Definition

Submitting reports to tax authorities is the provision of a set of documents that reflect information about the payment of taxes. This process consists of two stages: preparing the declaration and calculating the advance.

No less important is the 6-NDFL report, which contains information about all persons who received income from a particular resident, about the amounts of accruals, payments, and deductions, which are the basis for taxation. For violation of deadlines, a fine is provided for late submission of reports to the Federal Tax Service.

Types of taxes

Let's consider all current types of reporting.

| Tax | Term | Payer |

| VAT | Quarterly, until the 25th of the next reporting month. | The report is provided by all organizations operating on the common taxation system at the place of registration. |

| Income tax | Quarterly, until the 28th of the next reporting month. | |

| Z-NDFL | Every year until April 30. | Individuals are tax agents. |

| 2-NDFL | Every year until April 1. | Individual entrepreneurs who have hired employees submit a report at the place of registration. |

| 6-NDFL | Quarterly, until the 1st day of the next reporting month. | |

| simplified tax system | Annually: individual entrepreneur – until April 30; LLC – until March 31. | At the place of registration. |

| UTII | Quarterly, until the 20th day of the next reporting month. | To the Federal Tax Service at the place of business. |

Sanctions

Let us consider in more detail what the fine is for late submission of reports to the Federal Tax Service. 2-NDFL, VAT and income tax are taxed at different rates. Therefore, the penalties for each of them are different.

| Responsibility | Tax | Administrative | Criminal |

| VAT | 5% of the tax amount monthly; 200 rub. for providing a paper report. Penalty - 0.003% of the Bank of Russia rate per day. Accounts may be seized. | 300 rub. or warning. | Fine up to 300 thousand. Forced labor for up to 2 years. Arrest for 6 months. Imprisonment for up to 2 years. |

| Income tax | The fine for late submission of reports to the Federal Tax Service is 200 rubles. | — | — |

| Transport tax | The fine for late submission of reports to the Federal Tax Service is 5% of the amount. | — | — |

| Land tax | |||

| 2-NDFL | 200 rub. per document | For physical persons – 100 rub. For officials – 500 rubles. Authorities – 1 thousand rubles. | — |

| 6-NDFL | For each month - 1 thousand rubles. After 10 days, the accounts are seized. | — | — |

| simplified tax system | For amounts paid but not declared – 1 thousand rubles. | — | — |

| UTII | 5% of the tax amount. | — | — |

Penalty for late submission of SZV-M and failure to submit at all

When a retired employee stops working, then his pension is indexed. For constant monitoring of working pensioners, the pension fund developed and introduced a new reporting form, called SZV-M. Now employers are required to provide data on the number of all employees, including working pensioners.

The form has its own deadlines for submission to the Pension Fund. The penalty for late submission of SZV-M is provided for by law.

Force majeure when filling

There is no organization or responsible person who in their practice would not encounter non-standard situations when filling out reporting documents. What situations may arise when filling out the SZV-M document?

When the responsible person fills out the document, he enters the following data:

- What kind of agreement does the employee work under? GPC, employment or license agreement. Perhaps he carries out his labor activity under a different contract.

- What reporting month is this agreement valid for? When filling out the document, whether the contract with this employee is valid or has already been terminated.

- Payments made to an employee are subject to contributions to the Pension Fund or not.

It does not matter whether payments were made to the employee, information about him must be provided without fail, even if the company has one employee or the director himself.

If a temporary or seasonal contract was concluded with an employee, the information is also submitted to the pension fund.

Who might not be included in the reporting data?

- Foreign citizens who are temporarily staying in the territory of the Russian Federation and were not insured by the Pension Fund.

- Entrepreneurs, lawyers and notaries who are engaged in private practice according to the law of the Russian Federation. They are not policyholders (Federal Law 212).

There should be no zero reporting to the Pension Fund of the Russian Federation; if the company operates and is not closed, this means that the information is submitted to the manager.

What are the fines under SZV-M?

The following violations are established by law (Federal Law 27, Article 17):

- If the document was not submitted at all.

- The deadlines for submitting the report were violated (late delivery).

- The employee's information was not provided or there was an error in the information.

- If the report did not include all insured persons.

Any of the above violations entails penalties. They amount to 500 rubles for each employee .

For example, if the SZV-M report was not submitted at all , then the organization is subject to a fine of 500 rubles * number of employees .

