How to make an update on 4FSS regarding additional accrued contributions based on the results of an on-site inspection

Dolina LLC did not accrue insurance premiums to the Pension Fund in a timely manner. As a result, due to the delay, the company's penalties increased by the end of the reporting period. The management decided to cover the debt through the discovered overpayment of Pension Fund contributions. The accounting department of Dolina LLC made the following entries:

- DT 99 CT 69 (collection “Payments for penalties of the Pension Fund”) - penalties for late insurance payments;

- DT 69 (collection “Payments for Penal Fund Penalties”) CT 69 (collection “Insurance Contributions to the Pension Fund”) - covering penalties by overpayment of Pension Fund contributions.

The accounted overpayment completely covered the penalty. Answers to frequently asked questions Question No. 1: How should a private entrepreneur pay additional insurance premiums if he has employees and when is reporting submitted in this case? The entrepreneur makes transfers for himself and all his employees, including those who have entered into a contract with him.

- Is it possible to clarify the SZV-M form?, No. 22

- SZV-M: reflecting the GPD with the start of work in the future, No. 19

- Due to the extra gap in admission to SZV-M, they will no longer be denied, No. 19

- When the fine for errors in SZV-M will be written off by collection, No. 19

- How to report to the Pension Fund about a founding director without salary, No. 19

- Main payments to individuals in reporting: 6-NDFL, RSV-1 and 4-FSS, No. 17

- Is an extra space in the SZV-M form a reason for a fine from the Pension Fund of Russia?, No. 17

- Travel expenses and RSV-1, No. 14

- Registration with the Social Insurance Fund: new rules, No. 12

- How NPOs confirm their main activity in the Social Insurance Fund, No. 8

- We fill out the new monthly form SZV-M, No. 8

- RSV-1: reflecting non-standard situations, No. 6

- RSV-1: working on mistakes, No. 5

- You will need to report to the Pension Fund on a monthly basis, No. 3

- "Away" duet of the Pension Fund of Russia and the Social Insurance Fund, No. 2

- 2015

Responsibility for failure to submit reports on insurance accruals and other violations Erroneous actions in the preparation of reports, failure to meet deadlines for submission, evasion of contributions by legal entities and emergency situations can have serious consequences. Depending on the degree of violation, the obligated person is subject to administrative liability, fined or charged a fine.

Main violations Sanctions Ground Failure to submit reports in accordance with the required deadlines Fine 5% of the amount of the insurance payment that must be made for each month (from 1000 rubles, but not more than 30% of the amount); The countdown starts from the date when it was necessary to pay the Tax Code of the Russian Federation, Article 119, clause 1. Lowering the tax base for calculating insurance payments. A fine of 20% of the unpaid amount, but not more than 40,000 rubles. Tax Code of the Russian Federation, art.

Correction of the 4-fss form

- How are fines calculated for late submission of Form 4-FSS, No. 21?

- How to count insured persons so as not to make a mistake with the procedure for submitting RSV-1, No. 20

- Features of filling out 4-FSS based on the results of 9 months of 2015, No. 19

- How to submit an updated calculation using the RSV-1 form, No. 19

- RSV-1 for the first half of 2015: filling out in a new way, No. 15

- Complaint as a final argument, No. 15

- Competent objections = good solution to the “stock” check, No. 14

- For the first half of 2015, you need to take the RSV-1 using a modified form, No. 14

- How to fill out RSV-1 to determine the length of service of the person with whom the GPA is concluded, No. 8

- We will submit the corrected 4-FSS in April, No. 7

- Will urgent correction of individual information after an on-site inspection save the Pension Fund from a fine, No. 4

- 2014

How are additional insurance premiums calculated for previous periods in 2021?

It happens that sometimes individual entrepreneurs who previously worked without employees and subsequently entered into employment contracts with individuals never pay contributions of the type in question. Ultimately, such a practice is discovered, and the Federal Tax Service obliges the corresponding payments to be made.

If any period is missed, then a fairly serious fine will most likely be imposed on the enterprise or individual entrepreneur. Its value is calculated based on the amount of debt to the extra-budgetary fund - the legislation indicates the corresponding interest rates.

Important

According to the inspection report Sometimes the need to make additional calculations of insurance premiums for past periods in the Social Insurance Fund arises after a desk inspection has been carried out. In this case, the basis confirming the need to perform this action is the audit report drawn up by the auditors.

Attention

Number of seats

Another popular question: how to reflect the special assessment in 4 FSS in 2020, in particular, fill out table 5. It always reflects the number of jobs, and the source of payment for expenses (contributions or the company’s own money) does not matter.

