Why is the final result of an organization/enterprise’s activities calculated?

Profit accounting, income and consumables are reflected in the documentation, the responsibility for which is the responsibility of the organization's accountant. The main accounting document is the “Income Statement”.

Counting is required for all types of organizations for a number of reasons:

- to determine the exact amount of net profit and distribute it among participants;

- to calculate taxes required to be paid;

- to compensate for losses in whole or in part;

- to rationalize costs in the future;

- to calculate the accumulated income of the enterprise;

- to account for all third-party ancillary income;

- for the correct repayment of loans/loans, if any.

What are the objects of taxation?

Accounting statements: basic requirements.How to write a business plan for a beauty salon? Read here.

Types of expenses that help reduce taxable income

Taxable income can be reduced due to certain expenses. Thus, expenses related to the production and sale of main products are deducted. Such expenses include materials, depreciation, labor, transportation of products, various administrative fees, etc.

In addition, a reduction in taxable profit can be achieved due to the costs of non-operating operations, namely due to:

- penalties and fines paid;

- legal expenses;

- losses of previous periods;

- payment for banking services;

- other costs provided for in Art. 265 NK.

When indicating expenses in reporting, the organization must attach a corresponding receipt, form or ordinary cash receipt to each item as confirmation. The presence of these documents is mandatory, since they are necessary to calculate the amount of profit made in the process of production activities of the enterprise for a certain period and the amount of tax deductions to the state budget.

How to Determine Gross Profit

Gross profit is the total difference between the actual revenue of a business or organization and the cost of goods or services.

The English abbreviation for gross profit is COGS (“cost of sold goods”).

Gross profit and operating profit are different concepts. The second includes the amount before payment:

- Income tax.

- Fines.

- Credit payments.

- Peneus.

Gross profit is calculated as net income minus the cost of goods.

What kind of reporting do NPOs submit to the Ministry of Justice?

Details

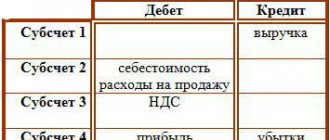

Net profit includes part of the enterprise's balance sheet profit, from which taxes, fees, other contributions to the budget, as well as the enterprise's expenses (commercial, administrative, wage costs, etc.) are excluded. It remains entirely at the disposal of the company. From it, the enterprise's funds are updated, dividends are paid to shareholders, and working capital is increased. The money can be used for business needs, its expansion, and equipment modernization.

Image 1. Places of net profit in the income system

To calculate net profit, you need to subtract costs and all mandatory payments from revenue.

How to calculate profit/loss before tax

The amount resulting from gross profit minus total non-production expenses. These include:

- product sales expenses;

- administrative;

- managerial.

This type of income has a second name: “operating profit”. It is calculated to cover the organization’s constant operating expenses, taking into account any loans, leasing (operational and financial).

The complete calculation formula is as follows:

Profit (loss) from sales + Income from participation in other organizations – Interest payable + Interest receivable + Other income – Other expenses = Profit (loss) before tax. The total amounts must be entered in line 2300 of the mentioned Report.

Profit itself is also an object on which tax is imposed, the payment of which is mandatory.

Income is calculated differently for Russian and foreign enterprises and organizations, regardless of whether they are included in tax consolidation or not.

Business without investment: step by step.

Women's business - where to start?Read about special tax regimes in Russia.

Why is EBIT calculated?

The popularity of EBIT is due to its visibility. Profit “not cleared” of interest for the use of borrowed funds, taxes - amounts that can have a significant impact on the value of the indicator, makes it possible to compare completely different companies by this indicator.

It is used:

- in a comparative analysis of Russian and foreign companies that have significant differences in tax rates and amounts, net profit does not provide an objective picture;

- in a comparative analysis of Russian companies, if one of them uses borrowed funds, and the other uses its own share capital; in the first case, interest is paid on loans, in the second - dividends to shareholders - net profit again does not give an objective picture;

- when a bank decides to provide a loan to a company, it is believed that the indicator cannot be lowered below certain values if the company is counting on financing.

EBIT analysts often analyze companies in the same industry or market sector. EBIT is considered one of the most objective benchmarks (the so-called “benchmarks”) in this area.

Attention! EBIT should not be confused with operating profit. It, unlike EBIT, does not include income and expenses from other operations

Determination of net profit

Net profit is the share of funds received by an enterprise or organization that remains at the free disposal of the company. It remains after all necessary deductions for taxes, credits and expenses have been made and accounted for.

The concept of net profit is often confused with economic profit, but this is absolutely forbidden. Net profit refers to those incomes that go to the benefit of the enterprise and are used for: investing in fixed assets, investing in the company's turnover, necessary reorganization. From which reserve funds are created and funds for circulating production are increased.

