The legislative framework

When an organization acquires a plot of land, it is reflected in accounting in accordance with PBU 6/10, the Tax Code of the Russian Federation, since this object is a fixed asset, as well as the norms of land and civil legislation.

The Land Code of the Russian Federation contains instructions that you can buy and sell such plots that have been assigned a cadastral number. The Civil Code of the Russian Federation states that the purchase and sale agreement must necessarily indicate the location of the actual location of the plot, its price, as well as restrictions or encumbrances, if any (

Accounting for land in accounting

And the amount of interest for the provision of installment plans is recognized in other income for each reporting period as they accrue (clause 16 of PBU 9/99). Until the final settlement with the buyer, the land is pledged to the seller (unless otherwise provided by the contract) and is reflected in the seller’s accounting in off-balance sheet account 008 “Securities for obligations and payments received.” Expert opinion When selling a plot on the terms of a commercial loan provided in the form of payment in installments, other income is recognized in accounting in the full amount of receivables (clauses 6.2, 10.1 of PBU 9/99), which at the time of transfer of ownership corresponds to the contract price of the plot ( excluding interest). And the amount of interest for the provision of installment plans is recognized in other income for each reporting period as they accrue (clause 16 of PBU 9/99).

The compensation amount includes the market value of the land, buildings on it and compensation for losses from the procedure (lost profits). The land is written off from the register on the day the rights to it are terminated.

The cost of the site on the balance sheet is included in other expenses, and compensation is included in income. When writing off a plot before the transfer of ownership of it is registered, an account is used to record the disposal. 45 subaccount "

Transferred real estate." Registration of a plot of land The acquired plot of land, like other assets, must be registered. First, the cost of the plot is determined. This information is contained in the purchase and sale agreement or other documents accompanying the transaction.

Features of land registration

There are several criteria that a piece of land must meet to be recognized as a fixed asset:

- The organization buys land in order to use it in its main activity, or for the purpose of subsequent rental.

- The land use period is more than a year.

- The plot of land is not planned for resale in the future.

- A company that plans to purchase a new site plans to make a profit from its use.

Thus, the site is included in the organization’s fixed assets. If a land plot is necessary for further sale, then its value is not included in non-current assets, but is reflected in the goods account. The value of an object consists of the costs that the company incurred to purchase it. It includes the following amount:

- the cost of the plot under the purchase and sale agreement;

- amounts that were paid to intermediaries (for example, a real estate agency);

- state duty paid upon land registration;

- interest on loans if the purchase of land was made with the use of loan funds (in this case, the cost of the plot, interest on the loan increases only until it is classified as fixed assets);

- other amounts that were paid when purchasing the plot.

A land plot is not subject to depreciation either in accounting or tax accounting, since it does not lose its useful properties . Therefore, the cost of purchasing land will not be included in the cost of production. Only if it is sold will the costs associated with its purchase reduce the profit received.

Important! When exploiting a land plot, it should be remembered that its use must be in accordance with the State Real Estate Cadastre. Thus, it will not be possible to independently decide to build buildings on the site. For example, when production premises are needed, the organization must buy an industrial site.

The organization bought a plot of land

Lev LLC decided to buy a plot of land for the construction of commercial warehouses for its own needs and size of 1 hectare. The organization contacted a real estate agency, where a plot of land was selected.

Land plots can only be purchased if they have passed state cadastral registration.

Lev LLC paid for the services of realtors in the amount of 180,000 rubles, incl. VAT 27,457.63 rubles, accounting entries were made based on a bank statement:

Debit 60 Credit 51 - 180,000 rub..

The cost of the service includes: state duty for registration of the site and other expenses associated with the acquisition of the site.

A purchase and sale agreement was concluded with the seller of the plot and an amount of 1,600,000 rubles was transferred. An entry was made in accounting based on the extract:

Debit 60 Credit 51 - 1,600,000 rub..

The sale of land plots is not subject to VAT taxation (in accordance with paragraph 6, paragraph 2, article 146 of the Tax Code of the Russian Federation).

The organization received a certificate of state registration of the right to the site.

Documentation procedure

The legislation does not provide for any special documents intended for recording land plots. The main document is the contract. In this case, you will need to prepare it in 3 copies, one of which is transferred to Rosreestr.

The transfer of land can also be carried out under an agreement, but in this case it must indicate that it is also an act of acceptance and transfer. You can choose the form for reflecting transactions with fixed assets in the company yourself, but such unified documents as OS-1, OS-6 and OS-6b can also be used.

Sometimes a company does not purchase a plot, but receives it as a contribution from the founder as a gift or in exchange for other property. In this case, an objective assessment of the land plot will be required, as well as its acceptance for registration at cadastral value . If a company leases a site, a lease agreement must be drawn up. For a long lease period, such an agreement must be registered with Rosreestr.

