Types of postings for salaries and taxes

The total employee payroll for the month is displayed on the last day of that month. At the same time, the amounts for calculated tax (personal income tax) and accrued insurance premiums are formed.

In some cases, accrual occurs at other times. We are talking about payments when granting vacation, upon dismissal of an employee and other settlement cases.

Wages are generated using account 70. Accounting is kept separately for each employee. The cost account is determined depending on the employee’s employment in one of the structural divisions, on the specifics of the organization, for example:

- Dt 20 Kt 70 - wages accrued to employees of the main production;

- Dt 26 Kt 70 - salary of the management staff;

- Dt 44 Kt 70 - wages for employees of a trading enterprise.

The formation of wages and other payments is accompanied by the withholding of personal income tax and the calculation of insurance premiums. Income tax is withheld from the calculated amounts to employees, while the responsibility for transferring personal income tax falls on organizations as tax agents. Insurance premiums are calculated entirely at the expense of the employer.

To generate income tax data, a subaccount 68.1 is opened for account 68. When making records of insurance deductions, the following subaccounts are used:

- 69.1 - contributions to the Social Insurance Fund;

- 69.2 - insurance contributions to the Pension Fund;

- 69.3 - amounts in the Federal Compulsory Medical Insurance Fund;

- 69.11—accruals to the Social Insurance Fund for injuries.

Transactions on tax withholding and assessment of contributions are reflected in the following transactions:

- Dt 70 Kt 68.1 - personal income tax is withheld from accrued earnings;

- Dt 20 (23, 25, 26, 44) Kt 69 - insurance premiums have been charged.

Where can a tax creditor come from?

The reason for the appearance of tax payables is, for example, the actions of an accountant that were not brought to their logical conclusion and the “luck” of the company.

As for the first, the following situation may happen. The accountant discovered errors when calculating taxes and independently assessed them. But he didn’t pay taxes or penalties and didn’t submit updated declarations.

As for luck, we can talk about it in the case when the inspection did not come with checks for the period of additional assessment, and the statute of limitations applied for tax audits has expired.

If these circumstances occur, tax payables can be written off. But first you need to weigh the pros and cons.

When writing off a tax creditor, you need to be on the safe side

In general, non-operating income is recognized as income in the form of amounts of accounts payable written off, in particular, due to the expiration of the limitation period (clause 18 of Article 250 of the Tax Code of the Russian Federation).

The exception is the amount of accounts payable of the taxpayer for the payment of taxes and fees, penalties and fines to budgets of different levels, for the payment of contributions, penalties and fines to the budgets of state extra-budgetary funds, written off and (or) reduced otherwise in accordance with the legislation of the Russian Federation (subclause 21 Clause 1 of Article 251 of the Tax Code of the Russian Federation).

How can you use the general rule for writing off a creditor if it is a tax creditor?

In general, this cannot be done without contacting the tax office.

To make sure that the inspection did not write off your creditor and does not expect any payments from you (and in fact it did not come with the inspection and did not issue a payment request), order a statement of reconciliation of payments. If there are no arrears in it, then the debt that is on your balance sheet can be written off in the reporting period.

The written-off creditor will need to be reflected in non-operating income for income tax.

If you go the other way and admit that you mistakenly did not file updated tax returns in previous tax periods and file them, having previously transferred the tax arrears and penalties to the budget, you will have to submit an update to the tax office.

And this will entail verification of this updated declaration. Because there is an exception to the rules on the three-year time limit for conducting an on-site tax audit. If a taxpayer submits an updated tax return for a period beyond 3 years preceding the year in which the updated tax return was submitted, a tax audit may be scheduled.

Typical payroll entries

In addition to the withholding tax, other withholdings may be necessary when calculating wages. For example, for loans:

This includes amounts for alimony and compensation for damage caused. Deductions are made after taxation of earnings:

- Dt 70 Kt 76 - amounts on writs of execution are withheld;

- Dt 70 Kt 73 - reflects other deductions from the employee’s income.

If the employee was on sick leave, the employer should calculate payments for the period of illness upon presentation of a certificate of incapacity for work. Based on the results of calculations, the following transactions can be generated:

- Dt 20 (23, 25, 26, 44) Kt 70 - sick pay is accrued at the expense of the employing organization;

- Dt 20 (23, 25, 26, 44) Kt 69.1 - sick leave at the expense of the Social Insurance Fund.

How to account for tax penalties

Penalties are not tax sanctions, and therefore we will consider their accounting separately.

A penalty is an amount of money that a company (IP) must pay to the budget if taxes (contributions, fees) are not paid on time (Article 75 of the Tax Code of the Russian Federation).

Penalties are accrued for each calendar day of delay in fulfilling the obligation to pay a tax or fee, starting from the day following the day of payment of the tax or fee established by law. If the tax payment deadline falls on January 25, then penalties must be accrued from January 26.

The penalty for each day of delay is determined as a percentage of the debt. The interest rate of the penalty is 1/300 of the current refinancing rate. The refinancing rate is equal to the key rate; as of March 1, 2017, it is equal to 10% (Information of the Central Bank of the Russian Federation dated September 16, 2016).

Penalties = Amount of tax not paid on time x Number of calendar days of delay x 1/300 of the refinancing rate.

From October 1, 2017, penalties will be calculated based on 1/150 of the refinancing rate if the delay in payment exceeds 30 days (Federal Law of November 30, 2016 No. 401-FZ).

