The balance sheet is not only one of the main forms of financial reporting, but also contains important methodological prerequisites that determine the accounting methodology.

The balance sheet as a reporting form characterizes the state of economic assets in terms of their composition and sources of formation in cash as of a certain date.

The funds represented in the asset undergo a continuous circulation, consisting of a countless number of various technological and organizational business operations that form the processes of acquisition and procurement of material resources, their processing, production and sale of finished products. The more actively the funds pulsate in the circulation, the faster they turn around, the more rationally they are used and the more economically efficient the enterprise operates, since each turn in the circulation not only reimburses the funds spent, but also makes a profit.

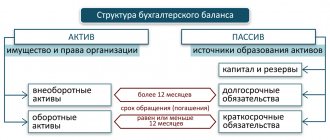

Balance sheet assets

Due to the different nature of participation in the circulation, economic assets are divided into current and non-current assets. The difference between them is not that some of them participate in the turnover and others do not, but in how they participate in it. Working capital, as it is consumed, enters circulation in its entirety, changing its form, transforming from one type to another - from cash into reserves of raw materials, from raw materials as they are processed into parts, semi-finished products and finished products, finished products for sale - in cash, etc.

Non-current assets , in the form of buildings, structures, machinery, equipment and other tangible objects of fixed assets or intangible assets, as well as other long-term investments, serve for a long time, wear out gradually and, as parts wear out, gradually enter into circulation. Their turnover becomes slow and takes a long time, so they are allocated in the balance sheet in a special section called “Non-current assets”

Since the funds in the balance sheet assets are grouped in order of accelerating turnover or increasing the level of liquidity - from fixed assets to inventories and cash, the second section of the balance sheet assets is “Current assets”.

What is included in equity capital on the balance sheet: calculation according to the Ministry of Finance

If we take into account that net assets are essentially equivalent to equity capital on the balance sheet, this will allow us to determine their essence based on the criteria given in Russian legal regulations. There are quite a lot of relevant documents. Among those that are most widely used is Order No. 84n of the Ministry of Finance of Russia dated August 28, 2014.

Read more about the provisions of Order No. 84n of the Ministry of Finance.

In accordance with the method of the Ministry of Finance, the structure of assets accepted for calculating equity capital must contain absolutely all assets, with the exception of those that reflect the debt of the founders and shareholders for contributions to the authorized capital of the company.

In turn, obligations must also be taken into account, except for some future income, namely those associated with receiving assistance from the state, as well as the gratuitous receipt of this or that property.

Balance Liabilities

Sources in the liability are divided into own and attracted . Own sources belong to the enterprise itself and are presented in the first section of the liability in the form of capital and reserves, and attracted, that is, borrowed or arising during settlement relations in the form of credit debt, in the next two sections. Those attracted , depending on their repayment period, are divided into long-term and short-term liabilities. This determines the structure of the balance sheet liability and the sequence of placement of sources of economic funds in it.

This construction of a balance sheet makes it possible to create a clear idea of the volume, structure and state of the enterprise’s funds, the availability of their own and attracted sources to cover them, as well as the financial results and their use. This information is extremely important for investors, creditors, suppliers, buyers, government financial and tax authorities and all other users of financial statements, as it allows assessing the profitability of the enterprise, its solvency, the condition and efficiency of the use of resources, credit and settlement relationships, viability and business efficiency.

What can result from reflecting negative net assets on the balance sheet?

A company must be liquidated if its net assets are negative for 2 years in a row.

As you can see, the consequences can be very serious. Moreover, it is not the company's choice or right. In fact, it no longer depends on her whether she will decide on liquidation or not. The company will be forcibly liquidated. All companies report net asset value as part of their annual financial statements. Joint-stock companies are required to record their value on the Fedresurs.ru website in the public domain. The liquidation will be carried out by the tax authorities on the basis of the relevant Federal Law No. 934-I of March 21, 1991. The very form in which the company is organized does not play a role in this case. The procedure will be initiated by the control agency in court.

However, before the expiration of the 2-year period, the company can carry out preventive measures aimed at preventing liquidation. This may be a decision to reduce the authorized capital, as required by the provisions of the Civil Code of the Russian Federation in Art. 90 for LLC and Federal Law 208 of December 26, 1995 in Art. 35 for JSC. The reduction must be formalized with notification to the company's creditors and the tax office. If the authorized capital of the company is already minimal, then in order to prevent liquidation, it is necessary to increase the value of net assets.

