How to correctly enter the required details into the delivery note in 2021

The recipient of the goods enters information on the delivery note into accounting, and not specifying the details does not affect the posting of products. Gross weight - the weight of the goods with containers or packaging - does not have to be noted as a detail when posting goods individually or by weight.

When filling out the invoice, the seller indicates the price, amount excluding VAT, calculation and amount including VAT. In cases where the goods are indicated with VAT on line 11 of the invoice, then, by decision of the tax service, it is possible to additionally charge the amount of tax to the organization. If OKDP is not indicated in the invoice, the risks of not accruing a VAT deduction are minimal.

Since the invoice is filled out by the seller, he indicates his type according to OKDP, which does not interfere with the receipt of data by the tax office about the buyer (taxpayer).

Which tax identification number and checkpoint to indicate in TORG-12 when working with a separate division

Since the buyer picks up the goods independently and your organization does not ship them to third parties specified by the buyer, the consignee of the goods in this case is the buyer.

The TORG-12 form does not specify the address of the consignee and the payer, so it may indicate both the legal and actual address of the buyer (warehouse address).

In our opinion, when filling out these details, you should be guided by the details of the parties specified in the supply agreement. However, taking into account the presence of a letter from the buyer clarifying his details, we believe that the seller should indicate in the appropriate lines of the TORG-12 form the address of the buyer’s separate division (address of its warehouse).

Please note that in the unified form of consignment note TORG-12 in the lines “Consignee” and “Payer” the following must be indicated: organization, address, telephone, fax and bank details.

What is the TORG-12 form

The TORG 12 consignment note is quite often used by organizations to register inventory items (material assets), measured in pieces or weight. The head of the organization may not use this form (see Federal Law-402 “On Accounting”). The consignment note (you can download it below) has a number of advantages, which we will discuss in this article.

You can download TORG 12 at the end of the article.

The TORG 12 consignment note form is included in the album of unified forms (OKUD 0330212). However, with the entry into force of Law 402-FZ, primary documents do not necessarily have to be in a unified form. It is enough that the document contains the entire list of mandatory details specified in the law.

However, the unified form TORG 12 (can be lower) is so convenient that many entrepreneurs have not abandoned the use of this consignment note for several reasons:

- It is familiar and understandable.

- Meets regulatory requirements.

- If necessary, the delivery note will serve as the basis for resolving controversial situations, for example, claims regarding the quality of the purchased goods (Law No. 2300-1).

- Confirms the fact of receipt or shipment of goods (Article 458 of the Civil Code of the Russian Federation).

- Is the rationale for the adoption of VAT.

- Serves as confirmation of the expiration of the warranty period (Law No. 2300-1), etc.

Is it necessary to indicate the Taxpayer Identification Number (TIN) and KPP on the delivery note?

12/18/2008 Question: If yes, then on the basis of what document and how can you “force” suppliers to change all documents from the beginning of the year if they have not provided the Taxpayer Identification Number (TIN) and KPP for 7 months.

Is it also necessary to issue a consignment note and what details are required in it? Answer: With regard to the preparation of a consignment note, the Instructions for the use and completion of forms of primary accounting documentation for recording trade operations, approved by Resolution of the State Statistics Committee of the Russian Federation dated December 25, 1998 N 132, contain insufficient information on filling out the TORG-12 form.

It should be noted that the organization’s demands for replacing primary documents are unlawful.

The supplier does not have the right to issue new documents, since according to the opinion of the Ministry of Finance of Russia, expressed in letter dated December 8, 2004 N 03-04-11/217, organizations do not have the right to issue new invoices with the same numbers and dates in place of previously issued old invoices. In our opinion, this provision also applies to invoices. At the same time, the current legislation of the Russian Federation allows changes to be made to primary documents, in particular, in accordance with clause 5 of Article 9 of the Federal Law of November 21, 1996 N 129-FZ “On Accounting”, corrections can be made to primary accounting documents (except for cash and banking documents) be introduced in agreement with the participants in business transactions, which must be confirmed by the signatures of the same persons who signed the documents, indicating the date of the corrections.

Please note that corrections are made only by the persons who originally signed this document and only in agreement with the other counterparty.