If the company employs 30 people, then the fine for not passing the SZV-M will be 500 * 30 = 15,000. What if there are 200 or 300 employees? These are very large amounts, so it is worth submitting all documents to the relevant regulatory authorities in a timely manner.

How can you avoid or reduce a fine?

Situations in organizations are different. Reporting can be affected by both the human factor and automation. You can look at an example of what to do if the report did not reach the regulatory authority on time.

The time has come to submit the documents to the Pension Fund, the accountant of Astra LLC entered all the data and sent the report electronically on May 10. Due to technical reasons, the report was not sent on time. He was sent again the next day, May 11. The pension fund warned that a fine would be imposed on the organization.

Current legislation does not provide for the possibility of avoiding a fine or at least reducing it. It can only be appealed in court.

How to reflect the fine for failure to submit SZV-M on time in postings

Any accounting documentation is reflected in the postings. The fine for SZV-M also needs to be reflected in the books. accounting We reflect it like this:

| Check | Operation |

| Dt 69 - Kt 51 | fine paid |

| Dt 99 - Kt 69 | fine charged |

To avoid incurring fines and penalties, we advise you to submit your reports correctly and on time. How to fill out the SZV-M correctly, watch this video:

Source: https://saldovka.com/nalogi-yur-lits/vznosyi-v-pfr-i-fss/shtrafyi-za-nesvoevremennuyu-sdachu-szv-m.html

Example

The income tax return was submitted on 12/16/15, although the deadline was set for 10/28/15. On the same day, an advance payment of 2 million rubles was paid. In April 2021, the organization submitted the following declaration, indicating the reduced tax amount.

The fine for late submission of reports to the Federal Tax Service, the accrual entries for which will be presented in the balance sheet below, is:

- provision of documents for the 3rd quarter of 2015 – 200 rubles;

- submitting an annual declaration late - 1 thousand rubles. + 300 rub. from the manager.

Penalty for late filing of returns in 2021

The application of tax sanctions against taxpayers is a fairly common occurrence, from which no one is immune.

As a rule, such incidents occur as a result of a banal lack of awareness regarding the reporting schedule, or due to frequent changes made to the Tax Code.

The most common administrative penalties are headed by a fine for late submission of a declaration.

Penalty for late submission of a declaration to the tax authorities

Legal consequences of failure to report

The amount of sanctions prescribed for failure to comply with the deadlines for submitting a declaration and non-payment of tax is equal to 5% of its amount for each month in which the delay occurred. The limit for penalty charges is 30%: the accrued amount payable cannot exceed this figure, nor can it be less than 1,000 rubles.

Until relatively recently, when reading the relevant articles of tax legislation devoted to this issue, taxpayers had some disagreements regarding its interpretation in terms of determining the date of occurrence of penalties.

The new wording introduces the necessary clarifications: if the tax is paid on time and in full, but the declaration was filed late, the amount of the fine is 1,000 rubles.

If only part of the tax was paid due to late filing, the penalty should be calculated based on the difference between the amount of tax payable and the amount received in the state treasury within the prescribed period.

For failure to submit reports or submit them later than the deadline prescribed by tax legislation, the judicial authorities, on the basis of an application filed by the Federal Tax Service, have the right to hold executives working in the company accountable by issuing a warning or applying penalties in the amount of 300 to 500 rubles. There are no sanctions for offenses with a statute of limitations of 3 years or more.

In addition to imposing fines, the Federal Tax Service may block company bank accounts

If we are talking, for example, about untimely submission of SZV-M or other personal reporting to the Pension Fund of Russia, such a violation provides for a fine of 500 rubles for each entity in respect of which it was necessary to submit information.

If a company has not submitted a tax return 10 working days after the deadline established by law, the account is blocked. There are no restrictions regarding the amount to be blocked by law.

Penalty for failure to submit a zero declaration

Taxpayers are not exempt from filing a return even if there is no need to pay tax: a zero return, which does not contain information about tax calculation, must also be filed. In connection with this obligation, the Federal Tax Service may collect 1,000 rubles from the violator.