Table 5 must be filled out based on data on special assessments and mandatory medical examinations of workers. In line 1 you need to indicate the indicators based on the results of the special assessment as of January 1 of the current year (2020). Line 2 shows the number of employees whose work is associated with harmful or dangerous working conditions and, in connection with this, are required to undergo preliminary and periodic medical examinations. Certificates from medical commissions are used to fill out.

Filling out Table 1 “Calculation of the base for calculating insurance premiums” of the Calculation form

7. When filling out the table:

7.1. line 1 in the corresponding columns reflects the amounts of payments and other remuneration accrued in favor of individuals in accordance with Article 20.1 of the Federal Law of July 24, 1998 N 125-FZ on an accrual basis from the beginning of the billing period and for each of the last three months of the reporting period ;

7.2. in line 2 in the corresponding columns the amounts not subject to insurance premiums are reflected in accordance with Article 20.2 of the Federal Law of July 24, 1998 N 125-FZ;

7.3. line 3 reflects the base for calculating insurance premiums, which is defined as the difference in line indicators (line 1 - line 2);

7.4. line 4 in the corresponding columns reflects the amount of payments in favor of working disabled people;

7.5. line 5 indicates the amount of the insurance tariff, which is set depending on the class of professional risk to which the insured belongs (separate division);

7.6. in line 6 the percentage of the discount to the insurance rate established by the territorial body of the Fund for the current calendar year is entered in accordance with the Rules for establishing discounts and surcharges for policyholders to insurance rates for compulsory social insurance against industrial accidents and occupational diseases, approved by the Decree of the Government of the Russian Federation dated 30 May 2012 N 524 “On approval of the Rules for establishing discounts and surcharges for insurers on insurance rates for compulsory social insurance against industrial accidents and occupational diseases” (Collected Legislation of the Russian Federation, 2012, N 23, Art. 3021; 2013, N 22 , Art. 2809; 2014, No. 32, Art. 4499) (hereinafter referred to as Decree of the Government of the Russian Federation of May 30, 2012 N 524);

7.7. line 7 indicates the percentage of the premium to the insurance rate established by the territorial body of the Fund for the current calendar year in accordance with Decree of the Government of the Russian Federation dated May 30, 2012 N 524;

7.8. line 8 indicates the date of the order of the territorial body of the Fund to establish an additional premium to the insurance tariff for the policyholder (separate unit);

7.9. line 9 indicates the amount of the insurance rate, taking into account the established discount or surcharge to the insurance rate. The data is filled in with two decimal places after the decimal point.

Explanation of the adjustments made according to the inspection report in the 4 fss report

Menu

Home — Financial law — Explanation of the adjustment of the audit carried out on the audit report in the 4 FSS report

Independent verification of the report FSS specialists carry out verification based on the benchmark indicators established for different columns of the table. Using their algorithm, you can evaluate the finished document yourself. For example, when filling out reports for the first quarter of the year, the amount of accrued contributions payable is always indicated as zero.

If the document is prepared based on the results of six months, 9 or 12 months, it is equal to the indicator at the end of the previous period. The policyholder cannot have both a debt to the Social Insurance Fund and the Fund's debts to it. Independent monitoring of completed reporting requires time and care.

There is a way to simplify this task - using special software products.

In what cases is it possible to make adjustments in the 4-FSS report?

Before starting to work with this document, you should review its original and take into account all the comments of the tax inspector. As practice shows, most complaints arise regarding the kopecks indicated in the amounts.

https://www.youtube.com/watch?v=FFU5tJ4EtDY

Once you have made all the appropriate changes to the database and achieved consistency, you can safely enter the changed values

When filling out the title page, you should pay attention to the line “Adjustment number” (Art.

17 of Law No. 212-FZ): it contains a digital value indicating which account calculation, taking into account the changes and additions made, is submitted by the policyholder to the territorial body of the Social Insurance Fund (for example: “001”, “002”, “003”, ... "010 " etc.).

Correction of the 4-fss form

AttentionThe sequence of actions is as follows:

- Log in to the social insurance website https://portal.fss.ru and go to the menu item https://portal.fss.ru/fss/services/f4input.

- On the portal, an electronic document template is filled out or an already generated report is uploaded.

- The 4-FSS report is checked on the FSS website, and the result produced by the program is analyzed.

Desk type of verification activities Non-visiting data reconciliation is carried out by employees of the regulatory body without the participation of the policyholder. The documentary basis for verification is the fact of receipt of the report.

