When to pay UTII in 2021

Transfer the calculated amount of UTII to the budget in 2021 no later than the 25th day of the first month following the expired tax period (quarter). This is provided for in paragraph 1 of Article 346.32 of the Tax Code of the Russian Federation. Therefore, the deadlines for paying UTII in 2021 are as follows:

| Deadlines for paying UTII in 2021 | |

| For the fourth quarter of 2021 | No later than 01/25/2018 |

| For the first quarter of 2021 | No later than 04/25/2018 |

| For the second quarter of 2021 | No later than July 25, 2018 |

| For the third quarter of 2021 | No later than October 25, 2018 |

Also see “Terms for payment of UTII in 2021”.

Payment order for UTII in 2021: sample

When calculating tax and filling out a payment order for UTII in 2018, it should be taken into account that the K1 coefficient for imputation has not changed compared to the two previous years. A visual example will help you fill out the UTII payment form.

A single tax on imputed income is paid by companies and individual entrepreneurs who have transferred one or more types of business to this special regime (clause 2 of Article 346.26 of the Tax Code of the Russian Federation). Payment orders for UTII are filled out at the end of each quarter. Let's give some samples.

Sample payment order for UTII in 2021 for individual entrepreneurs

Sample payment order for UTII for individual entrepreneurs

In field 8, the entrepreneur fills in the last name, first name, patronymic and in brackets - “Individual Entrepreneur”, as well as the registration address at the place of residence or the address at the place of residence (if there is no place of residence). Before and after the address information you must put a “//” sign.

In field 101 “Payer status” you must enter the code “09” (Appendix 5 to the order of the Ministry of Finance of Russia dated November 12, 2013 No. 107n). With this status, the TIN or UIN must be filled in (field 22).

For current payments, “0” must be entered in the “Code” detail (field 22), for payments at the request of the inspection - a 20-digit number, if it is in the request. If there is no number in the request, the value is “0”.

Field 110 “Type of payment” does not need to be filled in in payment slips for taxes and contributions from March 28, 2021 (Instruction of the Bank of Russia dated November 6, 2015 No. 3844-U).

When paying tax before filing a return, you must enter “0” in field 109. For current payments, after submitting reports - the date of signing the declaration. When repaying arrears: without an inspection requirement - value “0”, upon request - the date of the requirement.

In field 108, the entrepreneur fills in the document number that is the basis for the payment. For current payments and debt repayment, you must enter “0”. And for payments at the request of the inspection - the requirement number. There are 10 characters in the props, they are separated by dots. The first two are the payment frequency (CP). The next two are the quarter number (01 - 04). The last four are the year for which tax is paid. When paying off the arrears, write down the payment deadline from the request.

In field 106, the entrepreneur writes the value “TP” - for current payments. If he repays the debt, he puts “ZD”, and when making payments at the request of the inspectorate – “TR”.

In field 105 you must fill in the code OKTMO. If the tax is credited to the budget of a subject or municipality, this code is 8-digit. If the tax is distributed among the settlements that are part of the municipality, 11 characters must be entered.

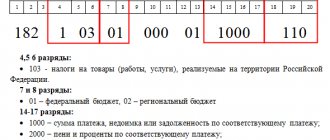

In field 104 you must put the budget classification code, which consists of 20 characters. UTII - 182 1 0500 110.

See KBK UTII 2021 for individual entrepreneurs and legal entities

Sample payment order for UTII in 2021 for organizations

The company pays tax four times a year. Each time you need to fill out a payment order. The sample can be downloaded from the link below.

Sample payment order for UTII for organizations

Organizations, unlike individual entrepreneurs, put the payer status “01” in the UTII payment order, since the company is a taxpayer.

Thirdly, banks write off taxes on behalf of the tax office (Article 855 of the Civil Code of the Russian Federation). That is, by collection. If the company pays the single tax itself, then this is the 5th stage. So, you need to put “5”.

