What is a payslip, are there any requirements for its preparation?

According to Art. 136 of the Labor Code of the Russian Federation, every employer who has at least 1 employee on his staff is obliged to notify him in writing on a monthly basis:

- about the components of his salary for a fixed period;

- the amount of other funds accrued to the employee;

- the amount of funds withheld and the reasons for this;

- the total amount due to him for a fixed period.

All this information is reflected in the payslip, which is issued to the employee regularly for each month. The legislation does not regulate the form of drawing up this document; it is approved by the relevant local act of the organization, and the opinion of the trade union must be taken into account.

See a sample payslip here.

Read about the features of registration and issuance of pay slips in the article prepared by ConsultantPlus specialists. Take advantage of a free trial access to the system to get acquainted with expert recommendations.

Despite the absence of strict requirements for the form of this document, it is important to remember that it must contain sections that indicate how many funds:

- accrued;

- withheld;

- paid;

- payable (or the amount of debt - both the employee and the employer).

Decoding the codes on the pay slip

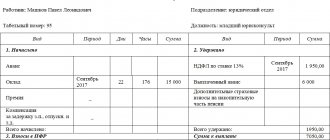

The sheet must be personalized, that is, contain information about the employee (last name, first name, patronymic, position and personnel number).

- It must have two large columns “Accrued” and “Retained”. In the “Accrued” column, all types of earnings should be listed: basic salary, all types of bonuses, overtime pay, bonuses, sick leave payments, vacation pay, and so on.

In this case, it is necessary to indicate the number of days and hours worked. Allowances must be indicated separately for each type. ImportantFor example, for length of service, qualifications, special working conditions, etc. The column “Withheld” shows the amount of personal income tax (13%), deductions on writs of execution (alimony, etc.), fines.

Amounts may also be withheld for damage caused to the enterprise or compensation for shortfalls. At the request of the employee, union dues may also be withheld from him, for example.

The main accounting document, which is issued to the employee and contains all types of accruals, is the payslip. It presents a detailed calculation on the right side - tax deductions from wages and the amount of money paid, and on the left - the amounts that are accrued with differentiation according to the types of various payments. In addition, in accounting, special codes are used to calculate remuneration for labor - these are the organization’s accounts, the digital values of which differ depending on the field of activity of the particular legal entity in question.

Income code "salary"

The employee's type of income must be completely clear to him. That is why it is necessary to decipher the codes on the payroll sheet. The employer can indicate it on each pay slip or familiarize employees with such information once.

The assignment of codes for each financial transaction to the accounting department is regulated by the Federal Tax Service order “On approval of codes for types of income and deductions” dated September 10, 2015 No. ММВ-7-11/ [email protected] (as amended by the Federal Tax Service order dated October 24, 2017 No. ММВ-7-11/ [ email protected] ).

According to it, funds paid to an employee as payment for his work are assigned code 2000.

Transfer of personal income tax and contributions

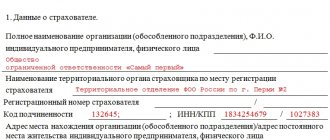

No later than the day following the day of salary payment, the organization is obliged to pay personal income tax. Insurance premiums, including insurance premiums, are paid by the 15th of the following month. Payment is made from the current account (account 51), the debt to the Federal Tax Service and funds is closed (accounts 68 and 69). Postings:

Read more: Which blood group is suitable for the first negative

D68 K51 - personal income tax paid

D69 K51 – fees paid

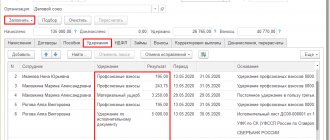

Example of payroll with postings

Employees were paid salaries for March 2021, personal income tax was withheld, and insurance premiums were calculated. Accounting for account 70 is carried out without analytics for employees, for account 69 - with subaccounts for each contribution. Expenses for salaries and contributions are included in account 20.

04/10/2019 – salary paid, personal income tax paid,

04/15/2019 – insurance contributions to the Pension Fund, Federal Migration Service, and Social Insurance Fund were paid.

| Full name | Accrued | Personal income tax | Paid |

| Ivanov I.I. | 25 000 | 3 250 | 21 750 |

| Petrov P.P. | 20 000 | 2 600 | 17 400 |

| Sidorov S.S. | 30 000 | 3 900 | 26 100 |

| Total | 75 000 | 9 750 | 65 250 |

- in the Pension Fund of Russia (22%) - 16,500 rubles

- to the Federal Migration Service (5.1%) - 3,825 rubles

- FSS (2.9%) - 2,175 rubles

- FSS injuries (0.9%) - 675 rubles

Postings for all operations:

| date | Wiring | Sum | Contents of operation |

| 31.03.2019 | D20 K70 | 75 000 | Salary accrued |

| D70 K68.NDFL | 9 750 | Personal income tax withheld | |

| Insurance premiums charged: | |||

| D20 K69.pfr | 16 500 | - to the Pension Fund of Russia | |

| D20 K69.fms | 3 825 | - to the FMS | |

| D20 K69.fss1 | 2 175 | - in the Social Insurance Fund (temporary disability) | |

| D20 K69.fss2 | 675 | — in the Social Insurance Fund (injuries) | |

| 10.04.2019 | D68.NDFL K51 | 9 750 | Personal income tax listed |

| D70 K50 | 65 250 | Employees' salaries were paid from the cash register | |

| 15.04.2019 | Insurance premiums listed: | ||

| D69.pfr K51 | 16 500 | - to the Pension Fund of Russia | |

| D69.fms K51 | 3 825 | - to the FMS | |

| D69.fss1 K51 | 2 175 | — FSS (temporary disability) | |

| D69.fss2 K51 | 675 | — FSS (injuries) | |

Keeping accounting records in the online service Kontur.Accounting is convenient. Quick establishment of a primary account, automatic payroll calculation, collaboration with the director.

