Accounting entries for fixed assets in budgetary organizations

Budgetary organizations are institutions financed from budgetary funds.

Accounting in such organizations is carried out on the basis of a special chart of accounts for budgetary institutions with their own entries, which is approved by Order No. 174n of the Ministry of Finance of the Russian Federation dated December 16, 2021. In all budgetary institutions, fixed assets, according to Instruction No. 25n, are accounted for in account No. 010100000 - Basic facilities. Fixed assets are recorded in accounting registers at their original cost. It includes the costs of purchasing and constructing facilities, consulting services, delivery and other costs required to bring the facility into a state of readiness for operation, taking into account the VAT charged. Accounting in budget accounting accounts is carried out in rubles and kopecks.

Benefits for victims of a nuclear power plant accident in the Russian Federation

Victims of the Chernobyl disaster are entitled by law to such privileges. The leave of Chernobyl survivors can be extended in terms of duration. All Russians who suffered in some way from the Chernobyl disaster or during the liquidation of the accident have the right to regular leave, for which the employer will pay. Russians determine the start time of their vacation independently. In addition, Chernobyl victims can take additional rest for a period of up to 14 days.

We recommend reading: Procedure for Refusing Benefits of a Veteran of Labor

Since Evgeniy Yuryevich is a liquidator of the consequences of the Chernobyl nuclear power plant, he is entitled to a state old-age pension (250% of the social pension). After indexation in April 2021, it is 13,101.64 rubles (up to 12,585.63 rubles). But citizen Sokolov is also a disabled person of the third group. In this regard, he is entitled to a disability pension, which is 125% (from April 1, 2021 - 6550.82 rubles). That is, twice as much.

Typical entries for budget accounting (examples)

Digits 1–17 encode the classification attribute of receipts and disposals and are formed from the BCC. Budget accounting instruction No. 162n contains a separate Appendix 2, in which for each account it is specified which BCC must be indicated: the code intended for budget expenditures (KRB), budget revenues (KDB) or sources of financing the budget deficit (CIF). Moreover, for institutions, categories 4–20 of the BCC are taken, and for financial authorities, categories 1–17.

Public sector organizations keep records based on the provisions of the Unified Chart of Accounts and instructions thereto, approved by Order of the Ministry of Finance of the Russian Federation dated December 1, 2021 No. 157n. According to clause 21 of instruction No. 157n, private charts of accounts for specific types of organizations also apply.

Calculations for damage and other income

Please note that before the changes were made by Order of the Ministry of Finance of the Russian Federation No. 89n to Instruction No. 157n, when determining the amount of damage caused to an institution due to loss, damage, or theft of property, one should proceed from the market value of the property on the day the damage was discovered ( clause 220 of Instruction No. 157n ).

Thus, the amount of damage caused by an employee cannot be lower than the value of the property (taking into account its depreciation) according to budget accounting data. In addition, federal law may establish a special procedure for determining the amount of damage subject to compensation caused to the employer by theft, intentional damage, shortage or loss of certain types of property and other valuables, as well as in cases where its actual amount exceeds the nominal amount.

Features of writing off shortages in budgetary and autonomous institutions

During the inventory process carried out in the institution before the formation of annual financial statements, it was discovered that one computer did not have a monitor. The person responsible for the loss has not been identified. The computer was purchased through a grant for other purposes and is considered particularly valuable property. It is used in the main activities of the institution, which are not subject to VAT.

Reflection in accounting for the disposal of parts of a fixed asset will depend on the decision of the manager on the procedure for using and accounting for material assets remaining at the disposal of the institution after theft is detected. This decision should be made based on technical capabilities and economic feasibility.

Repayment of the deficiency at the expense of the guilty party

Shortage (damage) of material assets within the limits of natural loss norms is not taken into account in account 0 209 00 000 “Calculations for property damage”, but is attributed in accordance with the order of the manager to the expenses of the institution (cost of finished products, works, services).

Account 0 209 00 000 “Calculations for property damage” is intended to record calculations for the amounts of identified shortages, thefts of funds, other valuables, for the amounts of damage caused to the property of the institution, subject to compensation by the perpetrators in the prescribed manner (clause 220 of Instruction No. 157n, p 107 Instructions No. 174n).

