Which account should deposit deposits be reflected in - 55 or 58? — Private lawyer Alexey Timofeev

admin10.15.2017 How to reflect in accounting the placement of funds on a deposit account and their return by the bank, if the bank deposit agreement stipulates that interest on the deposit is paid by the bank simultaneously with the return of the deposit amount? In accordance with the bank deposit agreement, the organization transferred funds in the amount of 2,000,000 rubles to a deposit account in the bank on March 17.

for a period of 183 days at 7% per annum. According to the terms of the agreement, interest on the deposit amount is calculated monthly on the last day of each month of the agreement, and their payment is made simultaneously with the return of the deposit amount upon expiration of the bank deposit agreement. After the expiration of the period established by the agreement (September 16), the deposit is closed, the funds placed on it and the interest accrued on the deposit are transferred by the bank to the organization’s current account.

Interim financial statements are prepared by the organization at the end of each month.

Reporting periods for income tax are one month, two months, and so on until the end of the calendar year. For income tax purposes, the accrual method is used. Content

- Question on accounting: Reflection of deposits in the balance sheet (BP 2.0.44.8)

- Accounting for deposit transactions.

Interest accrual on deposits- Interesting publications:

- Interest accrual on deposit

- Refund of a deposit

- Interesting publications:

- Accounting for funds on deposit

- Placing funds on deposit

- Corporate income tax

- Value added tax (VAT)

- Civil relations

- Accounting

Civil legal relations Under a bank deposit agreement, one party (the bank), which has accepted the amount of money (deposit) received from the other party (depositor) or received for it, undertakes to return the deposit amount and pay interest on it under the conditions and in the manner specified provided for by the contract (clause 1 of article 834 of the Civil Code of the Russian Federation).

What transactions reflect interest on a deposit?

Important

But sometimes these 11 months are not so spent. <... Income tax: the list of expenses has been expanded. A law has been signed that has amended the list of expenses related to wages. Thus, employers will be able to take into account in the “profitable” base the costs of paying for services for organizing tourism, sanatorium-resort treatment and recreation in Russia for employees and members of their families (parents, spouses and children).

<... Check employee salaries with the new minimum wage From 05/01/2018, the federal minimum wage will be 11,163 rubles, which is 1,674 rubles more than now. This means that employers who pay their employees at the minimum wage must raise their wages from May 1. <...Paying taxes has become easier. To pay personal taxes, citizens no longer have to fill out a payment order “from and to.”

You just need to enter one number. <...

Increasing capital: accounting for ruble deposits and interest on them

1.

What terms of a bank deposit agreement are most important for an accountant. 2. How to reflect the deposit and interest on it in accounting and tax accounting.

3. How to take into account the consequences of early termination of a bank deposit agreement.

Having a financial airbag, that is, a certain reserve of funds, is the “golden” rule of both personal and corporate finance. However, simply keeping the nth amount of money in reserve in your account is extremely unprofitable.

As you know, money should work and bring... money.

That is why competent managers try to place free funds in financial investments. One of the most common types of financial investments is a bank deposit, or deposit. And there are at least two reasons for this. Firstly, opening a deposit does not require special knowledge and skills in the field of investing.

And secondly, a deposit is traditionally considered one of the least risky ways to invest money (all other things being equal). What an accountant should know about the accounting for bank deposits and interest on them, and what “pitfalls” this seemingly simple operation may hide, we’ll look into this article. The main document that serves as the basis for recording a bank deposit and interest on it in accounting is the bank deposit agreement.

Checking the correctness of the contract, as well as the legal nuances and consequences of the transaction, is rather the task of a lawyer. An accountant, as a rule, is only interested in some of the terms of the contract, on which the accounting reflection of the deposit depends. So, what should an accountant pay close attention to:

- Deposit term. A bank deposit can be opened for a certain period or on demand (Clause 1, Article 837 of the Civil Code of the Russian Federation). The period for which the deposit is opened depends on the order in which it is reflected in the financial statements: as part of long-term or short-term financial investments.

- Type of deposit: replenishable or non-replenishable.

Depending

Interest on deposit: postings

One of the most common types of deposit is a deposit, hence the name “deposit”. Deposits can be placed in the form of investments in banking institutions and commercial organizations. Depositors (investors) are both ordinary citizens and enterprises. The main characteristics of any deposit are:

- It must return to its owner and this right must be guaranteed by contract.

- During the placement of a deposit, its owner must necessarily receive benefits in the form of interest accrual on the use of valuables.