According to its content, the correctness of calculations for insurance premiums, the completeness of their transfer, and compliance with the deadlines for repayment of obligations are analyzed.

Error 404

In the “code” line, the period for which the calculation is being submitted and the number of requests from the policyholder for the allocation of the necessary funds to pay the insurance compensation are entered. The reporting periods are the first quarter, half a year and nine months of the calendar year, while the billing period is the calendar year, which is designated by the number “12”.

Let us remind you that the amounts in the first and second sections of the report must match completely. Thus, if an adjustment is made for June 2011, then this value is entered in the “3rd month” line. In both sections, the data in this line and the total accrual amount for the last three months of the reporting period should be corrected.

4-fss adjustment

Such innovations lead to errors in the releases of electronic programs for the new reporting form, which, as a rule, appear immediately before the start of its submission and are reissued almost every day during the “hot period”.

Therefore, until the deadline for submitting reports, an accountant cannot be completely sure that he has the right option. The FSS recommends that policyholders do not wait for letters from the fund demanding that they submit an update, but conduct a data check themselves.

Penalties on insurance premiums do not need to be calculated independently in the same way as the FSS calculates them itself.

Typical errors After checking the 4-FSS reports for the second quarter, fund employees compiled a list of the most common errors when filling them out. 1.

Online magazine for accountants

Social security reporting is considered submitted if the 4-FSS report has been successfully verified. If any shortcomings are found in the document, they must be promptly eliminated in order to have time to submit a new version of the completed form within the established time frame.

Identification of errors is not grounds for postponing deadlines for submitting reporting forms. Subscribe to the accounting channel in Yandex-Zen!

- 1 Ways to check reports

- 2 Checking on your own

- 3 Desk type of verification activities

- 4 Monitoring as part of an on-site inspection

Methods for checking reports by Law of July 24, 1998 No. 125-

Important

When can a corrective 4-FSS be submitted?

The updated 4-FSS, sent to the fund after the expiration of the deadline established for submitting reports using the 4-FSS form, does not provide grounds for recognizing the taxpayer as having violated the deadline for submitting these reports in the event that information is corrected, the basis for calculating contributions for which becomes inflated (Clause 2 of Article 17 of Law No. 212-FZ).

If the corrective document is submitted before the deadline for sending reports to social security, Form 4-FSS is considered submitted on the day the corrective document is submitted to the fund (Clause 3, Article 17 of Law No. 212-FZ).

If the adjustment is sent to the Social Insurance Fund after the expiration of the deadline, while the contribution base has become underestimated as a result of errors, the taxpayer is released from liability under one of the following conditions:

- The updated form 4-FSS was sent to the fund until the moment when the taxpayer was informed about his error in the calculations by the auditing authority.

- The updated Form 4-FSS was sent to the fund before the on-site inspection of the company was scheduled for the corresponding reporting period.

- An audit conducted by the Social Insurance Fund did not show that the company made any errors in reporting, which led to an understatement of the base for calculating contributions.

In this case, sanctions are not imposed on the policyholder only if, before the appearance of the conditions reflected in paragraphs above. 1 or 2, it managed to transfer to the budget the missing amount of contributions, as well as penalties calculated in the manner prescribed by law.

How to fill out an interim report

The report is prepared in accordance with Form 4-FSS. In terms of filling out the interim report, it does not differ from the standard quarterly report.

There are several features that should be taken into account when filling out interim reporting to the Social Insurance Fund:

- There is no fixed date for submitting the report. It is compiled as needed.

- On the title page of the report, in the “Reporting period” field, you need to fill in the second pair of cells (after the fraction). The cells contain the serial number of the interim reporting. If the company is renting it out for the first time, you need to enter code 01.

- The report (in tables with monthly data) reflects data for the first or first and second months of the quarter. The report itself is submitted from January to the month in which benefits were paid.

- Along with the report, you must submit an application and supporting documents (sick leave, child’s birth certificate, etc.).

Submit the 4-FSS interim report online without errors and right now. 3 months Kontur.Externa as a gift!

Online magazine for accountants

Social security reporting is considered submitted if the 4-FSS report has been successfully verified. If any shortcomings are found in the document, they must be promptly eliminated in order to have time to submit a new version of the completed form within the established time frame.

Identification of errors is not grounds for postponing deadlines for submitting reporting forms. Subscribe to the accounting channel in Yandex-Zen!

- 1 Ways to check reports

- 2 Checking on your own

- 3 Desk type of verification activities

- 4 Monitoring as part of an on-site inspection

Methods for checking reports by Law of July 24, 1998 No. 125-

Important

The Federal Law establishes that filing and checking Form 4-FSS is the responsibility of all types of employers. They prepare the document on a quarterly basis.

