Making changes in the current tax period

The procedure for making changes to the purchase book is regulated by the Decree of the Government of the Russian Federation “On the forms and rules for filling out (maintaining) documents used in calculations of value added tax” dated December 26, 2011 No. 1137 (hereinafter referred to as the Rules).

If you make changes before the end of the tax period, then in the purchase book:

- cancel the erroneous invoice (adjustment invoice) - write it down in the purchase book with negative cost values;

- then register the corrected (corrected adjustment) invoice with positive correct values (clause 9 of Appendix 4 to the Rules).

Thus, to correct errors in the sales book in the current quarter, you do not need to draw up an additional sheet - correct erroneous entries directly in the purchase book.

This method of making adjustments has not previously been denied by tax authorities. We informed you about this on our website: see details here.

Why should a seller or buyer cancel invoices and how to do it correctly, find out here.

Answers to crossword of the day No. 22925 from Odnoklassniki

22924 22926

Horizontally: - Additional sheet in the book - Strands of hair with springs - A man from the bottom - Nickname of a calf from the cartoon Vacation in Prostokvashino - Criterion in the Russian way - Soviet president - Processing until ready - The lowdown for the personnel department - The good soldier from the poem by A. Tvardovsky - Crushed cereals - Harmless to humans shark - Coniferous crossbill in rhyme with the flywheel - 45th President of the USA - Folk hero of the Georgian epic - Ancient Rome as a state - Pre-revolutionary Suvorov officer - Casting for beauty queens - What can be made from the word “rotunda” by rearranging the letters

Vertical: - Southern neighbor of the Chinese and Japanese - The most popular device at the nuclear power plant - Profit, self-interest, gamble - Finnish folklorist - “Cord” on which the gymnast sits - Italian painter ... da Vinci - Vakula (Gogol) went after them - Wonderful River not for rare birds - Eastern sweetness rahat-.. - Sister of the elusive Danka - Church rite of remembrance of the deceased - “Hat” for a lamp - A well-known brand of good tea - The old name of a thief and villain - Wine of Italian bottling - What word can be “obtained” by rearranging just one letter in the word “vice” – Financial audit – Fishnet boa constrictor

INSERT - That which is inserted into something. as a supplement, application.

PLEBEIAN - 1. A person from the lower strata of the free (not enslaved) population, who initially did not enjoy political and civil rights (in Ancient Rome). 2. transfer decomposition A person of non-aristocratic origin, coming from the lower classes.

MEASUREMENT Wed. decomposition 1. Something that is used to measure something. 2. That which serves as the basis for evaluating, measuring something. or comparison with something; criterion.

COMPLETION - 1. Action according to the meaning. verb: to finish, to finish, to finish, to finish. 2. What is completed is the result of completion.

QUESTIONNAIRE - 1. Questionnaire for obtaining something. information compiled in a specific form. 2. decomposition Someone's biographical information. 3. decompression Same as: survey.

SECTION - 1. Action according to the meaning. verb: to cut. 2. A tool for chopping cabbage or other vegetables; hoe. 3. Crushed cereal. 4. local Finely chopped straw with flour and bran, used as livestock feed.

KATRAN - A plant of the cruciferous family with large leaves and numerous white flowers.

KATRAN is a shark that lives in the Pacific and Atlantic oceans, as well as in the Black, Barents and Far Eastern seas.

EMPIRE - 1. A monarchical state headed by an emperor or empress. 2. transfer decomposition A large monopoly that exercises control over something. branch of production or over smb. activities.

CADET - A student of a cadet school.

CADET - Member of the Constitutional Democratic Party.

COMPETITION - 1. Competition with the aim of identifying the most worthy participants or the best works from among those presented. 2. A special commission that considered the claims of creditors against an insolvent debtor and disposed of his property (in the Russian state until 1917 and some countries). // Temporary management of the debtor's affairs.

KOREAN - see Koreans.

DOSIMETER - A device for measuring the dose of radioactive radiation.

BENEFIT - 1. Profit, income derived from something. 2. Benefit, use, personal interest. // The advantage of one over the other.

TWINE - Twisted or spun thread used for wrapping, tying or stitching; twine.

SPLIT - A figure in gymnastics, acrobatics, figure skating, etc., during which the athlete, spreading his legs, forms one straight line with them.

CHEREVIKI pl. local 1. Women's boots (usually pointed and high heels). // Any women's shoes. 2. Leather work shoes.

FRIZNA - 1. The final part of the funeral rite of the ancient Slavs, accompanied by war games, competitions, and also a funeral feast. 2. Church ritual of funeral or commemoration of the deceased. // Ritual meal with wine in memory of the deceased after the funeral or on the anniversary of his death; wake. 3. transfer outdated A sad memory of someone or something. lost, dead.