Failure to provide 2-NDFL and 6-NDFL certificates

For such oversights, various sanctions are prescribed: the absence of a timely submitted 2-NDFL on the inspector’s desk is fraught with sanctions in the amount of 200 rubles for a document not provided and a fine of 300 to 500 rubles, which must be paid to officials of the organization. If the employer forgot to submit 6-NDFD to the fiscal authorities, the amount of the fine will be 1,000 rubles for each month, including incomplete ones, starting from the date set for its submission.

Download declaration 2-NDFL

Download declaration 6-NDFL

If an organization acts as a tax agent, penalties are applied, as a rule, to its managers

Don’t know how to fill out forms 2-NDFL and 6-NDFL ? You can familiarize yourself with these topics on our portal. Step-by-step instructions, sample forms, and how to avoid basic mistakes when filling out a declaration.

Penalty for failure to provide interim tax reporting

For some types of taxes, taxpayers are required to file interim reports. For example, all organizations using the simplified tax system must submit reports regarding income tax by March 28. If it is not provided, the monetary equivalent of the fine varies depending on the following factors:

Table 1. Amount of fine depending on the situation

SituationAmount of fine

| If payment is transferred to the treasury on time | You should transfer 1000 rubles as a fine |

| If both filing and payment of tax are late, the penalty will be 5% of the total amount for each full and partial month of delay. | The fine will be 5% of the total amount for each full and partial month of delay |

A 30% fine, which is the maximum allowable fine for failure to file a return, must be paid if a company is more than 6 months late in filing its returns.

Legislation

Art. 119 of the Tax Code of the Russian Federation provides that failure by the payer to submit a tax return may result in a fine being imposed for late submission of reports - 5% of the tax amount on the return. The minimum amount of recovery cannot exceed 1 thousand rubles.

The fine for late submission of reports, which is imposed on the manager of the partnership, is 1 thousand rubles. for each month of delay.

The larger the collection amount and the longer the delay, the higher the fine rate. The minimum fine is 1 thousand rubles, and the maximum is 30% of the declared tax amount.

Features of calculations

Let's look at some of the calculation nuances using an example.

A citizen sold a car in 2014 for 300 thousand rubles, which he purchased in 2012 for 350 thousand rubles. The citizen did not generate any income from this operation. Since we are talking about the sale of property that he owned for less than 3 years, according to the Tax Code the citizen was obliged to submit a declaration in form 3-NDFL by 04/30/2015. The citizen did not know about this obligation. In May, he received a letter from the Federal Tax Service demanding to report on the transaction. The citizen submitted a report on May 25 of that year. The fine for late submission of personal income tax reports to the Federal Tax Service, even if the declaration is “zero”, is 1 thousand rubles.

The individual entrepreneur filed a VAT return for the 2nd quarter of 2015 on August 25. The calculated tax amount is 30 thousand rubles. The duration of the delay is two months. The fine for late submission of reports to the Federal Tax Service for individual entrepreneurs is 10%, that is, 3 thousand rubles. What should an entrepreneur do in this case:

- voluntarily pay the fine;

- try to reduce the amount of the sanction by 2 times;

- do not take any action and wait for the bailiffs.

With the first and last options, everything is more or less clear. Let's take a closer look at the second one.

Sanction amount

A taxpayer who received income in the reporting period that is subject to personal income tax must report to the inspectorate by April 30 of the following year. The exception is for citizens for whom the tax is paid by a tax agent.

If the payer of the fee does not send 3‑NDFL to the inspectorate within the prescribed period, then he faces a fine of 5% of the calculated tax amount. Penalties are assessed for each full/incomplete month of delay.

Example

Citizen Samoilov P.B. sold a car in 2021 for 670 thousand rubles. The tax payable was:

(670,000 – 250,000) × 13% = 54,600 rub.

He had to submit 3-NDFL by April 30, 2021. Samoilov P.B. reported to the Federal Tax Service only on June 17, 2021. The inspectorate fined him:

54,600 × 5% × 2 = 5,460 rub.

The maximum fine cannot exceed 30% of the assessed tax.

Example

Romanov A.A. In 2021, I received an income of 300 thousand rubles. In 2018, he must submit a report and pay 39 thousand rubles to the budget. Romanov filed a declaration only in December 2021, the Federal Tax Service applied A.A. to Romanov. penalty in the amount of:

39,000 × 30% = 11,700 rub.

If the restriction had not been established, the amount of punishment would have been:

39,000 × 5% × 8 = 15,600 rub.