The legislation of the Russian Federation considers all deposits under the guise of deposits, therefore the adopted laws and regulations use this name and stipulate: Deposit (or deposit) - securities, funds, in foreign or national currency, placed for the purpose of preserving or making a profit.

Where are short-term bank deposits reflected on the balance sheet?

this is what an auditor friend suggested: Accounting To account for the movement of funds invested by an organization in bank and other deposits, the Instructions for the use of the Chart of Accounts for financial and economic activities of organizations (approved by Order of the Ministry of Finance of Russia dated October 31, 2000 N 94n) propose using subaccount 3 “Deposit accounts" account 55 "Special accounts in banks."

The amount of funds deposited into the deposit account is at the same time recognized as a financial investment (clause 3 of the Accounting Regulations “Accounting for Financial Investments” (PBU 19/02), approved.

Order of the Ministry of Finance of Russia dated December 10, 2002 N 126n).

To account for financial investments, the specified Instruction prescribes the use of account 58 “Financial investments”. With this option, to account for deposits, it is logical to open a special sub-account 5 “Bank deposit (deposit)”. It is advisable to consolidate the use of a specific account in the accounting policy of the organization (clause

clauses 4, 7 of the Accounting Regulations “Accounting Policy of Organizations” (PBU 1/2008), approved. Order of the Ministry of Finance of Russia dated October 6, 2008 N 106n). Financial investments are accounted for at their original cost (clause

clauses 8, 9, 21 PBU 19/02), which in this case is equal to the amount of funds contributed to the deposit. Thus, when placing funds on a deposit account in a bank, the following posting is made: Debit 58-5 (55-3) Credit 51 - funds are transferred to the deposit account. Regardless of which accounting account the deposits are reflected in, information about them should be shown in the balance sheet as part of financial investments.

Let us remind you that: - line 1170 “Financial investments” of the balance sheet indicates the cost of long-term financial investments, the circulation (repayment) period of which exceeds 12 months (clause 19 of the Accounting Regulations “Accounting Statements of an Organization” (PBU 4/99), approved .

By Order of the Ministry of Finance of Russia dated July 6, 1999 N 43n, p.

41 PBU 19/02); — line 1240 “Financial investments (except for cash equivalents)” shows

Cash equivalents on balance sheet

The purpose of cash equivalents (CE) is not investment. They are used as short-term cost liabilities. These include:

- funds invested in banks and credit institutions as demand deposits; shares (preferred) of companies occupying a significant market share; bearer securities (bills) of Sberbank of the Russian Federation.

The company's shares are highly liquid securities and are classified as DE because they can be easily sold at any time at a price known in advance.

The point of purchasing cash equivalents is the ability to quickly transform them into a specified amount with benefit for the enterprise. (understand how to keep accounting records in 72 hours) > 8,000 books purchased The accounting policy of each individual organization needs to decide on the approaches that determine the separation of cash equivalents from other types of financial investments It should be based on the following characteristics: DE are part of financial investments (account 58)

Short-term financial investments are...

→ → Update: December 20, 2021 In the process of carrying out economic activities, an enterprise makes various investments aimed at generating profit.

They can be short-term or long-term. Let's take a closer look at short-term financial investments (in the balance sheet this is line 1240). In accounting and reporting, an organization's investments are classified into short-term and long-term.

Let's look at their differences. Long-term means investments for a long period (more than one year). These could be, for example:

- provision of interest-bearing loans to other organizations;

- acquisition of securities (shares, bonds, etc.) with a long maturity.

- equity participation in the capital of other organizations;

In the reporting they are indicated in line 1170 of the balance sheet.

In contrast, short-term financial investments are investments whose circulation or maturity period is one year or less. The assets in which the organization's funds are invested can be securities of other enterprises and organizations, finances in time deposit accounts of credit institutions, etc. Such assets are characterized as liquid and most easily sold.

In the reporting they are indicated in line 1240 of the balance sheet. In another way, regardless of the specific type of investment, accounting for financial investments can be briefly explained as follows. In many ways, the classification of assets into one category or another is related to the enterprise’s plans in relation to them.

For example, if an enterprise has invested in the authorized capital of another organization, it can plan various options for obtaining economic benefits for itself. This may be influence on the organization, control over it, making profit through dividends. In this case, such investments are recognized as long-term financial investments.

However, the purchased share in the authorized capital can also be resold, making a profit from just such a transaction.

