Off-balance sheet account 09 in budget accounting

Spare parts accounting often raises questions among users of 1C programs. In this article I will describe an example of reflection in 1C: Accounting of a government agency 8th edition. 1.0 purchasing a spare part, installing it on a vehicle and deregistering it as a result of failure.

According to clause 349 of Instruction No. 157n, off-balance sheet account 09 “Spare parts for vehicles issued in replacement of worn-out ones” takes into account material assets issued for vehicles in replacement of worn-out ones (filters, batteries, tires, engines, etc.) for control purposes their use. The first document that we will enter in our example is “Purchase of materials”. You can read more about inventory accounting in the article Procedure for filling out materials accounting documents in “1C: Accounting of a government institution, 8th ed. 1.0"

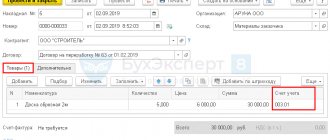

First, the spare part is registered on account 105.00 and remains there until it is installed on the vehicle. At the time of installation of this spare part on the vehicle, it is necessary to enter the document “Write-off of materials” with the type of operation “Write-off of spare parts for vehicles (receipt to off-balance sheet account 09)”.

When installing spare parts, we assign them to account 09 (spare parts for vehicles issued to replace worn-out ones), and they remain there until they fail and are written off from the register.

When writing off, we indicate the vehicle on which the spare part is installed.

Postings generated by the document “Write-off of materials”:

After this spare part on the vehicle fails, it will need to be written off from account 09. To do this, create a document “Write-off of materials (off-balance sheet accounting)”, located in the menu “Material inventories” - “Materials on off-balance sheet accounts”.

After posting this document, a credit entry for account 09 was generated.

The wiring was formed one-sided, because 09 account is off-balance sheet. According to clause 349 of Instruction No. 157n, the write-off of material assets from off-balance sheet account 09 is carried out on the basis of an acceptance certificate for completed work, confirming their replacement. Therefore, as a printed form for the document “Write-off of materials (off-balance sheet accounting)”, you can generate a Certificate (f. 0504833).

If you need more information about working in 1C: BGU 8, then you can get our collection of articles for free using the link.

Author of the article: Natalya Stakhneva

Consultant on 1C programs for government agencies

Did you like the article? Subscribe to the newsletter for new materials

When is it impossible to transfer property from off-balance sheet accounts 03 and 07?

The answer is obvious - when it does not satisfy at least one of the conditions listed above.

Let's take a closer look at examples.

Example 1. In the accounting of the institution, fuel cards are taken into account in off-balance sheet account 03 in accordance with the provisions of the accounting policy. There is no need to transfer them from off-balance sheet account 03 to the balance sheet as part of material inventories. The fact is that fuel cards, as a rule, are the property of the company that issued them. Accordingly, they do not satisfy the concept of an asset.

More on the topic: Budget (accounting) reporting for the 1st half of 2018: recommendations from the Ministry of Finance of Russia and the Federal Treasury for preparation

Example 2. In the accounting of the institution on off-balance sheet account 07, certificates acquired in 2014-2015 are taken into account. The institution does not have a warehouse. The certificates are kept by the employees responsible for issuing them. In this case, there is no need to transfer certificates from off-balance sheet account 07 to balance sheet account 105 06.

General accounting procedure for off-balance sheet accounts

The list of standard off-balance sheet accounts was approved by Order of the Ministry of Finance of Russia dated December 1, 2010 No. 157n: numbered from 1 to 27, as well as 29, 30, 31, 40 and 42.

A simple accounting scheme is applied to all off-balance sheet accounts, that is, income is reflected only as a debit, and expenses - as a credit, without correspondence.

Data on off-balance sheet accounts does not have to be reflected in the journals of transactions and in the General Ledger.

All material assets, as well as other assets and liabilities recorded on off-balance sheet accounts, are inventoried in the manner and within the time limits established for objects recorded on the balance sheet.