At the same time, the consignment note, the form of which was approved by Decree of the State Statistics Committee of the Russian Federation dated November 28, 1997 N 78

“On approval of unified forms of primary accounting documentation for recording the work of construction machinery and mechanisms, work in road transport”

(form N 1-T), is the main transportation document intended to record the movement of inventory items and payments for their transportation by road.

We recommend reading:

At the same time, the obligation to draw up a customs form arises for the shipper only if goods are transported by a motor transport organization under a contract for the carriage of goods (Section 2 of the Instructions for the use and completion of forms approved by Resolution of the State Statistics Committee of the Russian Federation dated November 28, 1997 N 78, clause 2 of Article 785 Civil Code of the Russian Federation, clause 47 of the Charter of Road Transport of the RSFSR, approved by Resolution of the Council of Ministers of the RSFSR 01/08/69 N 12).

Thus, if the delivery of goods is carried out by the supplier’s or buyer’s transport (in case of self-pickup) without the involvement of a motor transport organization, drawing up a consignment note is not required. In this case, it is enough to use a consignment note, the form of which is approved by Decree of the State Statistics Committee of the Russian Federation dated December 25, 1998 N 132 (Form N TORG-12).

A similar point of view was expressed by arbitration courts (see, for example, resolution of the FAS North-Western District dated September 14, 2005 N A26-1530/2005-217, resolution of the FAS North-Western District dated December 28, 2006 in case No. A13-16213/2005 -19, resolution of the Federal Antimonopoly Service of the North-Western District dated December 26, 2007 in case No. A05-3299/2007). Dubinyanskaya E.N. Head of the Audit and Finance Department of United Consulting Group CJSC Answers to questions posted in the Codex Legal Reference System 12/18/2008

Corrections and changes

In which cases?

The document must be filled out correctly in all columns. TORG-12 does not contain unimportant and unnecessary information.

It doesn’t matter where the error was made: in the name of the supplied product, in the price, in quantity, in the % VAT rate, or in the details. The document must be corrected and brought into proper form.

One way or another, any error in the delivery note will not pass without leaving a trace and will lead to the emergence of new ones.

Editing technique

Correction of original documents in the absence of replacements is possible. Primary accounting documents (except for cash and bank documents) can be adjusted (clause 7 of article 9 of the Law).

All participants in the operation must be informed about the change, who confirm their consent with the signature of those persons who signed the document earlier. Be sure to indicate the date when the corresponding changes were made (Letter No. 07 02 06/9 dated 01/25/2012).

An example of the most common way to change data during shipment is to replace TORG-12.

Canceling an incorrectly completed document and generating a new one that meets all the requirements is the most common correction method. Correction in the original document is not prohibited, but is done, in most cases, if it is impossible to replace the document.

If an error is made on only one sheet, it will be enough to replace only it without changing the entire package of documents.

The document flow in accounting is very large, many forms are subject to strict accounting and therefore are filled out extremely carefully. Although the TORG-12 invoice is not such, it requires no less careful attention. In some cases, the amount of tax to be paid and even the relationship with the tax authorities may depend on its correctness.

“New Accounting”, 2006, N 2 Question: During a desk audit, due to the supplier’s failure to fill out the buyer’s OKDP and OKPO in the invoice (form N TORG-12), the Federal Tax Service Inspectorate refused to reimburse the “input” VAT. Are suppliers required to fill out the buyer's OKDP and OKPO in the delivery note in form N TORG-12? Are the actions of the Federal Tax Service legal? Answer: The standard form of the consignment note (unified form N TORG-12) was approved by Resolution of the State Statistics Committee of Russia dated December 25, 1998 N 132. The specified form is the primary accounting document. In accordance with the Procedure for the use of unified forms of primary accounting documentation, approved by Resolution of the State Statistics Committee of Russia dated March 24, 1999 N 20, all details of the unified forms must remain unchanged (including codes). Removing individual details from unified forms is not allowed. Federal Law No. 129-FZ of November 21, 1996 “On Accounting” provides that primary accounting documents are accepted for accounting if they are drawn up in the form contained in the albums of unified forms of primary accounting documentation (clause 2 of Article 9 of Law No. 129- Federal Law). Since the coding zones for certain information (in particular, OKPO, OKDP) are provided for by the unified form N TORG-12, the specified details (codes) must be filled out by suppliers without fail. Russian legislation does not provide otherwise. Another question is whether the Federal Tax Service’s refusal to reimburse “input” VAT is justified due to the supplier’s failure to fill out codes in form N TORG-12. In our opinion, it is illegal. A document serving as the basis for accepting the presented amounts of tax for deduction or reimbursement in the manner prescribed by Chapter. 21 of the Tax Code of the Russian Federation is an invoice (clause 1 of Article 169 of the Tax Code of the Russian Federation). Therefore, if the supplier’s invoice is issued in accordance with the requirements specified in clause 5 of Art. 169 of the Tax Code of the Russian Federation, then the actions of the Federal Tax Service in terms of refusing to reimburse the buyer for “input” VAT on the grounds specified in the question contradict the norms of tax legislation. I. Gorshkova Signed for publication on January 26, 2006