Rules for evaluating financial statements items

PBU 4/99 “Accounting statements of an organization” establishes rules for evaluating items of financial statements that are taken into account when preparing the balance sheet.

1. The balance sheet data at the beginning of the reporting period must be comparable with the balance sheet data for the period preceding the reporting period, taking into account the reorganization carried out, as well as changes associated with the application of PBU 1/08 “Accounting Policies”.

2. In the financial statements, offsetting between items of assets and liabilities, profits and losses is not allowed, except in cases where such offsetting is provided for by the relevant accounting provisions.

3. The balance sheet must include numerical indicators in net estimates, i.e. minus regulatory values, which must be disclosed in the notes to the balance sheet and profit and loss account. PBU 21/2008 Accounting Regulations “Changes in Estimated Indicators”, Appendix No. 2 to Order of the Ministry of Finance of the Russian Federation dated October 6, 2008 No. 106 introduced the concept of “change in estimated values.”

4. The rules for evaluating individual items of financial statements are established in the relevant accounting provisions:

— Regulations on accounting and financial reporting in the Russian Federation”, approved by Order of the Ministry of Finance of the Russian Federation dated July 29, 1998 N 34n (as amended on December 30, 1999, March 24, 2000, September 18, 2006, March 26 2007);

— PBU 1/2008 Accounting Regulations “Accounting Policy of the Organization”, Appendix No. 1 to the Order of the Ministry of Finance of the Russian Federation dated October 6, 2008 No. 106n.

5. Items in the financial statements prepared for the reporting year must be supported by the results of the inventory of assets and liabilities.

6. Assets and liabilities are reflected in the Balance Sheet depending on the timing of their circulation (repayment), divided into long-term and short-term.

What it is

Equity can be negative or positive. If the ratio is positive, it means the company has more than enough assets to cover its liabilities. If this indicator is negative, the company has debts that outweigh its assets.

In general, a company with negative equity is not considered a safe investment choice because either its total assets are too low or its total liabilities are too high. In either case, the company has more debt than its current assets can satisfy, putting them at risk of loan default and bankruptcy.

Equity is used in accounting in several ways. Often the word "equity" is used to refer to the ownership interest in a business. Examples include share capital or equity.

Sometimes capital is used to refer to a set of liabilities:

Assets = Liabilities + Equity becomes assets = Shares

Rules for evaluating balance sheet items

The organization's funds are reflected in the balance sheet as follows:

• fixed assets - at residual value, i.e. at the actual costs of their acquisition, construction and production minus accrued depreciation; • intangible assets - at residual value, i.e. at actual acquisition costs, including costs of bringing them to a state in which they are suitable for use for the intended purposes, minus accrued depreciation; • unfinished capital investments—at actual costs for the developer (investor); • equipment—at the actual cost of acquisition; • financial investments (investments in securities, in the authorized capital of other enterprises, bonds, loans provided, etc.) - at actual costs for the investor; • material assets (materials, fuel, spare parts, containers and other material resources) - at their actual cost; • work in progress - at actual production cost (in mass and serial production - at standard (planned) cost or at direct costs, or at the cost of raw materials, materials and semi-finished products); • distribution costs - in the amount of costs attributable to the balance of unsold goods in trade and public catering organizations; • deferred expenses - in the amount actually incurred in the reporting period, but relating to the following reporting periods; • finished products - at actual or standard (planned) production cost; • goods - at the cost of their acquisition; • goods shipped, work delivered and services provided - at full actual or standard (planned) cost; • accounts receivable—in the amount recognized by debtors; • balances on foreign currency accounts, other funds (including monetary documents), securities, receivables and payables in foreign currencies—in rubles, determined by converting foreign currencies at the exchange rate of the Central Bank of the Russian Federation effective on the last day of the reporting period. The organization's sources of funds are reflected in the balance sheet: • authorized capital - in the amount determined by the constituent documents; • reserve capital—in the amount of unused funds of this capital; • reserves for doubtful debts - in the amount of reserves created at the end of the reporting year to cover the organization's receivables; • reserves to cover future expenses - in the amount of unused reserves during the year and in the amount of reserves carried over to the next year - in the balance sheet at the end of the reporting year; • deferred income - in the amount received in the reporting period, but relating to the following reporting periods; • financial result of the reporting period—as retained earnings (uncovered loss), i.e., the final financial result identified for the reporting period, minus taxes and other similar payments due from profits, including sanctions for non-compliance with tax rules; • accounts payable - in the amounts of actual debts to creditors.