The remaining fields must be filled out in the same way as described above.

Let us remind you that you must send the UTII payment no later than the 25th day of the first month following the expired quarter (clause 1 of Article 346.32 of the Tax Code of the Russian Federation). For example, for the 1st quarter of 2021 - no later than April 25, for the 2nd quarter - no later than July 25, etc.

For grouping in the system of accounting for expenses and income of the budget system of the Russian Federation, the state introduced a unified classification of accounting indicators. We will talk about the concept of “Budget Classification Code”, the use of the BCC for “imputed” tax by individual entrepreneurs and legal entities, and the deciphering of the composition of the codes in today’s review. In addition to these key questions, we will offer you the current UTII KBK 2021 for legal entities and individual entrepreneurs.

Where to pay

In 2021, pay UTII according to the details of the Federal Tax Service, which has jurisdiction over the territory where the “imputed” activity is carried out. In this case, the organization must be registered by the Federal Tax Service as a payer of UTII (clause 2 of Article 346.28, clause 3 of Article 346.32 of the Tax Code of the Russian Federation). However, if there are certain types of business that these rules do not apply to, namely:

- delivery and distribution trade;

- advertising on vehicles;

- provision of services for the transportation of passengers and cargo.

For these types of businesses, organizations do not register as UTII payers at the place where they conduct their activities. Therefore, they pay UTII at the location of the head office.

Where to pay UTII

The Federal Tax Service is the body that is responsible for tax control. The service has divisions in populated areas. The choice of branch for payment is carried out on a territorial basis using UTII KBK. A general rule has been established: tax is paid at the place of activity.

Exceptions to the rule:

- cargo transportation;

- transportation of passengers;

- advertising placed on vehicles;

- delivery trade;

- payment of insurance premiums for employees.

Both categories are paid at the place of registration of the individual entrepreneur. Other types of activities, from household and veterinary services to the lease of a retail outlet, are subject to the main norm.

Budget classification code for 2018

The budget classification code for paying UTII in 2021 is 182 1 0500 110. In payment orders you must put this 20-digit BCC for paying UTII for the 1st quarter of 2021 and subsequent reporting periods.

If, in addition to tax, it is necessary to pay a penalty or a fine, the BCC will be distinguished by four characters from 14 to 17. The meanings of these codes are as follows:

- for imputed tax – 1000;

- penalties – 2100;

- fine – 3000.

As a result, the table with BCC for UTII for 2021 looks like this:

KBK table from 2021 for LLC and individual entrepreneur

| Payment type | KBK details |

| Imputed tax | 182 1 0500 110 |

| Penalty | 182 1 0500 110 |

| Fine | 182 1 0500 110 |

KBK UTII in 2021: what changes

As of January 1, 2018, changes to the BCC for payment of taxes and fees came into effect. They did not affect all payments. To pay the single tax on imputed income, the same budget classification codes are used as in 2021.

KBK UTII 2021 for legal entities and individual entrepreneurs

To pay the tax, a twenty-digit budget classification code is used. For late payment, the Tax Inspectorate will issue a fine and charge a penalty. Tax, penalty and fine must be sent to different KBK. There will be differences in the code of 14-17 characters.

So, to pay the main payment in KBK 14-17, the characters will be “1000”, to pay a fine – “3000”, to pay a penalty – “2100”.

| Purpose of payment | KBK UTII 2021 for individual entrepreneurs and legal entities. persons |

| Imputed tax | 182 1 0500 110 |

| Fine | 182 1 0500 110 |

| Penalty | 182 1 0500 110 |

UTII also provides for interest. The single tax on imputed income for certain types of activities in the form of interest on the corresponding payment must be paid to the following BCC:

182 1 0500 110

For tax periods expired before 01/01/2011, the single tax on imputed income for certain types of activities (interest on the corresponding payment) is paid according to the following BCC:

Sample payment order for payment of UTII in 2021

The BCC for payment of UTII in the payment order must be indicated in field 104.

