Indirect costs

In accounting, indirect (overhead) costs

- these are expenses that are common to a workshop, production, or organization. And they cannot be directly attributed to a specific type of product, service, work or product.

Indirect expenses in accounting are accumulated in accounts 25, 26, 44 (except for TZR).

These accounting accounts are closed monthly and there should be no balance.

Indirect costs at NU

– these are all other expenses associated with the production and sale of goods (works and services), except for direct and except for non-operating expenses (Article 265 of the Tax Code of the Russian Federation).

At the end of the month the account balance should not be 25!

General production expenses are distributed to the debit of account 20 “Main production” by type of product, work, service during the Month Closing

.

Rules for the distribution of overhead costs are set using the link Methods for the distribution of indirect costs

.

At the end of the month there should be no account balance of 26!

Option #1.

General business expenses are distributed to the debit of account 20 “Main production” by type of product, work, service during the

Month Closing

, i.e. the “full” cost is calculated.

Rules for the distribution of overhead costs are set using the link Methods for the distribution of indirect costs

.

Option

No. 2.

General business expenses are completely written off to the financial result in the debit of account 90.08 “Management expenses” (Direct costing method).

To write off costs monthly, select the option In cost of sales (direct costing)

in

the General business expenses section are included

.

Rules for the distribution of overhead costs are set using the link Methods for the distribution of indirect costs

.

Section XVII. Accounting policies for loans and borrowings

Of all the costs of manufacturing a product, its cost is added up.

Account 20 contains almost all production costs that can be classified as direct. The main production account on debit corresponds with accounts 02, 10, 23, 25, 26, 60, 69, 70 on credit. To determine the cost of a product of a certain type, open analytical accounts for individual types of products and costs for account 20. This will simplify the procedure for generating cost by type. Indirect costs are contained in accounts 25 and 26. To prepare loan entries, the same correspondence is used as for direct costs. Do not forget that indirect costs cannot be attributed directly to the cost of one product. Select a reasonable allocation basis and note your choice in the accounting policy.

Why might similar precedents related to lawsuits against the Federal Tax Service arise? Most often, it is because tax authorities recognize the company’s inclusion of certain expenses as indirect as unreasonable.

In this case, the Federal Tax Service simply charges additional income tax, as if the corresponding costs were direct, and obliges the company to pay it. However, the taxpayer always has a chance to defend the legality of his actions and the wrongness of the Federal Tax Service in court.

Example 1

There is a known judicial precedent in which the Supreme Arbitration Court of the Russian Federation recognized as legitimate the negative assessment by the courts of previous instances of the approach of the Federal Tax Service to the classification of expenses of one of the companies that produces paper and cardboard (more information about this precedent can be found by reading the determination of the Supreme Arbitration Court of the Russian Federation dated October 19, 2011 No. VAS- 13628/11).

The tax authorities considered that the company did not have the right to include in the structure of indirect costs the costs associated with the production of packaging for the packs of paper it produced. These expenses, as the Federal Tax Service considered, should have been considered direct and could not be used to reduce the tax base in the corresponding period.

However, the arbitrators of the first instance did not agree with the opinion of the Federal Tax Service, since it was established that packaging is not a mandatory component of the production cycle within which the company produces paper. Packaging, as the courts have found, is more of an accompanying component of the delivery, which is not even taken into account when weighing the goods before placing them in the warehouse.

Let us note that in a number of cases the separation of the manufactured product from the packaging may be considered by the court to be not as obvious as in the case discussed above.

Example 2

The Presidium of the Supreme Arbitration Court of the Russian Federation, in resolution No. 8617/10 dated November 2, 2010, established that the costs of purchasing containers, labels, and lids of a plant for the production of alcoholic beverages and food products should be considered as direct expenses. The fact is that the relevant components, as the court considered, cannot be considered as related to the production technology of a particular product of the relevant categories.

PBU 10/99 establishes that expenses in accounting are recognized taking into account the relationship between expenses incurred and revenues (correspondence between income and expenses). In other words, expenses must be recognized when revenue directly attributable to those expenses is recognized.