Owning a share with its resale within a year is considered a liquid asset and short-term financial investment.

Accrual of interest on deposit: postings

6 PBU 23/2011):

– payments related to investing funds in cash equivalents;

– cash receipts from the repayment of cash equivalents (excluding accrued interest);

– exchange of some cash equivalents for other cash equivalents (excluding losses or benefits from the transaction).

This report, along with cash flows, reflects the balances of cash and cash equivalents at the beginning and end of the reporting period. Based on the above, it is in the balances of cash equivalents at the beginning and end of the reporting period that the registered demand deposit should be recognized in the organization’s cash flow statement.

No votes yet.

Please wait…

Short-term deposit on balance

> > Annual accounting (financial) statements (except for cases established by Law N 402-FZ) consist of a balance sheet, a statement of financial results and appendices thereto (Part.

1 tbsp. 14 of Law N 402-FZ). The reporting forms were approved by Order of the Ministry of Finance of Russia dated 07/02/2010 N 66n “On the forms of financial reporting of organizations” (hereinafter referred to as Order N 66n).

Paragraph 20 of PBU 4/99 defines the items (numerical indicators) that the organization’s balance sheet should contain.

Thus, assets accounted for under the item “Financial investments”, depending on the period of their circulation, can be reflected in the first or second sections of the balance sheet - “Non-current assets” and “Current assets”. Current assets include, among other things, financial investments with a maturity of less than 12 months.

In our case, it is the norms of PBU 19/02 that must be followed, since it came into force in 2003, and PBU 4/99 - in 2000.

Therefore, you should not classify your own repurchased shares as financial assets. In p. This is:

- quantitative accounting of assets;

- nominal (book) value;

- date of registration;

- number, series of the document;

- name of valuable assets;

- date of disposal.

According to the norms of PBU 19/02, accounting for short-term financial investments is recognized subject to certain conditions. Such income is taken into account as part of other credit account 91 “Other income and expenses” in correspondence with account 76 “Other debtors and creditors” (p.

7 PBU 9/99, clause 34 PBU 19/02). Interest accrued on deposits in 2015 and reflected on the credit of account 91 is indicated in column 9 of table 3.1. Line 5316 according to 2014 data is filled in in a similar manner.

Separately, columns 5 (for investments at the beginning of the year), 8 (for investments retired or redeemed during the year), 12 (for investments at the end of the year) of Table 3.1 reflect such an indicator as the accumulated adjustment.

For financial investments for which the current market value is not determined (except for debt), the indicated columns display the amount of the reserve for depreciation of financial investments.

Deposit in transaction currency

At the same time, the bank, purchasing a currency option, ensures payment to the client of funds in the currency that corresponds to the target rate chosen by the client himself earlier. In accordance with the Chart of Accounts for accounting financial and economic activities of organizations and instructions for its application (approved by order of the Ministry of Finance of Russia dated October 31 .2000 N 94н, hereinafter referred to as the Chart of Accounts and the Instructions, respectively), to summarize information on the availability and movement of funds in foreign currencies in the organization’s foreign currency accounts opened with credit institutions both in the Russian Federation and abroad, a balance sheet account is intended 52 “Currency accounts”.

Short-term financial investments are...

> > > June 22, 2021 Short-term financial investments are financial investments with a period not exceeding 12 months. A comparison of short-term and long-term financial investments allows us to better understand their economic meaning.

This article is devoted to these aspects. Investments in financial assets with a maturity of less than 12 months (acquired rights to receivables, short-term interest-bearing loans, deposits, securities, other financial investments) are short-term financial investments. They are reflected on line 1240 of the enterprise’s balance sheet.

Let us recall that 1240 is one of the asset lines of the balance sheet, characterizing the current assets of the enterprise.

IMPORTANT! Clause 20 PBU 4/99 “Accounting statements of an organization” indicates that the company’s own repurchased shares must also be included among short-term financial investments. However, this directly contradicts paragraph. 4 clause 3 PBU 19/02 “Accounting for financial investments”. What should I do? There is a general legal principle according to which a contradiction between normative acts of the same level (PBU 4/99 and PBU 19/02 are normative documents of the same level) is resolved in favor of the one that has a later date of adoption.

In our case, it is the norms of PBU 19/02 that must be followed, since it came into force in 2003, and PBU 4/99 - in 2000. Therefore, you should not classify your own repurchased shares as financial assets. Line 1240 reflects the sum of the balance on Dt 58 (in terms of short-term financial investments), the balance on Dt 73 (in terms of short-term loans to personnel) and the balance on Dt 55 (in terms of short-term deposits).

