An invoice in Russia is a tax document of the established form, which is required to be drawn up by the seller or contractor. Based on received invoices in , and based on issued invoices - “Sales Book”.

According to the Tax Code of the Russian Federation, only VAT taxpayers are required to provide customers with an invoice. Companies that are on the simplified tax system are not payers of this tax and do not have to prepare invoices.

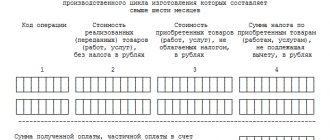

The invoice contains data on the name and details of the seller and buyer, the list of goods or services, their price, value, rate and amount of VAT. This list is mandatory and enshrined in the Tax Code of the Russian Federation. The invoice must also contain information about the number and date of issue of the invoice, and, if necessary, the amount of excise tax, the country of origin of the goods, and the customs declaration number.

In Russia, the purpose of an invoice is tax accounting for VAT. It imposes on the seller the obligation to transfer VAT to the budget; for the buyer it serves as the basis for presenting VAT for deduction.

Packing list

The invoice is a primary document, which is drawn up in 2 copies and serves as proof of transfer and the basis for writing off (accepting for registration) the goods. The invoice must contain the signature and seal of the seller and buyer. It is drawn up in two copies, one of which remains with the supplier, the second with the recipient.

Goskomstat has approved a unified form of consignment note (form No. TORG-12), but an organization can use its own form.

The invoice must contain the following details: name, number and date of the document, name of the supplier organization; name of the product, its quantity and cost; positions of responsible persons, their signatures and seals. If the invoice form does not correspond to the Torg-12 form, it can also be accepted for accounting by the purchasing organization.

When participating in trade operations of a third-party transport company, experts recommend abandoning the Torg-12 form and using another document - a consignment note (Bill of Lading).

Types of operations

Goods (invoice)

The type of transaction Goods (invoice) should be selected in the case when it is necessary to reflect the receipt of goods from the supplier (account 41 “Goods”) or materials (account 10 “Materials”).

It allows you to register the receipt of goods both at the wholesale warehouse and at retail outlets: automated and non-automated.

Find out the features of filling out the document Receipt (act, invoice) type of transaction Goods (invoice)

Services (act)

The transaction type Services (act) formalizes the receipt of services (work) of third-party organizations in the case when they are debited to the following accounts:

- 08.03 “Construction of fixed assets”;

- 20 “Main production”;

- 23 “Auxiliary production”;

- 25 “General production expenses”;

- 26 “General business expenses”;

- 44 “Sales expenses”;

- 91 “Other income and expenses”;

- 97 “Deferred expenses”.

Find out the features of filling out the document Receipt (act, invoice) type of transaction Services (act)

Fixed assets

Transaction type Fixed assets are convenient to use when it is necessary to simultaneously register the receipt and acceptance for accounting of an object of fixed assets (FA). In this case, the conditions must be met that for the OS object:

- acceptance for accounting (commissioning) is carried out simultaneously with receipt;

- no installation required;

- no additional expenses are required to be reflected;

- in accounting (AC) the linear method of calculating depreciation is used;

- the parameters for calculating depreciation for tax accounting (TA) and accounting are the same (SPI, initial cost);

- the procedure for including cost in the composition of expenses for NU assumes only the calculation of depreciation;

- depreciation bonus is not accrued according to NU;

- There is no special coefficient for depreciation according to NU.

In this case, the document generates transactions using account 08.04.2 “Purchase of fixed assets”.

Find out the features of filling out the document Receipt (act, invoice) type of operation Fixed assets .

Goods, services, commission

A universal type of operation in which you can register an admission:

- goods and materials;

- services (works) of third parties;

- returnable packaging;

- goods on commission from the consignor;

- goods and services (works) purchased for the principal;

This type of operation is convenient to use when different inventory items and services are simultaneously taken into account with one primary document.

The supplier, as a primary document, issued a universal transfer document (UDD), which reflects the supply of goods and at the same time reflects the services for their delivery.

Materials for recycling

The Materials for processing operation registers the receipt of customer materials for customer processing. The materials will be recorded in off-balance sheet account 003.01 “Materials in warehouse”.

Find out the features of filling out the document Receipt (act, invoice) type of operation Materials for processing .

