Why do you need 70 count?

The accounting account is used to collect information about payments to personnel. Based on the loan, the accounting department calculates salaries, increasing the company's debt to the staff. And the debit reflects payments, reducing the amount of debt to employees. Also, debit 70 of the account records the deduction of personal income tax from wages.

Account 70 has a credit balance at the end of the month, since salary accrual occurs on the last day of the month, and payment occurs in the next month, for example, on the 5th or 10th. A debit balance on account 70 is also possible, for example, if an employee’s salary was transferred more than what was accrued.

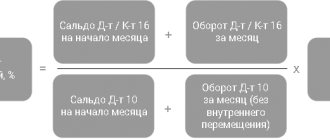

The procedure for recording transactions in SALT on account 70

Account 70 turnover is used to group information on employee payments. It forms balances at the beginning, end of the period, as well as turnover for account 70 for each employee. All operations on account 70 are regulated by section. VI Order of the Ministry of Finance dated October 31, 2000 No. 94 “On approval of the chart of accounts...”.

The debit of account 70 reflects:

- amounts paid to employees. In addition to wages, this includes bonuses, pensions, benefits, income from participation in the company’s management company, etc.);

- personal income tax withheld from wages;

- deductions based on writs of execution, etc.;

- salary deposition if the employer does not use a non-cash form of payment to employees.

On credit account 70 show:

- accrued salary amounts (due to cost, vacation reserve and other sources);

- accrued social insurance benefits;

- accrued income of employees from participation in the management company.

The balance of account 70 in the balance sheet can be passive, active, and also active-passive. But more often than not, it is passive, since salaries are calculated on the last day of the month, and they are paid to employees on the next day.

However, if the employee is paid an amount exceeding the accruals, the account balance 70 will become active or active-passive.

What is Deposited Salary?

There are situations when the salary was accrued, but the employee was not given it on time due to his absence.

Now this is rare, since most people receive their salary on a bank card, but such situations do happen. The reasons why an employee was unable to collect his salary from the cash register on time are different, for example, he was admitted to the hospital and he was unable to appear at the organization’s cash desk. In this case, his salary is deposited, that is, it is reflected as not received in the primary documents. To do this, do the wiring:

Dt 70 Kt 76. Settlements on deposited amounts

When the employee receives the deposited salary, the following posting is made:

Dt 76 Kt 50

Salaries are deposited for up to 3 years. If during this time the employee does not show up for it, then it is subject to inclusion in the company’s income.

Keep records of exports and imports in the Kontur.Accounting web service. Simple accounting, payroll and reporting in one service

general description

On account 70 “Settlements with personnel for wages” of the chart of accounts, “ information” about the organization’s debts to personnel for the payment of wages.

The account reflects the accrual of wages, the accrual of social benefits, deductions from wages to pay personal income tax and deductions for other purposes (professional contributions, alimony).

If we need to find out all the information about how much our organization owes employees for wages, what accruals for the salary were made for the period and when wages were paid, then feel free to study account 70 using basic reports in the 1C program (turnover balance sheet , account analysis, account card).

Which accounts does account 70 correspond to?

Account 70 corresponds with many expense accounts. For convenience, we have collected everything in a table.

| Account 70 corresponds by debit with | Account 70 corresponds for the loan with |

|

|

Score 70

Account 70 Designed to summarize information on settlements with employees of an organization for wages (for all types of remuneration, bonuses, benefits, pensions for working pensioners and other payments), as well as for the payment of income on shares and other securities of this organization.

In other words, this account is needed to record salaries, sick leave, and vacation pay for employees. In the credit of account 70 “Settlements with personnel for wages” the accrual amounts are reflected:

- Salaries to employees.

- Temporary disability benefits.

- Awards

- Vacation pay

- Dividends

The debit of account 70 reflects:

- Payment of wages.

- Deduction based on writs of execution (For example, alimony).

- Withholding personal income tax.

- Deposited wages. (Not issued salary on time)

Analytical accounting for account 70 “Settlements with personnel for wages” is maintained for each employee of the organization. That is, from the account you can determine who earned and how much and received salary.

Let's look at standard wiring:

- Debit 20 credit 70-1500 Wages accrued to employees of main production

- Debit 44 credit 70- 3500 Wages have been accrued to employees involved in the sale of goods; this posting can be used in trading enterprises for all employees.

- Debit 08 credit 70-4580 Wages accrued to employees involved in the construction of fixed assets.

- Debit 69 credit 70-6580 Temporary disability benefits have been accrued.