This amount should be reduced by the balance under Kt 59 in terms of the formation of reserves for short-term financial investments. The difficulty is presented by the fact that for the count. 58 of the modern chart of accounts (order of the Ministry of Finance of the Russian Federation dated October 31, 2000 No. 94n, hereinafter referred to as order No. 94n) there is no division into long-term and short-term financial investments.

At the same time, the enterprise independently

Which line will the deposit be reflected in the balance sheet?

Contents A deposit is the transfer of funds located in the client’s current account for temporary use to the bank, on contractual terms.

This is a kind of borrowed funds that the company provides to the bank. Any organization engaged in commercial activities provides for the transfer of funds to a deposit - a benefit, which is expressed in the receipt of interest for the use of funds.

Let us, in this article, clearly look at which account the deposit is accounted for and how the deposit is reflected in the balance sheet.

In the current accounting system, there are contradictions in the accounting of deposit funds.

There are two options for accounting for deposit funds; they are taken into account in the account:

- 55.03 “Deposit accounts”;

- 58.03 “Loans provided.”

According to the current Chart of Accounts, a separate account has been allocated for recording deposit funds, it is called 55.03.

But since the deposit is opened by an organization (firm) in order to receive material benefits in the form of interest, it is advisable to take it into account in account 58.03.

Funds are transferred to the deposit account from the current account, and accounting entries are generated:

- Debit account 55.03 “Deposit account” and account credit. 51 “Current account”.

If the deposit account is opened for the period:

- More than 12 months, then investments should be taken into account in the balance sheet in the first (I) section “Non-current assets” on the line “Financial investments”;

- If it is less than 12 months, then investments should be taken into account in the balance sheet in the second (II) section “Current assets” also in the line “Financial investments (except for cash equivalents”).

The situation is written above in relation to account 58.03, as for account 55.03, it is indicated in the second (II) section “Current assets” in the line “Deposit accounts” to the decoding of the line “Cash and cash equivalents”. The choice of accounting method - in which accounting account your organization will account for deposit funds, depends on what will be stated in the accounting policy of your company.

Deposits: concept, accounting, postings. score 55

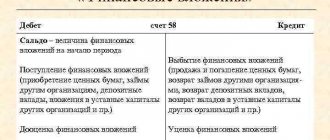

When placed, these investments are reflected by postings in their original amount, which is equal to the amount of funds credited to the deposit account. All funds that were placed for safekeeping in the form of a deposit can be displayed on the debit side of the following accounts:

- No. 55, special bank accounts;

- No. 55.03, deposit accounts;

- No. 58, deposit investments.

Accounting for interest on deposits in transactions Interest on deposits, which are accrued every month, is included in the section of other income of the organization. They must also be displayed in accounting on a monthly basis until the term of the banking agreement expires.

Where are short-term bank deposits reflected on the balance sheet?

A deposit is the transfer of funds located in the client’s current account for temporary use to the bank, on contractual terms.

This is a kind of borrowed funds that the company provides to the bank. Any organization engaged in commercial activities provides for the transfer of funds to a deposit - a benefit, which is expressed in the receipt of interest for the use of funds.

Let us, in this article, clearly look at which account the deposit is accounted for and how the deposit is reflected in the balance sheet. In the current accounting system, there are contradictions in the accounting of deposit funds. There are two options for accounting for deposit funds; they are taken into account in the account:

- 55.03 “Deposit accounts”;

- 58.03 “Loans provided.”

According to the current Chart of Accounts, a separate account has been allocated for recording deposit funds, it is called 55.03.

But since the deposit is opened by an organization (firm) in order to receive material benefits in the form of interest, it is advisable to take it into account in account 58.03. Funds are transferred to the deposit account from the current account, and accounting entries are generated:

- Debit account 55.03 “Deposit account” and account credit. 51 “Current account”.

If the deposit account is opened for the period:

- If it is less than 12 months, then investments should be taken into account in the balance sheet in the second (II) section “Current assets” also in the line “Financial investments (except for cash equivalents”).

- More than 12 months, then investments should be taken into account in the balance sheet in the first (I) section “Non-current assets” on the line “Financial investments”;

The situation is written above in relation to account 58.03, as for account 55.03, it is indicated in the second (II) section “Current assets” in the line “Deposit accounts” to the decoding of the line “Cash and cash equivalents”.