Equipment

Equipment operation reflects the receipt from the supplier:

- equipment that requires installation (account 07 “Equipment for installation”) and is subsequently taken into account as an installation item;

- fixed assets (account 08.04.1 “Purchase of components of fixed assets”), which are subject to further registration as fixed assets.

Find out the features of filling out the document Receipt (act, invoice) type of operation Equipment .

Construction objects

Transaction type Construction objects should be selected to reflect the receipt of objects recorded in the accounts:

- 08.01 “Acquisition of land”;

- 08.02 “Acquisition of natural resources”;

- 08.03 “Construction of fixed assets”.

Find out the features of filling out the document Receipt (act, invoice) type of operation Construction objects .

Leasing services

With a document with the transaction type Leasing services , the lessee reflects the accrual of current lease payments when accounting for property on the lessee’s balance sheet.

Find out the features of filling out the document Receipt (act, invoice) type of transaction Leasing services .

Difference between invoice and delivery note

The following can be distinguished between an invoice and a delivery note:

Documents come in various forms;

An invoice has a strictly regulated form, while a delivery note has a free form;

The delivery note is signed in two copies - by the seller and the buyer, the invoice - only by the supplier;

These documents do not replace each other, but complement each other and are issued simultaneously upon transfer of goods;

An invoice is issued for payment for goods and services, while an invoice is issued only upon shipment of goods, the provision of services is formalized by an act;

Unlike an invoice, an invoice does not confirm the fact of transfer of goods to someone, but only serves as a basis for VAT offset;

Based on the invoice, you cannot make a claim against the supplier of the goods.

Many people who have little knowledge of accounting think that an invoice and an invoice are the same accounting document. This opinion is wrong. In fact, these documents are directly related to the creation of the same operation; the difference exists in their purpose and design.

In what cases is it necessary to draw up an act?

Typically, the process of transferring goods does not take into account the formation of an act of acceptance and transfer of goods; as a rule, a consignment note is sufficient. The delivery note represents proof of the product's shipment process.

But in isolated cases, the circumstances of the supply agreement call for the compulsory preparation of a goods acceptance and transfer certificate upon acceptance and transfer of goods from the supplier to the buyer.

In addition, there are often situations when the actual volume of the product differs from the declared one, the wrong baggage arrived, or the batch turned out to be defective. In order to demonstrate complaints to the supplier, these facts must be registered in the proper way by issuing an acceptance certificate stating absolutely all detected inconsistencies.

Some types of products (for example, equipment) are always transferred according to the act, due to the fact that this is directly required by the procedure for their acceptance: inspection, work ability testing, etc.

If the products are sent for serious storage, an act is drawn up in order to explain the place of the valuables being handed over, determine the conditions of their stay and identify the financially responsible person.

When concluding a supply contract, the parties have every opportunity to introduce into it a clause on the strict signing of an important document on acceptance of the product during its transfer to the buyer.

This action establishes the entire process of transferring the product, its detailed characteristics, high-quality and quantitative properties, and also the cost of the product.

It is worth noting that the product acceptance document is drawn up in two copies. At the same time, the two documents must not be copied, but originals. It must contain all the necessary details and information.

In the absence of the necessary details, it is possible to prove its inauthenticity. The act is considered real only if it includes all the necessary data and details.

What is the difference between an invoice and an invoice?

Typically, the invoice is issued by an accountant.

There must be a basis for this - a purchase and sale agreement or an agreement for the provision of any services. This document indicates the specific amount that the payer undertakes to transfer to a current account or pay at the cash desk of the supplier organization for a service performed or for a specific product. If the contract stipulates a reusable service (once a month for a year or once a quarter), then this invoice can be issued once a month, once a quarter, or for the whole year at once. As a rule, the invoice is not a strict reporting form and is not recorded in the sales book. Having an account is necessary mainly for prepayment.

Does it replace an invoice, a waybill TORG-12 and a transport note (TTN)?

Let's consider whether the universal transfer act replaces the consignment note (TTN) or not, which is better - UPD or TORG-12, and whether a consignment note is needed if there is a universal document.

The UPD does not replace the waybill, since it does not contain lines related to transport that are available in the second document. A bill of lading is needed to accompany the transportation of goods .

