Features of bills of exchange as securities

Being an unconditional debt document, a bill of exchange can be:

- Simple, i.e. drawn up between two persons and having the nature of a promissory note of the direct debtor;

- Transferable – a document, the preparation of which takes place with the participation of a third party (used to formalize the transfer of receivables).

Both a simple and a bill of exchange can be:

- Someone else's or your own;

- Discount – interest rate, i.e. providing for an interest rate at which interest will be calculated on the amount of the bill, or interest-free.

Both types of bills of exchange can be commodity, i.e., confirm the debt under a contract for the supply of goods and materials, or financial. In this case, the subject of the transaction is the bill itself. The difference in the purpose of using bills of exchange affects the accounting accounts that will be used to account for bills of exchange.

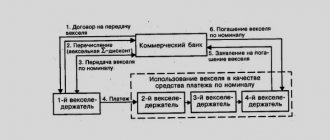

What should we consider when we buy bank bills?

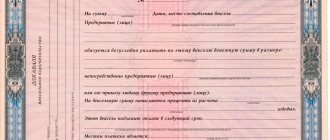

A bank bill, like all forms and types of credit, must necessarily contain the necessary details:

- bill of exchange mark (information that confirms that this document is a bill of exchange);

- a clearly defined amount and an obligation to pay it;

- maturity date (at presentation, a specifically established date, after a certain period from the date of presentation, after a time from the date of sale);

- place of payment (in the case where the debtor is a bank, its address is indicated);

- name and address of the parties. With a promissory note, the payer is not specified; by default, it is the bank. When transferring, this data must be indicated;

- date and place of compilation;

- signature of the director, chief accountant and seal of the bank that is the drawer.

Accounting for bills of exchange: postings

Often, a promissory note in a buyer-seller relationship plays the role of a promissory note, since it arises in a situation where the buyer cannot pay for the goods with available funds, and the seller agrees to accept the bill. Such a commodity bill is not considered a security until it is transferred to a third party. To account for such bills, the buyer has an account. 60 open a subaccount 60/3 “Bills issued”, and the seller opens a subaccount 62/3 “Bills received”.

Transactions with it are recorded on both sides in the settlement accounts by postings:

| Operation | D/t | K/t |

| Accounting entries for bills issued | ||

| Reflected delivery debt | 60/1 | 60/3 |

| Security for future payment issued (behind balance) | 009 | |

| If the bill is interest-bearing, then the buyer’s debt will increase by the amount of accrued interest | 91 | 60/3 |

| Repayment of a debt | 60/3 | 51 |

| Writing off the bill after payment | 009 | |

| Accounting entries for bills received | ||

| The debt on the shipped goods is reflected | 62/ 3 | 62/1 |

| Payment security received | 008 | |

| Interest income from the bill | 62/3 | 91 |

| Received payment for goods secured by a bill of exchange | 51 | 62/3 |

| Writing off a bill after receiving payment | 008 | |

Example 1

Blitz LLC, to secure payment obligations under the supply agreement, Atrium LLC issued a promissory note in the amount of RUB 236,000. including VAT RUB 36,000. The accounting records of both organizations will reflect:

Operation D/t K/t Sum At Blitz LLC Debt to supplier for goods 41 60/1 200 000 VAT 19 60/1 36 000 A bill of exchange was issued 60/1 60/3 236 000 The bill is included in the balance sheet 009 236 000 Amortization 60/3 51 236 000 Writing off a bill 009 236 000 At Atrium LLC Revenue reflected 62/1 90/1 236 000 VAT charged 90/3 68 36 000 The cost of goods is written off 90/2 41 100 000 Bill received 62/3 62/1 236 000 The bill is included in the balance sheet 008 Payment for goods and materials received 51 62/3 236 000 Writing off a bill 008 236 000

Bill as loan posting

The procedure for accounting for such bills is established by the Accounting Regulations “Accounting for Loans and Credits and the Costs of Servicing Them” (PBU 15/01), approved by Order of the Ministry of Finance of Russia dated June 2, 2001 No. 60n.

Thus, paragraph 18 of PBU 15/01 defines the procedure for accounting for interest and discount on a bill of exchange from the borrowing organization. Suppose an organization issues a bill of exchange as security for a loan agreement.