Deadlines for submitting the new form 4-FSS from 2021

The deadlines for submitting a new calculation for “injuries” remained the same, and depend on the number of employees of the insured (clause 1, article 24 of the law dated July 24, 1998 No. 125-FZ):

- if there are more than 25 employees, then the calculation is submitted electronically, and the deadline for submitting form 4-FSS 2021 is no later than the 25th day of the month, after the reporting quarter;

- if there are fewer employees, then the calculation can be submitted on paper, but in a shorter period of time - on the 20th of the month following the reporting period.

The calculation must be submitted quarterly on an accrual basis. For the 1st quarter of 2021, the electronic form is due on 04/25/2017, and the paper form is due on 04/20/2017.

If the electronic form is not followed when it is necessary, the policyholder faces a fine of 200 rubles. For late submission of Form 4-FSS from 01/01/17, a fine is imposed on only one basis - contributions for “injuries”. For each overdue month, the FSS will collect from 5% to 30% of the amount of contributions excluding benefits paid, but not less than 1000 rubles.

Let us remind you that by April 15, policyholders must confirm their main type of activity by submitting to the Social Insurance Fund a certificate indicating those types of businesses for which income was received in 2021. If this is not done, the Fund will assign the highest class of pro-insurance from all types of activities of the policyholder, which will increase the rate of contributions for “injuries” (Resolution of the Government of the Russian Federation dated June 17, 2016 No. 551).

Reimbursement of Social Insurance Fund expenses in 2020

Since 2021, contributions for temporary disability and maternity (VNiM) have come under the control of the Federal Tax Service, while the FSS retains only contributions from accidents and occupational diseases (NSiPZ). Due to the change of administrative bodies, these contributions are reflected in different reports:

- VNiM - as part of a new unified calculation of contributions to the tax service;

- NSiPZ - according to form 4-FSS to the social insurance fund.

In 2021, reimbursement of contributions is provided by Social Insurance. If the overpayment occurred after January 1, 2021, then the following must be submitted to the Social Insurance Fund:

- application for reimbursement in the form recommended for use by the FSS letter dated December 7, 2016 No. 02-09-11/04-03-27029;

- a calculation certificate containing information on accrued, reimbursed, and paid contributions to VNiM;

- copies of documents confirming expenses.

Please note: regarding contributions for temporary disability and maternity (VNiM), interim reports are not required to be submitted to the social insurance fund. If the overpayment occurred for the period 2021 and earlier, then you can make such a report in the Kontur.Extern system as follows: when filling out the details of the 4-FSS form, you need to clear the “Reporting period” field and fill in the “Subsidy application number” field with the required number

Next, the report is printed and submitted independently to the Fund.

If the overpayment occurred for the period 2021 and earlier, then you can make such a report in the Kontur.Extern system as follows: when filling out the details of the 4-FSS form, you need to clear the “Reporting period” field and fill in the “Subsidy application number” field with the required number. Next, the report is printed and submitted independently to the Fund.

Table 7 of Section II of Form-4 FSS (calculation updated) (fragment)

| Indicator name | Line code | Sum |

| 1 | 2 | 3 |

| Debt due to the policyholder at the beginning of the billing period | 1 | — |

| Accrued for payment of insurance premiums | 2 | 596,00 |

| At the beginning of the reporting period | — | |

| For the last three months of the reporting period | 596,00 | |

| 1 month | 74,00 | |

| 2 month | 262,00 | |

| 3 month | 260,00 |

Note. The amount of insurance premiums is underestimated by 62 rubles.

Since the updated calculation for the reporting period is being submitted for the first time, we indicate code 001 in the “Adjustment number” field on the title page of Form-4 FSS. A fragment of filling out the title page of the updated calculation for the first quarter of 2013 is given below.