How to reduce the amount of the fine?

The first step is to contact the Federal Tax Service and sign the Inspection Report. From this moment on, the citizen has 14 days to write a petition with reference to Art. 114 of the Tax Code of the Russian Federation on reducing the amount of the fine. This paragraph states that if there is at least one mitigating circumstance (Article 112), the amount of the fine can be reduced by half. Such circumstances include the occurrence of an offense as a result of a combination of difficult personal, family circumstances, financial situation or under the influence of other circumstances, in particular:

- prosecution for the first time;

- whether the individual entrepreneur has dependents.

The more such circumstances are indicated in the petition, the more opportunities there are to reduce the fine.

How to record fines for tax violations and penalties for arrears

Fines for tax violations and penalties are reflected in accounting as part of tax sanctions. When calculating income tax, do not take into account fines and penalties.

Tax legislation (legislation on the payment of insurance premiums) separates the concepts of “penalty” and “fine”. A penalty is an amount of money that an organization must transfer to the budget in case of untimely fulfillment of the obligation to pay a tax or contribution (Clause 1 of Article 75 of the Tax Code of the Russian Federation, Part 1 of Article 25 of the Law of July 24, 2009 No. 212-FZ). A fine is a tax sanction that is collected from an organization for a tax offense or violation of the law on insurance premiums (Article 114 of the Tax Code of the Russian Federation, Articles 46–48 of the Law of July 24, 2009 No. 212-FZ). The amounts of fines for tax offenses are shown in the table.

For accounting purposes, fines and penalties can be combined into one category of accounting objects - tax sanctions. This approach does not contradict the objectives of accounting, in particular, providing complete and reliable information about the activities of the organization and the basic principles of its management - rationality and the priority of content over form (clause 1 of article 13 of the Law of December 6, 2011 No. 402-FZ, clause 10 Regulations on accounting and reporting).

The amount of accrued tax sanctions - both for the current year and for previous ones - does not form a conditional income tax expense (clause 83 of the Accounting and Reporting Regulations, clause 20 of PBU 18/02). Therefore, in accounting, reflect these amounts directly on account 99 “Profits and losses” in correspondence with account 68 “Calculations for taxes and fees” (69 “Calculations for social insurance and security”). To ensure analytical accounting of tax sanctions to accounts 68, 69, it is advisable to open sub-accounts in the context of taxes for which sanctions are accrued (for example, the sub-account “Fines (penalties) for income tax”).

Reflect the accrual of tax penalties by posting:

Debit 99 Credit 68 (69) subaccount “Fines (penalties)” – a fine has been charged for a tax offense (fines for arrears).

When calculating income tax, the organization does not have the right to take into account the amount of fines and penalties (clause 2 of Article 270 of the Tax Code of the Russian Federation).

An example of how tax sanctions (fines and penalties) are reflected in accounting and taxation

Based on the results of six months, the following data is reflected in Alpha’s accounting: – on the loan of subaccount 90-1 – sales revenue in the amount of 11,800,000 rubles; – on the debit of subaccount 90-2 – cost of goods sold in the amount of 7,500,000 rubles; – on the debit of subaccount 90-3 – VAT on sales proceeds in the amount of 1,800,000 rubles.

In June, based on the results of a tax audit, the organization was assessed penalties in the amount of 200,000 rubles. and a fine of 250,000 rubles. on income tax.

When closing the reporting period, the financial result was generated in accounting:

Debit 90-9 Credit 99 subaccount “Profit (loss) before tax” – 2,500,000 rubles. (11,800,000 rubles – 1,800,000 rubles – 7,500,000 rubles) – profit from sales for six months is reflected;

Debit 99 subaccount “Conditional income tax expense” Credit 68 subaccount “Calculations for income tax” – 500,000 rubles. (RUB 2,500,000 * 20%) – the amount of conditional income tax expense has been accrued.

The amounts of tax sanctions were not taken into account when forming the financial result. The accountant reflected the accrual of sanctions by posting:

Debit 99 Credit 68 subaccount “Fines (penalties) for income tax” - 450,000 rubles. – fines and penalties for income tax were assessed.

In the Balance Sheet, the amount of tax sanctions participates in the formation of the indicator in line 1370 “Retained earnings (uncovered loss)” (clause 83 of the Regulations on Accounting and Reporting). In the Statement of Financial Results, the amount of sanctions can be reflected in line 2460 “Other”.