The amount indicated in the bill is reflected as accounts payable, that is, on the credit of account 66 or 67, depending on the maturity of the bill.

When issuing a bill of exchange to obtain a loan in cash, the amount of interest due is reflected by the drawer as part of operating expenses. example: On February 1, 2001, Karusel LLC received a loan in the amount of 100,000 rubles from Perevertysh JSC. for a period of 6 months to replenish working capital.

Accounting for the organization that received the bill from the bill holder by endorsement In the accounting of OJSC Rostock, the transactions for the acquisition and presentation for redemption of a financial bill are as follows: DEBIT 58-2 “Debt securities” CREDIT 76-30,000 rubles.

— the purchased financial bill was capitalized; DEBIT 76 CREDIT 51-30,000 rub. - funds were transferred to pay for the financial bill; DEBIT 76 CREDIT 91-1 “Other income” - 30,000 rubles. Issuance of a loan by bills of exchange During the term of the loan agreement, the amount of debt in accounting does not change.

Interest on a loan issued under a bill of exchange is written off as expenses on a monthly basis. To do this, use accounting account 97. The operation is carried out by recording Debit 97 Credit 66 (67).

In taxation of profits and expenses, only that part of the discount on the bill of exchange that does not exceed that calculated based on the refinancing rate can be recognized as expenses.

What is a bill of exchange? reflected in accounting

- or the book value of the bill will not change (clause 21 of PBU 19/02) and will be taken into account at the time of its disposal, reflected in the financial result;

- or the increase in the book value to the par value will be done evenly during the circulation period of the bill (clause 22 of PBU 19/02):

Dt 58-2 Kt 91. Interest on a bill is accrued monthly, but they do not increase the accounting value of financial investments (clause

21 PBU 19/02) and therefore are reflected in the settlement accounts: Dt 76 Kt 91. The amount of these interests will be included in the book value of the bill upon its disposal: Dt 91 Kt 76.

Loan agreement and bill of exchange as instruments for raising borrowed funds

Important

Payment on the bill will be reflected as the closure of the debt on it:

Dt 60veks Kt 51, where 60veks is a subaccount of the debt on the issued own bill;

Dt 51 Kt 62veks, where 62veks is a subaccount of the debt on the buyer’s own bill of exchange received. At the same time, the bills will be written off from off-balance sheet accounts:

Kt 009;

Kt 008. Read more about off-balance sheet accounts in the article “Rules for maintaining accounting records on off-balance sheet accounts.”

Accounting for other people's bills of exchange as part of financial investments The signs of financial investments correspond to bills purchased at a price below par or interest-bearing, i.e., capable of generating income (clause 2 of PBU 19/02, approved by order of the Ministry of Finance of Russia dated December 10, 2002 No. 126n).

The procedure for accounting for bills of exchange in accounting

6 months later, after presenting the bill of exchange for payment, the following entries were made in the accounting of Karusel LLC: DEBIT 62 CREDIT 90-1 “Revenue” - 24,000 rubles. — the buyer’s debt for shipped products is reflected; DEBIT 90-3 “VAT” CREDIT 76 subaccount “Calculations for unpaid VAT” - 4000 rubles.

— value added tax is charged on the cost of products sold; DEBIT 62 subaccount “Bills received” CREDIT 62 - 30,000 rubles. — reflects the amount of the bill received in payment for shipped products; DEBIT 62 CREDIT 90-1 “Revenue” - 6,000 rubles.

— the buyer’s debt has been accrued up to the amount specified in the bill. After the sale of the commercial bill of exchange of Rostok OJSC, the following entries need to be made in the Salyut accounting: DEBIT 76 CREDIT 91-1 “Other income” - 30,000 rubles.

— the debt of the buyer of the bill is reflected; DEBIT 91-2 “Other expenses” CREDIT 62 subaccount “Bills received” - 30,000 rubles.

Issuance of a loan by bills of exchange

Attention

When receiving funds, the following entries are made:

The interest reflected in the bill takes into account:

- according to debit 91.2 of account and credit 66 (67).

When reflecting transactions for the issuance of a bill of exchange, its amount is taken into account as part of accounts payable. If the bill is interest-bearing or non-interest-bearing, the accounts payable reflects the entire amount of the security. During the term of the loan agreement, the amount of debt in accounting does not change.