The choice of accounting method - in which accounting account your organization will account for deposit funds, depends on what will be stated in the accounting policy of your company.

Question on accounting: Reflection of deposits in the balance sheet (BP 2.0.44.8)

IGreetings to all!

Voaros is like that. There are deposits in the organization's deposit account (short-term). Essentially a transfer from account to account (dt51 kt 55.03). In the balance sheet, the amount falls into line 1240 (Financial investments (except for cash equivalents)). In the DDS report in line 4500 (Balance of cash and cash equivalents at the end of the reporting period). Glbusha assures that balance sheet lines 1250 and 4500 must match, otherwise there will be distortion of accounting records and fines. those. the balance sheet should not classify transfers to a deposit account as financial investments.

What is the truth? a reflection of the 1C balance sheet or the opinion of the head of state?

On the screenshot is the reporting and posting of deposit statements https://s017.radikal.ru/i427/1302/6f/09d90ceab4ff.jpg

Get your work in order using the 1C configuration “IT Department Management 8”

ATTENTION!

If you have lost the message input window, press

Ctrl-F5

or

Ctrl-R

or the Refresh button in your browser.

The topic has not been updated for a long time and has been marked as archived. Adding messages is not possible.

But you can create a new thread and they will definitely answer you!

Every hour there are more than 2000

people on the Magic Forum.

Short-term financial investments on the balance sheet

Home — Entrepreneur's Directory — Investments — The short-term category includes investments for a period of no more than a year. It is understood that upon its expiration, the costs incurred turn into receivables.

In this capacity, the purchase of securities, the issuance of loans at interest with a repayment period of up to 12 months, deposits and other returnable investments that generate profit are taken into account. Contents: 1. The essence of short-term financial investments 2.

Short-term investments on the balance sheet 3.

Financial investments in accounting 4. Increasing and decreasing short-term investments 5. Managing short-term investments The essence of short-term financial investments You can invest funds only if there is a free money supply.

This is possible when receiving unplanned profits or its seasonal nature. Receiving increased income makes it possible to place the “surplus” at interest, subject to repayment within a year. It is not mandatory to have records for accounts and balance sheets intended for short-term investments.

Short-term investments in the balance sheet Short-term financial investments are included in the assets of the balance sheet and are reflected on line 1240 as of December 31. The amount reflected in it is the balance of the following accounts, reduced by the balance of the loan of account 59:

- 55 – for short-term deposits;

- 73 – internal loans to employees with a repayment period within a year.

- 58 – for short-term investments in a second-order subaccount;

Line 1240 reflects only investments that involve profit. If a loan is issued without interest (borrowed money), it loses the status of a financial investment and cannot be reflected in account 58 and line 1240 of the balance sheet.

Account 59 collects a reserve of financial investments necessary to compensate for their depreciation.

In addition to line 1240, explanatory section 3 (subsections 3.1 and 3.2) is filled out in the balance sheet. They show the presence, movement and use of investments.

Financial investments in accounting Account No. 58 is common for long- and short-term investments.

Short-term deposit on balance

» Consumer law 1. What terms of the bank deposit agreement are most important for an accountant.

2. How to reflect the deposit and interest on it in accounting and tax accounting.

3. How to take into account the consequences of early termination of a bank deposit agreement. Having a financial airbag, that is, a certain reserve of funds, is the “golden” rule of both personal and corporate finance.

However, simply keeping the nth amount of money in reserve in your account is extremely unprofitable. As you know, money should work and bring... money. That is why competent managers try to place free funds in financial investments.

One of the most common types of financial investments is a bank deposit, or deposit. And there are at least two reasons for this. Firstly, opening a deposit does not require special knowledge and skills in the field of investing.

And secondly, a deposit is traditionally considered one of the least risky ways to invest money (all other things being equal). What an accountant should know about the accounting for bank deposits and interest on them, and what “pitfalls” this seemingly simple operation may hide, we’ll look into this article.

The main document that serves as the basis for recording a bank deposit and interest on it in accounting is the bank deposit agreement. Checking the correctness of the contract, as well as the legal nuances and consequences of the transaction, is rather the task of a lawyer. An accountant, as a rule, is only interested in some of the terms of the contract, on which the accounting reflection of the deposit depends.

So, what should an accountant pay close attention to:

- Deposit term. A bank deposit can be opened for a certain period or on demand (Clause 1, Article 837 of the Civil Code of the Russian Federation). The period for which the deposit is opened depends on the order in which it is reflected in the financial statements: as part of long-term or short-term financial investments.