Calculation methods

All the information needed to calculate a company's equity is available on its balance sheet. The calculation involves determining the companies' total assets and total liabilities, including current and long-term assets.

Current assets include retained earnings, stockholders' equity, and other cash held in bank and savings accounts, stocks, bonds, and money market accounts.

Long-term assets include equipment, property, illiquid investments and vehicles. Current liabilities include any payments and interest on loans in the current year, accounts payable, wages, operating expenses and insurance premiums.

Long-term liabilities include any debts that are not due in the current year, such as mortgages, loans and payments to bondholders.

Own capital is reflected in line 1300 of the balance sheet. The traditional calculation is as follows:

Equity = value in line 1300

Shareholders' equity can also be expressed as a company's share capital plus retained earnings, less the value of treasury shares. However, this method is less common. Although both methods should produce the same figure, using total assets and total liabilities provides a clearer indication of a company's financial health.

According to Order of the Ministry of Finance of Russia No. 84n, that net assets and equity capital are the same thing, their essence can be determined based on the criteria of Russian regulatory legal acts.

In turn, obligations must also be taken into account, except for some future income, namely, those associated with receiving assistance from the state, as well as the gratuitous receipt of certain property.

Calculation of net assets, and therefore equity capital according to the Ministry of Finance method, assumes information from lines 1400, 1500 and 1600 of accounting. balance.

You will also need information showing the amount of debts of the founders of a business company (DUO), if any (they are reflected by posting Dt 75 Kt 80), as well as deferred income, or DBP (account credit 98).

- The structure of the formula for determining net assets and at the same time equity capital is as follows: (Line 1400 + line 1500)

- Next, you should subtract from the resulting number the amount that corresponds to the credit of account 98.

- Next, calculate the indicators on line 1600 according to the posting Dt 75 Kt 80.

- From point 3, point 2 is calculated.

Thus, the formula for determining the value of the insurance premium using the Ministry of Finance method will look like this:

Sk = (line 1600 – DUO) – ((line 1400 + line 1500) – DBP)

By comparing specific numbers that reflect everything a company owns and all its liabilities, the net worth equation reveals a clear picture of a company's financial health that is easily interpreted by laymen and professionals alike.

In accordance with the method of the Ministry of Finance, the structure of assets accepted for calculation must contain absolutely all assets, with the exception of those that reflect the debt of the founders and shareholders for contributions to the authorized capital of the company.

Change in estimates

PBU 21/2008 introduced a new concept of “change in estimated values”, which is understood as an adjustment to the value of an asset (liability) or a value reflecting the repayment of the value of an asset, due to the emergence of new information, which is made based on an assessment of the current state of affairs in the organization, expected future benefits and obligations and does not constitute a correction of an error in the financial statements.

In this case, the estimated value is:

the amount of reserve for doubtful debts, reserve for reduction in the value of inventories, other valuation reserves,

- useful lives of fixed assets, intangible assets and other depreciable assets,

- assessment of the expected receipt of future economic benefits from the use of depreciable assets, etc.

- A change in the way assets and liabilities are measured is not a change in accounting estimates.

If any change in accounting data cannot be clearly classified as a change in accounting policy or a change in an estimated value, then for the purposes of financial reporting it is recognized as a change in the estimated value.

A change in the estimated value is subject to recognition in accounting by including in the income or expenses of the organization (prospectively):

- the period in which the change occurred, if such a change affects the financial statements only for this reporting period;

- the period in which the change occurred, and future periods, if such a change affects the financial statements of this reporting period and the financial statements of future periods.

A change in the estimated value that directly affects the amount of the organization's capital is subject to recognition by adjusting the corresponding capital items in the financial statements for the period in which the change occurred.

In the explanatory note to the financial statements, the organization must disclose information about changes in the estimated value.

Why does negative income tax appear?