Interest on a loan issued under a bill of exchange is written off as expenses on a monthly basis. To do this, use accounting account 97. The operation is carried out by recording Debit 97 Credit 66 (67). In taxation of profits and expenses, only that part of the discount on the bill of exchange that does not exceed that calculated based on the refinancing rate can be recognized as expenses. Interest on the note is payable on the maturity date of the security.

Accounting for bills of exchange issued as security for a loan agreement

for the buyer: Dt 60calculation Kt 60veks, where: 60calculation is a subaccount for reflecting the debt for the supply, 60veks is a subaccount for the debt on the issued own bill of exchange;

Dt 62veks Kt 62calculation, where: 62veks is a subaccount of the debt on the buyer’s own bill of exchange received, 62calculation is a subaccount for reflecting the debt on shipment. At the same time, both parties show the appearance of such a bill on their balance sheet:

- buyer - as security issued:

Dt 009;

- supplier - as security received:

Dt 008. If the bill is interest-bearing, then income will be accrued on it monthly, increasing the amount of the buyer’s debt on the bill:

Dt 91 Kt 60veks, where 60veks is a subaccount of the debt on the issued own bill;

Dt 62veks Kt 91, where 62veks is a subaccount of the debt on the buyer’s own bill of exchange received.

Loan in the form of a bill of exchange

Features of accounting and taxation of bills The features of reflecting a bill of exchange in accounting are influenced by the fact that it can be:

- own or someone else's;

- simple (drawn up between 2 persons) or transferable (drawn up with the participation of a third party who will make the payment, repaying his debt to the drawer);

- discount (transferred at a price different from that indicated in it), interest (providing for the accrual of a certain percentage on the amount reflected in it) or interest-free (with a zero interest rate);

- a debt obligation, a means of payment, borrowing or investment.

It is extremely important for this document to comply with the requirements for the rules of execution and, in particular, to indicate in it (paragraph. The issue of the bill must be reflected in the debit of account 009. When it is repaid, an entry will need to be made on the loan. Income on the bill with the purchase price below its face value can be taken into account in one of two ways, the choice between which must be reflected in the accounting policy:

- or the book value of the bill will not change (clause

Accounting for bills of exchange issued as security for a loan agreement Important For example:

- when purchasing this security:

Dt 58-2 Kt 76;

- payment by the buyer for delivery by third party bill:

Dt 58-2 Kt 62;

- receiving it as a contribution to the management company:

Dt 58-2 Kt 75;

- property exchange transactions:

Dt 58-2 Kt 91, Dt 91 Kt 10 (01, 04, 41, 43, 58);

- free admission:

Dt 58-2 Kt 91. Since each debt security is individual, bills in accounting are reflected individually and the valuation upon disposal is made at the cost of each unit.

The procedure for accounting for such bills is established by the Accounting Regulations “Accounting for Loans and Credits and the Costs of Servicing Them” (PBU 15/01), approved by Order of the Ministry of Finance of Russia dated June 2, 2001 No. 60n.

Thus, paragraph 18 of PBU 15/01 defines the procedure for accounting for interest and discount on a bill of exchange from a borrowing organization. Let’s assume that an organization issues a bill of exchange as security for a loan agreement.

The amount indicated in the bill is reflected as accounts payable, that is, on the credit of account 66 or 67, depending on the maturity of the bill.

When issuing a bill of exchange to obtain a loan in cash, the amount of interest due is reflected by the drawer as part of operating expenses. Example LLC "Karusel" on February 1, 2001 received a loan in the amount of 100,000 rubles from JSC "Perevertysh". for a period of 6 months to replenish working capital.