The UPD cannot replace the TTN if the contract provides for the shipment of goods to the buyer’s warehouse by road.

A consignment note in form N 1-T is issued in any case, regardless of who delivers the goods : the buyer, the seller or a hired carrier hired by any of the parties to the contract.

UPD can replace an invoice, since the main part is formed in its image and likeness and contains all the necessary data.

In addition to the mandatory invoice details listed in paragraph 5 and paragraph 6 of Article 169 of the Tax Code of the Russian Federation, the UPD contains the mandatory data of the primary accounting document, legalized by parts 2 of Article 9 of Law No. 402-FZ.

What data is included in the invoice?

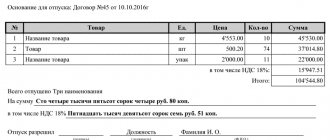

This document is a table that indicates a specific service or product name, unit of measurement, quantity and price per unit of product.

At the end the total amount is indicated. Also, the invoice must indicate the details of the service provider to whom the customer must transfer the money. The invoice is issued by the seller or contractor upon completion of the work performed or services provided. Presentation of this document is mandatory if the company is refunding VAT (the amount must be indicated in the document), i.e. is on the general taxation system. In other situations, an invoice is usually not required. If the presence of this document is mandatory, it must be executed in the same period when the transaction was made (a service was provided, confirmed by a certificate of completion, or goods were purchased, as evidenced by the presence of a delivery note).

In fact, the accountant issues both an invoice and an invoice both when providing any services and when completing a purchase and sale agreement. The only difference is the purpose of these documents. The buyer needs an invoice in order to pay for the services provided, which are specified in the contract. It is for this purpose that the invoice contains the details for transferring the required amount of money and the services or goods for which this amount will be paid.

An invoice is needed so that the transaction performed is reflected in tax accounting, i.e. VAT must be recorded on the completed service or product that is planned to be performed under the specified transaction.

As a rule, the invoice bears the seal of the service provider (mandatory), while the invoice does not. Another difference between these documents is that the invoice must be submitted to the tax office, since this document is a strict reporting form, while an invoice does not have this function.

Invoice (IF) is a document that certifies the actual shipment of goods, or the provision of services, as well as their cost. In accordance with paragraphs. 6.7 hours 2 tbsp. 9 of the Law of December 6, 2011 N 402-FZ, the Federation Council is not a primary accounting document.

Why is SF needed? An invoice is issued by sellers or performers to the buyer, or customer, after the buyer accepts the product or service.

Attention!

The only purpose of an invoice is to record value added tax. As a result, this document is a tax document and has a strictly established template.

Based on the SF, the accounting department creates a “purchase book” and a “sales book.”

Organizations conducting business under the simplified taxation system do not use them, since in such situations the second party has the right to use other documents, for example, a payment order, to account for VAT.

Was there any transportation or what is more important: a certificate of completion of work or a waybill?

PROBLEM.

