What to show on account 71

Order of the Ministry of Finance of the Russian Federation No. 94n approved that account 71 “Settlements with accountable persons” is intended to reflect transactions for the issuance and return of accountable amounts.

What is a subreport? This is a certain amount of money from the organization that is transferred to the employee for specific purposes. Moreover, the purpose of expenses and the reporting period are strictly limited. After the allotted time has passed, the subordinate must provide a report on the expenses incurred. In simple words, money is given in advance, but with the condition that the employee provides a report - this is the essence of reporting.

For example, the company secretary was given 100 rubles from the cash register to buy an envelope and send a letter. When the reporting employee sends the letter, he will be given a receipt or check at the post office. It is these payment documents that the secretary will attach to the report, which will confirm the fact that the funds were spent on purpose.

For what purposes can a report be issued:

- Advance on travel expenses. This is relevant when an employee is sent on a business trip. Travel allowances include payment for accommodation and travel, daily allowances and other expenses en route.

- Expenses for the business needs of the company. Money can be issued for any purpose, from buying a light bulb for a utility room to building materials for major repairs.

- Settlements with counterparties. For example, the issuance of money is subject to payment for the services of third-party organizations. The operation is used less and less often, since non-cash payments are much more convenient.

- Other goals fixed by the decision of the company management. The director has the right to order the issuance of a report for any purpose. For example, for the purchase of equipment, exclusive rights, software products, etc.

IMPORTANT!

Loans and advances to employees cannot be reflected in account 71. For this purpose, a separate account is provided in accounting - 73. Some companies, wanting to simplify accounting and evade taxes, issue short-term loans to employees through 71 accounts. This is a violation.

Transactions that are reflected in accounting on account 71

Account 71 in the accounting department is intended to reflect the company's settlements with its accountables, i.e., with persons who received money on account from the company to pay for any of its needs.

Such expenses may include:

- procurement of goods and materials;

- payment for work or services;

- expenses associated with business trips.

Only persons working for the company under an employment contract or within the framework of the GPA can be accountable. The issuance of money on account can be carried out on an ongoing basis or on a one-time basis.

The list of employees who receive money regularly is approved in the order of the manager. It also indicates the period for which the employee is given the company's money. To receive money one-time, the employee must write an application indicating the amount and period for which it is required.

The employee who received the money, in accordance with clause 6.3 of the instructions of the Central Bank of the Russian Federation “On the procedure for conducting cash transactions” dated March 11, 2014 No. 3210-U, must report on expenses no later than 3 days:

- after the end of the period for which the money was issued;

- completion of a business trip;

- the end of the period of incapacity;

- coming out of vacation.

Accountable persons report by filling out an advance report. How to reflect in accounting the expenses of an accountable person and exchange rate differences on an advance report in foreign currency? The answer to this question can be found in a ready-made solution from ConsultantPlus experts. If you don't already have access to the system, get a free trial online.

Operations on account 71 “Settlements with accountable persons” are carried out in accordance with the requirements of the Chart of Accounts, approved by order of the Ministry of Finance of the Russian Federation dated October 30, 2000 No. 94n.

Rules for issuing money report

The organization is obliged to independently develop and approve the procedure for settlements with accountable persons. For example, by identifying uniform provisions in the annex to the accounting policies. The company calculates limits and standards on an individual basis.

Key requirements for conducting settlements with accountable persons:

- Money can only be given to an employee of the company. That is, accountable persons (account 71 is used only in this case) must be determined by a separate order of the manager.

- Funds can be transferred in cash from the cash register or by bank transfer. Which method will be used in settlements with accountable persons should be specified in the accounting policy.

- The maximum amount to be issued for reporting can be fixed by a separate order of management.

- It is recommended to approve the limits on travel expenses in the subsistence report separately.

- The deadline for submitting a report on accountable money is also fixed in the regulations or in the accounting policy.

- All settlements with accountable persons (account 71) must be documented. To do this, checks, invoices, tickets, receipts and other documentation are attached to the report.

