Hello, Vasily Zhdanov is here, in this article we will look at business expenses. If it is customary for a company’s accounting department to keep account 44 “Sales expenses,” commercial expenses must be reflected (line 2210 of the Income Statement). Doubts, as a rule, are raised by the list of possible expenses that could be classified as commercial, since the costs of trading and manufacturing enterprises differ in composition. In addition, it is not always clear how to write off business expenses, what entries to make in the balance sheet, and how to maintain financial statements. All this will be discussed in the article.

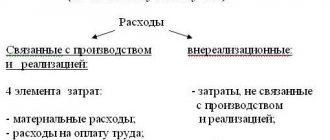

What costs can be included in business expenses (line 2210)

Depending on whether the enterprise is a trade (wholesale, retail) or manufacturing enterprise, the list of business expenses may vary:

Take our proprietary course on choosing stocks on the stock market → training course

| Kind of activity | What are the costs involved? | additional information |

| Production | Includes any costs associated with sales: – entertainment expenses; – costs of advertising the product; – depreciation costs (wear and tear of office and commercial equipment); – payment for security services; – wages of employees (including office workers) engaged in sales; – costs of maintaining an office and warehouse space. | Any other expenses reflected in the debit of account 44 and related to distribution costs are also taken into account. |

| Trade (retail, wholesale) | Costs of selling manufactured products: – entertainment expenses aimed at promoting the product; – advertising costs; – costs of maintaining warehouses with goods ready for sale; – commission fees; – transport costs (delivery to the place where goods are sent); – packaging costs; – other similar expenses. | If we are talking about a manufacturer (processor) of agricultural products, in addition to commercial expenses include: – costs of maintaining reception and procurement points (including caring for poultry and livestock there); – general procurement costs; – other similar costs. |

What is included in business expenses for wholesale and retail trade enterprises?

Selling expenses for wholesale and retail trade enterprises include all sales costs, for example:

- expenses for maintaining warehouses and offices;

- wages of employees engaged in trade, including office workers;

- security services;

- depreciation of commercial and office equipment;

- advertising expenses;

- entertainment expenses;

- all other costs that relate to distribution costs and are reflected in the debit of account 44.

How are business expenses written off?

Enterprises are allowed to independently decide on the procedure for writing off business expenses (the rules are not approved by legislative and regulatory acts). At the same time, companies are required to consolidate the write-off method they have chosen in their accounting policies.

Important! For manufacturing companies, there are recommendations for writing off business expenses, which are given in the text of the Instructions for using the Chart of Accounts.

Product manufacturers are recommended to write off sales costs as a debit to their account. 90 “Sales” s/ac. 2 “Cost of sales”. The costs of a manufacturing company for transportation and packaging should be distributed among the varieties of shipped goods based on considerations of an independently selected indicator (cost of ready-to-sell products, volume, weight, quantity).

To calculate the amount of business expenses to be written off, you must first calculate the value of the special coefficient using the formula below:

Knowing the value of this coefficient, you can proceed to calculating the volume of business expenses of the enterprise to be written off:

Selling expenses for manufacturers

This type of cost includes manufacturing companies the costs of selling finished products, which, in particular, can be:

- product packaging costs;

- transportation costs for moving to the places where products are sent;

- commission fees;

- costs for finished product warehouses;

- advertising expenses;

- entertainment expenses associated with product promotion;

- other similar expenses.

Firms that procure and process agricultural products may additionally include:

- general procurement expenses;

- expenses for maintaining procurement and receiving points, including keeping livestock and birds there, and other similar expenses.

ConsultantPlus experts explained in detail what other costs are written off as commercial expenses. Get trial access to the legal reference system and study the material for free.

For information on how sales expenses are collected in accounting, read the article “Accounting entries for business expenses.”