In practice, penalties are taken into account in different ways: some experts attribute tax penalties to account 91, while others - to account 99. Not a single regulatory act gives a clear answer on which account penalties should be taken into account. The decision must be made independently and consolidated in the accounting policy of the enterprise.

Option No. 1. Penalties are taken into account on account 91

If you read the definition of penalties, you can conclude: penalties do not relate to tax sanctions, and therefore cannot be taken into account on account 99. The characteristics of account 99 are presented in the chart of accounts and literally read as follows: “account 99 reflects the amounts of accrued conditional expenses for income tax, permanent liabilities and payments for recalculation of this tax from actual profit, as well as the amount of tax penalties due.” There is no talk of penalties here.

Since penalties are not taken into account for tax purposes (clause 2 of Article 270 of the Tax Code of the Russian Federation), only account 91-2 remains for their accounting. However, the chart of accounts explains that under account 91 only penalties for violation of contractual terms can be taken into account. The list of expenses is disclosed in PBU 10/99, and among those listed there are also no tax penalties. But in PBU 10/99 there is an article “other expenses”, and penalties can be attributed to it. The main thing is to fix the reflection of penalties on account 91 in the accounting policy of the organization.

Taking into account the penalties on account 91, a permanent tax liability will have to be accrued (PBU 18/02).

The accountant made the following entries:

Option No. 2. Penalties are taken into account on account 99

It is much more convenient to take into account penalties on account 99. Then the accountant will not have to accrue PNO.

In the instructions for using the chart of accounts, neither account 91 nor account 99 is directly suitable for accounting for penalties. However, in its economic content, the concept of penalties is very close to tax sanctions that must be taken into account in account 99. Transactions in accounting must be reflected based on their economic content , which takes precedence over the legal status of the operation (clause 6 of PBU 1/2008).

Example. received a request to pay interest on income tax in the amount of 421 rubles. The organization records penalties on account 99.

The accountant made the following entries:

Regardless of the chosen option for reflecting penalties, you must remember that penalties do not reduce profits for tax purposes. In the financial statements, penalties are reflected depending on the selected accounting account. Ultimately, the net profit will be the same for any option for accounting for penalties. If the amount of penalties is significant, it is advisable to disclose information about it in an explanatory note.

Penalties on the first payment are calculated for 64 days (from January 26, 2017 to March 30, 2017).

Penalties for the second payment are calculated for 31 days (from 02/28/2017 to 03/30/2017).

Penalties for the third payment are calculated for 3 days (from 03/28/2017 to 03/30/2017).

You can calculate penalties online using a calculator.

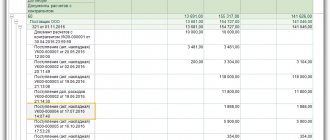

Example of accounting entries for wages

Let’s assume that employee K.V. Ivanov received a salary for September in the amount of 36,000 rubles. In addition, he has a writ of execution for the payment of alimony. Withholding percentage is 25% after tax.

What amounts for wages and contributions will be accrued, withheld, as well as postings for wages and taxes are presented in the table:

| Sch Dt | Sch Kt | the name of the operation | Amount, rub. | A document base |

| 26 | 70 | Salary accrued | 36 000 | Salary calculation |

| 70 | 68.1 | Personal income tax withheld | 4 680 | Salary calculation |

| 70 | 76 | The amount under the writ of execution was withheld | 7 830 | Salary calculation |

| 26 | 69.1 | Contributions to the Social Insurance Fund have been accrued | 1 044 | Salary calculation |

| 26 | 69.2 | Pension Fund contributions | 7 920 | Salary calculation |

| 26 | 69.3 | Contributions to the FFOMS | 1 836 | Salary calculation |

| 26 | 69.11 | Insurance premiums for injuries to the Social Insurance Fund | 72 | Salary calculation |

| 70 | 50 | Salary issued through the cash register after deductions | 23 490 | Payroll |

| 68.1 | 51 | Personal income tax listed | 4 680 | Payment order |

| 76 | 51 | Alimony payments listed | 7 830 | Payment order |

| 69.1 | 51 | Contributions to the Social Insurance Fund have been paid | 1 044 | Payment order |

| 69.2 | 51 | Pension Fund contributions | 7 920 | Payment order |

| 69.3 | 51 | Contributions to the FFOMS | 1 836 | Payment order |

| 69.11 | 51 | Contributions for injuries | 72 | Payment order |

Basics of accounting for insurance premiums and posting them

Peculiarities of reflecting tax penalties in accounting To display penalties in accounting, you can use two accounts - 91 or 99. To display accrued penalties, it is recommended to use account 99, which allows you to avoid a permanent tax liability, since when generating an income tax return, the accrued penalty for insurance contributions are not included in the calculation of the tax base. It is recommended to consolidate the use of account 99 in the accounting policy of the enterprise. List of possible entries for accrual of penalties for income taxes, VAT, personal income tax and insurance contributions Account Dt Account Kt Posting amount, rub.

Property tax

If the law “On Enterprise Property Tax” directly stipulated that the tax relates to the financial results of the organization, then the Tax Code does not contain any indication in this regard.

Where should property tax be attributed this year—still to financial results or can it be included in the company’s expenses? Tax officials recommend applying the previous procedure (see UNP No. 18, 2004, p. 6). Property tax is considered a non-operating expense.

Example 1.