Money is issued based on a written application from the employee or by order of management. The recipient is required to sign the cash receipt order if funds are issued in cash from the cash register. When making purchases or while on a business trip, the reporting employee must keep all receipts and checks in order to account for the advance received. Upon returning from a trip or upon completion of the purchase, the subordinate draws up an advance report. Supporting documents are attached to the report. The deadline for drawing up a report on accountable money is 3 days.

Account 71.01 “Settlements with accountable persons”

“Entering initial balances: settlements with accountable persons in rubles.”

ENTRY: Debit 000 “Subsidiary account” Credit 71.01 “Settlements with accountable persons”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: -

Entering initial balances

in the “Enterprise” menu, type of business transaction: “

Settlements with accountable persons (account 71)”

“Inclusion in the cost of equipment requiring installation, expenses of the accountable person in rubles.”

ENTRY: Debit 07 “Equipment for installation” Credit 71.01 “Settlements with accountable persons”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Advance report

in the “Cashier” menu

“Inclusion in the cost of the land plot of expenses of the accountable person in rubles.”

ENTRY: Debit 08.01 “Purchase of land” Credit 71.01 “Settlements with accountable persons”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Advance report

in the “Cashier” menu

“Inclusion in the cost of a natural resource management facility of the expenses of the accountable person in rubles.”

ENTRY: Debit 08.02 “Purchase of natural resources” Credit 71.01 “Settlements with accountable persons”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Advance report

in the “Cashier” menu

“Inclusion in the cost of the construction project of the expenses of the accountable person in rubles.”

ENTRY: Debit 08.03 “Construction of fixed assets” Credit 71.01 “Settlements with accountable persons”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Advance report

in the “Cashier” menu

“Inclusion in the cost of a non-current asset (equipment) of the expenses of an accountable person in rubles.”

ENTRY: Debit 08.04 “Purchase of fixed assets” Credit 71.01 “Settlements with accountable persons”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Advance report

in the “Cashier” menu

“Inclusion in the value of an intangible asset that has not been put into operation, the expenses of an accountable person in rubles.”

ENTRY: Debit 08.05 “Acquisition of intangible assets” Credit 71.01 “Settlements with accountable persons”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Advance report

in the “Cashier” menu

“Acceptance for accounting of raw materials and supplies received from an accountable entity in rubles.”

ENTRY: Debit 10.01 “Raw materials and supplies” Credit 71.01 “Settlements with accountable persons”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Advance report

in the “Cashier” menu

“Acceptance for accounting of purchased semi-finished products, components, structures and parts received from an accountable entity in rubles.”

ENTRY: Debit 10.02 “Purchased semi-finished products and components, structures and parts” Credit 71.01 “Settlements with accountable persons”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Advance report

in the “Cashier” menu

“Acceptance for accounting of fuel received from an accountable person in rubles.”

ENTRY: Debit 10.03 “Fuel” Credit 71.01 “Settlements with accountable persons”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Advance report

in the “Cashier” menu

“Acceptance for accounting of reusable collateral containers and packaging materials received from an accountable entity in rubles. in organizations engaged in production activities or provision of services"

ENTRY: Debit 10.04 “Containers and packaging materials” Credit 71.01 “Settlements with accountable persons”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Advance report

in the “Cashier” menu

“Acceptance for accounting of spare parts received from an accountable person in rubles.”

ENTRY: Debit 10.05 “Spare parts” Credit 71.01 “Settlements with accountable persons”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Advance report

in the “Cashier” menu

“Acceptance for accounting of other materials received from the accountable entity in rubles.”

ENTRY: Debit 10.06 “Other materials” Credit 71.01 “Settlements with accountable persons”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Advance report

in the “Cashier” menu

“Acceptance for accounting of construction materials received from an accountable entity in rubles.”

ENTRY: Debit 10.08 “Construction materials” Credit 71.01 “Settlements with accountable persons”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Advance report

in the “Cashier” menu

“Acceptance for accounting of inventory and household supplies received from an accountable person in rubles.”

ENTRY: Debit 10.09 “Inventory and household supplies” Credit 71.01 “Settlements with accountable persons”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Advance report

in the “Cashier” menu

“Acceptance for accounting of special equipment and special clothing received from an accountable person in rubles.”