Commercial expenses are written off to (line 2210) in accounting

The following regulations and legislative acts will help you understand how to write off business expenses:

| Regulatory act, law | Application area |

| Order of the Ministry of Finance of Russia dated October 31, 2000 No. 94n | Instructions for the chart of accounts |

| Order of the Ministry of Finance of Russia dated December 28, 2001 No. 119n | Approval of Appendix 3 to the guidelines. Instructions for allocating costs for normal inventories. |

| Order of the Ministry of Agriculture of Russia dated January 31, 2003 No. 26 | Approval of appendices 3 and 4 to the guidelines. Distribution instructions for inventories that are formed in agricultural companies. |

Expenses accumulated on the account. 44, are subject to debit to the account every month. 90. But at the end of the month, this account may have a balance related to unsold finished goods (for manufacturing companies) or remaining unsold goods (for trading enterprises). The mentioned balance appears due to the distribution of transport and procurement costs, including costs for:

- procurement of agricultural raw materials, poultry and livestock (from companies engaged in agricultural production and processing);

- transportation (from trading enterprises and intermediary firms);

- packaging and transportation (from product manufacturers).

Distribution is carried out according to instructions approved by regulations listed in the table above.

Administrative and commercial expenses

For accounting purposes, an enterprise is given the right to independently determine the procedure for recognizing management and commercial expenses, which it must necessarily consolidate in its accounting policy (clause 20 of PBU 10/99).

The mentioned expenses may be charged to the cost of production to the extent that they are recognized as expenses of the reporting period for ordinary activities. In addition, administrative and selling expenses can be written off to the cost of products sold, goods, works, services in the full amount of expenses recognized in a given reporting period. The Ministry of Finance recently recalled this in a letter dated September 2, 2008 No. 07-05-06/191.

Before we begin to understand the procedure for recognizing such expenses, we will determine which expenses are called commercial and which are management.

Management expenses include expenses not related to the production or commercial activities of the enterprise: for the maintenance of the personnel department, legal department; for lighting and heating of non-production facilities, as well as for business trips, communication services and other similar expenses.

Selling expenses are expenses associated with the shipment and sale of goods. Those enterprises that carry out production activities have the right to include commercial expenses for packaging products; for delivery of products to the departure station, loading into vehicles; commission fees paid to intermediary organizations; product storage costs; for advertising, entertainment and other similar expenses.

In turn, trade organizations can include as sales expenses the funds spent on transporting goods, on wages, on rent, on the maintenance of buildings, structures, premises and equipment; costs of storing goods; for advertising; for entertainment and other similar expenses. Such a list is given in the Instructions for the Chart of Accounts.

Recognition of management expenses

In accounting, management expenses are reflected in the debit of the general expenses account. If, according to the accounting policy, administrative expenses are partially included in the cost of production, they will be written off in one of the following entries:

Debit 20 Credit 26 - if the production of this type of product is the main activity of the organization.

Debit 23 Credit 26 - if auxiliary production produced products and work and provided services to the outside.

Debit 29 Credit 26 - if servicing industries and farms performed work and services outsourced.

If such costs are attributed to accounts 20, 23 or 29, they will be included in the cost price as the products produced are sold, that is, as these costs are written off from accounts 20, 23 and 29 to account 90.

If administrative expenses are recognized in full, then as semi-fixed expenses they will be charged directly to the cost of sales of the reporting period in which they arose. The posting in this case will be as follows: Debit 90 Credit 26

When writing off administrative expenses to account 90, they are fully included in the cost of production in the reporting period when they were recognized as “expenses for ordinary activities.” However, there is one caveat here. This can be done only on the condition that the organization complies with the procedure for generating expenses on account 26, provided for by the Instructions for the Chart of Accounts, approved by Order of the Ministry of Finance dated October 31, 2000 No. 94n. It says that account 26 is provided to reflect information on expenses for management needs not directly related to the production process.

It turns out that account 26 was originally intended to record expenses specifically for managing the organization. However, in practice, it may turn out that this account takes into account not only administrative expenses, but also production costs. In this case, it is incorrect to talk about writing off the entire amount from the general expenses account by posting Debit 90 Credit 26 . You can write off only that part of expenses that are directly administrative.

We also note that when filling out a profit and loss statement, you should remember that the line “Administrative expenses” is filled in only if administrative expenses are not distributed among costing objects, that is, the second option for reflecting costs is selected in the accounting policy and there are no accounting entries Debit 20 Credit 26, Debit 23 Credit 26, Debit 29 Credit 26. Otherwise, management costs are not deducted from production costs and the line “Management costs” is not filled in (clause 21 of PBU 10/99).

What about business expenses?

Commercial expenses are accumulated in the debit of account 44 “Sales expenses”. As noted above, they are written off to the cost of products sold either in full or in proportion to the volume of products sold. In both cases, the write-off is made to the debit of account 90 “Sales”.