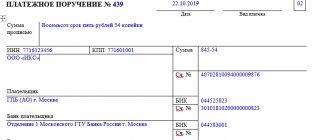

Submitted no later than the 15th day of the calendar month following the reporting period to the territorial body of the Social Insurance Fund of the Russian Federation Form-4 FSS Registration - -TTTTTTTTTT-¬ -TTTTTTTTTT-¬ -TT-¬ number ¦7¦7¦0¦4¦0¦ 1¦5¦8¦6¦9¦/¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ Page ¦0¦0¦1¦ of the policyholder L-+-+-+-+-+-+-+-+-+— L-+-+-+-+-+-+-+-+-+— L- +-+— —TTTT-¬ Code ¦7¦7¦0¦4¦ ¦ subordination L-+-+-+-+— CALCULATION for accrued and paid insurance contributions for compulsory social insurance in case of temporary disability and in connection with maternity and for compulsory social insurance against industrial accidents and occupational diseases, as well as for the costs of paying insurance coverage Number —TT-¬ —TTTT-¬ —TTT-¬ adjustments- ¦0¦0¦1¦ Reporting period ¦0¦3 ¦/¦ ¦ ¦ Calendar year ¦2¦0¦1¦3¦ roving L-+-+— (code) L-+-+-+-+— L-+-+-+— (03—I quarter. ; 06 - half a year; (000 - initial, 09 - 9 months; 12 - year/01, 02 -¬ 001, etc. - etc. - when applying for Termination ¦ ¦ number of allocation of necessary funds for activities L— adjustments) for payment of insurance coverage)—————————————————————————¬¦ Limited Liability Company "Romashka" ¦L——————— ——————————————————

Note. Before submitting the updated calculation, it is necessary to pay all additional assessed contributions and penalties (Part 4 of Article 17 and Clause 1 of Article 47 of Law No. 212-FZ).

Along with the corrective calculation, it is advisable to submit a covering letter to the Social Insurance Fund about the changes made in the calculation. This will help eliminate additional questions from inspectors when conducting a desk audit regarding this updated calculation. How to write an explanatory (covering) letter will be discussed below.

Tags: accountant, tax, expense

What form should I use to submit a “clarification” to the FSS of the Russian Federation?

The corrective calculation must be submitted on the form that was used to submit reports during the period when the error was made (Part 5, Article 17 of Law No. 212-FZ).

Note. Reasons for submitting a clarification

If a fact of non-reflection or incomplete reflection of information, as well as errors leading to an underestimation of the amount of insurance premiums payable, is detected in an already submitted calculation for accrued and paid insurance premiums, the accountant is obliged to make the necessary changes to the previously submitted calculation (that is, submit an updated calculation) ( Part 1 of Article 17 of Law No. 212-FZ).

Law No. 212-FZ does not contain requirements to submit a corrective calculation in case of overestimation of the amount of insurance premiums. In this case, the payer has the right to submit an updated calculation (and it is advisable to do this).

We add that the territorial bodies of the fund are required to accept updated calculations from policyholders both for the current period, for example in April 2013 for the first quarter of 2013, and for past settlement periods - in April 2013 for 2011 or 2012.

The only difference is that when filling out the title page of the updated calculation for the corresponding period, in the “Adjustment number” field, the payer of insurance premiums must indicate which account calculation, taking into account the changes and additions made, is submitted by the policyholder to the territorial body of the Social Insurance Fund (for example, 001 , 002… 007 etc.). For a fragment of filling out the title page, see p. 36.

When preparing an updated calculation, the general filling procedure is applied. The payroll must be filled out completely, and not just the table of the section in which the indicators change. We will show you with an example how to correctly make corrections to a payslip.

Example 1. Romashka LLC submitted reports to the Federal Social Insurance Fund of the Russian Federation for the first quarter of 2013 on time. In April 2013, the accountant discovered that an arithmetic error was made in the submitted calculation - the amount of payments in favor of individuals for February was underestimated by 31 000 rub. As a result, the amount of insurance contributions for compulsory social insurance was incorrectly calculated:

- in case of temporary disability and in connection with maternity;

- for injuries.

Romashka LLC must submit to the territorial branch of the FSS of the Russian Federation an updated calculation in accordance with FSS Form-4 for the first quarter of 2013. How to make corrections to the reporting?

Note. The calculation according to FSS Form-4 for the first quarter of 2013 is filled out according to the form established by Order of the Ministry of Health and Social Development of Russia dated March 12, 2012 N 216n.

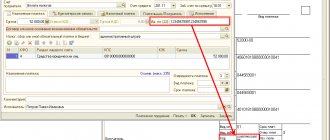

Solution. We adjust the indicators of section. Form I-4 of the Social Insurance Fund, which reflects information on accrued and paid insurance contributions for compulsory social insurance in case of temporary disability and in connection with maternity and expenses incurred.

Let's correct the indicators of the table in Section 3. I form-4 FSS. In the primary reporting, the organization incorrectly indicated the base for calculating insurance premiums for February.

In line 1, column 5 of table 3, section. The first calculation according to FSS Form-4 indicated the amount of 100,000 rubles. (sample 1).

Sample 1