ENTRY: Debit 10.10 “Special equipment and special clothing in warehouse” Credit 71.01 “Settlements with accountable persons”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Advance report

in the “Cashier” menu

“Inclusion in the costs of the main production of the amount of expenses incurred by the accountable person in rubles.”

ENTRY: Debit 20.01 “Main production” Credit 71.01 “Settlements with accountable persons”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Advance report

in the “Cashier” menu

“Inclusion in the costs of auxiliary production of the amount of expenses incurred by the accountable person in rubles.”

ENTRY: Debit 23 “Auxiliary production” Credit 71.01 “Settlements with accountable persons”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Advance report

in the “Cashier” menu

“Writing off as general production expenses the amount of expenses incurred by an accountable person in rubles.”

ENTRY: Debit 25 “General production expenses” Credit 71.01 “Settlements with accountable persons”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Advance report

in the “Cashier” menu

“Writing off as general business expenses the amount of expenses incurred by an accountable person in rubles.”

ENTRY: Debit 26 “General business expenses” Credit 71.01 “Settlements with accountable persons”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Advance report

in the “Cashier” menu

“Inclusion in the expenses of service industries and farms of the amount of expenses incurred by the accountable person in rubles.”

ENTRY: Debit 29 “Service production and facilities” Credit 71.01 “Settlements with accountable persons”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Advance report

in the “Cashier” menu

“Acceptance for accounting of goods received from an accountable person in rubles.”

ENTRY: Debit 41.01 “Goods in warehouses” Credit 71.01 “Settlements with accountable persons”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Advance report

in the “Cashier” menu

“Acceptance for accounting of goods at a retail outlet received from an accountable person in rubles. (retail, accounting at cost of acquisition)"

ENTRY: Debit 41.02 “Goods in retail trade (at purchase price)” Credit 71.01 “Settlements with accountable persons”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Advance report

in the “Cashier” menu

“Acceptance for accounting of purchased items received from an accountable person in rubles.”

ENTRY: Debit 41.04 “Purchased items” Credit 71.01 “Settlements with accountable persons”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Advance report

in the “Cashier” menu

“Writing off as distribution costs the amount of expenses incurred by an accountable person in rubles in organizations engaged in trading activities”

ENTRY: Debit 44.01 “Costs of distribution in organizations engaged in trading activities” Credit 71.01 “Settlements with accountable persons”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Advance report

in the “Cashier” menu

“Write-off of expenses incurred by an accountable person in rubles for business expenses in organizations engaged in industrial and other production activities”

ENTRY: Debit 44.02 “Business expenses in organizations engaged in industrial and other production activities” Credit 71.01 “Settlements with accountable persons”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Advance report

in the “Cashier” menu

“Receipt of cash to the organization’s cash desk from an accountable person in rubles. (return of unspent amounts previously issued on account)"

ENTRY: Debit 50.01 “Cash of the organization” Credit 71.01 “Settlements with accountable persons”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Receipt cash order

in the “Cash” menu, type of business transaction: “

Return by accountant”

“Receipt of cash to the operating cash desk from an accountable person in rubles. (return of unspent amounts previously issued on account)"

ENTRY: Debit 50.02 “Operating cash” Credit 71.01 “Settlements with accountable persons”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Receipt cash order

in the “Cash” menu, type of business transaction: “

Return by accountant”

“Receipt of funds to the organization’s current account from an accountable person in rubles. (return of unspent amounts previously transferred to the report)"

ENTRY: Debit 51 “Current accounts” Credit 71.01 “Settlements with accountable persons”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Receipt to the current account

in the “Bank” menu, type of business transaction: “

Other receipt”

“Deduction of unspent accountable amounts in rubles from the employee’s salary.”

ENTRY: Debit 70 “Settlements with personnel for wages” Credit 71.01 “Settlements with accountable persons”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Operation (accounting and tax accounting)

in the menu “Operations — Operations entered manually”

“Issuance of cash from the organization’s cash desk to an accountable person in rubles.”