As for the other fields of the payment order for the payment of current UTII payments in 2021, pay attention to the following:

- in field 105 “OKTMO” - OKTMO of the municipality in which the company or entrepreneur is registered as a payer of “imputed” tax;

- in field 106 “Basis of payment” - for current “imputed” payments - “TP”;

- in field 107 “Tax period indicator” - the number of the quarter for which UTII is transferred. Let’s say “KV.01.2018”;

- in field 108 “Document number” – for current payments “0”;

- in field 109 “Date of payment basis document” - for current payments - the date of signing the UTII declaration;

- Field 22 “UIN” – is filled in if the company (IP) pays imputed tax at the request of the Federal Tax Service. Then this detail will be required by the tax authorities. Otherwise, field 22 is “0”.

- field 110 “Payment type” is not filled in.

Example:

Stella LLC pays UTII for the 1st quarter of 2021. The deadline for paying UTII for the 1st quarter is no later than April 25, 2021. In field 104 of the payment, the company will indicate KBK - 182 1 0500 110. In field 101, Stella LLC will write 01, in field 105 there will be OKTMO, in field 106 - TP, in field 107 - KV.01.2018. The accountant will put 0 in field 108, and in field 109 the date of signing the UTII declaration for the 1st quarter of 2021. In field 21 –5, in field 22 – 0.

If you find an error, please select a piece of text and press Ctrl+Enter.

BCC for UTII in 2021 for legal entities and individual entrepreneurs: table

What budget classification codes (BCC) for UTII are defined for 2018? Have the BCCs for UTII changed? Have new codes been approved for the single imputed tax? This article presents an up-to-date table with a breakdown of the BCC for UTII for 2021, and also provides a sample payment order for the transfer of a single tax. The table may be useful for legal entities and individual entrepreneurs. If you indicate an incorrect BCC on your payment slip, you will need to clarify the payment. Also see “Changes to UTII in 2021“.

When to pay UTII in 2021

Transfer the calculated amount of UTII to the budget in 2021 no later than the 25th day of the first month following the expired tax period (quarter). This is provided for in paragraph 1 of Article 346.32 of the Tax Code of the Russian Federation. Therefore, the deadlines for paying UTII in 2021 are as follows:

| Deadlines for paying UTII in 2021 | |

| For the fourth quarter of 2021 | No later than 01/25/2018 |

| For the first quarter of 2021 | No later than 04/25/2018 |

| For the second quarter of 2021 | No later than July 25, 2018 |

| For the third quarter of 2021 | No later than October 25, 2018 |

Also see “Terms for payment of UTII in 2021”.

Where to pay

In 2021, pay UTII according to the details of the Federal Tax Service, which has jurisdiction over the territory where the “imputed” activity is carried out. In this case, the organization must be registered by the Federal Tax Service as a payer of UTII (clause 2 of Article 346.28, clause 3 of Article 346.32 of the Tax Code of the Russian Federation). However, if there are certain types of business that these rules do not apply to, namely:

- delivery and distribution trade;

- advertising on vehicles;

- provision of services for the transportation of passengers and cargo.

For these types of businesses, organizations do not register as UTII payers at the place where they conduct their activities. Therefore, they pay UTII at the location of the head office.

Budget classification code for 2021

The budget classification code for paying UTII in 2021 is 182 1 0500 110. In payment orders you must put this 20-digit BCC for paying UTII for the 1st quarter of 2021 and subsequent reporting periods.

If, in addition to tax, it is necessary to pay a penalty or a fine, the BCC will be distinguished by four characters from 14 to 17. The meanings of these codes are as follows:

- for imputed tax – 1000;

- penalties – 2100;

- fine – 3000.