Here it is necessary to remember that, recognizing business expenses in an incomplete amount, the company will need to distribute certain types of expenses listed in the Instructions for using the Chart of Accounts.

Firstly, these are the costs of packaging and transporting products in organizations engaged in industrial and other production activities. Distribution is carried out between individual types of shipped products on a monthly basis, based on their weight, volume, production cost or other relevant indicators.

Secondly, these are transportation costs in organizations engaged in trading and other intermediary activities, which are distributed between the goods sold and the balance of goods at the end of each month.

Thirdly, these are the costs of procuring agricultural raw materials and the costs of procuring livestock and poultry in organizations that procure and process agricultural products. Moreover, the first are distributed to the debit of account 15 “Procurement and acquisition of material assets”, and the second - to the debit of account 11 “Animals for growing and fattening”.

S. Lisitsyna , expert at the Federal Financial Information Agency

How are selling expenses (line 2210) reflected in the income statement

Selling expenses of trading and manufacturing companies, which were reflected on account 90, are subject to accounting in the total cost of sales. Such costs should be reflected in line 2210 “Business expenses” in the income statement.

It also happens that an enterprise does not use account 44. This is only possible if the costs collected on the account do not have a component that is subject to mandatory distribution. If the company does not use an account. 44, business expenses are usually reflected in account 26, which is closed in 2 ways:

- By writing off the total amount of expenses accumulated by the company on account 26, directly to the debit of account 90 (then commercial expenses fall into line 2220 “Administrative expenses”).

- By including in the cost of finished goods the method of distributing the expenses collected by the company on account 26 (then the expenses are included in the amount of line 2120 “Cost of sales” in the process of writing off the cost of goods sold).

Results

In the income statement, line 2210 reflects selling expenses written off to account 90, which are preliminarily collected under account 44 “Sales expenses”.

If there are costs subject to distribution as part of business expenses, account 44 may have a balance at the end of the month. This balance in the balance sheet will appear in line 1210. You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Example of filling out line 2210 “Business expenses”

Let's look at an example of how line 2210 of the Income Statement is filled in:

| Indicators for s/sch 90-2 sch. 90 in correspondence with account. 44 (rubles) | ||||

| Turnover for the reporting period (2014) | Sum | |||

| 1 | 2 | |||

| 1. According to Dt s/sch 90-2 in correspondence with the account. 44 | 735 555 | |||

| Fragment of the financial results report for 2013 | ||||

| Explanations | Indicator name | Code 3 | For 2013 | For 2012 |

| 1 | 2 | 3 | 4 | 5 |

| Business expenses | 2210 | (1021) | (734) | |

Selling expenses for the reporting period amounted to 735,555 rubles.

| Fragment of the financial results report for 2013 | ||||

| Explanations | Indicator name | Code 3 | For 2014 | For 2012 |

| 1 | 2 | 3 | 4 | 5 |

| Business expenses | 2210 | (860) | (1021) | |

The procedure for optimizing commercial expenses

Reducing the company's sales costs allows it to increase its profitability and profitability . There are several points that are worth paying attention to when optimizing a company’s commercial expenses:

- organization of effective management, rather than targeted cost reduction;

- each cost unit should bring maximum results;

- expenses are the result of the company’s actions, as well as the result of inaction;

- reduction of costs impossible without costs that are directly invested in this;

- maintaining optimal cost levels is the key to successful operations and increased economic efficiency;

- You should not save on costs that allow you to insure the company against more significant costs;

- Analytical work aimed at optimizing business expenses should be carried out constantly.

Read more Selling expenses (line 2210). What is included

An example of reflecting business expenses in accounting

The following information is known about the enterprise, the main activity of which is retail trade in food and household goods:

| Business expenses item | Amount (rub.) |

| Depreciation charges (fixed assets) | 41 000 |

| Employees' wages, insurance contributions to funds | 233 000 |

| Expenses for consulting and legal services | 321 000 (including VAT RUB 44,000) |

| Costs for the delivery of goods by transport (subject to accounting as part of distribution costs, according to accounting policies) | 987 000 (including VAT RUB 135,317) |

| Rental payments for sales areas, warehouses and general business areas | 625 000 (including VAT RUB 85,687) |

| Total expenses of the enterprise for the reporting period | 3 125 000 (including VAT RUB 428,437) |

