How non-profit organizations account for fixed assets

The conditions under which non-profit organizations accept fixed assets for accounting differ from the rules for commercial structures. Here are the criteria for a fixed asset for non-profit organizations:

- period of use of the object – more than 12 months;

- the organization does not plan to sell the property;

- the object is intended for the statutory, entrepreneurial activities of the organization or for its management needs.

Such conditions are written in paragraph 4 of PBU 6/01.

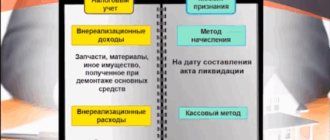

If an NPO has acquired or received free of charge (as a gift) an object that is intended for transfer to third parties, it is not included as a fixed asset. These assets are taken into account as part of materials.

Accounting entries for the receipt of fixed assets will vary depending on how they were received: for a fee or free of charge.

Reporting of non-profit organizations

The composition of the reporting forms differs depending on the types of activities of the NPO. The differences are shown in the table.

| Activity | Reports | Frequency of delivery |

| a commercial | balance sheet how to fill out form 1; profit and loss how to fill out form 2; changes in capital (form 3); movement of money (f. 4); how to fill out form 4 appendix to the balance sheet (form 5); intended use of funds (form 6); explanatory note. | Quarterly |

| Non-profit | Forms No. 1, 2, 6. | Once a year |

What postings should be used to reflect fixed assets for a fee?

Purchased fixed assets are reflected in the accounting of non-profit organizations depending on the funds with which they were acquired and for what activity. There can be two sources: income from business activities or targeted income. Postings for each individual case are in the tables below.

Fixed assets came from income from business activities subject to VAT

| Contents of operation | Debit | Credit | Sum | Primary document |

| Paid for a computer | 60 | 51 | 48 380 | payment order, bank statement |

| Received a computer | 08 | 60 | 41 000 | invoice |

| The amount of VAT paid to the supplier is reflected | 19-1 | 60 | 7380 | invoice |

| Accepted for VAT crediting on activities subject to VAT | 68 | 19-1 | 7380 | invoice, bank statement |

| The computer is accepted for accounting as an object of fixed assets | 01 | 08 | 41 000 | act of acceptance and transfer of fixed assets |

Fixed assets came from income from business activities, which are not subject to VAT

| Contents of operation | Debit | Credit | Sum | Primary document |

| Paid for a computer | 60 | 51 | 48 380 | payment order, bank statement |

| Received a computer | 08 | 60 | 41 000 | invoice |

| The amount of VAT paid to the supplier is reflected | 19-1 | 60 | 7380 | invoice |

| VAT is included in the price of the property, which will be used in income-generating activities exempt from VAT | 68 | 19-1 | 7380 | invoice, bank statement |

| The computer is accepted for accounting as an object of fixed assets | 01 | 08 | 41 000 | act of acceptance and transfer of fixed assets |

Fixed assets purchased using targeted proceeds*

| Contents of operation | Debit | Credit | Sum | Primary document |

| Paid for fixed asset | 60-2 | 51 | 41 300 | payment order, bank statement |

| Computers received | 08 | 60-1 | 41 300 | waybill, invoice |

| Advance paid to supplier credited | 60-1 | 60-2 | 41 300 | check |

| The computer is accepted for accounting as an object of fixed assets | 01 | 08 | 41 300 | act of acceptance and transfer of fixed assets |

| The source of financing for the purchased OS is reflected | 86-1, etc. | 83-1 | 41 300 | accounting certificate, estimate of income and expenses |

* A peculiarity of accounting for fixed assets that were received through targeted financing is that it is necessary to use account 83. The Russian Ministry of Finance recommends that the balances on it be reflected in the balance sheet in the line “Real estate and especially valuable movable property fund.”

Such recommendations are given by the Ministry of Finance of Russia in paragraph 15 of information PZ-1/2015, in letters dated February 19, 2004 No. 16-00-14/40, dated February 4, 2005 No. 03-06-01-04/83.

Features of accounting in non-profit organizations

Non-profit organizations (NPOs) maintain accounting and prepare reports in accordance with the legislation of the Russian Federation. To maintain it, management is obliged to introduce the position of an accountant or draw up an agreement for the relevant services with another company.