As a result, the table with BCC for UTII for 2021 looks like this:

KBK table from 2021 for LLC and individual entrepreneur

| Payment type | KBK details |

| Imputed tax | 182 1 0500 110 |

| Penalty | 182 1 0500 110 |

| Fine | 182 1 0500 110 |

Sample payment order for payment of UTII in 2021

The BCC for payment of UTII in the payment order must be indicated in field 104.

As for the other fields of the payment order for the payment of current UTII payments in 2021, pay attention to the following:

- in field 105 “OKTMO” - OKTMO of the municipality in which the company or entrepreneur is registered as a payer of “imputed” tax;

- in field 106 “Basis of payment” - for current “imputed” payments - “TP”;

- in field 107 “Tax period indicator” - the number of the quarter for which UTII is transferred. Let’s say “KV.01.2018”;

- in field 108 “Document number” – for current payments “0”;

- in field 109 “Date of payment basis document” - for current payments - the date of signing the UTII declaration;

- Field 22 “UIN” – is filled in if the company (IP) pays imputed tax at the request of the Federal Tax Service. Then this detail will be required by the tax authorities. Otherwise, field 22 is “0”.

- field 110 “Payment type” is not filled in.

Example:

Stella LLC pays UTII for the 1st quarter of 2021. The deadline for paying UTII for the 1st quarter is no later than April 25, 2021. In field 104 of the payment, the company will indicate KBK - 182 1 0500 110. In field 101, Stella LLC will write 01, in field 105 there will be OKTMO, in field 106 - TP, in field 107 - KV.01.2018. The accountant will put 0 in field 108, and in field 109 the date of signing the UTII declaration for the 1st quarter of 2021. In field 21 –5, in field 22 – 0.

If you find an error, please select a piece of text and press Ctrl+Enter.

UTII (KBK): at what KBK should entrepreneurs pay UTII?

When paying UTII, the payment order must indicate the BCC corresponding to this type of tax. At the same time, the BCC for UTII for individual entrepreneurs in 2019 did not change compared to those applied in 2021.

When specifying the BCC in a payment order for the payment of UTII, it is necessary to differentiate whether the tax itself is paid or a penalty or fine on it, since categories 14-17 of the BCC depend on the type of payment:

| Type of payment for UTII | KBK |

| Tax | 182 1 0500 110 |

| Penalty | 182 1 0500 110 |

| Fine | 182 1 0500 110 |

KBK penalties for UTII for individual entrepreneurs in 2020-2021

In addition to the timely payment of taxes, penalties and fees, the state, represented by the Ministry of Finance, has made it obligatory for the taxpayer to independently “arrange” their payments according to the purpose, levels and classification of budget income and expenses, indicating a 20-digit digital code (KBK) in field 104 of the payment order.

Read about the rules for filling out the BCC in payment orders in the article “Filling out field 104 in a payment order (nuances)” .

For information about filling out other fields of a payment order for paying taxes, read the article “Filling out the code field in a payment order.”

Lists of KBK are established by the Ministry of Finance. To pay penalties on UTII KBK in 2020-2021, a single number is used for both individual entrepreneurs and enterprises: 182 10500 110.

You can see which BCC you need to pay UTII in 2020-2021 in this article.

If an error was made in the KBK

If the taxpayer made a mistake when paying UTII, he will not have to pay the same amount again. After all, even if there is an error in the KBK, the tax, penalty or fine will be credited to the budget system of the Russian Federation, if the Federal Treasury account number and the name of the recipient’s bank are correctly indicated in the payment slip (Clause 4 of Article 45 of the Tax Code of the Russian Federation). To clarify the payment, the taxpayer just needs to send a letter to the inspectorate to clarify the payment, in which he indicates which BCC is considered correct, and attach to it a copy of the originally sent payment order with an error.

Payment order for penalties in 2021

It is calculated either as a percentage or a specific amount is indicated.

The actual penalty or penalty in the narrow sense is established, as a rule, for a continuing violation, calculated as a percentage of the amount of the unfulfilled obligation or in a fixed sum of money; the fine is paid one-time and must be initially agreed upon in the contract.