Accounting for land when selling/purchasing

When purchasing land, its initial cost is the amount of purchase costs. These include:

- Funds transferred to the seller under the agreement;

- Registration fees and charges;

- Payment to the competent authorities for cadastral documents and land surveying;

- Payment for registration data;

- Payment for the work of intermediaries (if any);

- Other purchase and registration costs.

Accounting for land acquisitions is carried out in accordance with PBU 6/01 in a manner similar to accounting for fixed assets:

| Operation | Account correspondence | A document base | |

| Debit | Credit | ||

| Paid plot of land | 60 | 51 | Bank statement |

| Purchase costs reflected | 08 | 60, 76 | Contract of sale |

| Acceptance of an object for accounting as fixed assets | 01 | 08 | Transfer and Acceptance Certificate |

After registration, the enterprise is required to pay land tax. Purchase costs reduce the taxable base under the Unified Agricultural Tax. Expenses are not accepted immediately, but over a certain period (indicated in the accounting policy). It must be at least 7 years.

To sell land, you need an agreement and an act in form OS-4. The cost on the balance sheet is included in other expenses, and the proceeds are included in income.

Example #1. Accounting for land on the balance sheet

Let's consider an example of accounting for a land plot on the balance sheet of an organization. Niva LLC sold for 2,150 thousand rubles. a plot with a balance value of 1,870 thousand rubles. Entries required:

Dt 62 Kt 91-1 2,150 thousand rubles - the plot has been sold;

Dt 91-2 Kt 01 1,870 thousand rubles — the value of the land is written off according to the balance sheet;

Dt 99 Kt 91,280 thousand rub. — reflects the financial result of the transaction.

The sale of land is not subject to VAT (clause 2 of Article 146 of the Tax Code).

Land plot: accounting and tax accounting

To account for a land plot in accounting, an 08 account is provided, to which a corresponding sub-account is opened . It opens for each new object. It reflects the costs that increase the cost of the object. The postings will be as follows:

| Business transactions | D | TO |

| Purchased land | 08.1 | 60 |

| Intermediary services, as well as state duty, are reflected | 08.1 | 76 |

| The land plot is reflected in accounting as fixed assets | 01 | 08.1 |

| If the land plot is purchased for the purpose of resale | 41 | 60 |

| Reflection of proceeds from sales if the plot was purchased for the purpose of resale | 62 | 91(90) |

| Write-off of the cost of the site | 91(90) | 01(41) |

| Reflection of other expenses for the sale of the site | 91(90) | 76,60 |

Important! When financial statements are prepared, land plots are reflected as non-current assets (the first section of the balance sheet).

Answer:

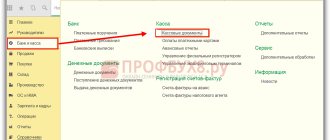

The acquisition of a land plot in 1C UPP and Comprehensive 1.1 must be documented in the document Receipt of goods and services with the transaction type Construction Objects.

Acquisition of construction projects in 1C UPP and Komplexnaya 1.1 Acquisition of construction objects in 1C UPP and Komplexnaya 1.1

In this case, it is necessary to create a directory element Construction objects. The expense item must be indicated with the nature of the Investment in non-current assets.

The accounting account is indicated in the tabular part of the document - 08.01, the VAT account - 19.08.

If there are additional expenses that need to be attributed to the cost of this land plot, then when they are received in the documents it will also be necessary to indicate the cost item with the nature of Investment in non-current assets, accounting account 08.01 and the Construction Project.

When accepting a construction project for accounting as a fixed asset, you will need to indicate the specific construction project and the accounting account. And the program will collect all the costs attributed to this account and object and record it as the cost of the fixed asset.

After receipt, the construction project (land plot) must be accepted for accounting as a fixed asset using the document Acceptance for accounting of fixed assets.

Acceptance of a land plot for accounting as a fixed asset in 1C UPP and Complex 1.1

We indicate the accounting account in BU and NU where the cost of acquisition and the construction project were assigned and click the Calculate amounts button.

In the Fixed Assets tabular section, create a new fixed asset and record the document.

On the next General Information tab, we must indicate the method for reflecting depreciation expenses.

But land plots are not depreciated. Nevertheless, we create a method, we simply do not fill it with anything except the name.

The method for calculating depreciation, if depreciation is not necessary, do not fill it out.

I indicated the name in the example: Not accrue, so that it would be clear what this method is.

After this, on the accounting tab we indicate that the fixed asset has been accepted for accounting.

Do not charge depreciation in the document Acceptance of fixed assets for accounting in 1C UPP and Complex 1.1

We indicate absolutely any method of calculating depreciation, useful life and depreciation account.