The chief logistician of the enterprise Voskhod-Center LLC (Bonape brand) – hereinafter referred to as the “enterprise”, taking advantage of its position as responsible for all transportation of the enterprise’s products, having certain broad powers, taking advantage of the trust of management, organized for itself, according to the conclusions of the internal investigation at the enterprise, in addition wages, obtaining additional income. This person contributed to the registration of his elderly mother as an individual entrepreneur, indicating as the main activity the activity of road freight transport, entered into a freight forwarding service agreement with his mother on behalf of the enterprise, and took under “his wing” all the drivers and carriers who Thus, transportation services were already provided to the enterprise directly, but contracts and primary transportation documentation were handed over and executed in the logistics department. The above-mentioned contract for transport and forwarding services allowed the chief logistician to make “his own” markup on the cost of services of all driver-carriers of the enterprise, issuing a general invoice to the enterprise on behalf of his mother-entrepreneur for all transportation, taking into account a certain margin. That is, allegedly individual carriers (individuals) worked on behalf of this woman or were carriers with whom she entered into contracts. Although they worked as before and continued, not even knowing that there was someone who seemed to be controlling them. This woman did not draw up any documentation with “her carriers”; she worked insolently. Such documents were drawn up by her later in the legal proceedings. The company's management was in the dark for several years. In the spring of 2015, the new head of the enterprise’s security service discovered this “interesting scheme”, surprised by the high cost of transportation; It turned out that the company has a certain number of carriers, the cost of services of which is acceptable, but for some reason, at some point, a woman appeared who began to position herself as the “main” carrier or as the organizer of these transportations (in court, her side did not agree with this was able to decide), and the total price of transportation then increased significantly. The chief logistician of the enterprise had broad powers and completely controlled all transport movements of the enterprise, no one was interested in this area, the management trusted the logistics department, therefore, for a long time these circumstances remained secret. In this regard, after bringing the circumstances to the attention of management, it was decided not to pay for the controversial services of the mother of the chief logistician for the last period - March and April 2015, and to continue the proceedings. At the same time, the chief logistician had already resigned and, on behalf of her mother, filed a claim with the Arbitration Court of the Moscow Region against the company for the collection of an alleged debt for services provided under a freight forwarding service agreement. The amount of the claim amounted to more than 3 million rubles, which subsequently only increased. The difficulties in protecting the interests of the enterprise were that the management of the enterprise, before identifying the above facts, had already signed part of the acts of work performed during the disputed period; also, the plaintiff’s side could very convincingly, which they did, appeal to the established cooperation with the enterprise for several years, in the process in which the enterprise, without any complaints, signed certificates of completed work and paid for the services of the entrepreneur.

The main legal problem in this case for a general resolution is due to the fact that the opponent of the enterprise (the mother of the former chief logistician) did not have any documents directly recording the fact of transportation (and she did not carry them out or even organize them, she simply took money from the enterprise for invented services), such as transport or waybills, and there were only single acts of work performed, signed on both sides, the question was: does the presence of signed acts of work performed prove the fact of the transportation taking place?

SOLUTION PROCESS.

Having carried out a thorough analysis of all the intricacies of this case, I, representing the interests of the enterprise, drew up a promising legal plan that worked in the arbitration process. It should be noted that initiating a criminal case was quite problematic due to the vague interpretation of the actions of the chief logistician of the enterprise. One of the main emphasis I placed, among other things, on the established judicial practice in such disputes, according to which certificates of work performed as such do not confirm the very fact of transportation; this is confirmed by transport or invoices. This is, for example, the Resolution of the Arbitration Court of the West Siberian District dated 06/22/2015 No. F04-20363/2015 - “Billing notes are the primary accounting documents confirming the fact of transportation of goods”, Resolution of the Arbitration Court of the Moscow District dated 03/12/2015 No. F05- 983/2015, Resolution of the Arbitration Court of the Moscow District dated 08/11/2014 No. Ф05-8435/2014, Resolution of the Federal Antimonopoly Service of the Moscow District dated 05/05/2014 No. Ф05-2401/2014, Resolution of the Arbitration Court of the Far Eastern District dated 05/27/2015 No. Ф03 -1772/2015, etc. According to the norms of the legislation of the Russian Federation on transportation, a bill of lading (bill of lading or other document for cargo) is the main document indicating the existence of legal relations for transportation, and its proper completion and signing indicates the provision of services. Regardless of who the plaintiff positioned himself in the disputed legal relationship (the question arose - a forwarder or a carrier), he should have had a technical specification or technical specification, drawn up jointly with the enterprise or carrier drivers. Why were they absent? Yes, because she was not involved in transportation as such at all. The plaintiff only had certificates of work performed and explanations of the case. The work I organized allowed me to collect and present the following evidence to the court:

— waybills, which included the shipper (enterprise), consignee (enterprise client), direct driver-carrier of the cargo,

— route sheets that included the company and the direct driver-carrier,

- waybills, in which the shipper (company), consignee (company client) appeared, and in the column provided for this, the direct driver-carrier was also listed,

- testimony of some delivery drivers who have never seen or known the entrepreneur - the mother of the chief logistician of the enterprise, and always thought that they were collaborating directly with the enterprise, and their services were paid for by a person authorized by the enterprise,

- written explanations that made it clear to the court of first instance that the plaintiff did not fulfill and cannot confirm the fulfillment of any of the conditions of the contract of transport and forwarding services concluded with the enterprise, the plaintiff did not carry out transportation during the disputed period, and also did not organize such.