The TORG-12 consignment note is a document that accompanies the delivery of inventory items. The form is not mandatory for use.

Packing list

This can be either a carrier of a third-party transport organization or a representative of the purchasing organization.

The head of the enterprise can accept the goods without a power of attorney - in this case, he signs in the line “Cargo accepted” and does not fill in the lines indicating the details of the power of attorney. At the same time, in both lines “The cargo was received by the consignee” and “The cargo was accepted” the same person can sign (if he has both a power of attorney for goods and materials and the right to sign primary documents).

In this case, the signature is placed only in the line “Cargo received”.

In the column “Consignor”, in accordance with the constituent documents, the full or abbreviated name of the consignor, legal address (possibly together with the actual one), telephone number and bank details (r./account and BIC required!) must be indicated.

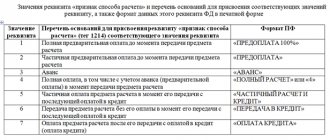

Is the “base” line of the TORG-12 invoice mandatory?

For example, in the resolutions of the FAS of the Central District dated 04/09/2010 N A68-4631/09, dated 07/22/2008 N A08-8948/06-10-15, FAS of the North-Western District dated 04/30/2010 N F07-3761/2010, dated 05/04/2009 N A44-80/2008, the judges came to the conclusion that the issuance by the supplier of an invoice for payment containing the essential terms of the contract, and the payment of such an invoice by the buyer, are considered by the courts as the conclusion of an agreement by the parties in writing.

In the decisions of the Federal Antimonopoly Service of the Ural District dated 02/10/2011 N F09-250/11-S3, the Ninth Arbitration Court of Appeal dated 10/18/2010 N 09AP-24205/2010, the judges considered that the buyer’s applications and the invoices issued by the seller on their basis indicate that the parties had concluded an agreement . In this regard, we believe that in the “grounds” line, not only the details of the purchase and sale (supply) agreement can be indicated, but also, for example, the details of the buyer’s application, the supplier’s invoice for payment.

Consignment note TORG-12, filling rules

The TORG 12 consignment note is prepared by the seller. The form contains information about the seller, buyer, name of the product, its quantity and cost, information about the financially responsible persons who shipped and received the goods.

| Invoice column TORG 12 | Invoice TORG 12, filling rules |

| Shipper organization, address, telephone, fax, bank details | The name fits both full and short. |

| Structural subdivision | Maximum complete information (name, contact details). |

| Provider | Full and short name, address and bank information. |

| Consignee | Same as for the supplier. |

| Payer | The purchasing organization is indicated (if it independently purchases and pays for the cargo). |

| Base | The data of the contract or work order on the basis of which the transaction took place is indicated. |

| OKUD and OKPO codes, type of activity according to OKDP | The codes assigned to the organization by the statistics body upon registration are indicated. |

| Tabular section TORG 12 | The supplier lists the goods sold, their units of measurement and quantity, gross and net weight, price and VAT rate. The amount of goods with and without VAT is also indicated here. |

| The consignee received the cargo | Signature of the manager or employee who has the right to sign (order, power of attorney). |

| Accepted the cargo | Signature of the financially responsible person receiving the goods (storekeeper, driver, manager, etc.). |

| By power of attorney No. | Power of attorney details of the employee who received the cargo. Not to be filled in if the manager signed the line “The cargo was received by the consignee”. |

| The consignee received the cargo | To be completed when the cargo is received by the head of the organization. |

| Supplier side printing location | The supplier's seal is affixed, if available. |

| Place of seal on the part of the consignee | The consignee's stamp is affixed. If the cargo is received by proxy, then stamping is not required. |

| Date indicator | The actual date of shipment must match the date on the invoice. |

Checkpoint in the invoice

In this case, the invoice is issued on the basis of the invoice, so the information in both documents must match - in the “Buyer” column in the invoice and in the “Payer” column in the delivery note.