There are several reasons for the occurrence of negative tax values. Here are some of them:

- the most common case is a negative tax for a newly created organization . This is understandable: even if the company has already concluded several contracts and successfully fulfilled their terms, it may well be that revenue from them will appear only after the reporting period. Accordingly, the company remains at a loss;

- wrong strategic choice of the company. If the management of an enterprise, when choosing a direction of activity, did not take into account all the possible pitfalls and obstacles to long-term development, then perhaps at some stage the company will slide into losses instead of profits;

- illiterate, unprofessional accounting . Sometimes accountants, out of ignorance or due to low qualifications, reflect the income and expenses of an enterprise in such a way that a negative balance arises.

In general, many factors, both external and internal, can lead to a negative income tax. But regardless of the reason for its appearance, it is worth thinking about how to improve the indicators, since a negative tax base always raises a lot of questions from representatives of the tax authorities.

Which line of the balance sheet contains the equity indicator

Calculating equity capital in the balance sheet using the Ministry of Finance method is a procedure that involves using data from the following sections of the balance sheet:

- lines 1400 (long-term liabilities);

- lines 1500 (current liabilities);

- lines 1600 (assets).

Also, to calculate equity capital, you will need information showing the amount of debts of the founders of a business company (let’s agree to call them DOO), if any (they correspond to the debit balance of account 75 as of the reporting date), as well as deferred income, or DBP (account credit 98 ).

For information on what kind of transactions are reflected in the accounting operations of the insurance company, read the material “Procedure for accounting for the equity capital of an organization (nuances).”

The structure of the formula by which net assets and at the same time equity capital in the balance sheet are determined is as follows. Necessary:

- Add the indicators along lines 1400, 1500.

- Subtract from the number obtained in paragraph 1 those that correspond to the credit of account 98 (for income in the form of assistance from the state and gratuitous receipt of property).

- Subtract the debit balance of account 75 from the number on line 1600.

- Subtract the result obtained in step 2 from the number obtained in step 3.

Thus, the formula for equity capital according to the Ministry of Finance will look like this:

Sk = (line 1600 – DUO) – ((line 1400 + line 1500) – DBP).

For information about who should apply this calculation procedure and how its result is formalized, read the article “The procedure for calculating net assets on the balance sheet - formula 2018-2019.”

Indicator value

Solvency is to counterparties

on time and in full With its help, the financial condition of the organization is determined. The concept is closely related to indicators of creditworthiness and liquidity. However, there are some nuances that distinguish all three coefficients:

- creditworthiness characterizes the ability of an enterprise to repay debts using short-term and medium-term assets, that is, property such as buildings and structures is not taken into account in calculations;

- liquidity is the ability to meet only short-term obligations;

- Solvency reflects the ability to cover debts using all assets.

It comes in two types:

- Long-term . It represents an opportunity to pay off obligations that are expected to be paid within a period of more than a year. At the same time, the analysis evaluates a number of indicators: the net capital of the organization;

- debt repayment schedule;

- debt/equity ratio;

- interest coverage.

To monitor the ability to repay debts, a company must regularly analyze its overall solvency ratio. Calculations are carried out according to accounting data monthly or quarterly. The company independently chooses the frequency of assessment, taking into account the amount of debt, the size of turnover and other individual characteristics.

The calculation of the indicator is very important for the efficiency of making management decisions, since a decrease in the level of solvency in the future leads to the risk of bankruptcy.

You can learn more about this concept from the following video:

What's behind the articles?

Let's briefly look at what is hidden behind this or that balance sheet item.

The article “Non-current assets” includes:

— intangible assets (IA): copyrights, patents, trademarks, licenses, R&D, expenses for creating an organization, business reputation;

— fixed assets: land, natural resources, buildings, structures, equipment, various instruments and devices, computer technology, transport, tools, inventory, etc. According to accounting rules, assets worth up to 20 thousand rubles. allowed not to be included in fixed assets. This provides direct savings on property tax (assets do not fall into the tax base) and indirect savings on income tax (the cost of assets is immediately written off as expenses, and not gradually through depreciation);

— construction in progress: costs of constructing facilities before they are put into operation, equipment requiring installation;

— profitable investments in material assets: property intended for leasing or rental;

— long-term financial investments: securities, deposits, loans provided, contributions to authorized capital;

— deferred tax assets (DTA): the amount by which income tax will be reduced in subsequent periods due to discrepancies between accounting and tax accounting. For example, a loss from the sale of fixed assets is taken into account in accounting immediately, and in tax accounting - gradually, which leads to the emergence of a loss;

— other non-current assets: long-term accounts receivable, long-term deferred expenses, incomplete R&D.