The report on financial results in terms of the formation of calculations for income tax and net profit (loss) was compiled by the Alpha accountant as follows:

| Title of report articles | Line codes | For six months, rub. |

| Profit (loss) before tax | 2300 | 2 500 000 |

| Current income tax | 2410 | (500 000) |

| Change in deferred tax liabilities | 2430 | (–) |

| Change in deferred tax assets | 2450 | – |

| Other | 2460 | (450 000) |

| Net income (loss) | 2400 | 1 550 000 |

When calculating income tax for six months, the amount of tax sanctions was not taken into account (clause 2 of Article 270 of the Tax Code of the Russian Federation).

Requisites

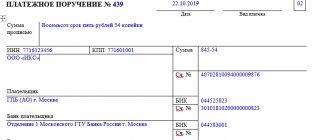

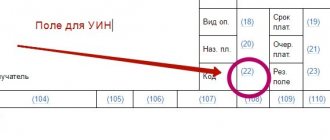

Let's take a closer look at the payment details and the KBK for the fine for late submission of reports.

The budget classification code is indicated in each document on the transfer of funds to the budget. The entire list of identifiers can be found in the directory of the same name. How is the fine for late submission of reports to the Federal Tax Service indicated on the payment slip? KBK 1821160301001600014. The fine is listed under the same code:

- for notifying tax authorities about opening/closing an account late;

- gross violation of the rules of conducting NU;

- violation of the procedure for using property;

- provision of documents during a counter inspection later than required, etc.

Calculation of a fine for late submission of reports: postings

Let's take a closer look at how to reflect transactions on the accrual of fines in the form of an increase in the tax amount in the balance sheet.

| Wiring | Operation |

| DT99 KT68 | Additional NPP accrued. |

| DT90 KT68 | VAT accrued in arrears. |

| DT91 KT68 | Additional land, transport and property taxes have been assessed. |

| DT73 KT68 | Additional personal income tax has been added. |

| DT20 KT69 | Additional insurance premiums have been added. |

Postings when calculating fines and penalties for taxes

In this article, we will study where to include tax fines in accounting, as well as the main entries for the accrual and payment of penalties, fines for taxes: profit, VAT, insurance premiums. Table of contents

- 1 Reasons for calculating tax penalties

- 2 Fine and penalty: what are their differences?

- 3 Display of tax penalties in accounting

- 4 Typical entries for the accrual and payment of fines and penalties for taxes

Reasons for accruing tax fines In accounting, there are several reasons for accruing fines and penalties:

- Late submission of the report;

- Payment of tax and insurance premiums within unspecified terms;

- Understatement of tax liability.

Fine and penalty: what are their differences It should be noted that a fine and penalty are different concepts:

- The fine is assessed immediately when the above reasons occur.

Corporate income tax

The rules for calculating and reporting this tax cause a lot of controversy. Let's consider the situation in more detail.

Russian and foreign organizations that receive income in the Russian Federation pay income tax to the budget. They are also required to provide the Federal Tax Service with a declaration calculating the amount of the fee. In this case, the declaration must be submitted regardless of whether there is an obligation to pay tax at the place of location or registration. There are exceptions to this rule:

- large organizations that have separate divisions must submit reports to the Federal Tax Service at the place of registration of the largest division;

- non-profit organizations, for example, public sector employees, can submit a declaration at the end of the tax period.

The tax period is considered to be the calendar year, and the reporting period is the first quarter. The report must be submitted by March 28 of the following year. For violating this deadline, a fine of 5% of the unpaid tax for each month is charged, but not more than 30% of the amount and a minimum of 1 thousand rubles. This is provided for in Art. 119 of the Tax Code of the Russian Federation.

The declaration is used to calculate tax liabilities for each tax period. At the same time, Ch. 25 of the Tax Code of the Russian Federation does not provide for the provision of advance payment calculations to the Federal Tax Service. Any income tax reporting provided has always been called a declaration. Therefore, there have been disputes between taxpayers and inspectors for a long time - can the Federal Tax Service Inspectorate fine for a “delay” in submitting a “profitable” declaration? Over the years, this issue has been considered differently.