The main thing: do not check the Accrue depreciation checkbox.

Then all the entered depreciation settings will not matter. But you will have to fill them out, since they are required.

Do not forget to indicate the account of the fixed asset itself. This field is hidden after all the shock absorption settings and is easy to miss.

If you maintain management accounting for fixed assets, then the tab for this type of accounting is filled out in the same way.

But in tax accounting you need to set the value Cost is not included in expenses.

Tax accounting in the document Acceptance of fixed assets for accounting in 1C UPP and Complex 1.1

That's it - now the document can be processed. Check that the postings for accounting for the construction project have been successfully generated.

Postings of acceptance for registration of a land plot in 1C UPP and Complex 1.1

But depreciation on such a fixed asset will not be calculated in the 1C program.

If you want to learn more about production accounting and cost distribution in 1C Integrated Automation 2, then come to the course:

Land revaluation

A land plot is a resource that does not change over time and does not lose its properties. Therefore, the period of effective use is not determined for it. Its cost cannot be recovered through depreciation. Until 2011, there was a ban on the revaluation of land plots recognized by the OS of the organization. But later this ban was lifted. Therefore, organizations have the right to decide to reassess it. This should be reflected in the company's accounting policies. When revaluing land plots, the organization must do this regularly. The company determines the procedure for such a procedure, as well as the rules for conducting it independently.

Cost adjustment occurs when using price indices determined by statistical bodies, or by directly bringing the cost into line with market values on a certain date. After the revaluation, a corresponding act is drawn up, which is signed by all members of the commission and the head of the company. Documents confirming the adequacy of the amount received at which the land will be reflected in accounting are attached to the act.

Important! When revaluing land, you should remember that it is only possible with accounting. The Tax Code of the Russian Federation does not provide for this possibility.

Tax accounting under OSNO

When purchase and sale transactions are concluded, the VAT tax base does not arise. The seller does not need to allocate VAT, and the buyer does not need to reimburse it. If the company is located on OSNO, then in the case of calculating income tax, the costs of purchasing the site are not included in the tax base. This can only be done if the plot is sold. An exception is the purchase of land from state or municipal authorities. In this case, the company determines the useful life of the land independently and during this period of time evenly applies the purchase price to taxable expenses. It should be remembered that this period should not exceed 5 years. The company can also include a taxable portion of the costs of purchasing land (30% of the base for the previous year) and continue to do so until the costs are paid in full. In this case, a difference arises between accounting and tax accounting, and hence the emergence of permanent tax differences.

Despite the fact that the land is classified as fixed assets, it is not subject to property tax. According to the clarifications of the Russian Ministry of Finance, an independent tax is provided for land plots, therefore they should not be included in the tax base for property tax. Land tax is calculated in accordance with Ch. 31 Tax Code of the Russian Federation. This is a local tax based on the cadastral value of the land. The tax rate is determined by the municipality, which may also provide benefits for it. Companies report land tax every quarter and make advance payments during the tax period.

Acquisition of land plots

In accordance with Art. 264.1 of the Tax Code of the Russian Federation, expenses for the acquisition of land plots from lands in state or municipal ownership, on which buildings, structures, structures are located, or which are acquired for the purpose of capital construction of fixed assets, can now be included in expenses for corporate income tax when provided that the taxpayer entered into an agreement to purchase such plots during the period from January 1, 2007 to December 31, 2011. The innovation is largely related to the re-registration of land rights. Thus, Federal Law dated October 25, 2001 N 137-FZ “On the entry into force of the Land Code of the Russian Federation” establishes the obligation of legal entities, with the exception of those specified in paragraph 1 of Art. 20 of the Land Code of the Russian Federation, re-register the right of permanent (perpetual) use of land plots to the right to lease land plots or acquire land plots in ownership before January 1, 2008. Take advantage of the provisions of Art. 264.1 of the Tax Code of the Russian Federation will also be available to taxpayers purchasing land plots for construction in accordance with Art. Art. 30 - 32 Land Code of the Russian Federation.

The legislator provided the taxpayer with the opportunity to choose the option of writing off such expenses, which is subject to enshrinement in the accounting policy for tax accounting purposes.

First option. Expenses are recognized evenly over a period determined by the taxpayer independently, but not less than 5 years.

Second option. Expenses are recognized in the reporting (tax) period in an amount not exceeding 30% calculated in accordance with Art. 274 of the Tax Code of the Russian Federation of the tax base of the previous tax period until the full amount of these expenses is fully recognized. For calculation purposes, the tax base of the previous tax period is determined without taking into account the amount of expenses of the specified tax period for the acquisition of rights to land plots.