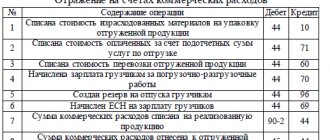

The enterprise accountant will reflect the listed expenses with the following entries:

| Accounting record | Amount (rub.) | DEBIT | CREDIT |

| Input VAT on rental costs is taken into account | 85 687 | 19 | 60 |

| Rental costs included | 539 313 (625 000 – 85 687) | 44 | 60 |

| Accepted for deduction of “input” VAT on rental costs | 85 687 | 68 | 19 |

| Input VAT on transportation costs is taken into account | 135 317 | 19 | 60 |

| The costs of transporting goods are taken into account | 851 683 (987 000 – 135 317) | 44 | 60 |

| Accepted for deduction of “input” VAT on transportation costs | 135 317 | 68 | 19 |

| Input VAT on expenses for consultations and legal services is taken into account | 44 000 | 19 | 60 |

| Costs for consultations and legal services are taken into account | 277 000 (321 000 – 44 000) | 44 | 60 |

| Accepted for deduction of “input” VAT on expenses for consultations with specialists and lawyers | 44 000 | 68 | 19 |

| Accrued wages of employees and insurance payments for wages | 233 000 | 44 | 69, 70 |

| Depreciation has been calculated on fixed assets | 41 000 | 44 | 02 |

| Total distribution costs as of the end of the reporting period | 1 941 996 (539 313 + 851 683 + 277 000 + 233 000 + 41 000) | ||

If the accountant writes off such expenses in the reporting period to account 90 “Sales” for accounting for revenue, the expenses should be reflected on line 2210 “Business expenses”. Next, in line 1210 “Inventories” (subsection “Work in Progress”) you need to indicate the amount of costs that have not been written off.

Procedure for calculating commercial expenses

The profitability of a company's production activities is directly related to the volume of resources invested in production, as well as to the promotion of these products on the market . If there is an increase in business expenses, this indicates that there is a decrease in the profitability of the company’s activities, and therefore the need to optimize costs for selling products.

Financial analysis includes certain methods for assessing the performance of sales departments by comparing the following indicators:

- business expenses;

- volume of products sold.

In this case, the first indicator is divided into semi-fixed costs, as well as variable costs. To calculate variable business expenses, it is necessary to add up all costs that are directly related to packaging, packaging, procurement and transportation. The dynamics of this amount reflects relative cost savings or cost overruns.

In order to calculate a constant type of business expenses, it is necessary to add up all costs that are not tied to the volume of products sold. This category includes rent and entertainment expenses. Analysis of indicators over time reflects absolute cost savings or overruns.

Important! The business expenses budget includes variable costs allocated to general production costs, advertising costs, marketing activities and market analysis, storage costs and fixed sales resources.

Answers to frequently asked questions about business expenses (line 2210)

Question: For what purpose should manufacturing companies distribute transportation and packaging costs between types of shipped products while partially writing off these costs?

Answer: Indeed, manufacturers need to do exactly this, since not all products that were shipped to customers will eventually be sold. It depends on what exactly is said in the contract between the seller and the buyer:

- if this is a supply agreement, the products are not considered sold until the buyer fully fulfills the terms of the agreement;

- if this is a goods exchange agreement, the products are not considered sold until the buyer makes a counter shipment of the goods.

Accounting entries for business expenses

This method is considered easy to implement because costs are not reassigned based on their functional classification.

The second form of analysis is the cost function or cost of sales method, which classifies costs according to their function as a component of cost of sales or, for example, distribution or administrative costs. When using it, an enterprise must, at a minimum, disclose its cost of sales separately from other expenses. An example of classification based on the cost function method is as follows:

| Indicator name | |

| Revenue | X |

| Cost of sales | (X) |

| Gross profit | X |

| Other income | X |

| Sales costs | (X) |

| Administrative expenses | (X) |

| other expenses | (X) |

| Profit before taxes | X |

As we can see, it is this form of analysis that is used by Russian companies when reflecting expenses in the income statement. IAS 1 paragraph 103 describes this method as providing users with more relevant information than classifying expenses by nature. However, its use may require arbitrary allocation and significant professional judgment.

O.V. Davydova

Journal expert

"Trade:

Accounting

and taxation"