Postings for accrual of penalties and fines for taxes - reflected in accounting

In the course of their work, every accountant is faced with such concepts as fines and penalties, for example, when violating the laws on taxes and fees. In this article, we will study where to include tax fines in accounting, as well as the main entries for the accrual and payment of penalties, fines for taxes: profit, VAT, insurance premiums.

Reasons for accruing tax penalties

There are several reasons for accruing fines and penalties in accounting:

- Late submission of the report;

- Payment of tax and insurance premiums within unspecified terms;

- Understatement of tax liability.

Fine and penalty: what are their differences?

It should be noted that a fine and a penalty are different concepts:

- The fine is assessed immediately when the above reasons occur. In addition, its size is clearly regulated by deadlines at the legislative level.

- A penalty is a penalty payment that is charged for each day of late payment as a percentage of 1/300 of the refinancing rate of the Central Bank of the Russian Federation.

The procedure for collecting taxes and penalties from organizations:

Displaying tax penalties in accounting

To display the costs incurred that arise when fines and penalties are calculated, account 99 Profit and loss is used. For convenience, it is divided into two subcontos - penalties and fines. The debit of this account corresponds with the corresponding tax payment, which is displayed on the credit of accounts 68 and 69.

There are opinions in accounting circles that account 91 Other expenses can also be used to display accrued penalties and fines. However, in this case, a permanent tax liability arises, which somewhat complicates the process of accounting for them.

In addition, if accrued penalties and fines are displayed on 91 accounts, this will lead to a decrease in the tax base and will violate the authenticity of the information provided in the financial indicators of the organization.

Important! Penalties and fines recognized in accounting are not reflected in tax accounting, and therefore will not reduce your tax liability in any way.

Get 267 video lessons on 1C for free:

Typical entries for the accrual and payment of fines and penalties for taxes

| Account Dt | Kt account | Transaction amount, rub. | Wiring Description | A document base |

| Accounting for fines and penalties on taxes on the account. 99 | ||||

| 99-1 | 68-4 (68-2, 68-1) | 19 000,00 | A fine was assessed for non-payment of tax (95,000.00*20%) | Buh. reference |

| 99-2 | 68-4 (68-2, 68-1) | 574,75 | A penalty has been charged for late payment of taxes. The delay was 22 days | Buh. reference |

| 68-4 (68-2, 68-1) | 51 | 19 574,75 | Payment of accrued fines and penalties for taxes | Plat. order |

| Accounting for fines and penalties on taxes on the account. 91 | ||||

| 91 | 68-4 (68-2, 68-1) | 574,75 | A penalty has been charged for late payment of taxes. The delay was 22 days | Buh. reference |

| 99-1 | 68-4 (68-2, 68-1) | 19 000,00 | A fine was assessed for non-payment of tax (95,000.00*20%) | Buh. reference |

| 68-4 (68-2, 68-1) | 51 | 19 574,75 | Payment of accrued fines and penalties for taxes | Plat. order |

| Accounting for fines and penalties on insurance premiums on the account. 99 | ||||

| 99-1 | 69 | 8 000,00 | A fine was assessed for non-payment of the insurance premium (40,000.00*20%) | Buh. reference |

| 99-2 | 69 | 275,00 | A penalty has been charged for late payment of the insurance premium. The delay was 25 days | Buh. reference |

| 69 | 51 | 8 275,00 | Payment of accrued fines and penalties on insurance premiums | Plat. order |

| Accounting for fines and penalties on insurance premiums on the account. 91 | ||||

| 91 | 69 | 275,00 | A penalty has been charged for late payment of the insurance premium. The delay was 25 days | Buh. reference |

| 99-1 | 69 | 8 000,00 | A fine was assessed for non-payment of the insurance premium (40,000.00*20%) | Buh. reference |

| 69 | 51 | 8 275,00 | Payment of accrued fines and penalties on insurance premiums | Plat. order |

| Imposition of a fine identified during an inspection | ||||

| 99 | 76 | 30 000,00 | Accrual of an administrative fine for non-use of cash registers for cash payments | Protocol |

| 76 | 51 | 30 000,00 | Payment of an administrative fine | Plat. order |

| Additional assessment of taxes and social contributions, payment of taxes and penalties | ||||

| 99 | 68-4 | 10 000,00 | Additional income tax accrual | Buh. reference |

| 90 (91) | 68-2 | 25 000,00 | Additional charge of underestimated VAT | Buh. reference |