Regardless of the write-off options used when purchasing land plots on an installment plan, the period of which exceeds the (actual) write-off period determined by the taxpayer, such expenses are recognized as expenses of the reporting (tax) period evenly over the period established by the agreement (clause 1, clause 3, art. 264.1 Tax Code of the Russian Federation). Expenses for the acquisition of land are included in other expenses associated with production and (or) sale from the moment of documented submission of documents for state registration of the specified right. Such a document is a receipt of receipt by the body carrying out state registration of rights to real estate and transactions with it, documents for state registration of these rights (clause 2, clause 3, article 264.1 of the Tax Code of the Russian Federation).

Writing off expenses for the acquisition of land in tax accounting will lead to permanent differences in accounting, since, according to clause 17 of PBU 6/01 “Accounting for fixed assets,” land plots are not subject to depreciation.

Example 1. Kraskor LLC purchased a plot of land from the city worth 500,000 rubles. In February 2007, the documents were submitted for state registration. The accounting policy for tax accounting purposes of Kraskor LLC stipulates that “expenses for the acquisition of land plots in municipal or state ownership are recognized in the reporting (tax) period in an amount not exceeding 30% of the calculated tax base of the previous tax period up to full recognition of the entire amount of these expenses.”

To reflect transactions in accounting, the following calculation is made (Table 1).

Table 1

| Year | Tax base of the previous tax period, rub. | Recognized land expenses, rub. | Tax base of the current tax period, rub. | PNA amount, rub. |

| 2006 | — | — | 800 000 | — |

| 2007 | 800 000 | 240,000 (800,000 x 30%) | 500 000 | 57,600 (240,000 x 24%) |

| 2008 | 740 000 (500 000 + 240 000) | 222,000 (740,000 x 30%) | -300 000 | 53,280 (222,000 x 24%) |

| 2009 | 0 0 > (240 000 — 300 000) | 0 | 200 000 | 0 |

| 2010 | 200 000 | 38,000 200,000 x 30% > (500,000 - 240,000 - 222,000) | — | 9,120 (38,000 x 24%) |

| Total | X | 500 000 | X | 120 000 |

The ban on attributing expenses to the acquisition of privately owned land plots has never been lifted. As before, land and other environmental management facilities are not subject to depreciation (clause 2 of Article 256 of the Tax Code of the Russian Federation). At the same time, according to paragraphs. 3 p. 1 art. 254 of the Tax Code of the Russian Federation, the taxpayer’s expenses for the acquisition of property that is not depreciable are included in material expenses in the full amount as it is put into operation.

Conflicting judicial practice has developed on the issue of including land acquisition costs in the tax base. For example, in favor of taxpayers on the basis of paragraphs. 3 p. 1 art. 254 of the Tax Code of the Russian Federation, decisions were made by the FAS CO in Resolution dated 08/17/2004 N A08-2355/04-21-16, FAS ZSO in Resolution dated 07/13/2005 N F04-4368/2005(12952-A75-33); in favor of the tax authority - FAS UO in Resolutions dated March 15, 2005 N F09-756/05-AK, dated November 10, 2005 N F09-756/05-S7; FAS PO dated 08/10/2006 N A65-11934/2005-SA2-11 (ground: clause 2 of article 256 of the Tax Code of the Russian Federation).

To assess tax risks in the judicial resolution of a dispute, of indisputable interest is the Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated March 14, 2006 N 14231/05, according to which the costs of acquiring land plots do not form the tax base, since on the basis of clause 2 of Art. 256 of the Tax Code of the Russian Federation, land is classified as objects not subject to depreciation. Absence in ch. 25 of the Tax Code of the Russian Federation, the rules on accounting for expenses for the acquisition of land plots by calculating depreciation amounts deprive the taxpayer of the opportunity to reduce the tax base for income tax by the corresponding amounts.

Except for the cases specified in Art. 264.1 of the Tax Code of the Russian Federation, current legislation provides the taxpayer with the opportunity to write off the cost of acquired land only at the time of its sale on the basis of paragraphs. 2 p. 1 art. 268 Tax Code of the Russian Federation.

USN and Unified Agricultural Tax

As for companies using the simplified tax system, the same rules are established for them as for companies using the main tax system. That is, they do not have the right to reduce their income by the amount of expenses associated with the purchase of a plot. However, in the case of resale of a plot, it is regarded as a product and costs can be taken into account when determining the simplified tax system. If a company pays the Unified Agricultural Tax, then it is provided with a special procedure for recognizing costs associated with the purchase of land. For example, a company can determine the period during which costs incurred will be written off. This period must be at least 7 years. However, there are certain requirements for the site. It must be paid for, used only for growing agricultural products, and also be in the process of state registration.