ENTRY: Debit 71.01 “Settlements with accountable persons” Credit 50.01 “Cash of the organization”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Cash order

in the “Cash” menu, type of business transaction: “

Issuance to an accountable person”

“Issuance of cash from the operating cash desk to an accountable person in rubles.”

ENTRY: Debit 71.01 “Settlements with accountable persons” Credit 50.02 “Operating cash”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Cash order

in the “Cash” menu, type of business transaction: “

Issuance to an accountable person”

“Transfer of funds from the organization’s current account to an accountable person in rubles.”

ENTRY: Debit 71.01 “Settlements with accountable persons” Credit 51 “Settlement accounts”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Debiting from a current account

in the “Bank” menu, type of business transaction: “

Transfer to accountant”

“Reflection of the debt of the accountable person for unspent amounts previously transferred to the report”

ENTRY: Debit 73.03 “Settlements for other transactions” Credit 71.01 “Settlements with accountable persons”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Operation (accounting and tax accounting)

in the menu “Operations — Operations entered manually”

“Inclusion in other expenses not related to the main activities of the expenses of the accountable person in rubles.”

ENTRY: Debit 91.02 “Other expenses” Credit 71.01 “Settlements with accountable persons”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Advance report

in the “Cashier” menu

“Inclusion in future expenses of expenses of an accountable person in rubles.”

ENTRY: Debit 97.21 “Other deferred expenses” Credit 71.01 “Settlements with accountable persons”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Advance report

in the “Cashier” menu

“Receipt of monetary documents to the organization’s cash desk from an accountable person in rubles. "

ENTRY: Debit 50.03 “Cash documents” Credit 71.01 “Settlements with accountable persons”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Receipt of monetary documents

in the “Cash” menu, type of business transaction: “

Receipt from an accountable person”

“Issuance of monetary documents from the organization’s cash desk to an accountable person in rubles.”

ENTRY: Debit 71.01 “Settlements with accountable persons” Credit 50.03 “Cash documents”

Which document 1 will be made in 1c:Accounting 2.0/1c:Accounting 3.0

: —

Issuance of monetary documents

in the “Cashier” menu, type of business transaction: “

Issue to an accountable person”

Characteristics of account 71

71 accounting accounts are considered active-passive accounts. This means that account balances can have both a debit and a credit balance at the end of the reporting period. This means that at the end of the month the debt may be registered with the employee. For example, a subordinate has just received an advance and has not yet had time to report.

The debt may also be attributed to the company. For example, if an employee spent his own funds to provide for business needs or on a business trip. Overexpenditure is reflected in accounting after the employee has provided an advance report and documented his expenses.

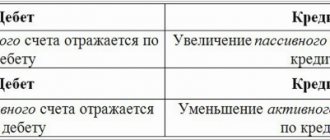

Debit and credit of account 71: what to reflect

| What we reflect on the debit of account 71 | What do we indicate in the credit of accounting account 71 |

| 71 debit account is the amount that was provided to the company employee in advance for specific expenses. That is, this is the money that the employee received as an account. For example, a cashier dispenses cash from a cash register. The balance of account 50 “Cash” decreases - the turnover to the credit account is reflected. 50. And at the same time the debit turnover on the account is reflected. 71 - the employee received accountable funds. Before the subordinate provides an advance report, he will be credited with an advance - a debit balance on the account. 71. Or a debit balance is formed if the employee reported less than the amount received in advance. The remainder should be returned to the organization's cash desk. | In the credit of the account we reflect the expenses of the accountable person, supported by documents. That is, the employee submitted an advance report, and the manager checked and approved it. Then the accountant accepts the transactions for accounting and accrues expenses according to the report. The expenditure of funds is reflected in the credit of accounting account 71. At the same time, the debit balance of the account decreases. The result of the operation may be the loan balance if the reporting employee spent his money on company expenses. The company must repay this debt. That is, pay the amount of the credit balance to the accountable person. |

SALT for account 71: sample filling with postings

For our example, the fact of issuing funds to Ivanov and Petrov in the amount of 10,000 and 20,000 rubles, respectively, is first recorded. These transactions correspond to the following transactions:

- Dt 71.01 Kt 50 - in the amount of 10,000 rubles;

- Dt 71.01 Kt 50 - in the amount of 20,000 rubles.