Budget entries for compensation of property damage to the lessor

Organization on the simplified tax system 6%. The property owns non-residential premises in a multi-storey building. The room was flooded by residents from the top floor. When receiving compensation for property damage, what entries in accounting should be used and is this compensation subject to 6%?

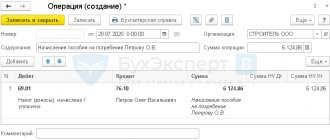

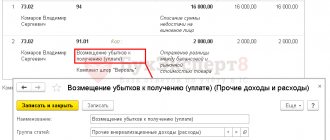

When receiving compensation for losses from property damage, make the following entries in accounting: Debit 76-2 Credit 91-1 - the amount of compensation for losses from property damage has been accrued; Debit 51 Credit 76-2 – compensation received.

When calculating the single tax, include the amount of compensation received as part of non-operating income.

Accounting entries when reflecting the amount of the deposit transferred to the lessor under the rental agreement 1 76 50 Reflects the payment of the deposit amount by the client for the rental object.

There is also no need to charge VAT on the amount of compensation received from the guilty employee, since there is no implementation of subclause. Tax Code of the Russian Federation. Simplified taxation system When calculating tax, a simplified tenant will not be able to take into account in expenses the damage reimbursed to the lessor in connection with the loss of the leased property. Since this type of expense is not included in the closed list of “simplified” expenses.

1 tbsp. 346.15, paragraph 3 of Art. 250, p.

Accounting press and publications 2008

Article: Compensation for damage by the organization (“New Accounting”, 2007, N 11) Source of publication “New Accounting”, 2007, N 11 “New Accounting”, 2007, N 11 COMPENSATION FOR DAMAGE BY THE ORGANIZATION In practice, there are situations when a company has to compensate for damage, caused to another organization. Read about in what cases this happens and how such expenses are reflected in the accounting and tax accounting of an organization.

What is meant by compensation for damage caused for the purpose of calculating income tax, Ch. 25 of the Tax Code of the Russian Federation does not explain. There is no specific list of such expenses in this chapter. Guided by the provisions of paragraph.

1 tbsp. 11 of the Tax Code of the Russian Federation, let us turn to the norms of civil legislation.

A tenant using the general taxation system suffered damage as a result of a roof leak in the rented premises during heavy rain - goods (food) were damaged.

.

The lessor agrees to compensate for the damage caused.

Therefore, no invoice is issued to the culprit. VAT, previously legally accepted for deduction on goods written off as a result of damage from flooding, does not need to be restored.

Due to the fact that in the situation under consideration, VAT on damaged goods was previously accepted for deduction and it is not required to restore it due to their write-off, we believe that the VAT amounts should not be taken into account when determining the amount of the claim.

According to Art.

Compensation for lost rental property

The amount of damage as a general rule is equal to the market value of the lost property and clause 3 of Art. 393 Civil Code of the Russian Federation; Resolution of the Presidium of the Supreme Arbitration Court of June 10, 2008 No. 1498/08.

1) . And the lessor must draw up an act of write-off of the fixed asset on the basis of documented information received from the tenant about the loss of property. It can be compiled either according to your own form or according to the unified form No. OS-4.

Secondly, the amount of damage compensated by the tenant is included in non-operating income when calculating income tax.

Accounting for leasehold improvements

The burden of major repairs is often placed on the lessor (Clause 1, Article 616 of the Civil Code of the Russian Federation). Such property owned by the tenant, depending on the cost and useful life, can be accounted for either as fixed assets or as business inventory.

Inseparable improvements cannot be dismantled without causing harm to the object.

According to the author, they will include both any repair (current or major) and reconstruction of the facility. If inseparable improvements are recognized as reconstruction (modernization) of a real estate property, then they must increase the initial cost of the property (clause 27 of PBU 6/01, clause 2 of Article 257 of the Tax Code of the Russian Federation).

At the property transferred to the tenant, inseparable improvements, or rather, work on its modernization, will be carried out at the expense of the tenant (either by his own forces, or by the forces of an engaged contractor).

Calculations for damages and other income (Zaripova M

Date of article posting: 04/09/2016 What do we take into account on account 209 00? In accordance with paragraph.