- Debit 96 credit 70-759 Vacation pay was accrued from the vacation pay reserve.

- Debit 84 credit 70- 8400 Dividends are accrued to employees if the employees are shareholders of the enterprise.

Debit 26 credit 70-2500 Wages accrued to management personnel.

The following hold transactions:

- Debit 70 credit 68-3500 Withheld Personal income tax.

- Debit 70 credit 71-800 Accountable amount withheld from salary

- Debit 70 credit 76-1000 Amounts under writs of execution (for example, alimony) are withheld from wages.

- Debit 70 credit 50-6502 Salaries issued from the cash register.

- Debit 70 credit 76-2500 Salaries deposited.

- Debit 70 credit 51- 3500 Employee salaries were transferred from the current account using bank cards.

Let's spread all the amounts into the account scheme and get:

As we can see from the diagram, the loan turnover amounted to 27,819 rubles. This indicates that 27,819 rubles were accrued for payments to employees. According to Debit, the turnover amounted to 17,802 rubles, which means that wages in the amount of 17,802 rubles were withheld and paid. The balance at the beginning of the loan is 50,000 rubles, which speaks of our debt to the employees. (Our debt, since this is the amount of the loan, and the loan is reflected in the accounts payable, is the balance). The balance at the end of the period is 60,017 rubles, also speaks of our debt to the employees.

Account balance calculation=50000+1500+2500+3500+4580+6580+759+8400-3500-800-1000-6502-2500-3500. (I gave how to calculate the balance in passive accounts in the article calculating the account balance)

The account balance (usually credit) is reflected in the liabilities side of the balance sheet, in the Current Liabilities section, under the accounts payable item.

D 91 to 68 wiring what does it mean | popular lawyer

Hello, in this article we will try to answer the question “What does D 91 to 68 wiring mean?” You can also consult with lawyers online for free directly on the website.

Followers of the second position insist that penalties, like fines, are inherently related to deviations from the rules of the Tax Code of the Russian Federation and are close to tax sanctions, and therefore should be reflected using account 99. In this case, the current income tax indicator in form N 2 (line 150) will be formed without the participation of penalties.

Account debit – reflection of the company’s other expenses:

- bank commission costs;

- shortages and damage to products and goods and materials, for which the perpetrators have not been identified or there is a court conclusion refusing to reimburse costs;

- fines and penalties required to be paid due to violations of the terms of agreements with counterparties;

- charity;

- interest on loans and borrowings;

- costs associated with the write-off of fixed assets and other assets of the company (with the exception of cash);

- write-off of expired accounts receivable;

- legal costs;

- exchange differences;

- losses of previous years accepted in the reporting period, etc.

Debit 91-2 credit 68 subaccount “property tax calculations”

On the credit side of account 68, the accounting records reflect accrued or withheld amounts of taxes and fees, and on the debit side - amounts actually transferred to the budget or otherwise reducing the debt to it.

We transfer the ending balance for each subaccount from November, it will be the beginning balance for December.

If there are any other sub-accounts on account 91, then they are closed in the same way to the 9th sub-account. Depreciation is the gradual transfer of the cost of a fixed asset to the cost of products (works, services).

Income related to the sale of own assets (with the exception of cash), interest payments to counterparties for the use of provided funds, participation in the authorized capital of third-party companies: income is accepted in the same way as revenue recognition.

Note! For business entities that, according to the criteria, are classified as small businesses, the application of PBU 18/02 is a right, not an obligation.

In the previous article, we examined the accounting of income and expenses received from the normal activities of the organization. Other income and expenses are recorded on 91 accounting accounts. The data from this account also forms the final financial result of the enterprise.

Account 68 “Calculations for taxes and fees”

The account reflects all transactions to charge VAT to the budget, as well as transactions to reduce VAT previously paid to suppliers of goods and services. I will not dwell on the rationale for such operations; in general, based on the analysis of account 68.02, the document “VAT Declaration” is drawn up. The account is used very often if your organization is a VAT payer.

Account 70 in accounting

The credit of the account reflects the accrual of wages to all categories of employees. The debit of the account reflects deductions from wages and their payment. The credit balance shows the balance of the company's wages owed to employees.

The 70 account diagram is shown below in the figure:

There are cases when an employee’s salary is paid for a full month, but accrued according to the timesheet for an incomplete month. For example, at the end of the month an employee took sick leave. In such cases, it is not the enterprise, but the employee who becomes the debtor. The balance in such cases remains a credit balance with a minus sign.