The totality of evidence, the masterly use of the plaintiff’s “weaknesses,” and the necessary motions filed in a timely manner—all this allowed the trial court to achieve an almost 100% result. The plaintiff’s claim was denied in full, but the only thing was that the defendant was also denied a counterclaim related to the premature payment of a small part of the plaintiff’s services during the disputed period. This conclusion of the court is quite controversial, to put it mildly, since the refusal to satisfy the claim automatically should have led to the satisfaction of the counterclaim, based on the essence of this dispute.

Subsequently, the proceedings moved to the appellate instance, where the panel of judges made a radically different conclusion on the circumstances of the case, grossly violating the norms of the Arbitration Procedure Code of the Russian Federation - they accepted additional evidence from the plaintiff, and even in copies. Such evidence, firstly, was not presented or mentioned in the first instance; in the second instance, explanations of the impossibility of presenting such evidence were not previously made; and secondly, the originals of these documents never appeared on appeal. And thus, including on the basis of this additional evidence, I am sure, concocted by the plaintiff at the last moment, the appeal ruling satisfied the interests of the plaintiff in terms of collecting the debt for transportation services (the decision of the first instance was canceled in part), but only according to the signed acts of execution works, the rest of the claim was rejected, and the defendant’s counterclaim, accordingly, also remained unsatisfied. How this could happen, with such a gross violation of procedural law, is an open question. The conclusions of the appellate court, in my opinion, of course, contradict the legal doctrine and judicial practice on the topic of documentary evidence of actual transportation.

The dispute reached the third instance, but the cassation, in my opinion, approached the consideration of the dispute formally and left the appeal verdict unchanged.

RESULT.

Despite the partial reversal of the decision of the Arbitration Court of the Moscow Region by the Tenth Arbitration Court of Appeal and the satisfaction of part of the plaintiff’s demands, the enterprise still remained in a winning position, since transportation of products during the disputed period was carried out in the required volume, but was not fully paid for - at the prices of the pseudo-carrier, and in a rather impressive amount, which was not received by the former chief logistics officer of the enterprise, represented by her mother-entrepreneur, who was counting on this. That is, they still saved some money for the enterprise. This victory is even more valuable because at the very last moment, when the company wanted to make a decision on agreeing to the demands or concluding a settlement agreement with the plaintiff on negative terms, the management’s opinion was changed based on my analytics.

The widespread legal conclusion, supported by the majority of courts, about confirmation of the fact of transportation only on the basis of a bill of lading or a similar document, and not an act of work performed, in our opinion, should always be relevant and continue to build uniformity of judicial practice on such disputes in order to optimize legal proceedings and to avoid miscarriages of justice.

Case No. A41-51135/2015 in AS MO.

Sharing

Can an invoice and a delivery note be issued for the same product? SF and TN not only can, but also must be issued for the same product.

Since, as we have already discussed above, this documentation performs different functions in accounting: the invoice reflects VAT, and delivery notes for the transfer of goods (you can find out who should sign the columns “received the goods”, “received the goods” and others) .

Do the numbers for one product have to match?

There are no requirements under the Tax Code, as well as other regulations stating that the SF and TN numbers must match. The main thing is to ensure that the VAT amounts coincide in both cases. Each organization has the right to choose the order and type of numbering of its documents independently.

Which document should be drawn up first?

Can SF be discharged before TN? Since the SF confirms the VAT on the transferred goods, it cannot be written out in advance to the TN,

except in cases where the transaction agreement provides for prepayment. The invoice must be issued no later than five days after shipment of the goods.

Is it possible to combine them?

In 2013, the Federal Tax Service introduced the UTD form into circulation - a universal transfer document that contains elements of tax and accounting. It is based on the invoice base, the rest is an element of the delivery note.

Is registration with different dates acceptable?

The invoice may have different dates from the delivery note.

But you need to consider:

- The SF must be issued no later than five days after shipment of the goods, that is, TN.

- If one of the five days is a weekend, then the required date is postponed to the next working day.

There is no liability for violating this five-day deadline, however, the Ministry of Finance indicates that the buyer cannot claim a deduction for late documents.