Operations related to the activities prescribed in the Charter and entrepreneurship are carried out separately. Income and cost accounts are presented in the table. (click to expand)

| Activity | Check |

| Non-profit | 86 “Targeted financing” |

| Entrepreneurial major | 90 "Sales" |

| Other entrepreneurial | 91 “Other income and expenses” |

Dt 90 Kt 99 - reflects the profit received at the end of the reporting period.

https://www.youtube.com/watch?v=ytpolicyandsafetyru

Dt 99 Kt 84 - net profit for the year is taken into account;

Dt 84 Kt 86 - financing of statutory work.

Dt 99 Kt 90 - loss for the period (month) is taken into account;

Dt 84 Kt 99 - annual loss is reflected.

Dt 76 Kt 84 - the loss is repaid through membership fees;

Dt 86 Kt 84 - due to last year’s profit;

Dt 82 Kt 84 - from the reserve fund.

NPO "Barrier" provides services for a fee. For 2016, income amounted to 614 thousand rubles, expenses - 389 thousand rubles.

Dt 62 Kt 90,614,000 - revenue from business is taken into account;

Dt 90 Kt 20,389,000 - the cost of services has been written off;

Dt 90 Kt 99,225,000 - the result of the association’s work is taken into account.

Dt 99 Kt 84,225,000 - profit written off;

Dt 84 Kt 86,225,000 - annual profit added to target amounts.

An NPO can take property into account as fixed assets if the following conditions are met:

- Application in the work established by the Charter, for the needs of management or entrepreneurship;

- Application for a period exceeding one year;

- Donation or transfer of ownership to other persons is not provided for.

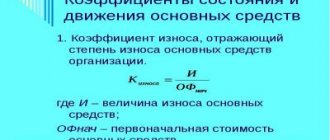

For fixed assets, NPOs charge depreciation instead of depreciation, like commercial companies. The data obtained is used when calculating property tax based on the annual average value of fixed assets (Article 375 of the Tax Code of the Russian Federation).

The amount of depreciation is shown on the off-balance sheet account, and fixed assets are shown on the balance sheet at their original cost. Otherwise, the asset will not be equal to the liability. A feature of the accounting of fixed assets received from earmarked funds is the use of accounts. 83. In the balance sheet, its balances are reflected in the line “Real estate and movable property fund”.

| ★ Best-selling book “Accounting from Scratch” for dummies (understand how to do accounting in 72 hours) purchased by {amp}gt; 8000 books |

What postings are made when receiving fixed assets free of charge?

Fixed assets that come to non-profit organizations free of charge are taken into account at their current market value. The postings to capitalize such a fixed asset are in the table below.

| Contents of operation | Debit | Credit | Sum | Primary document |

| The obligation under the donation agreement, payment of the membership fee, etc. is reflected. | 76 | 86 | 45 000 | donation agreement, etc. |

| The market value of the object is reflected | 08 | 76 | 45 000 | Act |

| Costs for delivery, assembly, installation are reflected | 08 | 76 | 1500 | contracts, acts, accounts, etc. |

| Included in fixed assets | 01 | 08 | 46 500 | act of acceptance and transfer of fixed assets |

| The source of financing for the purchased OS is reflected | 86-1, etc. | 83-1 | 46 500 | accounting certificate, estimate of income and expenses |

Where in the balance sheet and its explanations do non-profit organizations reflect fixed assets?

In the Balance Sheet, the value of fixed assets of non-profit organizations is reflected in section 1 in the line “Fixed Assets”. This must be done at the full original cost. Do not reduce it by the amount of wear.

In the explanations to the Balance Sheet, the value of fixed assets of non-profit organizations is reflected in Section 2 “Fixed Assets”, Table 2.1 “Availability and Movement of Fixed Assets”. However, in this NPO table, the columns “Accumulated depreciation” and “Accrued depreciation” are renamed “Accumulated depreciation” and “Accrued depreciation”, respectively. That is, unlike the balance sheet, the table shows both the full original cost and accrued depreciation.

This is stated in Note 6 to Appendix 3 to Order No. 66n of the Ministry of Finance of Russia dated July 2, 2010.

How to write off fixed assets

The Russian Ministry of Finance recommends writing off fixed assets that can no longer be used in the accounting of non-profit organizations as follows. Reduce the indicators for the groups of articles “Fixed assets” and “Fund of real estate and especially valuable movable property”. At the same time, reduce the amount of wear and tear.

| Contents of operation | Debit | Credit | Sum | Primary document |

| Fixed assets purchased using targeted proceeds or received free of charge have been written off | 83 | 01 | 45 000 | Accounting information |

| Depreciation written off | – | 010 | 45 000 | Accounting information |

This procedure is prescribed in paragraph 6 of the information of the Ministry of Finance of Russia PZ-1/2015.