If the organization does not have a separate division registered at all, and the checkpoint was assigned in connection with tax registration when applying UTII, then the name and address of the organization must be indicated in the invoices both in the “Payer” column and in the “Consignee” column. And in this case, the buyer must indicate the organization’s checkpoint in both columns in accordance with the details specified in the concluded agreement. At the same time, such details as checkpoints may not be indicated at all in the delivery note.

It is indicated only as an optional additional detail. Rationale From the recommendation In what cases should an organization register with the tax office and how to do it How to register separate divisions Based on the location of each of its organizations, the organization must register with the tax authorities ().

Preparation of delivery notes and invoices

Answer The consignee must be indicated on the invoice and delivery note.

For more details on this, see the materials in the justification.

The rationale for this position is given below in the materials of the Glavbukh System.

1. Situation: What information about the consignee and consignor must the seller indicate in the invoice for shipment? “Lines 3 “Consignor and his address” and 4 “Consignee and his address” are filled out by the seller only when selling goods. If the seller and the shipper are different persons, then in line 3 indicate the full or abbreviated name and postal address of the shipper, as in its constituent documents.

INN and KPP in the invoice

1016 lawyers are now on the site Good afternoon! Are suppliers required to indicate INN and KPP (their own and the buyer’s) in the delivery note?

We recommend reading: List of documents for a contractor in a construction organization to confirm a preferential pension

Where is this stated in the Laws? August 14, 2014, 14:39, question No. 530088 Julia, Moscow Collapse Victoria Dymova Support employee Pravoved.ru Try looking here: You can get an answer faster if you call the free hotline for Moscow and the Moscow region Free lawyers on the line: 7 Answers from lawyers (3)

- Padva Alexander VladimirovichLawyer, Moscow

- 931response

413 reviews

There is no unified form of TORG-12; it was canceled in 2013.

From January 1, 2013, an organization or entrepreneur can approve its own form of consignment note. The details of the Shipper, Consignee, Supplier and Payer must indicate: name of the organization or entrepreneur, address, telephone, fax, tax identification number, checkpoint, bank details, bank name, BIC, correspondent account, r/account or l/account.

Federal Law “On Accounting” and August 14, 2014, 14:48 Was the lawyer’s answer helpful? + 1 — 0 Collapse Client clarification Thank you!

The supplier claims that INN and KPP are not bank details. 14 August 2014, 14:56

All legal services in Moscow Best price guarantee - we negotiate with lawyers in every city on the best price.

Moscow

- 931response

413 reviews

The supplier claims that INN and KPP are not bank details. Yulia Let him send an accountant for advanced training. 14 August 2014, 14:57 Was the lawyer's answer helpful? + 0 — 0 Collapse Client clarification Believe it or not, this supplier is the Metro Cash & Carry network.

)))) August 14, 2014, 14:59

- 931response

413 reviews

Believe it or not, this supplier is the Metro Cash & Carry chain. ))))Yulia-Western brand was dragged to the market, but they were not taught to work according to Russian laws... At least you will bring them a ray of light))) August 14, 2014, 15:02 Was the lawyer’s answer helpful?

+ 0 — 0 Collapse

Similar questions

- June 30, 2021, 12:39, question No. 1300431

- June 30, 2021, 12:39, question No. 1300432

- December 22, 2015, 21:04, question No. 1081066

- 07 July 2015, 15:24, question No. 896959

- 05 July 2021, 14:22, question No. 1687561

see also

Accounting and legal services

41, BC "Finlyandsky" To send a comment you need. If you need additional information, have any questions or need help, WE OFFER READY TURNKEY COMPANIES WITH OR WITHOUT AN OPEN ACCOUNT, AND WE WILL ALSO MANUFACTURE TO ORDER, FOR ANY OF YOUR REQUIREMENTS When purchasing a ready-made company from our company, you can count on comprehensive consulting assistance on all issues regarding the start of your business. Our lawyers are ready to come to your aid at any time in the formation and development of a ready-made company that you purchased from us.