The fine is collected for a one-time or ongoing violation in a fixed sum of money or as a percentage of the amount of the unfulfilled obligation. The penalty, as a rule, is paid by one counterparty to another. Penalty is applied, as a rule, to debts of enterprises, as a measure of punishment for delay in monetary obligations. It is a type of penalty and is paid for each day of delay. According to tax legislation, penalties are charged for delays in paying taxes, as well as advance payments on them.

If the company does not transfer the fine on time, its account may be blocked.

Reporting (UTII) for individual entrepreneurs in 2019

| Period | Deadline for submitting UTII |

| 4th quarter 2021 | January 21, 2021 |

| 1st quarter 2021 | April 22, 2021 |

| 2nd quarter 2021 | July 22, 2021 |

| 3rd quarter 2021 | October 21, 2021 |

For failure to submit a tax return for UTII in 2019 within the established deadlines, a fine is charged in the amount of 5% of the amount of tax payable, but not more than 30% of this tax amount and not less than 1,000 rubles (clause 1 of Article 119 of the Tax Code of the Russian Federation ).

Deadlines for paying UTII in 2021

According to Article 346.32 of the Tax Code of the Russian Federation, taxes are transferred to the budget for individual entrepreneurs and organizations using UTII until the 25th day of the month following the tax period (quarter). Deadlines for paying UTII in 2021:

- April 25, 2019;

- July 25, 2019;

- October 25, 2019;

- January 25, 2021.

Payment of tax to the budget is possible earlier than the specified deadlines, and the listed dates are the deadlines for making payments. As for fines and penalties, they should be listed as they are recognized. If the tax office requires payment of fines and penalties, be guided by the date indicated in the requirement.

UTII: payment deadlines for individual entrepreneurs 2021

The single tax is paid to the budget quarterly no later than the 25th day of the month following the quarter (Clause 1, Article 346.32 of the Tax Code of the Russian Federation).

| Period | Deadline for payment of UTII |

| 4th quarter 2021 | January 25, 2021 |

| 1st quarter 2021 | April 25, 2021 |

| 2nd quarter 2021 | July 25, 2021 |

| 3rd quarter 2021 | October 25, 2021 |

For non-payment of the single tax, a fine is imposed in the amount of 20% of the amount of tax debt (clause 1 of Article 122 of the Tax Code of the Russian Federation). It threatens if the tax is incorrectly reflected in the declaration, leading to non-payment of tax.

Payment order for payment of UTII for the 1st quarter of 2021 - 2021 sample

Before and after the address information you must put a “//” sign.

In addition, it is necessary that the type of activity of the subject be included in the list from Art. 346.26 of the Tax Code of the Russian Federation, the number of staff did not exceed 100 people and the requirements for the participation of other organizations in them were met.

In field 101 “Payer status” you must enter the code “09” (Appendix 5 to the order of the Ministry of Finance of Russia dated November 12, 2013 No. 107n). With this status, the TIN or UIN must be filled in (field 22). For current payments, “0” must be entered in the “Code” detail (field 22); for payments at the request of the inspection, a 20-digit number, if it is included in the request.

If there is no number in the requirement, the value is “0”.

Field 110 “Type of payment” from March 28, 2021 in payments for taxes and contributions does not need to be filled in (Instruction of the Bank of Russia dated November 6, 2015 No. 3844-U). When paying tax before filing a declaration, you must enter “0” in field 109.

For current payments, after submitting reports - the date of signing the declaration. When repaying arrears: without an inspection requirement – value “0”, upon request – the date of the requirement. In field 108, the entrepreneur fills in the document number that is the basis for the payment.

What is the BCC for UTII in 2021?