If expenses determine the receipt of income over several reporting periods, or the relationship between income and expenses cannot be clearly defined, or is determined indirectly, then a reasonable distribution of expenses between reporting periods is necessary.

straight-line write-off over the period to which they relate;

write-off of expenses in proportion to the volume of production.

However, an organization can independently develop its own economically sound algorithm for writing off expenses, enshrining it in its accounting policies.

Nonprofit organizations are required to keep accounting records just like for-profit organizations. Most non-profit organizations, in addition to their main activities, also engage in entrepreneurial activities. In this case, they have a problem with the allocation of costs common to both activities.

According to experts, the distribution base can be taken as the share of costs for remuneration of employees engaged in business activities in the general wage fund or the area of premises occupied by the business unit.

However, the most popular distribution base is income from these activities. At the same time, income for non-profit activities is proposed to be understood as the amount of targeted funding for the purposes defined by the charter.

This position must be fixed in the accounting policy.

However, there are serious objections to this interpretation of accounting legislation.

For example, the Ministry of Taxes and Taxes of Russia, in letter dated April 2, 2002 N 02-2-10/20-n340, explained the following. The costs of maintaining a non-profit organization and the costs of conducting their statutory activities are the costs of carrying out the statutory activities of non-profit organizations.

The concepts of “maintenance of a non-profit organization” and “conducting the statutory activities” of a non-profit organization are not equivalent.

Expenses for the maintenance of non-profit organizations include expenses for remuneration of administrative, managerial and other personnel carrying out statutory activities, travel expenses, expenses for office supplies, expenses for renting premises, expenses for the maintenance of buildings and premises, expenses for the maintenance and operation of vehicles, expenses for the acquisition of fixed assets, etc.

Conducting statutory activities is the direction of targeted funds to achieve the goals provided for in the charter of a non-profit organization.

Thus, the expenses of a non-profit organization in the form of salaries of administrative and managerial personnel, payroll charges, utilities, transportation costs, communication services must be made at the expense of earmarked funds received for the management and maintenance of the said organization.

The distribution of these expenses between the non-profit and commercial activities of the organization is not provided for by tax legislation.

And although this letter relates to tax legislation, in the author’s opinion, the same arguments can be made in relation to accounting.

Thus, if certain expenses are common to both types of activities, but they are financed from targeted revenues, then there is no reason to distribute them between these two types of activities.

Therefore, indirect costs are subject to distribution, which were not paid from targeted financing and which cannot be clearly attributed to costs associated with business activities.

In relation to those R&D projects that have yielded a positive result, the accountant has the right to choose the method and timing of writing off expenses for them.

In paragraph 11 of the Accounting Regulations “Accounting for expenses on research, development and technological work” PBU 17/02, approved by Order of the Ministry of Finance of Russia dated November 19, 2002 N 115n, it is said that the period for writing off R&D expenses is determined by the organization independently, based on the expected period of use of the results obtained from these works. However, this period cannot exceed five years.

linear method;

a method of writing off expenses in proportion to the volume of products, works or services.

The organization must consolidate its choice in its accounting policies.

At the same time, the Tax Code of the Russian Federation establishes that R&D, both those that gave and those that did not produce a positive result, are written off as expenses for the purpose of calculating income tax evenly over one year based on the provisions of paragraph 2 of Art. 262 of the Tax Code of the Russian Federation.

Thus, for an accountant who wants to bring accounting and tax accounting closer together, the optimal choice is to establish in the accounting policy for accounting purposes a linear method of writing off R&D expenses during the year.

We invite you to read: Obtaining a certificate of no criminal record through government services

We note that R&D expenses (including those that did not produce a positive result) made by taxpayers-organizations registered and operating in the territories of special economic zones created in accordance with the legislation of the Russian Federation are recognized for tax accounting purposes in the reporting or tax period in which in which they were carried out, in the amount of actual costs.

on the transfer of long-term debt to short-term debt;

on the composition and procedure for writing off additional borrowing costs;

on the choice of methods for calculating and distributing income due on borrowed obligations;

on the procedure for accounting for income from the temporary investment of borrowed funds.

Paragraph 6 of PBU 15/01 allows the borrower to transfer long-term debt into short-term debt or to account for borrowed funds at his disposal, the repayment period of which under a loan or credit agreement exceeds 12 months, before the expiration of the specified period as part of long-term debt.