Net profit is calculated as follows:

Income Tax Expense – Income Tax Recovered + Extraordinary Expenses – Extraordinary Revenues + Interest Paid – Interest Received. The result is an amount equal to EBIT, which stands for “earnings before interest and taxes.”

If you add depreciation deductions to the resulting amount and subtract the revaluation of assets, you get the EBITDA value. This indicator is used to level out the impact of income tax payments, borrowed funds and non-current assets.

Ways to reduce the tax rate

Today, the most popular way to reduce the tax percentage is to officially register a company in another country.

After gaining a stable position in the market, the owners of a company registered in this way at the initial stage of active business begin to carefully withdraw financial profits to the so-called offshore. As a result, the profit received by the enterprise is not taxed, which makes it possible to manage it independently

You should also know that in the Russian Federation, taxable profit is calculated by enterprises using OSNO. Only organizations working on UTII and the simplified tax system are exempt from this. The tax interest rate is 20%, of which 2% will be directed to the state budget, and 18% to the regional budget. Some businesses carrying out commercial activities can take advantage of special tax incentives and a reduction in the rate to 0%. Educational and medical institutions, as well as agricultural enterprises, can receive tax benefits.

Use of the obtained financial result

In financial calculations, there are several basic concepts called absolute. These terms include the aforementioned EBIT, EBITDA, net profit and operating profit.

The obtained result clearly shows where the company could save, where it took out an extra loan, and where it would not hurt to add funds and invest in development so that income increases in the future.

All data must be entered into the Report, which also stores information about the amount accumulated by the enterprise for the entire period of operation. Despite the seemingly extreme clarity of the term “profit” itself, in practice a huge number of controversial situations arise when it is unclear whether a particular payment is included in the calculations.

Calculation of gross profit

It is represented by the difference between revenue and costs associated with the production or purchase of goods. Revenue consists of various cash receipts related to the main activities of the enterprise. In the calculation process, indicators excluding VAT are taken into account.

Costs include expenses associated with the purchase or production of goods. If a company provides services or performs any work, then all expenses related to this activity are taken into account.

The following indicators are not included in the cost:

- business expenses

- administrative expenses

- other costs

VP calculation is carried out at the end of each month, quarter and year. It can be determined for almost any period, for which only official payment documents are required.

The formula used for calculation is:

Video: how to calculate the difference and summarize financial results

More information about preparing a financial results report - how to correctly calculate and calculate, determine the balance - is described in this video:

Particular attention should be paid to calculations of compensation payments for municipal organizations, since the amount received was paid by the owner of the enterprise. Such funds are part of income and cannot be designated as targeted funding. That is, they are also subject to tax.

To summarize, it is worth noting that the concept of “profit” has many subparagraphs: gross, net, operating; before and after taxes and other expenses. All these concepts, despite the obvious similarity, should be clearly distinguished in order to avoid errors in regulatory documents, including the “Report on Financial Results”.

What is profit before tax

The value under consideration is also called operating profit - that is, that which remains in the organization as a result of deducting a number of indicators:

- Cost of services or products sold. This category includes labor costs, depreciation, marketing and advertising costs;

- Administrative expenses;

- Commercial expenses;

- Costs that do not relate to sales.

Thus, this value can be used to cover tax obligations and subsequent use as available funds for other purposes. This means that this value acts as a kind of link between the indicators of gross and net profit.

Get 267 video lessons on 1C for free:

Tags: asset, balance sheet, accountant, job description of the general director, capital, loan, tax, expense, Form, formula

How to calculate it? Formula options

This indicator can be calculated using several formulas. The meaning of all methods is the same, and the final amount will not differ, so you can use any of them.

Expanded formula

PP = FP + VP + OP - N , where

- PE - net profit;

- FP - financial profit. It is calculated by subtracting similar expenses from income from financial activities;

- VP - gross profit. Calculated as sales revenue minus production costs;

- OP - operating profit. Expenses are deducted from income from other activities;

- N is the amount of taxes.

Calculation example. For example, LLC Firma in 2015 sold products worth 600 thousand rubles, the cost of which was 400 thousand rubles. One of the premises was also rented out, the proceeds amounted to 100 thousand rubles. Income from financial investments in other enterprises - 70 thousand rubles. Other costs - 100 thousand rubles.

- Let's calculate the gross profit: 600 – 400 = 200.

- Financial profit: 70 thousand rubles.

- Operating profit: 100 – 100 = 0 rub.

- Tax: (200 + 70)*20% = 54 thousand rubles.

- Net profit will be: 70 + 200 – 54 = 216 thousand rubles.

Simplified formula

PP = B + PD – SP – UR – PR – N , where

- B - revenue;

- PD - other income;

- SP - cost of production;

- UR - administrative expenses, advertising costs;

- PR - expenses for other activities;

- N is the amount of taxes paid.

Data for calculation using this method can be taken from the company’s financial performance report for the required period.

