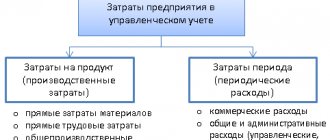

Why divide costs into direct and indirect?

When calculating income taxes, direct and indirect expenses reduce the tax base, but at different times.

Therefore, it is necessary to divide expenses into direct and indirect in order not to make a mistake with the moment of recognizing expenses as expenses. That is, correctly determine the tax base and calculate the tax.

The tax base can be reduced by the amount of direct expenses only after the sale of products in the production costs of which they are taken into account. That is, their amount for the current month must be distributed between work in progress and products manufactured during the month (work performed, services provided).

You can write off only that part of direct expenses that falls on finished, shipped and sold products (Articles 318, 319 of the Tax Code of the Russian Federation).

Indirect expenses are written off to reduce the tax base in the month in which they were incurred, that is, without reference to sales.

Therefore, sometimes there is a temptation to expand the list of indirect expenses as much as possible and reduce the list of direct ones - in order to pay less income tax. However, it is better not to do this, but try to divide your expenses into direct and indirect so that you don’t have to pay more later.

What are other indirect costs and what do they include?

As noted above, it is difficult to identify a structure of direct and indirect costs . After all, everything depends on the scale of the enterprise, specialization of activities and other determining factors. Moreover, as a rule, it is difficult to even identify items of fixed (indirect) expenses “in their pure form.” Therefore, when classifying expenses at an enterprise, the concept of semi-fixed expenses is used. These can be called costs that will be considered constant only up to certain limits.

An example is the cost item presented above - payment for utilities. If we are talking about a small enterprise, where it does not matter how many machines are illuminated by one light bulb, it is necessary in any case - then this will relate to indirect costs. But, for example, if this light bulb will function on each machine and their number will depend on the volume of production, then in this case we will be talking about direct costs.

Also in the theory and practice of economic analysis, there is such a thing as “other indirect costs”. This is a cost item that assumes the occurrence of unexpected or possible in certain cases costs associated with servicing the production process.

How to safely separate expenses into direct and indirect

Tax authorities will not find fault if in tax accounting you take into account as direct expenses the costs that are included in the cost of products (works, services) in accounting.

The list of costs included in the cost of production in accounting may only include direct costs. That is, those expenses that are directly necessary for the production of products. These include the costs of raw materials and supplies, wages of production personnel, depreciation of production equipment, etc.

Just keep in mind that the accounting list of direct costs should be based on the normal, and not the truncated cost of finished goods. The formation of truncated cost is based on the distribution of costs into variables that depend on the volume of products produced, and constants that do not depend on it. It turns out that indirect costs include those associated with the production of several types of products, including the costs of maintaining and operating equipment. The inspectorate will not allow this approach (see, for example, letter of the Ministry of Finance dated January 13, 2014 No. 03-03-06/1/218).

What expenses form indirect costs?

Indirect costs are included in the following three types of expenses.

- General production expenses are the costs of maintaining and operating the company’s main and auxiliary production facilities.

- General business expenses are expenses spent on meeting the management needs of the company. They are not directly related to the production process.

- Selling expenses are expenses related to the sale of products. These include, for example, expenses for marketing campaigns and advertising campaigns, remuneration for salespeople, costs for packaging goods, etc.

Direct and indirect costs for Tax Code

However, do not forget that the Tax Code of the Russian Federation also gives its recommendations for tax accounting.

The list of recommended direct expenses is directly established in paragraph 1 of Article 318 of the Tax Code of the Russian Federation:

- costs of raw materials or materials used in the production of goods, components, semi-finished products;

- expenses for remuneration of personnel involved in the production process and insurance premiums for it;

- depreciation amounts of fixed assets used in production.

Costs that are not directly related to production or, according to technical regulations, are not included in it, are classified as indirect.

For example, the salary of management personnel and insurance premiums for it (see letter of the Ministry of Finance dated September 20, 2011 No. 03-03-06/1/578). This is the remuneration of the director, accounting, personnel, economic, and financial services.

But only those expenses that cannot be classified as direct can be recognized as indirect. Thus, tax authorities will not accept as indirect expenses the costs of:

- payment for the services of subcontractors or processors of customer-supplied raw materials;

- rent and utility payments for industrial premises.

These costs are related to production and therefore should be classified as direct.

Don't forget to secure lists of direct and indirect expenses in the company's accounting policies.

Read in the berator “Practical Encyclopedia of an Accountant”

How to fill out Appendix No. 2 to sheet 02 of the income tax return

Indirect costs include

The list of indirect costs will vary depending on the specifics of each specific enterprise, but their single distinguishing feature can be identified - these are always investments that do not depend on production volumes. Although such “independence” exists only to certain limits.

Let us list the main areas of indirect costs and explain their content.