In 2021, the BCC for UTII did not change compared to 2021. As before, the BCC depends on the type of payment (tax, penalty or fine):

| Type of payment for UTII | KBK |

| Tax | 182 1 0500 110 |

| Penalty | 182 1 0500 110 |

| Fine | 182 1 0500 110 |

Differences in the KBK by type of payment (tax, penalty, fine) are only in 14-17 categories (1000, 2100, 3000, respectively).

According to the BCC table, taxes, penalties and fines are listed by both organizations and individual entrepreneurs using UTII.

It is worth noting that KBK-UTII (2019) for legal entities are the same as KBK-UTII (2019) for individual entrepreneurs.

BCC for penalties on UTII in 2021 - 2021

Penalties for individual entrepreneurs who paid the tax late are calculated using the formula: P = DP × ∑tax × 1/300 × StRSB, where: P - penalties; DP - number of days of delay; ∑tax - the amount of UTII; STRB is the Central Bank refinancing rate, the value of which from 01/01/2016 is equal to the value of the Central Bank key rate. Legal entities can use this formula only in 2 cases: if the tax arrears arose before October 1, 2017 or if the payment is overdue for no more than 30 days. Starting from the 31st day of delay, penalties for taxpayers - legal entities will be calculated according to the formula: P = ∑tax × StRSB / 300 × 30 + ∑tax × StRSB / 150 × (DP – 30).

To calculate the penalty, use ours.

Example 1 The taxpayer paid UTII on 08/09/2021 instead of 07/25/2019, that is, he was 15 calendar days late (in accordance with the explanations of the Federal Tax Service of Russia from the letter dated 12/06/2017 No. ZN-3-22/ [email protected] the day of actual payment is not included in calculation of penalties).

KBK penalty (UTII)

Days of delay are counted from the day following the due date for tax payment until the day the tax debt is repaid, inclusive. The interest rate of the penalty depending on the type of UTII payers and the number of days of delay is determined as follows: Taxpayer UTII Number of calendar days of delay Up to 30 days (inclusive) Over 30 days Organization 1/300*R 1/150*R Individual entrepreneur 1/300*RR is , valid in the corresponding period.

The BCC for paying penalties on UTII in 2021 has not changed compared to 2021. You need to pay penalties for the “imputed” tax according to the following BCC: 182 1 0500 110 By the way, the UTII tax itself is paid to BCC 182 1 0500 110, and the tax penalty is paid to BCC 182 1 0500 110.

Also read:

Accountant forum: Share:

How to fix an error in KBK?

Let us remind you that errors in a payment order that lead to non-crediting of tax to the budget system of the Russian Federation are incorrect instructions (clause 4 of Article 45 of the Tax Code of the Russian Federation):

- Federal Treasury account numbers;

- name of the recipient's bank.

An incorrect indication of the BCC is not an error that prevents the tax from being credited to the budget system. Therefore, it cannot be said that the taxpayer’s obligation to transfer UTII in this case will not be fulfilled. There is no need to pay taxes, penalties or fines again if there is an error in the KBK. It is enough to send a letter to your inspection to clarify the payment, in which you indicate the correct BCC to which the payment should have been credited. It is advisable to attach to the letter a copy of the payment slip originally sent to the bank with an error in the KBK.

KBK for UTII for individual entrepreneurs and organizations in 2019

The cloud service Kontur.Accounting helps generate payment orders with current BCCs for paying taxes.

The KBK in 2021 is no different from the code that was in force in 2018. It depends on the type of payment that needs to be made - tax, fine, interest or penalties. For example, to pay UTII, you need to enter the following 20-digit code in the appropriate section (field 104) of the payment slip: 182 1 0500 110. In order to pay a fine or penalty, you need to make changes to this code by changing 4 digits. Thus, the final version of the CBC:

- for tax - 182 1 0500 110;

- for penalties - 182 1 0500 110;

- for interest - 182 1 0500 110;

- for fines - 182 1 0500 110.

BCCs differ for different types of payments (tax, penalties, interest or fine) - only in digits from the 14th to the 17th.