Calculation example. Let’s say the following amounts are indicated in the reports of the “Korabliki” store:

| Index | Line | 2015 (thousand rubles) |

| Revenue | 2110 | 150 |

| Cost price | 2120 | 60 |

| Business expenses | 2210 | 15 |

| Management costs | 2220 | 20 |

| Other income | 2340 | 2 |

| Other expenses | 2350 | 1.5 |

| Income tax | 2410 | 11.1 |

- Net profit will be: 150 + 2 – 60 – 15 – 20 – 1.5 – 11.1 = 44.4 thousand rubles.

Folded formula

PP = P – N , where

- P - profit;

- N is the amount of taxes.

In this calculation option, profit is understood as the difference between the organization’s total income and costs for the reporting period.

Calculation example. Let the income of LLC “Organization” in the reporting year amount to 500 thousand rubles. Cost - 300 thousand rubles. The machine was sold for 20 thousand rubles. Other costs - 100 thousand rubles.

- First you need to calculate all income: 500 + 20 = 520 thousand rubles.

- Next, we determine the costs: 300 + 100 = 400 thousand rubles.

- We determine the final profit: 520 – 400 = 120 thousand rubles.

- We charge income tax: 120*20% = 24 thousand rubles. to the budget.

- Amount of net profit: PE = P – N = 120 – 24 = 96 thousand rubles.

Balance calculation formula

Page 2400 = page 2300 – page 2410 , where

- line 2400 - net profit;

- line 2300 - profit before tax;

- line 2410 - amount of income tax.

The data for this calculation method must be taken from the income statement.

Calculation example. Let’s say the financial statements of LLC “Enterprise” contain the following data:

| Index | Line | 2015 (thousand rubles) |

| Revenue | 2110 | 150 |

| Cost price | 2120 | 60 |

| Business expenses | 2210 | 15 |

| Management costs | 2220 | 20 |

| Other income | 2340 | 2 |

| Other expenses | 2350 | 1.5 |

| Balance sheet profit | 2300 | 55.5 |

| Income tax | 2410 | 11.1 |

Net profit will be:

- (150 – (60 + 15 + 20) + 2 – 1.5) – 11.1 = 44.4 thousand rubles.

- 55.5 – 11.1 = 44.4 thousand rubles.

For more information on how to calculate this indicator, see the following video:

If you are interested in how to calculate labor productivity, read this article.

Information about what profitability is is provided here.

FAQ

Question No. 1. What are the limitations when calculating the indicator?

Answer. Depreciation is included in the calculation of earnings before taxes and can lead to different results when comparing companies in different industries. If an investor compares a company with a significant amount of fixed assets to a company that has few fixed assets, depreciation expense can hurt a company with fixed assets because the expense reduces profits.

Additionally, companies with a large amount of debt are likely to have high interest costs. Earnings before taxes reduce a company's earnings potential, especially if the company had a lot of debt. If debt is not included in the analysis, the problem may be that the firm will increase its debt due to lack of cash flow or poor sales performance. It is also important to consider that in a rising rate environment, interest costs will rise for companies that have debt on their balance sheet, and this must be taken into account when analyzing a company's financial performance.

Question No. 2. What is the indicator used for?

Answer. Profit before taxes takes into account all the profits a company generates, whether from core activities or non-core activities. The indicator calculation was invented to account for the constantly changing tax expenses of a company. It gives company owners and investors a good idea of how much profit a company makes without taking into account payments to the budget.

Question No. 3. Where is the value reflected?

Answer. Profit before tax is indicated exclusively in the income statement on line 2300.

Calculation of enterprise profit

Profit reflects the financial performance of a business.

Types of profit

- revenue

TR = P * Q

TR (total revenue) – volume of revenue

P (price) – price

Q (quantity) – quantity of goods

- gross

GP = TR – TCtech

GP (gross profit) – volume of gross profit

TR (total revenue) – revenue indicator

TCtechn (total cost) – level of technological cost

- from sales

RP = TR – TC

RP (realization profit) – the amount of profit from sales

TR (total revenue) – volume of revenue

TC (totalcost) – indicator of total cost

- clean

NP = BP – T

NP (net profit) – net profit level

BP (balanced profit) – size of balance sheet profit

T (taxes) – indicator of the size of the tax burden

- marginal

MP = TR – VC

MP (marginal profit) – level of marginal profit

TR (total revenue) – revenue size

VC – variable costs per volume of goods

- balance sheet

BP = RP – OE + OR

BP (balanced profit) – size of balance sheet profit

RP (realization profit) – level of profit from sales

OR (other revenue) – indicator of other income

OE (other expenses) - additional expenses

- operating room

OP = BP + PC

BP (balanced profit) – size of balance sheet profit

PC (percent) – interest payable

The calculation of each type of profit is important for solving certain business problems, which allows for a qualitative study of the success of activities and obtaining a clear picture of what is happening.