220 Instructions No. 157n account 209 00 “Calculations for damage and other income” is intended to account for calculations: - for the amounts of identified shortages, thefts of funds, other valuables, losses from damage to material assets, damage caused to the property of the institution, subject to compensation by the guilty parties in the prescribed manner legislation of the Russian Federation; — for amounts of advance payments not returned by the counterparty in the event of termination of contracts (other agreements), including by court decision; - for amounts of debt of accountable persons that were not returned in a timely manner (not withheld from wages); - on the amount of debt for unworked vacation days when an employee is dismissed before the end of the working year for which he has already received annual paid leave; - on the amounts of excessive payments made; - for the amounts of forced seizure, including compensation for damage in accordance with the legislation of the Russian Federation, in the event of insured events, as well as for the amounts of damage caused as a result of the actions (inaction) of officials of the organization.

Accounting for property damage settlements

According to Art. 241 of the Labor Code of the Russian Federation for damage caused, the employee bears financial liability within the limits of his average monthly earnings, unless otherwise provided by this code or other federal laws.

The financially responsible person, warehouse manager I., was found guilty of the identified shortage.

S. Sidorov. By order of the employer, the amount of damage will be deducted from his salary, which is 22,500 rubles.

Source: https://152-zakon.ru/bjudzhetnye-provodki-po-vozmescheniju-uscherba-imuschestva-arendodatelju-12444/

Repayment of Deficiencies in Budget Institution Postings in 2021

At the same time, the disposal of fixed assets when a shortage is identified is reflected in the debit of the corresponding analytical accounting accounts, account 0 104 00 000 “Depreciation”, account 0 401 10 172 “Income from transactions with assets” in correspondence with the credit of the corresponding analytical accounting accounts, account 0 101 00 000 “Fixed assets” (clause 12 of Instruction No. 157n). At the same time, if the object was accounted for in off-balance sheet account 21 “Fixed assets worth up to 3,000 rubles inclusive in operation,” its disposal as a result of a shortage is reflected by reducing this off-balance sheet account (clause 332 of Instruction No. 157n). At the same time, the amounts of identified damage are reflected in debit accounts 0 209 74 000 “Calculations for damage to inventories” and 0 209 71 000 “Calculations for damage to fixed assets” (clause 109 of Instruction No. 174n, clauses 220, 221 of Instruction No. 157n).

- Posting food shortage

- Budgetary accounting of calculations of shortages

- Accounting for food products in budgetary institutions*(1)

- Compensation for shortages by the guilty parties, reflected in accounting

- Surpluses, shortages, mis-grading. how to reflect it in accounting? (Alekseeva M.)

- Postings on food shortages in a budgetary institution

Accounting entries of a government institution

At the end of the year, the institution purchased inventory in the amount of 30,200 rubles. Payment was made on the last day the Treasury accepted payments. The accountant mistakenly submitted an application for cash expenses in the amount of 30,000 rubles.

Monetary obligations accepted in the amount of the debit turnover of the account 0 208 00 000 are reflected regardless of the transaction with which they are closed on the loan, the main thing is not to return them, since the return reduces the monetary obligation.

Reflection in postings of surpluses and shortages in the cash register

The cash register inventory can be carried out unscheduled, suddenly and without warning, in order to control the responsibility of the MOL. The timing and procedure for unscheduled inventory are also established by the regulations of the enterprise.

The commission must include at least three people. The presence of the MOL on the commission's list is mandatory. In addition, the presence of security and internal audit employees (if available) is desirable. If there is no signature of even one of the commission members, the inventory is considered invalid.

Write-off of accounts payable in a budget institution (postings)

The inventory must be approached with special care and thoroughness. It is the inventory of receivables and payables that allows timely identification of doubtful and bad debts. Based on the results of the audit, work is carried out in management accounting with receivables and a reserve for doubtful debts is formed.

Inventory initiated by an enterprise decision implies that accounts can be selected at the discretion of the organization . Afterwards, an order is issued indicating the commission, the name and list of accounts and creditors, deadlines and a list of necessary documentation.

Postings on food shortages in a budgetary institution

The inventory commission found that the vegetables had become unsuitable for further use due to non-compliance with their storage conditions. The financially responsible person was found guilty. The latter admitted guilt and voluntarily agreed to compensate for the damage caused. The amount of damage according to the loss assessment report is 90 UAH. The guilty person compensated for the damage caused by depositing cash into the institution's cash desk.

Important!

From the amounts collected from the perpetrators, compensation is made for losses caused to the institution, taking into account the actual costs of restoring damaged or acquiring new material assets and the cost of work to restore them.