JUSTIFICATION

This issue was discussed in the professional community and, in particular, at meetings of the industry committee on non-profit organizations of the BMC. Preservation of the NOCDI Fund allows non-profit organizations to generate more informative reporting on the use of targeted funds. Taking into account the specific reporting requirements of non-commercial organizations, as well as the significantly different (compared to commercial organizations) audience of reporting users, it seems advisable to largely preserve the procedure for accounting for fixed assets in non-commercial organizations, which was formed as part of the application of PBU 6/01 (2001 - 2021) in terms of , which does not contradict the FSBU OS.

We invite you to familiarize yourself with: What account is corporate property tax accounted for?

The current regulatory and legal acts in the field of accounting, in particular, Order of the Ministry of Finance of the Russian Federation dated July 2, 2010 No. 66n, letters of the Ministry of Finance of Russia (including summarizing the practice of applying legislation - “PZ”) regarding the formation and write-off of the NOCDI Fund are not contradict the FSBU OS and are applicable taking into account the above recommendations.

EXAMPLES

Example 1. As of 01/01/2018 (date of commencement of application of the Federal Accounting Standards of Ukraine), the non-profit organization has a fixed asset on its balance sheet with an initial cost of 100,000 rubles. Expected period of OS use: 4 years. The depreciation accumulated behind the balance sheet is RUB 25,000. The NOCD fund is accounted for in account 83.

Balance sheet indicators of non-commercial organizations as of December 31, 2017 (before the application of the Federal Budgetary Accounting Standards)

| |

| Fixed assets | 100,000 rub. |

| III. Special-purpose financing | |

| Fund of real estate and especially valuable movable property | 100,000 rub. |

Dt 010 Depreciation (behind balance sheet) 25,000 rub.

| Dt. 83 Kt 02 | 25,000 rub. | recognition of accumulated depreciation as depreciation to reduce the NOCDI Fund |

| Dt 010 | — 25,000 rub. | Reversal (write-off) of previously accrued depreciation taken into account on the balance sheet |

| |

| Fixed assets | 75,000 rub. |

| III. Special-purpose financing | |

| Fund of real estate and especially valuable movable property | 75,000 rub. |

010 Depreciation (behind balance) 0 rub.

Example 2 (continuation of example 1). During 2021, a new fixed asset was recognized with a cost of 50,000 rubles. Expected period of use is 5 years.

| Dt 01 Kt 08 | 50,000 rub. | OS recognition |

| Dt. 26[2] Kt 83 | 50,000 rub. | Formation of the NOCDI Fund |

| Dt 86.1 Kt 262 | 50,000 rub. | Accounting record of the closing of the month with the expense of the entire cost of the fixed asset included in the expenses of the period |

Example 3 (continuation of examples 1-2). For 2021, annual depreciation was accrued at a time for a fixed asset recognized (put into operation) before the start of application of the Federal Budgetary Accounting Standards (FSBU OS) (see also example 1). The amount of depreciation for this fixed asset for 2021 is 25,000 rubles. In addition, for fixed assets recognized (acquired) in 2018, one-time annual depreciation in the amount of 10,000 rubles was accrued (see also example 2).

| Dt 262 Kt 02 | RUB 35,000 | Accrual of depreciation on two fixed assets with its attribution to period expenses |

| Dt. 83 Kt 86.VR[3] | 25,000 rub. | Reduction of the NOCDI Fund for an OS object recognized (put into operation) before the start of application of the Federal Budgetary Accounting Standards for OS |

| Dt 86.VR Kt 262 | 25,000 rub. | Accounting record for closing the month: attributing to expenses of target financing depreciation accrued on fixed assets recognized before the start of application of the Federal Accounting Standards for Financial Accounting |

| Dt 86.1 Kt 83 | (10,000) rub | Partial reversal of the formation of the NOCDI Fund for OS recognized (put into operation) in the current reporting period |

| Dt 86.1 Kt 262 | 10,000 rub. | Accounting entry for closing the month: attributing to expenses of target financing depreciation accrued on fixed assets recognized in the current reporting period |

| |

| Fixed assets | RUB 90,000[4] |

| III. Special-purpose financing | |

| Fund of real estate and especially valuable movable property | 90,000 rub. |

Example 4. A fixed asset with a cost of RUB 100,000 is written off, accumulated depreciation is RUB 50,000

| Dt. 02 Kt 01 | 50,000 rub. | Write-off of depreciation |

| Dt 83 Kt 01 | 50,000 rub. | Write-off of the book value of fixed assets with simultaneous write-off of the residual value of the NOCDI Fund |

| In accordance with the explanations of the Ministry of Finance, the following version of accounting entries can also be used when writing off fixed assets | ||

| Dt 91.2 Kt 01 | 50,000 rub. | Write-off of the book value of fixed assets |

| Dt 83 Kt 91.1 | 50,000 rub. | Write-off of the residual value of the NOCDI Fund |