- Type of deposit: replenishable or non-replenishable.

What are deposits? accounting of deposits in accounting (postings). score 55

The organization VESNA LLC applied to the bank to terminate the contract and early return of the deposit amount on May 15, 2021.

The bank returned the deposit amount with the total amount of accrued interest (500,000.00+46,903.45) Bank statement Example 2 Organization VESNA LLC On March 01, 2021, transferred 500,000.00 rubles to the bank. for deposit. According to the terms of the agreement, the deposit period is 12 months, therefore, the bank must return the funds on February 28, 2021. Simple interest on the deposit is accrued monthly at a rate of 9% per annum.

Interest on the deposit is accrued starting from the day following the day of transfer of funds, including the day the bank returns the funds to the depositor. Calculation of the amount of income, deposit and payment scheme for accrued interest on the deposit: Postings for accounting for the amount of the deposit and interest on the deposit: Debit Account Credit Account Posting amount, rub. It is stipulated that analytical accounting for subaccount 55-3 “Deposit accounts” is maintained for each deposit. According to the Instructions, the transfer of foreign currency funds to deposits is reflected by the organization by debiting account 55 in correspondence with account 52 “Currency accounts”. When a credit institution returns deposit amounts, reverse entries are made in the organization's accounting. From the point of view of PBU 19/02 “Accounting for Financial Investments” (hereinafter referred to as PBU 19/02), deposits in credit institutions are financial investments (clause 3 of PBU 19/02) , for the accounting of which the Instructions provide for the corresponding account 58 “Financial Investments”. Regulatory acts on accounting do not regulate in detail the procedure for accounting for funds in dual-currency and (or) multi-currency deposits. Thus, guided by clause PBU 3/2006, the value of funds in bank accounts (bank deposits), as well as financial investments (etc.), expressed in foreign currency, must be recalculated into rubles for reflection in accounting and financial statements. Conversion of the value of an asset or liability expressed in a foreign currency into rubles is carried out at the official exchange rate of this foreign currency to the ruble established by the Central Bank of the Russian Federation (clause 5 of PBU 3/2006). According to clause 6 of PBU 3/2006, for accounting purposes, this recalculation in rubles is made at the rate in effect on the date of the transaction in foreign currency. The dates of individual transactions in foreign currency for accounting purposes are given in the appendix to PBU 3/2006. As stated in paragraph.

Which line reflects short-term financial investments?

» » » Assets The current form of the balance sheet, which is submitted to the tax office, was approved by Order of the Ministry of Finance dated July 2, 2010 No. 66n. Its basis is the balance sheet lines, which reflect the balances transferred from the accounting accounts.

Therefore, for correct preparation, it is important not only to keep accounting records correctly and completely, but also to understand the information from which accounts each line of the balance sheet reflects.

Our consultation will help you figure this out.

Below is a complete breakdown of the 2021/2021 balance sheet lines. Moreover, each line is specified according to the most characteristic accounts for it, which are reflected in it. Of course, the specifics of economic activity in practice may leave their mark on this correspondence.

Also, the order of formation of accounting reports, as well as the reflection of certain indicators, is influenced by the accounting policy for accounting purposes adopted by the company.

The following is a breakdown of the balance sheet lines for the accounts in two tables - by asset and liability of the balance sheet.

Name of indicator Code Data of which accounts are used Algorithm for calculating the indicator Intangible assets 1110 04 “Intangible assets”, 05 “Amortization of intangible assets” Dt 04 (excluding R&D expenses) – Kt 05 Results of research and development 1120 04 Dt 04 (in terms of R&D expenses) Intangible search assets 1130 08 “Investments in non-current assets”, 05 Dt 08 – Kt 05 (all in terms of intangible search assets) Tangible search assets 1140 08, 02 “Depreciation of fixed assets” Dt 08 – Kt 02 (all in terms of tangible search assets) Fixed assets 1150 01 "Fixed assets", 02 Dt 01 - Kt 02 (except for depreciation of fixed assets accounted for in account 03 "Income-generating investments in tangible assets" Income-generating investments in tangible assets 1160 03, 02 Dt 03 - Kt 02 (except for depreciation of fixed assets funds accounted for in account 01) Financial investments 1170 58 “Financial investments”, 55-3 “Deposit accounts”, 59 “Provisions for impairment of financial investments”, 73-1 “Settlements on loans provided”