Acceptance of tires for registration by state employees

Tires are usually delivered separately or together with the vehicle. Their accounting in the first and second cases will be different. The fact of their receipt by state employees is directly confirmed:

- advance report (form according to OKUD 0504505, introduced by Order of the Ministry of Finance of the Russian Federation No. 52n dated March 30, 2015, as amended in 2021);

- receipt order (form according to OKUD 0504207, also maintained by Order of the Ministry of Finance of the Russian Federation No. 52n);

- supplier's shipping documentation.

Important! Tires received along with the vehicle (hereinafter abbreviated as “TS”) are not subject to separate accounting.

| Accounting for admission separately from the vehicle | Accounting together with the vehicle | Basic transactions (regarding the accounting of tires for public sector employees) |

| Tires are taken into account among material inventories, using an account. 0 105 06 000 “Other mat. stocks." Moreover, accounting is carried out at their actual price, formed using an account. 0 106 04 000 | Tires are displayed as part of transport (as an OS object) using an account. 0 101 05 000 "TS" | Acceptance of tires for registration: DT 0 105 36 340 CT 0 106 34 340 (at actual price). DT 0 105 36 340 CT 0 302 34 730 0 208 34 660 (at the purchase price, if there are no other expenses) |

State employees conduct accounting using the norms of two Instructions for the use of the chart of accounts, approved by Order of the Ministry of Finance of the Russian Federation No. 174n dated December 16, 2010 (as amended in 2021) and Order No. 157n dated December 1, 2010 (as amended in 2017).

Property accounting

Property is accounted for in 14 off-balance sheet accounts: 01, 02, 05, 06, 07, 09, 12, 13, 21, 22, 24, 25, 26, 27:

- Account 01 “Property received for use.” The account takes into account property received by the institution for use, but these are not rental objects. These are values that, in accordance with the legislation of the Russian Federation, are not subject to reflection on the balance sheet of the institution: museum objects and museum collections included in the state part of the Museum Fund of the Russian Federation, non-exclusive rights to use the results of intellectual activity, rights to limited use of other people's land plots. Property is registered on the basis of an acceptance certificate or other document that confirms receipt of the property and rights to it. Property must be reflected at the cost indicated in the transfer and acceptance certificate. Accounting is carried out in the context of property objects, owners (balance holders) of property, as well as by inventory, serial, register numbers specified in the transfer and acceptance certificate or other document.

- Account 02 “Material assets accepted for storage.” It is here that it is now necessary to take into account the material assets of the institution that do not meet the criteria of assets, as well as property in respect of which a decision has been made to be written off until it is dismantled, disposed of, or destroyed. Material assets accepted by an institution for storage and processing are accounted for on the basis of a primary document that confirms their receipt: an acceptance certificate, a contract, etc. Objects are reflected at the cost indicated in the primary document. If the institution executed the deed unilaterally - according to the conditional valuation: one object - 1 ruble. The disposal of MC from off-balance sheet accounting is reflected on the basis of supporting documents at the cost at which they were accepted for off-balance sheet accounting.

Accounting for car batteries and tires before disposal

And when they are subsequently replaced with new spare parts or when a car with installed spare parts is written off, it is reduced.

Therefore, as a printed form for the document “Write-off of materials (off-balance sheet accounting)”, you can generate a Certificate (f. 0504833). If you need more information about working in 1C: BGU 8, then you can get our collection of articles for free.

Keep analytical accounting for account 09 in the quantitative and total accounting card (f.

0504041). On account 09, take into account spare parts during the entire period of their operation (use) as part of the vehicle. Write off spare parts from off-balance sheet accounting based on the acceptance certificate for repaired, reconstructed and modernized fixed assets (f. 0504103), which confirms their replacement.

This is stated in paragraph 349 of the Instructions to the Unified Chart of Accounts No. 157n and the Methodological Instructions approved by order of the Ministry of Finance of Russia dated March 30, 2015.

No. 52n. From the situation How to take into account property that needs to be dismantled or disposed of Property that the institution’s commission decided to write off, dismantle or dispose of should be recorded in off-balance sheet account 02 “Tangible assets accepted for storage.”