Invoices and delivery notes are important documents, control over the completion and storage of which must not be overlooked in order to protect yourself from further problems and misunderstandings with counterparties or inspection authorities. And the choice of the form of the consignment note or the use of the opportunity to work with a universal transfer document, first of all, remains with the entrepreneur himself.

Federal Law 402-FZ “On Accounting” describes all accounting and primary documents. They are needed mainly for tax purposes - as documents that confirm the expenses you have incurred and the correctness of determining the tax base.

Primary documents must be stored for 4 years. During this time, the tax office may request them at any time to check you or your counterparties. “Primary” is also used in litigation in disputes with counterparties.

Primary accounting documents are drawn up at the time of business transactions and indicate their completion. The list of documents accompanying a particular transaction may vary depending on the type of transaction. The preparation of all necessary primary documents is usually carried out by the supplier. Particular attention should be paid to those documents that arise during transactions where you are the buyer, because these are your expenses, and therefore you are more interested in complying with the letter of the law than your supplier.

Required details

A standard document for acceptance and transfer of a product or product must include established essential details, without which, in the event of disagreement between the parties, it will be considered invalid.

This act must include the following essential details, and in particular:

- Title of the document;

- the current date and place of its composition;

- detailed information about the persons receiving the goods - the seller, the buyer or trusted persons. This is primarily the first name, last name, passport information, identification code number, citizenship, contact telephone numbers, residential addresses;

- act number;

- a clear representation of the numerical data of the transferred product, and the actual assortment and number;

- indication of the quality data of the product;

- presentation of absolutely all detected defects of the product (if there are no defects, it should be noted that there are no defects);

- probable complaints of the two parties to the agreement that arose during the acceptance and transfer of the product are indicated;

- signatures of both parties;

- seals of the institutions that transferred and received the product;

In addition to the integral data that must be enshrined in the product acceptance certificate, there may also be other auxiliary details noted at the request of the parties.

At certain points, it makes sense to indicate by what method and in what period the payment for the goods was made - before or after the practical transfer of the product.

Also, if the contract takes into account not a one-time, but a long-term supply of goods, an independent document is drawn up.

In addition, counterparties are required to streamline the issue regarding whether it is enough to draw up an acceptance certificate for a single product item, or for a specific batch of product.

the acceptance certificate for goods can be found here (Word, .doc format)

Requirements for filling out in accordance with Article 9 of the Federal Law on Accounting

Article 9 of the Federal Law “On Accounting” states that all business procedures, including monetary procedures, must be documented in the main papers on the basis of which accounting is carried out in the company.

This kind of act must be collected during the procedure or immediately after its completion.

The document that proves the implementation of currency transactions must be drawn up exactly in accordance with the law and be signed by the manager of the organization, the main accountant or an authorized person.

Primary accounting papers must be drawn up in the appropriate form and have the following details:

- Title of the document;

- formation period;

- name of the institution;

- natural and currency expression of a business transaction;

- information about officials;

- signatures of persons;

Separation of primary documents by business stages

All transactions can be divided into 3 stages:

Stage 1. You agree on the terms of the deal

The result will be:

- contract;

- an invoice for payment.

Stage 2. Payment for the transaction occurs

Confirm payment:

- an extract from the current account, if the payment was made by bank transfer, or by acquiring, or through payment systems where money is transferred from your current account;

- cash receipts, receipts for cash receipt orders, strict reporting forms - if payment was made in cash. In most cases, this payment method is used by your employees when they take money on account. Settlements between organizations are rarely in the form of cash.

Stage 3. Receipt of goods or services

It is imperative to confirm that the goods have actually been received and the service has been provided. Without this, the tax office will not allow you to reduce the tax on money spent. Confirm receipt:

- waybill - for goods;

- sales receipt - usually issued in conjunction with a cash receipt, or if the product is sold by an individual entrepreneur;

- certificate of work performed/services rendered.

Mandatory primary documents

Despite the variability of transactions, there is a list of mandatory documents that are drawn up for any type of transaction:

- contract;

- check;

- strict reporting forms, cash register, sales receipt;

- invoice;

- certificate of work performed (services rendered).

Agreement

When carrying out a transaction, an agreement is concluded with the client, which specifies all the details of the upcoming business transactions: payment procedures, shipment of goods, deadlines for completing work or conditions for the provision of services.