Let's reflect them on the turnover sheet:

- enter the amounts 10,000 and 20,000 rubles. in the “Debit” column opposite the corresponding analytical characteristics of the subaccount (these are the names of employees Ivanov and Petrov);

- we add up the 2 available figures that form the debit of subaccount 71.01, and indicate in the turnover sheet the resulting total amount of 30,000 rubles. in the “Debit” column opposite this subaccount;

- if no other operations were carried out on synthetic account 71 (let’s agree that this is the case), we duplicate the amount of 30,000 rubles. in the “Debit” column opposite account 71.

As soon as Ivanov and Petrov bring their advance reports and checks, we draw up the postings:

- Dt 10 Kt 71.01 - in the amount of 9,000 rubles;

- Dt 26 Kt 71.01 - in the amount of 19,000 rubles.

On the turnover sheet:

- enter 9,000 and 19,000 rubles. in the “Credit” column opposite the employees’ names;

- we add up the figures for credit transactions, and the resulting value is 28,000 rubles. We enter in the “Credit” column opposite the subaccount 71.01, as well as the main synthetic account 71.

If the opening balance is zero, then in order to determine the balance at the end of the period and indicate it in the turnover sheet, you need to subtract the smaller ones from the larger values indicated in the columns under the cell “Turnover at the end of the period”. If 1st is recorded in the Debit column and 2nd is recorded in the Credit column (as in our scenario), the results are recorded in the Debit column under the Ending Balance cell. In this case it consists of:

- from 1,000 rub. according to Ivanov’s reports (enter this amount next to Ivanov’s last name);

- 1,000 rub. according to Petrov’s reports (we record opposite the name Petrov).

In turn, in the “Debit” column under the “Balance at the end of the period” cell opposite subaccount 71.01, the indicators of all analytical characteristics of the subaccount are summarized. That is, in our case, we will fix here the amount of 2,000 rubles. We duplicate this value in the “Debit” column under the “Balance at the end of the period” cell opposite the synthetic account 71.

Thus, based on the results of transactions, a debit balance for account 71 is recorded in the turnover sheet. Its total amount is 2,000 rubles.

A finished sample of the turnover sheet reflecting the above operations will look like this:

| Account (sub-account) / Analytical characteristics of a sub-account | Balance at the beginning of the period | Period transactions | balance at the end of period | |||

| Debit | Credit | Debit | Credit | Debit | Credit | |

| 71 | 30 000,00 | 28 000,00 | 2 000,00 | |||

| 71.01 | 30 000,00 | 28 000,00 | 2 000,00 | |||

| Ivanov | 10 000,00 | 9 000,00 | 1 000,00 | |||

| Petrov | 20 000,00 | 19 000,00 | 1 000,00 | |||

For other nuances of filling out the SALT, read the material “How can you check the balance sheet” .

Accounting entries for account 71

Let's look at how to correctly make transactions for 71 accounts. Here are typical transactions and correspondence of accounts. Let us indicate which documents to draw up during the operation.

| Operation | Debit | Credit | Foundation documents |

| Money issued in cash report | 71 | 50 | A cashier's report and an expense order were drawn up |

| Funds are credited to the bank card account | 71 | 51 | Bank statement, payment order for transfer |

| Funds are credited to the report on the organization’s corporate card | 71 | 55 | Bank statement from special company accounts |

| The purchase of fixed assets is reflected in the advance report | 08 | 71 | Certificate of acceptance of works and services |

| Materials and raw materials purchased by the accountable person were capitalized | 10 | 71 | Invoices, sales receipts, transportation documents, acceptance certificate |

| The amount of expenses according to the advance report for production and economic needs is reflected | 20, 26, 44 | 71 | Advance report, invoices |

| Return to the cash desk of funds unspent by the accountable person | 50 | 71 | Cashier's report, receipt order |

| Debt accrued for amounts not returned on time by the accountable person | 73 | 71 | Advance report |

Now let's look at examples of posting entries for various situations.