Accounting on account 09 “Spare parts for vehicles issued to replace worn-out ones”

Analytical accounting of the account is kept in the Card of quantitative and total accounting in the context of persons who received material assets, indicating their position, surname, first name, patronymic (personnel number), vehicles, by type of material assets (indicating production numbers, if any) and their quantity.

2. Situation: What documents need to be drawn up when receiving car tires and putting them into operation. Tires purchased separately from the vehicle. Vehicle tires are included in other inventories (). Therefore, the rules for registering transactions related to their receipt and commissioning are similar to the general procedure for registering incoming and written-off inventories.

However, there is one peculiarity.

If tires are included in, at the time they are written off from the tire, you need to reflect on

“Spare parts for vehicles issued to replace worn-out ones”

().

Accounting for strict reporting forms, vouchers, periodicals

The listed assets are recorded in off-balance sheet accounts: 03, 08, 23.

- Account 03 “Strict reporting forms”. The list of SSBs and the procedure for their evaluation (according to a conditional valuation - 1 ruble per form or acquisition cost) is established in the accounting policy. Records are kept in the book of strict reporting forms for each type of form, broken down by responsible persons and storage locations. Forms are written off on the basis of an acceptance certificate or a write-off act in cases of issuance of BSO, transfer to another organization or damage, theft, shortage.

- Account 08 “Unpaid vouchers.” Vouchers are accepted for accounting when stored at the cash desk at the nominal value indicated on the voucher form or in the conditional valuation in the absence of a nominal value. Accounting is carried out in a quantitative and total accounting card for responsible persons, storage locations, types of vouchers and cost.

- Account 23 “Periodicals for use.” Acceptance for accounting is carried out on a conditional basis. Analytical accounting is maintained in a quantitative accounting card for each periodical. Write-off of accounting objects is carried out by decision of the commission on the basis of an act.

Example 2. Writing off damaged tires that are unsuitable for further use

By decision of the commission, the budgetary institution wrote off 4 pieces. tires with a total cost of 5,000 rubles, after which they were sent for recycling. Until the moment of disposal they are accepted for disposal. sch. 02 (conditionally: 1 piece - 1 rub.). The written-off parts were capitalized at an estimated price of 1,000 rubles. (as determined by the commission).

| Postings for writing off unusable tires | the name of the operation | Amount (rub.) |

| CT scan. sch. 09 | Write-off from account sch. | 5 000 |

| DT ob. sch. 02 | Acceptance for registration before scrapping | 4 |

| CT scan. sch. 02 | Write-off from account accounting | 4 |

| DT 2 105 36 340 CT 2 401 10 189 | Posting | 1000 |

| DT 2 401 10 172 CT 2 105 36 440 | Scrapping | 1000 |

| DT 2 209 89 560 CT 2 401 10 172 | Profit from disposal | 1000 |

Accounting for money, settlements and settlement documents

Money, settlements and settlement documents are taken into account from the 14th to the 19th and on the 30th off-balance sheet accounts.

- Account 14 “Settlement documents awaiting execution” and account 15 “Settlement documents not paid on time due to lack of funds in the account of a state (municipal) institution).” Accounting for settlement documents is maintained in the accounting card for settlement documents awaiting execution, broken down by accounts for each document.

- Account 16 “Overpayments of pensions and benefits due to incorrect application of legislation on pensions and benefits, accounting errors.” Keep records in the Funds and Settlements Accounting Card. Registration is carried out on the basis of audit reports, inspections and other similar documents. In account 16, the amounts of overpaid benefits continue to be recorded until they are fully repaid or written off. If repayment or collection occurs over a period of several months, amounts held off balance may also be written off gradually.

- Account 17 “Cash receipts” and account 18 “Cash outflows”. Accounts must be opened for balance sheet accounts: 201.00 “Cash of the institution”, 210.03 “Settlements with the financial authority for cash” and 304.06 “Settlements with other creditors” (in terms of cash settlements). Accounting is carried out in a multi-graph card or a card for recording funds and settlements in the context of institution accounts, by type of disposals and receipts (in the context of KOSGU). At the end of the year, account balances are not carried over to the next year. Thus, accounts 17 and 18 must be closed as of December 31 of the reporting year.