Deductions under writs of execution: features of calculation and recording

the amount of one-time financial assistance paid in connection with a natural disaster or other emergency circumstances, a terrorist attack, in connection with the death of a family member, as well as paid in the form of humanitarian assistance;

We recommend reading: Young Family Program in the Trans-Baikal Territory Terms and Conditions

the amount of full or partial compensation for the cost of vouchers, with the exception of tourist vouchers, paid by employers to employees and (or) members of their families to sanatorium-resort and health-improving institutions located on the territory of the Russian Federation, as well as the amount of full or partial compensation for the cost of vouchers for children under age 16 years old, to sanatorium-resort and health-improving institutions located on the territory of the Russian Federation;

Capitalization of surplus during inventory in a budgetary institution

Fixed assets, materials and finished products are classified as particularly valuable property. The identified discrepancies were reflected in the statements. The identified assets (fixed assets and materials) are planned to be used within the framework of activities financed by a subsidy for the implementation of government assignments. Goods and finished products are used in the income-generating activities of the institution.

According to paragraph 7 of Instruction No. 148n, an inventory of property, financial assets and liabilities is carried out by a budgetary institution in accordance with the regulatory legal acts of the Ministry of Finance of Russia. In turn, the procedure for conducting an inventory and recording its results is established by the Methodological Guidelines for the Inventory of Property and Financial Liabilities, approved by Order of the Ministry of Finance of Russia dated June 13, 1995 No. 49 (hereinafter referred to as the Guidelines).

“Budget-funded educational institutions: accounting and taxation”, 2011, N 9

ACCOUNTING FOR CALCULATIONS FOR SHORTAGES

Shortage is the incomplete availability of material and monetary resources, identified as a result of control, audit, and inventory. The shortage of any property of an institution is one of the types of damage caused (inflicted) to the institution. How are calculations of shortages taken into account in the accounting of state-owned, budgetary and autonomous educational institutions? What is the peculiarity of writing off shortages that arose within and above the norms of natural loss? How to reflect transactions for attributing the amounts of shortfalls to the account of the guilty parties? How to determine the value of property for which a shortage has been identified? The answers to these and other questions are in the article.

In accordance with clause 220 of Instruction No. 157n <1>, account 209 00 “Calculations for property damage” is intended to record calculations for the amounts of identified shortages.

———————————

<1> Instructions for the application of the Unified Chart of Accounts for public authorities (state bodies), local governments, management bodies of state extra-budgetary funds, state academies of sciences, state (municipal) institutions, approved. By Order of the Ministry of Finance of Russia dated December 1, 2010 N 157n.

Analytical accounting for this account is maintained in the Funds and Settlements Accounting Card (f. 0504051) in the context of persons responsible for compensation for damage caused (perpetrators), type of property and (or) amount of damage.

Grouping of calculations for damage to property caused by shortages is carried out according to groups of receipts reimbursed for damage to property according to analytical groups of the synthetic account of the accounting object:

a) 70 “Calculations for damage to non-financial assets”. Calculations for property damage are recorded on account 109 70 in the context of the following analytical codes of the type of synthetic account of non-financial assets:

— 1 “Calculations for damage to fixed assets”;

— 2 “Calculations for damage to intangible assets”;

— 3 “Calculations for damage to non-produced assets”;

— 4 “Calculations for damage to inventories”;

b) 80 “Calculations for other damage.” Settlements for property damage are recorded on account 109 80 in the context of the following analytical codes of the type of synthetic account of financial assets:

— 1 “Calculations for cash shortages”;

— 2 “Calculations for shortages of other financial assets.”

Taking into account the above, we present a table of accounts used by state (municipal) institutions in accordance with:

— Instructions for the application of the Chart of Accounts for Budget Accounting, approved by Order of the Ministry of Finance of Russia dated December 6, 2010 N 162n (hereinafter referred to as Instruction N 162n). Applied by state institutions and budgetary institutions that are recipients of budget funds (hereinafter referred to as state institutions);

— Instructions for the application of the Chart of Accounts for accounting of budgetary institutions, approved by Order of the Ministry of Finance of Russia dated December 16, 2010 N 174n (hereinafter referred to as Instruction N 174n). Applied by budgetary institutions in respect of which a decision has been made to provide subsidies from the corresponding budget of the budgetary system of the Russian Federation (hereinafter referred to as budgetary institutions);