Source: https://juristufa.ru/2018/04/21/veksel-v-kachestve-zajma-provodki/

Bills of exchange in accounting as financial investments

If an enterprise, having free money, invests it in the purchase of bills issued by banks and capable of generating income, then we are talking about financial investments. Such bills are the object of purchase and sale, they are recorded in subaccount 58/2 “Debt securities”. Let's figure out how bills of exchange are accounted for in accounting. Postings:

| Operation | D/t | K/t |

| Purchase of a bill of exchange | 76 (60) | 51 |

| Acceptance for registration | 58/2 | 76 (60) |

| The difference between the purchase price and the face value is reflected | 58/2 | 91/1 |

Example 2

On January 25, 2018, the company acquired a bank bill with a face value of RUB 2,000,000, issued on January 25, 2018, with a payment due date at sight, but not earlier than May 5, 2018. Interest accrual is 8% per annum. On 04/05/2018, the company executed a compensation agreement with the condition of transferring the bill of exchange to the counterparty who performed the work worth RUB 2,000,000. without VAT. It was accepted as payment for the work. The transaction was formalized by an agreement for the transfer of a promissory note.

Accounting entries:

Operation D/t K/t Sum 25.01.2018 Bill paid 76 51 2 000 000 The bill is included in financial investments 58/2 76 2 000 000 31.01.2018 Accrual of interest on the bill for January 2,000,000 x 8% / 365 x 6 days. 76 91/1 2630 28.02.2018 Interest accrued for February (2,000,000 x 8% / 365 x 28) 76 91/1 12 274 31.03.2018 Interest accrued for March (2,000,000 x 8% / 365 x 31) 76 91/1 13 589 05.04.2018 The work performed was accepted for accounting 20 60 2 000 000 Interest accrued for April (2,000,000 x 8% / 365 x 5) 76 91/1 2192 The contractor was given a bill of exchange to repay the mortgage 60 91/1 2 000 000 The nominal value of the bill has been written off 91/2 58/2 2 000 000

What is a bill of exchange

They gained great popularity in the nineties of the twentieth century.

Most organizations used them to increase capital and then stopped meeting their own obligations. Because of this factor, commitment is associated with something negative.

A bill of exchange is the same financial instrument as a security or a share. It is a debenture under which the holder is obligated to pay the owner a pre-agreed amount within a specified period of time.

Features of the bill

Its main features include:

- release on official letterhead with a unique number;

- produced in 1 copy;

- absolutely any denomination;

- cannot be transferred to other persons.

The main indicator is the face value, that is, the amount that will be paid after the end of the repayment period.

Formula used to calculate cost:

- P is the selling price;

- t is the circulation period;

- S is the rate that the holder will receive.

For example, take the following indicators:

- R – twenty thousand rubles;

- t – two hundred days;

- S – fifteen percent.

We substitute these values into the formula:

As a result, we get 21,643 rubles. This amount will be received by the holder by the end of the redemption period.

Organizations are able to use it in the form of:

- deposit instrument;

- currencies for settlement;

- bank guarantees when concluding transactions.

Types of bills

The following types exist:

- simple. The organization is obliged to pay the depositor the funds specified in the obligation upon expiration of the term.

- percentage. Similar to the Central Bank. It has a face value that is redeemable upon expiration of the obligation and additional interest income paid when the paper is redeemed.

- discount. It is sold at a value less than its face value, and after the end of the period it is redeemed at its face value.

- translated. The acquirer of the funds is not the buyer, but a third party.

Where can I buy and how to sell a bill of exchange?

You can buy them for yourself:

- in the bank;

- from a legal entity.

It is given to the investor after initial negotiations have been held to discuss the terms of the purchase.

Bills of exchange, unlike the Central Bank, are not issued on the organized market. It is impossible to purchase them using intermediaries. You can only buy from the issuer itself.

Central Banks are offered to a large number of investors. If we talk about bills, then there is a pre-agreed plan with the buyer. They can be purchased by both investors and banking companies, pension funds and so on. The conditions of each purchase are individual, but, most often, the interest rate is higher than in the Central Bank. The longer the repayment period, the more cash the investor will receive.

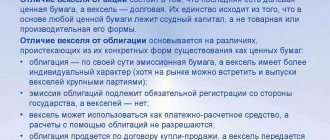

What is a bond

A security is a debt obligation. If it is issued by a legal entity, then the paper becomes corporate. If a country issues a central bank, then it becomes a federal loan central bank. Regions of the Russian Federation, as well as cities, have the opportunity to raise funds using this method. Such securities are called municipal securities.

Characteristics of a bond as an investment instrument

There are many differences between a security and a bill. A bill is a confirmed loan that is issued in person, while a security is a public debt.