- Account 19 “Unexplained receipts from previous years.” Accounting is carried out according to the dates of crediting of uncleared receipts and the dates of their clarification.

- Account 30 “Settlements for the fulfillment of monetary obligations through third parties.” Analytical accounting of the account is maintained in a multigraph card and (or) in a card for accounting for funds and settlements in the context of monetary obligations by type of payment of budget funds or other types of payments.

Accounting for receivables and payables

To account for receivables and payables on the off-balance sheet, two accounts are provided: account 04 “Debt of insolvent debtors” and account 20 “Debt unclaimed by creditors”.

Debt is reflected in accounting at the moment when the commission for the receipt and disposal of assets makes a decision to write it off from the balance sheet.

Debt accounting is maintained in the card for accounting for funds and settlements:

- by type of revenue and debtor for accounts receivable;

- by types of payments and receipts and by creditors for accounts payable.

From account 04, the debt is written off by decision of the commission (in the event of death or liquidation of the debtor), when the debt collection procedure is resumed, or if money has been deposited into the account to repay the debt.

Accounting for guarantees

Accounting for guarantees is carried out on accounts 10 and 11.

- Account 10 “Ensuring the fulfillment of obligations.” Collaterals are accepted for accounting according to source documents in the amount of the obligation for which the collateral was received. Accounting is kept in a multigraph card in the context of obligations by type of property (collateral), its quantity, storage locations and obligations for which the property was received as security. The collateral is written off if obligations are fulfilled.

- Account 11 “State municipal guarantees”. Accounting is kept in the card for accounting funds and settlements in the context of subjects of civil rights and obligations for which guarantees are provided, by type and amount of guarantee. Collateral amounts are debited from the account when the obligations in respect of which the guarantee was provided are fulfilled.

Accounting for financial investments

- Account 31 “Shares at par value”. Accounting is maintained by a body with the powers of a shareholder or another authorized body. Shares are placed on off-balance sheet accounting simultaneously with their reflection in account 204.30 “Shares and other forms of participation in capital.” Accounting is maintained in the securities register.

- Account 40 “Assets in management companies.” The off-balance sheet takes into account assets that are listed in account 204.51 “Assets in management companies.” The value of the property is adjusted at the reporting date. Accounting is carried out by groups and types of non-financial and financial assets.

- Account 42 “Budget investments implemented by organizations.” Acceptance for accounting occurs based on data on the transfer of funds or transfer of assets. Investments are written off from the balance sheet upon completion of work and commissioning of capital construction projects. Analytical accounting of the account is carried out by recipients of funds.

Additional off-balance sheet accounts

The Ministry of Finance reserved for budgetary institutions the right to introduce additional off-balance sheet accounts necessary for collecting information and monitoring property. To do this, it is enough to fix the accounting procedure for off-balance sheet accounts in the accounting policy. But it should be noted that the numbering of additional off-balance sheet accounts should not conflict with the numbering of accounts assigned by the Ministry of Finance. To do this, it is best to assign a three-digit or letter code to additional off-balance sheet accounts (for example, 100, 101, TR, etc.).

The procedure for reflecting vehicles on off-balance sheet account 09

If an institution that has one passenger car on its balance sheet has nine nameless tires and one battery without a brand name on its account, it can be assumed that the account is not kept at all, since it does not allow one to check whether a replacement has occurred. In accordance with clause 349 of Instruction No. 157n, the list of types of components that are subject to reflection on the account must be approved by the institution as part of its accounting policy (unless this is determined by industry or territorial accounting standards). It should be noted that the description of this account in Instruction No. 157n (as well as in the previous budget accounting instructions) does not accurately reflect its meaning and contains a number of logical inaccuracies: The description only talks about spare parts issued to replace worn-out ones, i.e. about the second set and subsequent ones.

However, it is important to monitor easily removable components from the very moment the car arrives at the institution.