- Salaries of non-production personnel;

- Payment of utility services;

- Security system of the organization;

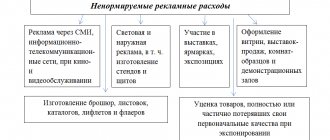

- Costs of developing an advertising campaign;

- In many cases, this can also include write-offs of costs associated with equipment depreciation.

Payment of wages will be considered an indirect expense if we are talking about such payments for employees of the accounting department, legal department, technical group. support, security guards and other categories of personnel not directly involved in the production of goods and services, but ensuring the maintenance of all business processes of the enterprise.

When classifying payment for utilities as indirect costs, we are talking about costs associated with lighting of premises, water supply not intended for the manufacture of products, heating, etc.

A security system also falls into this category and involves costs associated with the operation of video surveillance, alarm systems, etc.

From the point of view of management accounting, methods for calculating depreciation of fixed assets, intangible assets, equipment in a linear and non-linear way are also important. By the way, for tax accounting only the linear method of calculating depreciation is used.

Depreciation

Any organization has office equipment, computers, furniture, and transport intended for management needs. They are not used in production. Depreciation on such fixed assets can be safely considered an indirect expense.

This is not the case with premises - often both production and non-production are located in the same building. Depreciation cannot be divided. Therefore, it will have to be classified as direct or indirect based on calculations, for example, depending on how many percent of the area is occupied by production premises and how much by non-production premises.

If the production area occupies less than half, then the depreciation amounts for the entire premises can be considered indirect costs (see the definition of the Supreme Arbitration Court of August 16, 2012 No. VAS-9792/12).

List of indirect income tax expenses

Indirect expenses have a direct impact on the amount of taxable profit. As you know, profit is calculated using the formula:

Profit = Revenue - Cost = Income - Expenses

Thus, the larger the expenses, the smaller the profit, the smaller the tax base, the less taxes you will have to pay. Therefore, determining the optimal amount of direct and indirect costs, and their impact on profit margins, are of decisive importance when conducting an economic analysis of an enterprise.

It is also worth noting that the tax code of the Russian Federation provides some preferences when writing off indirect expenses. For example, it is possible to write off indirect expenses in full in the current reporting (tax) period. This in turn leads to a reduction in taxable profit, which is obviously very beneficial for entrepreneurs. This is especially attractive for companies that have a large amount of indirect costs, as well as those that often use services and cooperation with external organizations (for example, on outsourcing terms, cooperation with contractors, etc.)

The taxpayer has the right to independently determine the list of direct expenses

In accordance with paragraph 1 of Art. 318 of the Tax Code of the Russian Federation, production and sales costs incurred during the reporting (tax) period are divided into direct and indirect. Direct costs may include, in particular: - material costs determined in accordance with paragraphs. 1 and 4 paragraphs 1 art. 254 Tax Code of the Russian Federation; - expenses for remuneration of personnel involved in the production of goods, performance of work, provision of services, as well as expenses for compulsory pension insurance, used to finance the insurance and funded parts of the labor pension, for compulsory social insurance in case of temporary disability and in connection with maternity , compulsory medical insurance, compulsory social insurance against industrial accidents and occupational diseases, accrued on the specified amounts of labor costs; — the amount of accrued depreciation on fixed assets used in the production of goods, works, and services. Indirect expenses include all other amounts of expenses, with the exception of non-operating expenses determined in accordance with Art. 265 of the Tax Code of the Russian Federation, carried out by the taxpayer during the reporting (tax) period. In paragraph 1 of Art. 318 of the Tax Code of the Russian Federation states that the taxpayer has the right to independently determine the list of direct costs associated with the production of goods (performance of work, provision of services), securing his choice in the accounting policy. Thus, the taxpayer has the right to independently determine the list of direct expenses, fixing it in the accounting policy. Chapter 25 of the Tax Code of the Russian Federation does not contain provisions limiting the taxpayer in attributing certain expenses to production and sales, incl. expenses in the form of insurance premiums, direct or indirect expenses. This is indicated in the Letter of the Ministry of Finance of Russia dated May 25, 2010 N 03-03-06/2/101. In this case, the taxpayer can use for profit tax purposes the list of direct expenses approved in accounting. In accordance with paragraph 3 of Art. 1 of the Federal Law of November 21, 1996 N 129-FZ “On Accounting”, one of the main tasks of accounting is the formation of complete and reliable information about the activities of the organization and its property status, necessary for internal users of accounting statements - managers, founders, participants and owners of property organization, as well as external investors, creditors and other users of financial statements. Thus, according to financiers, when forming the composition of direct expenses in tax accounting, the taxpayer can take into account the list of direct expenses associated with the production and sale of goods (performance of work, provision of services), used for accounting purposes. This conclusion was made in Letter of the Ministry of Finance of Russia dated December 19, 2011 N 03-03-06/1/834.