The contract regulates the rights and obligations of the parties. Ideally, each transaction should be accompanied by a separate contract for the supply of goods or services. However, with long-term cooperation and the implementation of similar operations, one general agreement can be concluded. The agreement is drawn up in two copies with stamps and signatures of each party.

Some transactions do not require a written contract. For example, a sales contract is concluded from the moment the buyer receives a cash or sales receipt.

An invoice for payment

An invoice is an agreement under which a supplier fixes the price of its goods or services.

The buyer accepts the terms of the agreement by making the appropriate payment. The form of the invoice for payment is not strictly regulated, so each company has the right to develop its own form of this document. In the invoice, you can specify the terms of the transaction: terms, notification of advance payment, payment and delivery procedures, etc.

In accordance with Article 9-FZ “On Accounting”, the signature of the director or chief accountant and seal are not required for this document. But they should not be neglected in order to avoid questions from counterparties and the state. The invoice does not allow you to make demands on the supplier - it only fixes the price of the product or service. At the same time, the buyer retains the right to demand a refund in the event of unjust enrichment of the supplier.

Payment documents: cash receipts, strict reporting forms (SSR)

This group of primary documents allows you to confirm the fact of payment for the purchased goods or services.

Payment documents include sales and cash receipts, financial statements, payment requests and orders. The buyer can receive the order from the bank by paying by bank transfer. The buyer receives a cash or goods receipt from the supplier when paying in cash.

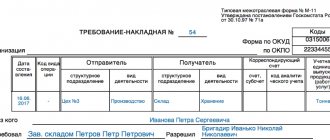

Bill of lading or sales receipt

Sales receipts, as we said above, are issued when selling goods to individuals or by the individuals themselves.

Invoices are used primarily by legal entities to register the release/sale of goods or inventory items and their further receipt by the client.

The invoice must be prepared in two copies. The first remains with the supplier as a document confirming the fact of transfer of goods, and the second copy is transferred to the buyer.

The data on the invoice must match the numbers on the invoice.

The authorized person responsible for the release of goods must put his signature and the organization’s seal on the invoice. The party receiving the goods is also obliged to sign and certify it with a seal on the delivery note. The use of a facsimile signature is permitted, but this must be recorded in the contract.

Certificate of services rendered (work performed)

is a two-sided primary document that confirms the fact of a transaction, the cost and timing of services or work.

The act is issued by the contractor to his client based on the results of the provision of services or work performed. This primary document confirms the compliance of the services provided (work performed) with the terms of the concluded contract.

Primary documents ► agreement, invoice, invoice, invoice, act - Elba

The primary document confirms various events in the business: the sale or purchase of goods, the provision of services to clients, the payment of salaries to employees, and others.

Depending on the event, the list of documents to be completed varies. Let's consider a common situation - a transaction involving the sale of goods and the provision of services. It is customary that the documents are prepared by the supplier or contractor.

Article “How people cheat in contracts”

- The contract is the beginning of the transaction. In it, you and the client determine the terms of cooperation: what, for what price and in what time frame you do. If the client is a regular one, you can draw up one agreement for several transactions.

- The invoice contains the amount to be paid, a list of goods and services and the bank details of the seller. This is an optional document, but is usually used for convenience.

- A cash receipt, sales receipt or strict reporting form confirms payment. Give them to the client who pays in cash or by card. When paying by bank transfer, payment is confirmed by the payment order.

- Invoice is a document that the supplier issues to the buyer when shipping goods.

- An act of provision of services or completed work is a document that the customer and the contractor sign based on the results of the provision of services or completion of work.

- Invoice - usually issued by individual entrepreneurs and LLCs using the general taxation system, because they work with VAT. In rare cases, invoices are issued using the simplified tax system, UTII and patent - read more about this in the article.

Elba will take over the accounting. The service will prepare reports and send them via the Internet. It will calculate taxes, reduce it by contributions - and you will receive ready-made payments for payment.

Agreement

Describes the rights and obligations of the parties to the transaction. Typically, a contract contains the following sections:

- Subject of the agreement: what is the result of the transaction.

- Contract amount and payment procedure: when and how much to pay.

- Rights and obligations of the parties: how the work happens.