LAMPSHAD - 1. Part of a lamp, usually in the form of a cap, designed to concentrate and reflect light and protect the eyes from its influence. 2. outdated A visor worn over the forehead to protect the eyes from light exposure.

VARNAK - 1st local Convict or former convict. 2. up-down Scoundrel, villain.

CHIANTI avg. several Grape wine produced in Italy.

PYTHON - A large non-venomous snake of the boa constrictor family, living mainly in the jungle.

Making changes at the end of the tax period

If you need to correct errors in the purchase book for an already ended quarter:

- draw up an additional sheet of the purchase book for the tax period in which the invoice requiring correction was registered (clause 4 of Appendix 4 to the Rules);

- submit an updated VAT return, pay additional tax and penalties if, as a result of errors in the purchase book, the amount of the tax deduction turned out to be overstated (Clause 1, Article 1 of the Tax Code of the Russian Federation).

The updated version of the Rules for maintaining an additional list for the purchase book has established a beneficial option for taxpayers for reflecting changes: the corrected invoice can be registered in the period when the primary invoice was received. In clause 6 of the Rules for maintaining an additional list for the purchase book, an algorithm for calculating the indicator using the “Total” line is now prescribed:

TOTAL0 = TOTAL0 – ASF + ISF

where: TOTAL0 is the indicator of the “Total” line of the additional list of the purchase book for the tax period in which the invoice was registered before corrections were made to it;

TOTAL0 — indicator of the “Total” line;

ASF - indicators of invoices subject to cancellation;

ISF - indicators of registered invoices (including adjustment ones) with corrections made to them.

Find out how to distinguish a corrected invoice from an adjustment one from the materials:

- “What is an adjustment invoice and when is it needed?”;

- “When is a corrected invoice used?”.

EXPLANATIONS from ConsultantPlus: In the fourth quarter of 2019, when purchasing fruit under an import contract, a VAT deduction was declared in the purchase book on the goods declaration at a rate of 20%. In May 2021, a decision was received from the customs authority to make changes and (or) additions to the information specified in the goods declaration at a rate of 10% for this transaction due to changes in legislation establishing the VAT rate on fruit from October 1, 2019 The decision was formalized by the customs authority. How should this be reflected in the purchase ledger? If you do not have access to the K+ system, get a trial online access for free.

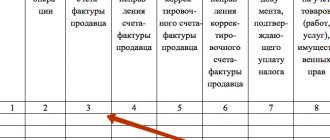

Form of an additional sheet of the purchase book and rules for filling it out

The form of the additional sheet of the purchase book and the rules for filling it out are established in Appendix 4 to the Decree of the Government of the Russian Federation dated December 26, 2011 No. 1137.

Additional sheets of the purchase book are an integral part of the purchase book.

The procedure for preparing an additional sheet for the purchase book:

- Transfer the final data to the “Total” line (clause 2 of the Rules for filling out an additional sheet of the purchase book):

- from column 16 of the purchase book for the tax period in which the erroneous invoice was registered (including an adjustment one), if additional sheets for this purchase book were not issued;

- from column 16 of the last completed additional sheet of the purchase book for the tax period in which an erroneous invoice (including an adjustment) was registered, if there are already additional sheets for this purchase book.

- On the line in columns 1 to 16, write down the indicators of the canceled erroneous invoice (adjustment invoice), while the indicators in columns 15 and 16 are reflected with a negative value (clauses 3, 5 of the Rules for filling out an additional sheet of the purchase book ). When canceling an entry on an advance invoice, columns 8 and 13 of the additional sheet are not filled in (clause 4 of the Rules for filling out an additional sheet of the purchase book).

- In the “Total” line, summarize the results in column 16 (from the indicators in the “Total” line, subtract the indicators of the records of the erroneous invoice (adjustment invoice) and to the obtained result, add the indicators of registered invoices (including adjustment ones) with those included in them corrections) (clause 6 of the Rules for filling out an additional sheet of the purchase book).

The indicators in the “Total” line are used to make changes to tax reporting previously submitted to the tax authority (clause 1, article 81 of the Tax Code of the Russian Federation, clause 6 of the Rules for filling out an additional sheet of the purchase book).

Highlights ↑

Today, the legislative level has fixed the point according to which it is necessary to generate special invoices when purchasing goods subject to value added tax.

All data about them, as well as other information, must be entered into a special purchase book. It is not recommended to make mistakes in this document.

To avoid this type of incident, you should study the following points in as much detail as possible:

- definitions;

- who needs to lead;

- legal grounds.

Definitions

The purchase ledger is used to store invoice information.

These documents represent legal confirmation of payment of value added tax upon acquisition:

- any services;

- goods.

Also, invoices are subsequently used to determine the amount of the deduction, if its use does not contradict current legislation.

Documents should be indicated in the appropriate section of the book not at the time of their formation, but only when the buyer’s ownership of the goods or services has become valid and realized.