Features of a security as a debt:

- production is carried out in large quantities;

- a country or company undertakes to redeem a security at par on a certain date;

- absolutely all parameters have the same indicators;

- The denomination of the paper is determined in advance;

- the price on the Central Bank is indicated during trading.

It is worth noting that the funds received during the placement of securities are included in the company's fixed capital. If the issuer goes bankrupt, then the holders of the securities will act as creditors and will be able to ask for compensation in the amount of the nominal value of the securities.

Types of bonds

According to the type of profit, Central Banks are divided into the following types:

- coupons. Here the company undertakes to pay funds to the investor in a fixed amount of the nominal amount;

- discount. Such securities do not have a coupon, but they are sold at a cost less than their face value.

Basically, investors purchase coupon securities to acquire stable profits.

These documents are divided according to the type of coupon:

- with a variable rate. The company has the opportunity to change the coupon size itself, based on economic indicators;

- with a constant rate. The fixed value of the coupon and the payment time are indicated here;

- with a floating rate. The size of the coupon depends on the refinanced rate or inflation indicators.

There are securities with depreciation - the issuer pays the face value step by step. This is used to prevent large debts during the redemption period. These securities are issued by medium-sized organizations, as well as municipalities.

Where is the bond purchased?

Trading of securities takes place on stock exchanges. It is impossible to simply reach an agreement with the issuer and purchase a security from him - this is how bills are purchased.

Bonds are purchased through a broker. The investor needs to open a brokerage account, deposit a certain amount into it, and then make purchases. The value of the Central Bank is formed during trading and depends on the currently available refinanced rate. A decline or rise in stock prices is usually triggered by sanctions or news.

Aspects of promissory note acquisition

When an enterprise decides to purchase a bill of exchange with its own funds, then the enterprise thus makes an investment of financial resources.

When a bill of exchange purchase operation is carried out, in order for the bill to become the property of the company, a special transfer and acceptance act or a purchase and sale agreement is drawn up. Thus, confirmation of the purchase of a bill of exchange is an act of acceptance and transfer or a purchase and sale agreement, the bill itself in paper form.

Accounting for such financial investments is carried out in accordance with the accounting policies of the enterprise. For this purpose, an accounting unit is selected. Typically, bills of exchange are taken into account one at a time.

In order to compile analytical accounting, the following criteria are used:

- name and title of the issuer, name of the security;

- number, series and other details of the bill;

- nominal price and purchase price;

- date of purchase and date of sale, in case of purchase from third parties;

- place of storage of the bill.

What is a bill of exchange

A bill, in simple terms, is a certain debt document distinguished by its value. It is the bill of exchange that gives the owner the right to demand from the debtor a certain amount noted in the bill of exchange, and to demand the return of the amount within a certain time frame, also specified in the document.

If we compare bills of exchange with other documents or with standard contracts, then we can note that the bill of exchange is in no way connected with loans or transactions. That is, the bill will only confirm that one party has a debt, as well as the right to take money from the other party.

Receipt of debt on a bill of exchange can be carried out at an ordinary banking institution, but it is important to choose the bank that has the account of the person who transferred the bill of exchange as a debt security.

After the bill expires, and this date can be found on the paper itself, the recipient party can appear at the bank demanding payment of the noted amount. It is worth considering that payments on bills of exchange in a bank can occur without the direct participation of the party that issued the bill. If the bill of exchange as a document is filled out correctly and with all the necessary data, the banking organization will be able to issue the required amount of funds.

simplified tax system

https://www.youtube.com/watch?v=https:tv.youtube.com

The issuance of your own bill of exchange does not affect the calculation of the single tax, regardless of what object of taxation the organization applies. For tax purposes, this operation is a guarantee of payment for purchased goods (works, services) with deferred payment. That is, when issuing your own bill of exchange, there is no payment for purchased goods (works, services) or repayment of other obligations. This follows from Articles 815 and 823 of the Civil Code of the Russian Federation and Article 346.17 of the Tax Code of the Russian Federation.

At the same time, to calculate the single tax, take into account the peculiarities of accounting for certain types of expenses when simplifying. For example, purchased goods for which a bill of exchange was received must not only be paid, but also sold (subclause 23, clause 1 and clause 2, article 346.16, subclause 2, clause 2, article 346.17 of the Tax Code of the Russian Federation).