[1] The term “Fund of Real Estate and Particularly Valuable Movable Property” was introduced into circulation by Order of the Ministry of Finance of the Russian Federation dated July 2, 2010 No. 66n “On Forms of Accounting Reports of Organizations.” Previously, other names were used to refer to this fund in reporting.

[2] In accordance with the explanations of the Ministry of Finance and established practice, accounts 20, 86 can be used in this debit accounting entry.

[3] Special subaccount of account 86, credit turnovers on which will not be taken into account when generating the Report on the Targeted Use of Funds, Sheet 7 of the Income Tax Declaration, etc., since credit turnovers on this subaccount do not reflect the receipt of targeted funds and /or restoration of targeted funding.

https://www.youtube.com/watch?v=channelUCbFnqL3oz0gIC8V90D8PIyg

[4] 90,000 rubles (book value of fixed assets) = 100,000 rubles (cost of fixed assets) - 25,000 rubles x 2 (depreciation accumulated over 2 years) 50,000 rubles (initial cost of fixed assets) - 10,000 rubles (depreciation accumulated over year).

What entries are made when selling fixed assets?

The accounting records for the sale of a fixed asset depend on the NPO taxation system. A set of wiring for the general and simplified system is in the tables below.

Postings when selling fixed assets to non-profit organizations under the general taxation regime

| Contents of operation | Debit | Credit | Sum | Primary document |

| Listed per OS object | 60 | 51 | 60 000 | payment order, bank statement |

| Supplier's invoice accepted | 08 | 60 | 50 847,46 | invoice |

| The amount of VAT on the acquired fixed asset is reflected | 19 | 60 | 9152,54 | invoice |

| The amount of VAT is included in the price of the object | 08 | 19 | 9152,54 | accounting information |

| The object is included in fixed assets | 01 | 08 | 60 000 | act of acceptance and transfer of fixed assets |

| The source of financing for the acquired fixed asset is reflected | 86-2 | 83 | 60 000 | accounting certificate, estimate of income and expenses |

| Accrued depreciation during the operation of the OS object | 010 | 21 000 | accounting certificate-calculation | |

| The buyer's debt for the asset being sold is reflected | 76 | 91-1 | 64 900 | contract, invoice |

| The amount of VAT payable to the budget has been accrued [(64 900 – 60 000) × 18/118] | 91-3 | 68 | 748 | invoice, calculation |

| The original cost of a retiring fixed asset has been written off | 83 | 01 | 60 000 | act of acceptance and transfer of fixed assets |

| Received funds from the OS buyer | 51 | 76 | 64 900 | bank statement |

| The financial result from the sale of an asset has been identified (without taking into account other operations) [64 900 – 748] | 91-9 | 99 | 64 152 | accounting certificate-calculation |

Postings for the sale of fixed assets to non-profit organizations in a simplified manner

| Contents of operation | Debit | Credit | Sum | Primary document |

| Listed per OS object | 60 | 51 | 60 000 | payment order, bank statement |

| Supplier's invoice accepted | 08 | 60 | 50 847,46 | invoice |

| The amount of VAT on the acquired fixed asset is reflected | 19 | 60 | 9152,54 | invoice |

| The amount of VAT is included in the price of the object | 08 | 19 | 9152,54 | accounting information |

| The object is included in fixed assets | 01 | 08 | 60 000 | act of acceptance and transfer of fixed assets |

| The source of financing for the acquired fixed asset is reflected | 86-2 | 83 | 60 000 | accounting certificate, estimate of income and expenses |

| Accrued depreciation during the operation of the OS object | 010 | 21 000 | accounting certificate-calculation | |

| The buyer's debt for the asset being sold is reflected | 76 | 91-1 | 64 900 | contract, invoice |

| The original cost of a retiring fixed asset has been written off | 83 | 01 | 60 000 | act of acceptance and transfer of fixed assets |

| The amount of depreciation accrued during the operation of the asset has been written off | 010 | 21 000 | accounting certificate-calculation | |

| Received funds from the OS buyer | 51 | 76 | 64 900 | bank statement |

| The financial result from the sale of an asset has been identified (without taking into account other operations) | 91-9 | 99 | 64 900 | accounting certificate-calculation |

| Single tax charged for simplification (64 900 × 6%) | 99 | 68 | 3894 | accounting certificate-calculation |

BASIC

Is it possible to calculate depreciation in tax accounting?