- Responsibility of the parties: what happens if you or your partner violate the deadlines.

- The procedure for changing and terminating a contract: how to terminate a contract or accept additional agreements to it.

- Details of the parties: what are your and your partner’s current accounts, INN, OGRN and addresses.

The agreement is usually drawn up in 2 copies and contains the signatures of each party.

If you use a standard contract form with clients and replace the necessary details in Word or Excel, use templates in Elba. Upload your agreement template, and Elba will automatically fill in the details of the counterparty from the directory.

For some transactions, a written contract is not necessary at all. For example, a purchase and sale agreement is considered concluded from the moment a cash receipt, sales receipt or other document is issued to the buyer, which confirms the fact of payment. This does not mean that during a retail purchase and sale it is impossible to conclude an agreement in writing - the law does not prohibit this.

Templates of common agreements:

Service agreement template

Contract agreement template

Supply agreement template

Check

An optional document in which the seller indicates the price, quantity of goods and details for transferring payment.

You can come up with an invoice form for payment yourself or find a ready-made one on the Internet. An invoice can replace a contract if all essential terms of the transaction are included in it.

Invoice template

Elba has a ready-made invoice template. Select the counterparty, indicate the goods or services, their quantity, and the document is ready.

Payment documents

Confirms payment for goods or services. This can be a payment order, a payment request, cash and sales receipts, a strict reporting form.

When you receive payment through a bank by bank transfer, you do not need to issue a payment document. The client retains the payment order . With this document he can confirm that he transferred the funds using your details.

When paying by cash, card or electronic means of payment, you must provide the buyer with a cash receipt, sales receipt or strict reporting form. What you choose depends on the tax system and what you do.

The cash receipt is printed using cash register equipment. It is required to be used by everyone who accepts payment in cash, by card, or by electronic means of payment. Exceptions are listed in paragraph 2 of Article 2 of Law 54-FZ. There is a deferment for entrepreneurs on UTII and patents, and for now they can work without a cash register. Read more in the article “How to use cash register equipment.”

A sales receipt is issued by individual entrepreneurs and LLCs on UTII and patent at the request of the buyer. It replaces a cash receipt, but only until July 1, 2021, and for catering and retail with employees - until July 1, 2018. Then you will need a cash register.

The form of the sales receipt has not been established, so you can develop your own with the required details: name of the document, number, date, name of the LLC or full name of the individual entrepreneur, INN, goods and services, amount of payment and signature with transcript and position.

A strict reporting form is issued by those who provide services to individuals. It replaces a cash receipt, but only until July 1, 2021, and for catering with employees - until July 1, 2021. Forms must be printed at a printing house or through a special service. You can't just print them out on a printer at home. Read more about BSO in the article.

Consignment note (N TORG-12)

Registers the sale of goods to another individual entrepreneur or LLC. It is usually not used for working with individuals.

The invoice is issued in two copies: the first remains with the supplier and records the shipment of goods, and the second is transferred to the buyer and is needed by him to accept the goods.

Usually the invoice is drawn up according to the standard TORG-12 form. But you can use your own template.

Invoice template

In Elba you can create an invoice based on an invoice.

The act of providing services

Signed by the contractor and the customer. The certificate confirms that the services have been provided or the work has been completed, and the customer has no complaints about their quality.

Act template

Draw up a deed in Elba: just select the counterparty and indicate the service, and then send the completed document to the counterparty with a signature and seal.

Invoice

This document is required to be issued only by organizations and entrepreneurs that are VAT payers - mainly those who work on the general taxation system.

https://www.youtube.com/watch?v=kVlA0A3itWc

Organizations and individual entrepreneurs on the simplified tax system, UTII and patent usually do not pay VAT and therefore are not required to issue invoices. There are a few exceptions, which we covered in a separate article.

The invoice is issued in duplicate and signed by the supplier of the product or service. One copy is given to the buyer, the other remains with the seller. An invoice must be issued no later than 5 days after shipment of goods or provision of services.

An invoice is the basis for deducting VAT, so all organizations treat it with special trepidation.

In order not to study the form and rules for issuing an invoice, use Elba.

The article is current as of 03/11/2019

Source: https://e-kontur.ru/enquiry/129