— Instructions for the application of the Chart of Accounts for accounting of autonomous institutions, approved by Order of the Ministry of Finance of Russia dated December 23, 2010 N 183n (hereinafter referred to as Instruction N 183n). Used by autonomous institutions.

| Account name | Account number | ||

| State institutions | Budget institutions | Autonomous institutions | |

| Calculations for damage to fixed assets | 0 209 71 000 | 0 209 71 000 | 0 209 71 000 |

| Increase in accounts receivable for damage to fixed assets | 0 209 71 560 | 0 209 71 560 | — |

| Reducing accounts receivable for damage to fixed assets | 0 209 71 660 | 0 209 71 660 | — |

| Calculations for damage to intangible assets | 0 209 72 000 | 0 209 72 000 | 0 209 72 000 |

| Increase in accounts receivable for damage to intangible assets | 0 209 72 560 | 0 209 72 560 | — |

| Reducing accounts receivable for damage to intangible assets | 0 209 72 660 | 0 209 72 660 | — |

| Calculations for damage to non-produced assets | 0 209 73 000 | 0 209 73 000 | 0 209 73 000 |

| Increase in accounts receivable for damage to non-produced assets | 0 209 73 560 | 0 209 73 560 | — |

| Reducing accounts receivable for damage to non-produced assets | 0 209 73 660 | 0 209 73 660 | — |

| Calculations for damage to inventories | 0 209 74 000 | 0 209 74 000 | 0 209 74 000 |

| Increase in accounts receivable for damage to inventories | 0 209 74 560 | 0 209 74 560 | — |

| Reducing accounts receivable for damage to inventories | 0 209 74 660 | 0 209 74 660 | — |

| Calculations for cash shortages | 0 209 81 000 | 0 209 81 000 | 0 209 81 000 |

| Increase in accounts receivable for cash shortages | 0 209 81 560 | 0 209 81 560 | — |

| Reducing accounts receivable for cash shortages | 0 209 81 660 | 0 209 81 660 | — |

| Calculations for shortages of other financial assets | 0 209 82 000 | 0 209 82 000 | 0 209 82 000 |

| Increase in accounts receivable for shortages of other financial assets | 0 209 82 560 | 0 209 82 560 | — |

| Reducing accounts receivable for shortages of other financial assets | 0 209 82 660 | 0 209 82 660 | — |

Transactions on account 0 209 00 000 are reflected in the journal of transactions with debtors for income.

Determining the amount of damage

When determining the amount of damage caused by shortages, one should proceed from the market value of material assets on the day the damage was discovered. Market value is understood as the amount of money that can be obtained as a result of the sale of these assets (clause 220 of Instruction No. 157n).

Data on the market value of an asset must be confirmed by documents, and if this is not possible, by expert evidence.

When determining the market value, the commission for the receipt and disposal of assets created in the institution on a permanent basis uses (clause 25 of Instruction No. 157n):

— data on prices for similar material assets received in writing from manufacturing organizations;

— information on the price level available from state statistics bodies, trade inspectorates, as well as in the media and specialized literature;

— expert opinions (including experts recruited on a voluntary basis to work in the commission for the receipt and disposal of assets) on the value of individual (similar) assets.

According to Art. 246 of the Labor Code of the Russian Federation, the amount of damage caused to the employer by the shortage cannot be lower than the value of the property according to accounting data, taking into account the degree of depreciation of this property.

Lack of funds

As a rule, a shortage of funds is identified during an audit of the institution's cash register.

The audit (inventory) of the cash register, in accordance with clause 3.39 of the Methodological guidelines for the inventory of property and financial obligations <2>, is carried out in accordance with the Procedure for conducting cash transactions in the Russian Federation, approved by the Decision of the Board of Directors of the Central Bank of the Russian Federation dated September 22, 1993 N 40 and communicated by the Letter of the Central Bank RF dated 04.10.1993 N 18.

———————————

<2> Approved by Order of the Ministry of Finance of Russia dated June 13, 1995 N 49.

In accordance with paragraph 37 of this Procedure, within the time limits established by the head of the institution, as well as when cashiers change, a sudden audit of the cash register is carried out with a complete page-by-sheet recalculation of cash and checking of other valuables in the cash register. The cash balance in the cash register is verified with the accounting data in the cash book.

