IT and SHE: what is it and how to calculate

Deferred tax assets (DTA) and deferred tax liabilities (DTL) are special concepts introduced into the accounting system to reflect the differences between accounting and tax profits.

The article “Calculating the difference between accounting and tax profit” will tell you why such differences arise.

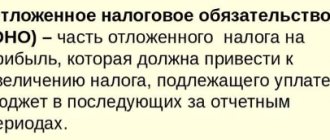

How accounting legislation deciphers the terms ONA and ONO, see the figure:

SHE and IT are determined based on the size of temporary differences, due to which differences arise between accounting and tax profits. The difference arises due to the fact that certain expenses and income are recognized in accounting in the reporting tax period, and in tax accounting in the next period and vice versa. To calculate the amount of SHE and IT, you need to multiply the temporary difference by the income tax rate.

What changes in income tax await us:

- “The list of income on which it is not necessary to pay income tax has been added”;

- “Disputes around the income tax rate: one less reason.”

Correct calculation of discrepancies in the amount of accounting and tax profits allows you to generate reliable indicators in reporting, as well as determine the amount of tax payments for the current and subsequent periods.

Accrual example

For example, Fialka LLC received revenue of 500,000 rubles, expenses for core activities amounted to 600,000 rubles. In order to summarize the results, the turnover in subaccounts 90 “Sales” fell to 90.09.

Also during the period, income from other activities was received in the amount of 100,000 rubles and expenses were incurred in the amount of 50,000 rubles. Turnovers from other activities are maintained on account 91 “Other income and expenses”. By analogy with account 90, a balance was formed on subaccount 91.9.

In turn, 90.09 and 91.09 are closed by transferring to account 99. A calculation is made to see what result the company got.

Table 1. Movements by revolutions

| RAS number | Debit amount | Loan amount |

| 90.09 | 600 000,00 | 500 000,00 |

| 91.09 | 50 000,00 | 100 000,00 |

| Account turnover 99 | 650 000,00 | 600 000,00 |

| Account balance 99 | 50 000,00 |

Consequently, the company incurred a loss on account 99 in the amount of 50,000 rubles. When calculating income tax in the program, the following will be recognized from this amount:

- 50,000 * 20% = 10,000 rubles;

- Dt 68.04 Kt 99 - income tax was reduced by 10,000 rubles;

- Dt 09 Kt 68.04 - reflected 10,000 rubles.

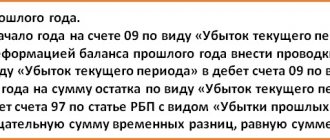

Before the balance sheet reformation, IT was transferred from a loss to deferred expenses:

- Dt 09 Kt 09 - 10,000 rubles.

At the same time, the accountant made an entry in tax accounting:

- Dt 97 “Future expenses” Kt 99 - in the amount of 50,000 rubles of transferred loss.

There is no need to record any amounts in this entry in accounting.

Which entry should be used to record the amount of tax liabilities and assets?

SHE and IT are reflected in accounting in two ways:

- As differences arise in accounting and tax accounting;

- At the time of calculation of income tax at the end of the year or reporting period.

The first method is typical for automated accounting programs. The second method is used in conditions of manual calculations for income tax.

How the amount of a deferred tax asset can be reflected - the posting links the following accounting accounts:

How the amount of deferred tax liability can be reflected - the posting is as follows:

Thus, different accounting accounts are provided for ONO and ONA. At the same time, all information about the value of these indicators is collected in one subaccount “Calculations for income tax” to account 68. As a result, SHE and IT participate in determining the final amount of the current income tax.

The latest clarifications on legislative innovations can be found on our website:

- “Land tax: changes 2019”;

- “Starting from 2021, the sale of part of the property of individual entrepreneurs will be preferential”;

- “The deduction for Plato is cancelled.”

Growing an asset from a loss

The application of PBU 18/02 “Accounting for income tax calculations” raises a lot of questions among accountants. One of them is whether additional accounting entries need to be made if the organization has incurred a loss and there is no current income tax? Yes need. We will tell you which ones in our article.

It’s unusual to grow an asset from a loss. However, from January 1 of this year, thanks to PBU 18/02 “Accounting for income tax calculations”, this is a new responsibility of the accountant. According to PBU 18/02, different rules for accounting and tax accounting of received losses lead to the formation of a deferred tax asset, which must be reflected in the accounting accounts and financial statements.

We don’t want to scare readers, but we’ll immediately warn you what the fine is for failure to comply with the requirements of the PBU. For distortion of any article (line) of the financial reporting form by at least 10 percent, a fine of 2,000–3,000 rubles is provided (Article 15.11 of the Code of Administrative Offenses of the Russian Federation). Since the distortion of reporting occurred as a result of one act - failure to comply with the requirements of PBU 18/02, there will be one fine (clause 5 of Article 4.1 of the Code of Administrative Offenses of the Russian Federation).