If the accountant chooses the first option, then the transfer of long-term debt on received loans and credits to short-term is carried out at the moment when, according to the terms of the loan or credit agreement, exactly 365 days remain until the repayment of the principal amount of the debt.

Additional costs associated with obtaining loans or credits, clause 19 of PBU 15/01 includes costs for consulting and legal services, examination, communication services, etc.

in full in the reporting period when they were made;

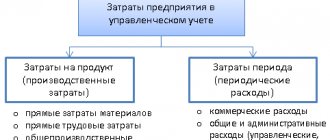

Direct expenses at NU

Direct expenses refer to expenses at the time

of sale

of products, works, services, in the cost of which they are taken into account (Article 318 of the Tax Code of the Russian Federation).

The list of direct expenses is determined in the accounting policy. It must be economically justified and applied for at least 2 tax periods (Article 319 of the Tax Code of the Russian Federation).

In NU, the list of direct costs is specified using the link Methods for determining direct production costs in NU .

In this case, different cost accounting accounts can be used (account 20, 25), the main thing is that the settings for such correspondence are indicated as part of direct expenses.

Cost calculation in 1C. Services and works

- revenue is reflected on the credit of account 90.01 by name of work;

- on the debit of account 90.02, from the credit of account 20, the cost of work (services) performed is written off.

Option No. 1. Without taking into account revenue from work (provision of services)

- All costs accounted for on account 20 for work and services will be written off automatically in full in Dt 90.02 always at the close of the month. Regardless of whether the proceeds from loan 90.01 are reflected or not reflected at all.

Option No. 2. Taking into account the proceeds from the performance of work (provision of services)

- If revenue is reflected for a product group, then the costs recorded on account 20 for the same product group will be written off automatically for the entire amount in Dt 90.02 when closing the month.

- If there was no revenue for the item group, then the costs will NOT be written off , but will remain as work in progress in the debit of account 20.

Option No. 3. Taking into account revenue only from production services

- Revenue from works and services should be reflected only using the document Provision of production services

. - If revenue is reflected by product group using this document, then the costs recorded on account 20 for the same product group will be written off automatically for the entire amount in Dt 90.02 when closing the month.

- If there was no revenue for the product group or it is reflected in the document Sales of goods and services

, then the costs will not be written off, but will remain in the form of work in progress in the debit of account 20.

5.1. Fixed Asset Accounting

5.1.1. When establishing the useful life of fixed assets, be guided by the Classification of fixed assets, approved. Decree of the Government of the Russian Federation dated 01.01.02 N 1.

5.1.2. Depreciation for all fixed assets is calculated using the straight-line method.

5.1.3. Reducing (increasing) coefficients should not be applied to the current norms of depreciation of fixed assets.

We suggest you read: What types of mortgages are there?

5.1.4. Assets in respect of which the conditions of clause 4 of PBU 6/01 “Accounting for fixed assets” are met, and cost no more than 20,000 rubles. reflected as part of inventories.

5.1.5. Real estate for which ownership has not been registered, after submitting documents for state registration, should be accounted for in a separate subaccount of account 01 and depreciated in the general manner.

5.1.6. Do not revaluate fixed assets.

Revenue from sales of goods, works and services

Nomenclature group

- this is a type of industrial and technical equipment, i.e. it is a generalized concept that accumulates costs and revenues by type of product, goods, work and services

The link Nomenclature

groups

for sales of products and services determines the types of industrial and industrial goods of own production, the proceeds from the sale of which must be reflected in the income tax return on page 011 of Appendix No. 1 to Sheet 02 “Income from sales and non-operating income.”

To fill out other lines of Appendix No. 1 to Sheet 02, there is no need to make special settings in the accounting policy.

See also:

- Accounting policy designer

- Setting up accounting policies for NU (STS)

- Setting up accounting policies for NU in 1C: Income Tax

- Accounting policy in 1C 8.3 Accounting 3.0

- Accounting policy for accounting: Distribution of indirect costs

- Implementation of work

- Provision of services with write-off of direct costs

- Sales of products

Did the article help?

Get another secret bonus and full access to the BukhExpert8 help system for 14 days free of charge