| 20 (26, 44, 91) | 69 | 30 000,00 | Additional payment of insurance premium | Buh. reference |

| 91 (20, 26) | 68 | 15 000,00 | Additional assessment of property tax, land tax, transport tax | Buh. reference |

| If VAT is not restored | ||||

| 19 | 68-2 | 25 000,00 | Additional charge of underestimated VAT | Buh. reference |

| 91 | 19 | 25 000,00 | Inclusion of recovered VAT in expenses | Buh. reference |

| Input VAT was incorrectly accepted (reporting not signed) | ||||

| 68 | 19 | 47 000,00 | Additional VAT calculation | Buh. reference |

| 20 (26, 44, 90, 91) | 19 | 47 000,00 | Writing off input VAT on expenses | Buh. reference |

| 01 (04, 10, 41) | 19 | 47 000,00 | Inclusion of input VAT in the cost of the object | Buh. reference |

| 20 (26, 44) | 02 (05) | 7 000,00 | Additional depreciation charge for the amount of input VAT | Amor. statement |

| Input VAT was incorrectly accepted (the reporting was signed) | ||||

| 19 | 68 | 4 700,00 | Additional VAT calculation | Buh. reference |

| 91 | 19 | 4 700,00 | Writing off input VAT on expenses | Buh. reference |

| 01 (04, 10, 41) | 19 | 4 700,00 | Inclusion of input VAT in the cost of the object | Buh. reference |

| 20 (26, 44) | 02 (05) | 700,00 | Additional depreciation for the current year for the amount of input VAT | Amor. statement |

| 91 | 02 (05) | 320,00 | Additional depreciation for the past year in the amount of input VAT | Amor. statement |

Add a comment Cancel reply

You must be logged in to post a comment.

This site uses Akismet to reduce spam. Find out how your comment data is processed.

If an organization or individual entrepreneur does not pay its taxes on time, in addition to the overdue amount of debt, such taxpayers will have to pay penalties. A penalty is an amount of money that must be paid in excess of the amount of overdue taxes (Clause 1, Article 75 of the Tax Code of the Russian Federation). But it happens that the payment of penalties is also provided for in business contracts (for example, a purchase and sale agreement). We will tell you in our consultation what kind of entries are formed in accounting when calculating penalties.

Accounting for penalties in accounting

In accordance with the Chart of Accounts (Order of the Ministry of Finance dated October 31, 2000 No. 94n), the amounts of tax penalties due are reflected in the debit of account 99 “Profits and losses” in correspondence with the account for accounting settlements with the budget for taxes.

Therefore, if an organization was assessed penalties on taxes, then the accounting entry will be as follows:

Debit account 99 – Credit account 68 “Calculations for taxes and fees”

Moreover, since analytical accounting for account 68 is carried out by type of tax, the credit of this account indicates the type of tax for which penalties were accrued.

So, when calculating penalties for value added tax, the posting will be as follows:

Until 2010

In letter No. 03-02-07 of the Ministry of Finance, the legislator separated the concepts of “declaration” and “advance calculation”. The taxpayer had to provide two different documents to the Federal Tax Service. This was contrary to Art. 119 of the Tax Code of the Russian Federation.

In the Presidium of the Supreme Arbitration Court No. 71, the arbitration court ruled that it is impossible to levy a fine for late submission of an advance payment calculation. But the inspectors had a different opinion on this matter. The basis for tax calculations is the amount calculated in the declaration. A fine will be charged for late submission. But! In ch. 215 of the Tax Code of the Russian Federation does not relate the imposition of a fine to the payment of tax. That is, the basis for applying sanctions may be untimely filing of a declaration for any period, regardless of whether an advance payment was made or not. Until 2010, arbitration courts also did not have a common point of view on this issue.

Current position

The situation changed when Resolution No. 57 was published by the Supreme Arbitration Court in August 2013. It provided clarifications on all controversial issues. The Tax Code specifies inconsistencies between tax and advance payment. At the same time, in Art. 80 shows the distinction between two documents - a declaration and an advance payment calculation. In Art. 119 does not stipulate liability for failure to submit a declaration for calculating the advance payment, regardless of what this document is called in the Tax Code of the Russian Federation. These clarifications are mandatory for arbitration courts. For all other bodies they are advisory in nature.