To carry out an audit of the cash register, a commission is appointed by order of the head of the institution, which draws up an act. If a shortage of valuables is detected at the cash desk, the act indicates their amount and the circumstances of their occurrence.

Cashiers are responsible for the lack of money in the cash register, since agreements on full financial liability are mandatory for these employees (Articles 243, 244 of the Labor Code of the Russian Federation).

The employee’s full financial liability consists of his obligation to compensate the direct actual damage caused to the employer in full. The damage caused may be compensated by the guilty cashier voluntarily or by court decision. Moreover, in the first case, the employee has the right to independently contribute the missing amount of money or such funds are withheld by the employer from the employee’s salary, taking into account the restrictions established by Art. Art. 137, 138 Labor Code of the Russian Federation.

Transactions to account for cash shortages are reflected in the following accounting entries:

Accrual of penalties for transactions with a budgetary institution in 2021

Recognition of expenses in accounting does not depend on the intention to generate income and the form of expenses. As an illustrative example, consider a situation where a building is confiscated from an organization in order to pay a tax, and subsequently sold through an auction. Postings for the operation (without displaying specific numbers) will be as follows: Dt 76 Kt 91-1 Display of proceeds from the sale of the building Dt 91-2 Kt 68 VAT accrued Dt 91-2 Kt 01 subaccount “Disposal of fixed assets” Write-off of the value of the building on the balance sheet Dt 68 Kt 76 Repayment of tax debt Dt 91-2 Kt 76 Display of enforcement fee Dt 91-2 Kt 76 Display of auction costs and organizer remuneration Dt 91-2 Kt 76 Display of the amount of the withheld fine Dt 51 Kt 76 Receipt of the amount remaining from the sale of the building Features for budget institutions In budgetary institutions, accounting is carried out in accordance with Instruction No. 174n.

Changes in postings for insurance premiums and penalties in 2021-2021 During the transition period (2021-2021), situations are possible when you will have to make adjustments or pay insurance premiums for the years preceding 2021, i.e. those in which the calculations were carried out directly with funds. To avoid confusion in calculations, it is best to create separate second-order subaccounts on account 69 to account for old (for 2021–2021) and new (from 2021) contributions for each type of insurance, thereby ensuring their analytical accounting for correct posting in reporting. IMPORTANT! In order to protect yourself in the event of a tax audit or legal proceedings, add provisions to the accounting policy order regarding changes in the accounting methodology for insurance premiums.

Postings for transfers to budget revenue of a government agency

Reflected by the financial authority as the revenue administrator is the receipt of distributed revenues into the budget, the administration of which is carried out by the corresponding revenue administrator of another budget (indicating in the first three digits of the account number the code of the corresponding chief budget revenue administrator)

It is advisable to reflect pension contributions for the payment of the funded part of the pension in accounting on account 0.303.10.000 “Calculations for insurance contributions for compulsory pension insurance for the payment of the insurance part of the labor pension.”

Return of accounts receivable from previous years in a budgetary institution 2021

After the advance payment is transferred to third parties, for various reasons the counterparty may violate the contractual terms and fail to deliver the goods. Or not provide services, delay the work. Violation of deadlines also occurs when the accountable is given more funds than actually spent. The resulting debt is subject to repayment by debtors. If the counterparty or accountable person does not object to the return, the funds are transferred within the following time limits:

By virtue of Instructions No. 65n, expenses for the payment of insurance premiums accrued for payments to employees provided for in employment contracts are reflected under KVR 119 and subarticle 213 of KOSGU, in other cases - according to those subarticles (articles) of KOSGU for which expenses for payment of remunerations (income) are reflected ) on which these contributions are calculated.

A shortage was detected at the cash register: postings

At enterprises, cash is accounted for in account 50 “Cash”, which has three sub-accounts: 50-1 “Cash of the enterprise”, 50-2 “Operating cash”, 50-3 “Payment documents”. Reporting forms on the off-balance sheet account 006 of the same name are taken into account separately.

The commission, in the presence of the cashier, records meter readings that reflect the amount of revenue. The data is checked against the submitted cash register tape. The difference in the balance at the beginning and end of the day reflects the daily amount of revenue. The numbers in the cash book, on the tape and on the counters must be identical.