Federal Tax Service of Russia dated January 25, 2013 No. BS-4-11/959 [Electronic. resource]. – Access mode: https://www.consultant.ru.

Pavlova A.A., tax specialist, Department of Tax and Legal Consulting,

CJSC United Consultants FDP

Who sets the cadastral value

In accordance with Art. 24.12 "(hereinafter referred to as Federal Law No. 135), the only one who can change the cadastral value (CV) of land is the government body of a federal subject or municipality. It is he:

- decides to conduct an initial cadastral assessment;

- approves its results;

- sets a date for the next revaluation.

However, the assessment for the purpose of establishing the CSA is carried out not by a government body, but by a special budgetary institution created by regional authorities and authorized to conduct cadastral assessment (Article 6, hereinafter referred to as Federal Law No. 237).

Since in most regions there were no such organizations in 2016, a transition period was in effect until 2020, and the powers to determine the CAP were transferred, as a rule, to private appraisers. According to Art. 24.14 Federal Law No. 135, an agreement was concluded with them to conduct an assessment. After carrying out work to determine the CPS, the experts compiled a report, the results of which were approved by the above-mentioned authority. From January 1, 2020, this work should be performed only by specialized budget organizations.

Read more about this in the material “Cadastral value of real estate”.

Step-by-step instructions when contacting the State Committee for Taxation Commission

The problem of changing the cadastral value of a land plot is solved in two ways:

- Administrative way, when contacting the State Committee for Taxation.

- By going to court after an administrative decision procedure.

In order for your application for revaluation of the land plot to be considered administratively , that is, by an authorized commission, contact the local cadastre and cartography department of the region to which the site subject to revaluation belongs. The appeal can be personal or by sending the necessary documents and their copies by registered mail with an inventory attached.

The application must be written using a special form, which can be found on the official website of Rosreestr or drawn up directly when contacting a cadastral specialist. It should contain the following information:

- all data of the copyright holder of the memory;

- his contact details for feedback;

- details (for legal entities).

The main part of the application indicates the reason for the application for land revaluation and the grounds that confirm the validity of the revaluation. The text of the application should be concise and clear, based on arguments requiring a revaluation of value.

You can download a sample form from here.

The application can be submitted exclusively by the owner of the site with the provision of a passport. If a representative acts on his behalf, he must present a power of attorney certified by a notary.

The following documents must be attached to the application:

- cadastral passport;

- a copy of the title document certified by a notary;

- documents confirming the unreliability of the information used when revaluing the cost of the site by the State Property Committee;

- a positive expert opinion on the assessment from an independent examination of assessment activities;

- receipt of payment of state duty.

An expert opinion must be obtained in advance, before contacting the authorized commission. To obtain it, you will need an extract from cadastral records.

The indicated documents must be submitted along with the application against receipt of receipt to the cadastral specialist . Without the specified documents, the application will not be accepted for consideration. It will take approximately 40 calendar days to consider the application, which includes the following deadlines:

- for consideration of the issue of accepting the application;

- consideration of the application;

- notification of the decision taken by the commission.

Please note that your claim for revaluation established by the State Tax Committee does not increase or decrease by more than 30% of the established amount.

If you adhere to a principled position on a more significant difference, then after receiving a refusal from the State Control Committee, you will have to go to court.

On the day whose date is indicated on the back of the issued receipt, you will appear for the result . If the decision on your application is positive, you must be provided with a new cadastral passport indicating the current cadastral value of the land plot and an extract from the accounting records with the introduction of new data after the revaluation. Are you interested in the cadastral and market value of land, how do they relate? Follow the link.

We pay duties

The fee for making corrections to cadastre records, including those made by State Committee for Taxation employees, is 350 rubles. To obtain a new cadastral passport with current data on the cadastral value of the plot, you will have to pay another 200 rubles.

If you decide the issue in court, the state fee for filing a statement of claim will be 200 rubles . For legal entities, rates for paying state fees will be slightly higher.

Keep in mind that the cost of obtaining an expert opinion is quite high. In the regions, it amounts to 2 thousand rubles per plot, based on the general assessment of the property. Subject to the need for an examination, the cost of work is calculated from 15,000 rubles . This is not surprising, since to reliably assess soil quality, expensive analyzes are carried out and the most modern equipment is used.

How to challenge the KSZ

If the owner of the plot considers the KS of the land to be overpriced, according to Art. 22 Federal Law No. 237, he has the right to challenge it. It does not matter in what year it was determined - this can be done before the results of the new revaluation are entered into the Unified State Register of Real Estate.

The owner has the right to challenge the assessment result in the following order:

- extrajudicial - by contacting the dispute resolution commission created at each territorial division of Rosreestr;

- judicial - by filing a lawsuit in court to challenge the KSZ and appealing the negative decision of the commission at Rosreestr.

The law does not oblige the owner to contact the commission first - he has the right to go straight to court. In any case, for this he will need a basis for appeal, which may be:

- identification of errors made by the expert during the assessment and which significantly inflated the final SSC;

- determination of market value by conducting an independent assessment commissioned by the owner on the date of determination of the CSA.

Read more in the article “Challenging the cadastral value of a land plot.”

Declaration of land tax

In January 2021, land tax payers will no longer prepare returns for the past year.

As of the 2020 tax period, land tax declarations have been cancelled. Article 398 of the Tax Code of the Russian Federation has lost force. This change was introduced by Federal Law No. 63-FZ of April 15, 2021.

Despite the abolition of reporting, payment amounts, as before, must be determined independently.

The inspectorates will send out tax payment notices, which will include the amount due. But you should not expect to receive such a notification. The inspectorate may send it much later after the due date for payment of the tax.

But updated declarations for periods up to 2021 will continue to be accepted by the Federal Tax Service - at the location of the land plots.

After the abolition of land tax declarations, a new obligation was introduced for land owners. If the Federal Tax Service did not take into account data about the site when calculating the tax and did not indicate it in the notification, you need to inform it about this site and provide documents confirming ownership. This will need to be done before December 31 of the year following the expired tax period. For failure to comply with this requirement, the company faces a fine of 20% of the unpaid tax amount.