Return to Payroll 2018

The wage type code in the timesheet reflects information about what a particular amount was accrued for. Special columns are provided for entering codes in unified timesheet forms. Find out what codes to use in your time sheet from our material.

A time sheet is a supporting document on the basis of which employees’ salaries are calculated. A Russian organization has the right to independently develop a form for recording the working hours of its personnel or use forms approved by the State Statistics Committee in the form T-12 or T-13.

The timesheet records the daily amount of time worked by each employee, as well as the total number of hours of attendance (absenteeism) by type of paid labor. Each type of labor corresponds to a specific code.

Codes for types of remuneration in the T-12 form sheet are filled out only if the organization maintains the second part of the specified form. Here, to reflect information about wages, a whole section is highlighted, which is called “Calculation with personnel for wages”. It indicates the type of remuneration not only in coded form, but also its name, for example salary (name) 2000 (code).

In the form of the T-13 working time sheet, columns 7, 8 and 9 are intended to reflect information on the calculation of wages, which are duplicated twice in this form.

The code can be entered in two ways:

• If the type and corresponding account for payroll is the same for all employees indicated in the timesheet, then the code is placed in the line “wage code”, which is located at the top and covers all columns from 7 to 9.

Read more: Temporary registration of a child for school consequences

• In the case when there are different types of accrual in the timesheet, the code is entered in the corresponding cell, in column 7, opposite each employee.

Up to 8 such codes can be used for one employee in this form of time sheet.

The list of wage codes that should be used in timesheets at the legislative level has not been approved, and in the Goskomstat Resolution “On approval of unified forms of primary accounting documentation for accounting of labor and its payment” No. 1, such details as payment code are only mentioned and only regarding form T-13. Nevertheless, columns for entering this designation are provided in both forms of timesheets.

Since the legislation has not established a specific list of codes, the employer can approve them independently.

You can do this in two ways:

• Develop your own internal local document, in which to encode all types of remuneration and additional employee benefits available at the enterprise.

• Use the list approved for other purposes, for example, the List of codes for types of income for tax purposes, approved by order of the Federal Tax Service of Russia No. ММВ-7-11 / [email protected] The use of this document is all the more advisable if accounting at the enterprise is carried out using specialized programs.

In this case, documents containing tax information, for example, forms 1-NDFL, 2-NDFL, etc., and payroll documents will have the same designations.

Let's look at the codes from the list for the tax office that can be used in timesheets:

• 2000 - the main code, it is used to reflect wages, that is, all amounts accrued for the employee’s performance of his job duties, with the exception of bonuses;

• 2002 - the amount of bonuses for the performance of labor duties, which are paid not at the expense of the organization’s profits, that is, they participate in reducing the profit tax base;

• 2003 - bonus amounts paid from the organization’s profits or targeted cash receipts;

• 2012 — payment of annual paid vacations;

• 2300 – payment of sheets for temporary incapacity for work;

• 2530 - code reflecting amounts paid to the employee in kind, that is, not in money; This code can be entered only if it is possible to indicate the exact number of days (hours) for which the salary is paid.

The list of codes for tax purposes has been supplemented with new income codes that will be applied from the beginning of 2021.

It seems difficult to reflect the entire accrued salary of an employee in the timesheet. This is the main reason why time sheets are most often used only to record time worked.

The legislation does not contain a specific list of wage codes for use in timesheets. In this regard, the employer can independently develop a list of codes and approve it as an internal document or use a list of codes approved for other purposes, in particular, it is convenient to use the list of codes for taxation of personal income.

Tax report 2021 Tax accounting 2021 Sales tax 2018 Inheritance 2021 National economy 2018

Deciphering payroll codes allows the employee to obtain comprehensive information about the amount of accruals and deductions. The procedure for compiling a payslip and the main codes used in it will be discussed in our article.

Salary codes in the payslip (or certificate 2-NDFL)

There are other salary codes that are also subject to indication in the 2-NDFL certificate:

2012 — vacation payments;

2300 — payment of sick leave;

2760 - payment of funds as financial assistance provided to an employee or former employee who retired due to disability or age;

4800 is a universal code that designates all payments that do not have a special code (for example, additional payments and compensation).

See also “Deciphering the codes in the 2-NDFL certificate.”

Payroll sheet

To code 514, columns 13, 17. From 01/01/2009 to 01/01/2012, in accordance with paragraph 40 of Article 217 of the Tax Code of the Russian Federation, amounts paid by organizations to their employees to reimburse the costs of paying interest on loans (credits) for the acquisition and ( or) construction of residential premises, included in the expenses taken into account when determining the tax base for corporate income tax. In accordance with clause 24.1 of Article 255 of the Tax Code of the Russian Federation, labor costs when calculating corporate income tax include expenses for reimbursing the costs of employees in paying interest on loans (credits) for the purchase and (or) construction of residential premises.

Wage type code: additional explanation

In addition to the listed salary codes, the order of the Federal Tax Service approved the following designations for income indicated in the 2-NDFL certificate:

1010 — dividends;

2001 - remuneration or similar payment to the company’s management structure;

2010 - payment based on a civil contract;

Subscribe to our newsletter

Yandex.Zen VKontakte Telegram

2530 - remuneration in kind;

2720 - income received as a gift;

2762 - payment of financial assistance to employees at the birth, adoption of a child.