Organizations and individual entrepreneurs transfer money to the same cash registers. Payment orders are distinguished by field 101 “payer status” - individual entrepreneurs put the code “09” in it, and legal entities - “01”.

When should I transfer UTII?

Payers must pay UTII tax quarterly. For the past quarter - no later than the 25th day of the first month of the next quarter (clause 1 of Article 346.32 of the Tax Code of the Russian Federation). If the deadline for payment falls on a weekend or non-working holiday, the tax can be transferred on the first working day following such a day (Clause 7, Article 6.1 of the Tax Code of the Russian Federation).

For the tax periods of 2021, UTII is transferred within the following periods:

The table shows the deadlines for payment. Of course, the taxpayer can transfer the tax before these dates (clause 1 of Article 45 of the Tax Code of the Russian Federation).

Penalties and fines calculated and transferred by the taxpayer voluntarily are paid as they are recognized. And penalties and fines presented on the basis of a tax demand are paid within the time limits specified in such demand.

Deadlines for payment of UTII for 2019

UTII is paid by entrepreneurs (as well as organizations) quarterly. Tax for the past quarter must be paid no later than the 25th day of the first month of the next quarter (Clause 1, Article 346.32 of the Tax Code of the Russian Federation). The above means that for the tax periods of 2021, UTII must be transferred within the following periods:

| Tax periods 2021 | Deadline for payment of UTII |

| 1st quarter | 25.04.2019 |

| 2nd quarter | 25.07.2019 |

| 3rd quarter | 25.10.2019 |

| 4th quarter | 27.01.2020 |

UTII is paid by entrepreneurs at the place of registration with the tax office as a special regime payer.

Where to transfer UTII

UTII (including penalties and fines) are transferred according to the details of the tax office in which the organization or individual entrepreneur is registered as a UTII payer (clause 1 of Article 346.32 of the Tax Code of the Russian Federation). In general, such a tax inspection is the inspection at the place where an organization or individual entrepreneur conducts business activities transferred to UTII. And for some types of activities (for example, the provision of motor transport services for the transportation of passengers and goods or placement of advertising using the external and internal surfaces of vehicles) - the tax inspectorate at the location of the organization or the place of residence of the individual entrepreneur (clause 2 of Article 346.28 of the Tax Code of the Russian Federation). Your tax office for transferring UTII will be indicated in the notification that is issued to the UTII payer after registering it (clause 3 of Article 346.28 of the Tax Code of the Russian Federation).

Contents of the act:

- date of preparation and type of payment;

- information about the individual entrepreneur, his name and TIN;

- information about the recipient (indicate BIC, TIN and KPP;

- payment amount in numbers and words.

Since an individual entrepreneur does not have a checkpoint, “0” is indicated in the field. The document is drawn up in printed form on a tangible medium. It is acceptable to prepare an order in electronic format. For ease of perception, below is a sample payment order that will help you avoid errors and typos when filling out.

UTII is a single tax on imputed income. It is simply called “imputation”. This tax system allows you to replace several tax fees:

- Personal income tax (for individual entrepreneurs);

- property tax (except for those for which the cadastral value is assessed to pay the tax fee);

- VAT (all items except export).

There are some types of activities for which it is impossible to switch to UTII. These include:

- advertising on vehicles;

- peddling and distribution trade;

- provision of services for the transportation of goods and passengers.

Every entrepreneur or legal entity can switch to UTII if its activities are on the list that provides for such a taxation system. Also, the company must have no more than 100 employees. The tax must be paid within the time limits specified in Article 346.42 of the Tax Code of the Russian Federation.

UTII is paid every quarter no later than the 25th day of the month following the month the quarter ends. So for the first quarter of 2018, the payment is transferred until 04/25/2018, for the second quarter - until 07/25/2018, for the third quarter - until 10/25/2018, for the fourth quarter - until 01/25/2019.