The format for maintaining a purchase ledger is specified in the current legislation - Government Decree No. 1137 of December 26, 2011.

Please remember that the following invoices cannot be recorded in the purchase ledger:

- if goods or any services were transferred free of charge;

- if any currency was purchased through a broker on a financial exchange;

- if the goods or services were received by the sales agent from the principal (committent) for sale;

- reflecting the commissions received by the intermediary during the sale.

It should not be assumed that the above transactions are not included in the declaration. This is an error, if allowed, the person forming it will need to make clarifications.

Who needs to lead

A purchase book must be kept by everyone who purchases goods and services on which they are required to pay value added tax.

VAT payers can be:

- individual entrepreneurs;

- all kinds of organizations;

- individuals transporting goods across the border of the Russian Federation;

- organizations of foreign origin selling their products or services in Russia.

The list of those not paying VAT includes:

- entrepreneurs and legal entities working under a simplified taxation scheme;

- transferring to the budget UTII - a single tax on imputed income;

- enterprises and individual entrepreneurs whose profits for three consecutive months did not exceed 2,00,000 rubles.

The list of exceptions does not apply to excisable goods. All the most important points regarding value added tax are indicated in Article No. 143 of the Tax Code of the Russian Federation.

Legal grounds

The purchase book, as well as various related materials (additional sheet and others), must be submitted on the basis of Order of the Federal Tax Service No. ММВ-7-3 / [email protected] dated 10.29.14.

This order also specifies the formats of documents that must be submitted to the Federal Tax Service.

VAT payers who create a purchase book must study the following materials:

- Chapter No. 21 of the Tax Code of the Russian Federation.

- Decree of the Government of the Russian Federation No. 914 of December 2, 2000

- Decree of the Government of the Russian Federation No. 451 of May 26, 2009

It is also important to remember that the book of purchases from 2021 must be reflected in section No. 8 of the declaration submitted to the tax service (but only for VAT).

This is interesting: What guarantees and compensations are provided to employees in Russia

Previously, it was acceptable to create this document on a simple paper medium. Today this is not allowed.

The sales book, as well as an additional sheet to it, should be saved in .xml format. It is transmitted via special telecommunication channels, through a gateway.

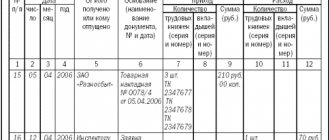

Example of designing an additional sheet of a purchase book

An example will help you understand how to fill out an additional sheet for the purchase book.

Example

In March 2021, Mechta LLC shipped products worth RUB 368,000 to PJSC Fantasia. (including VAT = 61,333.33 rubles). Moreover, in the invoice the total cost was erroneously indicated in the amount of 386,000 rubles. (including VAT = 64,333.33 rubles).

The error was noticed after the end of the quarter and the submission of the VAT return for the 1st quarter.

07/08/2019 Fantasia LLC received a corrected invoice from PJSC Mechta. On the same day, the accountant of PJSC Fantasia prepared an additional sheet for the purchase book for the 1st quarter of 2021, in which:

Then the accountant of PJSC Fantasia filed an updated VAT return for the 1st quarter of 2021, paid additional tax and penalties - as a result of an error, the declared deduction was overstated by 3,000 rubles. (64,333.33 – 61,333.33).

How the accountant of PJSC Fantasia prepared the additional sheet, see the sample.

Adjustment of goods receipt

Based on a previously created goods receipt, you can create an adjustment document. To do this, open the previously created document No. 789 dated June 15, 2016

Purchases -> Purchases -> Receipt (act, invoice)

and using the “Create based on” button

Let's create an adjustment document:

The nomenclature now has two lines:

- before change - price and quantity of the original document

- after a change, a new price or quantity is set

Also the supplier costs us 100 rubles. increased the cost of transport):

Register entries are created for the changed amount:

After posting the adjustment document, we will register the adjustment invoice:

See also our video on adjusting sales and issuing an adjustment sales invoice:

Results

Correct erroneous entries in the purchase book differently depending on whether the quarter has ended or not. Within the quarter, make corrective entries in the purchase book itself (first cancel erroneous data by reflecting them with a minus sign, then register correct data with positive values).

If the quarter has already ended and the declaration has been sent to the tax authorities, correct the purchase book using an additional sheet to the purchase book in which the primary invoice is registered.

The procedure for filling it out is described in Resolution No. 1137. You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Generating purchase ledger entries in 1C 8.3

Reflection of transactions

- VAT is accepted for deduction on fixed assets

- VAT is accepted for deduction upon adjustment of receipts

is made by a document. You can find the purchase book using the following path:

Operations -> Closing a period -> Regular VAT operations -> Create -> Generating purchase ledger entries

By clicking the “Fill” button, we see the records of the documents we created earlier in this section. After posting the document, we receive entries in the accumulation registers:

And in the “Purchase Book” report: