The role of the journal

The main task of the journal is to put in order the movement of primary expenditure and receipt documents, so they must be registered immediately after creation. And only then can they be transferred to the cashier for further work (exceptions are orders for receiving wages, which are drawn up for one day, but cannot always be implemented in a timely manner).

In addition, the presence of a journal allows the management of the enterprise to avoid situations related to the unlawful use of payment documents. For this purpose, at the end of each working day, the company’s accountant must reconcile all entries made in the journal with the available stubs of “receipts” and “consumables”.

Also, a correctly completed journal in cases of tax audits allows you to quickly control the balance in the cash register (here it would be useful to remind you that when using the cash register, you should strictly adhere to the maximum allowable cash limit).

Why do you need a logbook for registration of PKO and RKO

The existing regulation on cash circulation (Law No. 86-FZ dated July 10, 2002) provides uniform rules that are mandatory for both organizations and banks.

According to Art. 34 of this law, the Bank of Russia establishes the procedure for conducting cash transactions by firms that must have a cash desk for receiving and issuing cash. Unused funds should be kept in a bank. When paying in cash for goods and services, the organization receiving the money must use a cash register to record the amount received. At the same time, a cash receipt order (PKO, form KO-1) is drawn up. If the amount received exceeds the cash balance limit, then the excess must be deposited at the bank. To do this, issue a cash receipt order (RKO, form KO-2). PKOs are also issued upon receipt of funds from the bank for the payment of salaries, accountable amounts, and travel expenses. RKOs are issued when money is issued for these purposes to specific employees of the company.

The procedure for conducting cash transactions is stipulated in the instruction of the Central Bank of the Russian Federation dated 03/11/14 No. 3210-U, which came into force on 06/01/2014. According to this instruction, all transactions for issuing or receiving money are recorded in primary documents (PKO and RKO), after which they must be reflected in the registration journal (form KO-3). All these forms are approved by the State Statistics Committee (Resolution No. 88 dated August 18, 1998).

The requirements for primary documents can be found in the article “Primary document: requirements for the form and the consequences of its violation.”

If you have access to ConsultantPlus, check whether you are filling out the PKO and RKO registration log correctly. If you don't have access, get a free trial of online legal access.

What documents must be recorded in the journal

The journal for registering incoming and outgoing cash documents must contain:

- all documents indicating the receipt and expenditure of funds, regardless of what sources they came from or for what purposes they were spent;

- information about payroll statements accompanying the issuance of wages to employees of the enterprise (but only after the payment procedure has been completed);

- invoices for payment;

- applications for receiving funds, etc.

Account cash warrant

An expense cash order, or RKO, is largely formed according to the same rules as the PKO. In 1C there are the following types of cash registers:

- Payment to the supplier

- Return to buyer

- Issuance to an accountable person

- Payment of wages according to statements

- Payment of wages to an employee

- Payment to an employee under a contract

- Cash deposit to the bank

- Repayment of the loan to the counterparty

- Repayment of loan to the bank

- Issuing a loan to a counterparty

- Collection

- Payment of deposited wages

- Issuing a loan to an employee

- Other expenses

For payments No. 4-5, pay slips should be prepared in advance, even if the payment is made to one employee.

Figure 11. RKO document options

We will issue a settlement settlement for the issuance of funds to an accountable person.

Figure 12. Completed cash register document

After posting the document, you can view the postings.

Figure 13. Postings by cash register

Let's consider the procedure for making wage payments in 1C. We will create a payroll. If all employees received a salary according to it, you can use the “Pay Statement” button (at the bottom of the form), and a settlement settlement will be automatically generated.

Figure 14. Options for cash documents based on payroll

Let’s simulate a situation where one employee’s salary is deposited and the rest are paid. In the paper version of the statement, the corresponding mark is placed on the deposited amounts. In 1C, when accounting for cash transactions, you should open the statement and use the Create based button, then Salary Deposit. For the deposition document, we leave the names we need.

Figure 15. Document Salary Deposit

After completing the document, we look at the postings.

Figure 16. Postings when depositing salaries

We return to the statement and click on the Create button on the basis of which the Cash Issue document . The amount will be recalculated automatically and will be reduced by the deposited amounts.

Figure 17. Document Cash issuance based on payroll

Postings for issuing salaries were generated for two employees, and that’s how it should be.

Figure 18. Postings for the document Cash withdrawal

Deposited amounts can only be kept in the cash desk if they do not exceed the cash storage limit. Otherwise, they should be handed over to the bank. We form a cash settlement cash deposit to the bank.

Figure 19. Filling out the document Cash deposit to the bank

The result of the document.

Figure 20. Postings according to the document Cash deposit to the bank

If you still have questions about working with orders, please contact our support, maintenance and modification service for 1C programs by leaving a request on the website or by phone.

Is it possible to do without a logbook?

By law, companies working with cash register equipment are required to maintain cash discipline. One of its basic rules states that all documents must be registered in a special journal. Moreover, if an organization violates this norm, in the event of a tax audit it faces administrative punishment in the form of a large fine (in this case, both the legal entity itself and its director are subject to punishment).

I was in a hurry and got fined

The issuance of accountable money was formalized by an expenditure cash order (clause 6 of instruction No. 3210-U). Since the contractor's office was located in the same building, the transaction of payment for the car did not take much time for both parties.

However, the joy of both companies was short-lived - the tax inspector who came on the same day fined both companies under clause 1 of Art. 15.1 of the Code of Administrative Offenses of the Russian Federation for cash payments with other companies in excess of the established limit.

Important! Currently, there is a restriction on cash payments between merchants: no more than 100,000 rubles. under one agreement (clause 6 of the Bank of Russia Directive dated October 7, 2013 No. 3073-U “On cash payments”). For more information about who checks cash discipline and what fines may be imposed, see the material “Are your cash discipline in order?”

Both companies were fined because they were liable for exceeding the limit of 100,000 rubles. provided for in Art. 15.1 Code of Administrative Offenses for participants in cash payments, which are both the seller and the buyer.

If companies were not in a hurry to pay in cash and had studied the legislative framework in advance, unforeseen penalties in the amount of 50,000 rubles would have been incurred. for each company and 5,000 rubles. – for their leaders could have been avoided. If the inspector came with an inspection 2 months later, there would be no fine, since a 2-month statute of limitations is established for such a violation (clause 1 of Article 4.5 of the Administrative Code).

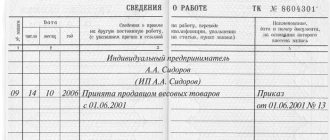

Rules for compiling a journal for registering incoming and outgoing cash documents

Today, there are several ways to keep a journal, since there is no single unified sample that is mandatory for use. Enterprises can maintain a document in any form or according to a template developed and approved in the company’s accounting policy, or use a previously generally applicable form. In this case, the log must contain a number of mandatory information:

- name of the enterprise and structural unit whose property is the document;

- organization code according to OKPO (All-Russian Classifier of Enterprises and Organizations);

- year or other period for which it is maintained;

- personal data of the employee directly related to its filling: his position, full name.

Basic information is presented in the form of a table into which data on all cash documents is entered in chronological order: on the left side about receipts, on the right side about expenses. For each of them, the following are entered in the corresponding cells:

- date of,

- number (according to the company’s internal document flow),

- the amount that passes through it

- note.

All lines are required to be filled out, including a note - it provides an explanation for a particular payment document.

Receipt cash order sample filling

Let's look at an example of filling out the PKO.

Main part

Filling out the document must begin by recording the company name or full name. entrepreneur. Also, in a separate field you need to enter the OKPO code that was assigned to the organization by Rosstat. If there is no such code, then you can put a dash in the column.

If the parishioner was registered in a separate structural unit, his name must be indicated in the next field. If division into departments is not used, then a dash should be placed here.

Next, the form contains the title of the document. After it you need to indicate its serial number and date of registration. The date is entered into the document in the format DD.MM.YYYY.

Then the document contains a table that displays accounting data - debit and credit accounts, analytical accounting. Then there is a column in which you need to write off the amount of the document in numbers.

The last column contains the target funding code. Information is entered into it if such encoding is accepted at this enterprise.

In the “Accepted from” field, information about who hands over the money to the cash register is recorded. This is indicated in the genitive case. If the person or employee is handing over, you must enter your full name here.

Sometimes a situation arises that he, the person of the company, makes payments to its employees. Then it is best to first indicate the name of the company, and then after the word “through” - full name. this employee. For example, “LLC Slavia through Gennady Fedorovich Ivantsev.”

In the “Base” field, the reason why the money is handed over to the cashier is written down. The name of a specific product, service, return of a report or salary, etc. may be indicated here.

You might be interested in:

Advance report: what can be taken into account, sample filling, main transactions

The “Amount” field duplicates the received amount of money previously indicated in numbers. Only this time it needs to be described in words. Kopecks, if any, are written in numbers.

If a company accepts payment for goods and services with VAT included, then the amount of tax in the amount received is indicated after the words “Including VAT...”.

Attention! If the company operates without VAT (exempt or uses a preferential regime), then here you need to write “Without VAT” or “VAT not subject to.”

In the “Attachment” field, you can write down the names of the documents that accompany the delivery of money to the cashier. This could be a shift closing report, an order, a statement, etc. If there are no such documents, then the field is simply crossed out.

After drawing up the document, it must be checked and signed by the chief accountant, and then the cashier himself must sign.

Receipt for cash receipt order sample filling

The information entered on the receipt must completely duplicate the data from the main part of the receipt.

The company name is written at the top. Next, in the “To the receipt order” field, the document number and the date on which it was drawn up are indicated.

The “Accepted from” and “Bases” fields duplicate information that was entered in similar fields in the main part of the form.

Then the amount of funds accepted according to the document is entered. This must be done first in numbers and then in written words.

If the accepted funds include tax, then in the “Including” field you must write down its amount. If there is no tax, then it is written here with a phrase, for example, “Without VAT tax.”

At the very end there is a place where you need to indicate the date of the transaction.

The cash receipt order is certified by the chief accountant, who checks the correctness of the document. After this, the cashier himself signs it.

Magazine design rules

The journal can be maintained both electronically and in paper form. Moreover, if it is carried out “live” at the enterprise, then all its pages must be numbered, fastened with a special strong thread and certified with a signature. It is not necessary to endorse the journal with a stamp, because it relates to the company’s internal document flow; moreover, starting from 2021, legal entities are legally exempt from the requirement to use stamps and seals in their work.

During the maintenance period, the journal must be kept in a certain place, access to which must be strictly limited. After losing its relevance, it should be transferred for storage to the archive of the enterprise, where it should be kept for the period established by law.