Non-profit organizations that received fixed assets free of charge or purchased them using earmarked funds and use them in their statutory activities do not accrue depreciation on them. This is directly stated in subparagraph 2 of paragraph 2 of Article 256 of the Tax Code of the Russian Federation.

How to determine sales proceeds

When calculating income tax, determine the proceeds from the sale of a fixed asset of an NPO as its full sales price excluding VAT. It cannot be reduced for the cost of purchasing the property. Since targeted funds are not taken into account in income, then costs at their expense are not taken into account either. In addition, the organization had no intention of using such property for the purpose of generating income. And generating income is one of the conditions to write off as expenses for the acquisition of an object.

This conclusion follows from paragraph 1 of Article 252, paragraph 2 of Article 251, Article 250 of the Tax Code of the Russian Federation and letter of the Ministry of Finance of Russia dated February 5, 2010 No. 03-03-06/4/9.

How to calculate VAT on the sale of fixed assets

For non-commercial organizations, there are two options for calculating VAT on the sale of fixed assets.

First option : VAT must be charged on the full sales price (clause 1 of Article 154 of the Tax Code of the Russian Federation). Do this if VAT was not paid upon receipt of the fixed asset. For example, they received it for free or purchased it from an organization on a simplified basis.

Second option : charge VAT on the difference between the sale and residual value of the property. That is, according to the rules of paragraph 3 of Article 154 of the Tax Code of the Russian Federation. Using these rules, determine the tax base when the fixed asset was purchased with VAT, but the tax was not deducted. For example, the object was used for statutory activities or in business activities exempt from VAT. For full details on how to do this and examples, see How to calculate VAT on the sale of property accounted for with input VAT.

simplified tax system

Acquisition costs

Expenses for the acquisition of fixed assets received free of charge or at the expense of earmarked funds for statutory activities cannot be recognized as expenses under the simplified procedure. This conclusion follows from paragraph 4 of Article 346.16, paragraph 1 and subparagraph 2 of paragraph 2 of Article 256 of the Tax Code of the Russian Federation.

Income and expenses upon sale

When calculating the single tax, an NPO includes in its income the full sales value of the fixed asset. And even if you use a simplification with the “income minus expenses” object, do not take into account the initial cost of the fixed asset in expenses. Since targeted funds are not taken into account in income, then costs at their expense are not taken into account either. In addition, the organization had no intention of using such property for the purpose of generating income. And generating income is one of the conditions to write off as expenses for the acquisition of an object.

This conclusion follows from paragraphs 1 and 4 of Article 346.16, subparagraph 1 of paragraph 1.1 of Article 346.15, paragraph 1 of Article 252, Article 250, paragraph 2 of Article 251 of the Tax Code of the Russian Federation and letter of the Ministry of Finance of Russia dated February 5, 2010 No. 03-03-06/ 4/9.

Simplified taxation in non-profit organizations

NPOs have the right to apply simplified taxation. They can choose the simplified tax system upon creation by submitting a corresponding application to the tax office, or switch to the regime during the management process. Restrictions on the use of the simplified tax system are presented in the table.

| Index | Limitation |

| State | No more than 100 people |

| Income for 9 months | Not higher than 45 million rubles. |

| Residual value of funds | Less than 100 million rubles |

| Branches | None |

| NPO is not a manufacturer of excisable products | |

Organizations on the simplified tax system submit a single simplified declaration to the inspectorate every year. They are exempt from paying income taxes, property taxes and VAT. NPOs use a simplified method to calculate the single tax. When taxed “by income”, it is equal to 6% of all income received. With the object “income minus expenses” - 15% of the difference, and if there is no difference - 1%. (see → NPO taxation, rates in 2018)

Revenues used for statutory purposes are not subject to a single tax. This applies to grants, membership fees, donations, and subsidies for targeted needs. Simplified NPOs are required to account for income and expenses of available target amounts separately.

Under this system, the manager has the right to perform the duties of the chief accountant and not resort to the services of other organizations for accounting. The transition to the simplified tax system is beneficial for non-profit organizations engaged in the sale of goods, work for a fee and having taxable property on their balance sheet.