The term “Current assets” means:

— inventories: building materials, structures, parts, fuel, costs of electricity, steam, water, purchased semi-finished products, components, spare parts, construction and installation work performed, manufactured building materials. Inventories are shown excluding value added tax (VAT). VAT is reflected separately under the relevant item;

— accounts receivable: debt of buyers, suppliers, customers, contractors, budget, employees, as well as other debtors (issued interest-free loans, discounted interest-free bills);

— short-term financial investments: securities for resale, short-term deposits, loans provided;

— cash: balances of Russian and foreign currency in the cash register, on current accounts, in collections;

- other current assets: shortages and losses, amounts of taxes for which no decision has been made on offset (refund) from the budget, amount of VAT on advances paid.

The article “Capital and reserves” includes:

— authorized capital: the amount of authorized capital registered in the constituent documents. The size of the authorized capital should not be less than the value of the net assets (equity) of the organization. Otherwise, we may be talking about the pre-bankruptcy state of the organization. When equity becomes a negative value (the organization has no net assets free from liabilities), then we have a bankrupt balance sheet;

- own shares purchased from shareholders: counter-liability, it reduces the total of the “Capital and Reserves” section and is therefore indicated in parentheses. Shares are shown at actual redemption price;

— additional capital: increase in the value of non-current assets as a result of revaluation, share premium from the sale of own shares at a price above their par value;

— reserve capital: reserve fund and other funds created in accordance with the organization’s charter. Funds created in accordance with the legislation on joint stock companies and unitary enterprises are also taken into account here. Examples of reserve funds: a fund for the payment of dividends on preferred shares, a fund for the repurchase of own shares from shareholders;

— retained earnings (uncovered loss) — the balance of net profit minus taxes; uncovered loss. It is because of losses that the amount of the organization’s own funds may be lower than the authorized capital.

The article “Long-term liabilities” includes:

— loans and credits: attracted long-term (repayment period over a year) loans and borrowings, issued bills of exchange, issued bonds;

— deferred tax liabilities (DTL): the amount by which the income tax will be increased in subsequent periods, arising due to discrepancies in accounting and tax accounting. For example, in accounting, interest on a loan taken for the purchase of fixed assets increases the cost of these fixed assets, but in tax accounting they are written off immediately, which leads to the emergence of IT;

— other long-term liabilities: debt to suppliers, contractors, customers with a repayment period of more than a year.

Finally, the item “Short-term liabilities” includes:

— loans and credits: debt on received loans and credits with a repayment period of no more than a year, issued loans and bonds. It should be noted that according to accounting rules, as maturity dates approach, the transfer of debt from long-term to short-term is not carried out;

— accounts payable: short-term accounts payable in accordance with the breakdown given in the balance sheet;

— debt to participants that arises during the period when a decision on the payment of dividends has been made but not yet executed;

— future income: upcoming revenues for shortfalls, targeted financing funds;

— reserves for upcoming expenses: reserves for vacation pay, for payment of remuneration for long service, based on the results of work for the year, for the repair of fixed assets, for warranty repairs and warranty service, for performing seasonal landscaping and asphalting work, for covering unforeseen expenses, etc. .;

- other short-term liabilities - targeted financing received by development organizations from investors and generating an obligation to transfer the constructed facility to them within 12 months, special-purpose funds.

Negative balance regulation: CySEC and FCA

The UK financial regulator, the Financial Conduct Authority (FCA), requires all Forex brokers under its jurisdiction to comply with the provisions of the negative balance protection policy.

The regulator is developing a framework that ensures that Forex and CFD brokers are committed to covering a certain percentage of the risk for investors.

The FCA will require firms that do not wish to comply with negative balance protection and guaranteed stop loss policies to use their capital to cover potential risks.

The Cyprus financial regulator, the Cyprus Securities and Exchange Commission (CySEC), announced its position on this issue on 18 September 2021.

According to CySEC, protection for the firms it oversees can only be established on a per-account basis. Therefore, a trader operating more than one account with a broker may have funds from another account to cover his negative balance in another account. However, no trading account can enter negative territory.