Turnover sheet for account 71

I want to continue talking about the formation of turnover for different accounts, and today the turnover sheet for account 71 is next..

Account 71 “Settlements with accountable persons” is used by almost all enterprises. In the 1C Accounting 8 edition 2 program, this account has several sub-accounts; we will look at the very first sub-account, which is also called “Settlements with accountable persons”. The account is active-passive. This means that the account balance can be either debit or credit. Debit balance means accounts receivable or debt of an accountable person to the enterprise. The credit balance, on the contrary, shows the accounts payable or debt of the enterprise to the accountable person.

The account structure itself is active. This means that the debit will show an increase in the debt of the accountable person (if cash advances are issued to him), and the credit will show a decrease in debt (when submitting documents for amounts issued or returning unused funds).

Advances to an accountable person can be issued from the cash register or from a current account.

In order to report on the funds issued, the employee submits an advance report. You can read more about generating an advance report in 1C here.

Let's look at how the turnover sheet is formed for account 71 in 1C. In our example, we will have two accountable persons: Petrov Petrovich and Ivanov Ivan Ivanovich. Petrov was given money from the cash register in the amount of 1,000 rubles for business expenses. Ivanov 10,000 rubles from his current account for travel expenses.

Next, Petrov presented an advance report in the amount of 900 rubles, and Ivanov in the amount of 11,800 rubles.

The turnover sheet for account 71 is generated from the “Reports” menu at the top of the program. You need to select “Account turnover sheet”. It can also be done through the “Cashier” tab. In the lower right part of this tab called “Reports”, the very last item is SALT for account 71.

What conclusion can we draw from this register? Turnovers on the debit account of the form turnover sheet for account 71 show the funds that were issued to accountable persons and, accordingly, the increase in their debt to the enterprise. According to the account credit, we see the amounts for which the reporting persons submitted advance reports and reduced their debt to the enterprise.

Next, consider the balance at the end of the period. For employee Ivanov, the balance is 1,800 rubles. on loan. This means that Ivanov spent more money than he was given (11,800 rubles, instead of 10,000 rubles). Therefore, the company owes Ivanov 1,800 rubles.

For employee Petrov, the balance at the end of the month is debit. This means that Petrov owes the company 100 rubles, since he was given 1,000 rubles, and the advance report was submitted only for the amount of 900 rubles.

If you look at the total balance in the turnover statement register for account 71, it amounts to 1,700 rubles for the loan, and this is the debt of the enterprise to its accountable persons.

Share the video on social networks, ask questions in the comments and subscribe to my Instagram

Visit my second blog

All courses on accounting and 1C

If you need individual training, consultations and other services for working with 1C, take a look at the “Consultations” section

Did you like the article? Share on social media networks

Example No. 1. Overspending - debt in favor of an accountable employee

Vesna LLC issued in June to secretary P.P. Karandashikov. 3000 rubles for the purchase of pencils. The funds were issued from the cash register. The employee made a purchase in the amount of 3,150 rubles. An advance report was drawn up on the costs incurred, a fiscal receipt and a delivery note were attached to the documents.

Postings:

| Operation | Debit | Credit | Amount, rub. |

| The report was issued from the cash register | 71 | 50 | 3000 |

| The advance report has been approved, the expenses for the purchase of pencils have been taken into account | 10 | 71 | 3150 |

| The overspending was transferred to the secretary's bank card | 71 | 51 | 150 |

Example No. 2. The balance is the debt of the accountable person

To purchase a laptop for Vesna LLC specialist K.K. Barankin. 35,000 rubles were transferred to the card. A computer hardware store provided Barankin with a 10% discount on the cost of the laptop (3,500 rubles). The total purchase amounted to 31,500 rubles. Barankin provided an advance report and returned the balance to the cashier.

Postings:

| Operation | Debit | Credit | Amount, rub. |

| The sub-report is listed on the Barankin map | 71 | 51 | 35 000 |

| The advance report has been approved, the expenses for the purchase of a laptop have been taken into account | 08 | 71 | 31 150 |

| The balance was returned to the cash desk of Vesna LLC | 50 | 71 | 3500 |