What is a collection order?

A collection order is a document that is provided directly to the debtor’s bank if there is an undisputed basis for collecting funds. Collection can be issued as a counterparty

in accordance with the clauses of the agreement, and by

the tax authorities

according to the law.

A mandatory condition is to notify the counterparty - the debtor - of the existence of an overdue debt before issuing collection. Such notice must specify the time limit for fulfilling the obligation to pay the amount without compulsion. If the debtor does not make payment independently within the specified time, then a collection order may be issued to his bank with the obligatory indication of a clause of the agreement or an article of a certain law

.

supporting documents from him

indisputable recovery (agreement or annex to it).

Tax authorities issue a collection order based on certain articles of the Tax Code, depending on what tax or fee has not been paid. In addition, the collection order issues the unpaid amount of fines and penalties.

Banks, in accordance with paragraph 1 of Article 60 of the Tax Code of Russia, are obliged to fulfill these instructions in the first place

. Also, the procedure for executing collection orders is prescribed in the Regulations of the Central Bank dated 07/06/2017 No. 595-P “On the payment system of the Bank of Russia”. That is, a block is placed on the amount indicated in the collection. If there are not enough funds on the current account to write off, the account is blocked until the bank is able to write off this amount in full.

Tax authorities have the right to demand additional clarification from the bank:

- about the write-off amount;

- why the collection order was not written off;

- balance of funds in the current account of the taxpayer-debtor and others.

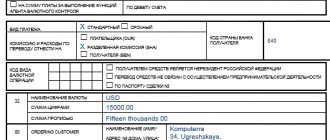

Before issuing collection to the bank, tax authorities are required to notify the taxpayer of the obligation

on payment of tax. To do this, through electronic communication channels (if available) or through Russian Post, the Federal Tax Service sends a request for tax payment. It looks something like this:

Only after the formation of such a requirement and after the period specified in it has passed, the tax authority has the right to issue a collection to the bank and a decision to suspend transactions on the accounts

.

Is the Federal Tax Service's refusal to revoke a collection order legal?

Quote (Regulations on the rules for the transfer of funds (approved by the Central Bank of the Russian Federation on June 19, 2012 N 383-P)): Chapter 2. Procedures for accepting for execution, recall, return (cancellation) of orders and the procedure for their execution The withdrawal of an order is carried out before the transfer is irrevocable Money. Revocation of an order submitted for the purpose of transferring funds to a bank account is carried out on the basis of a revocation application in electronic form or on paper submitted by the sender of the order to the bank. Drawing up an application for revocation and the procedure for accepting it for execution are carried out by the bank in a manner similar to the procedure provided for the application for acceptance (refusal of acceptance) of the payer in subclause 2.9.2 of clause 2.9 of these Regulations. The bank, no later than the business day following the day of receipt of the application for revocation, sends to the sender of the order a notification in electronic form or on paper about the revocation, indicating the date, possibility (impossibility due to the irrevocability of the funds transfer) of revocation of the order and marking the order on on paper with the stamp of the bank and the signature of the authorized person of the bank. The application for revocation serves as the basis for the bank to return (cancel) the order. Revocation of the order of the recipient of funds presented to the payer's bank through the bank of the recipient of funds is carried out through the bank of the recipient of funds. The recipient's bank revokes the recipient's order by sending to the payer's bank an application for revocation, drawn up on the basis of an application for revocation of the recipient of funds in electronic form or an application from the recipient of funds on paper, indicating the date of receipt of the application of the recipient of funds, the stamp of the recipient's bank and signature authorized person of the recipient's bank. Revocation of an order transmitted using an electronic means of payment is carried out by the client by canceling the operation using an electronic means of payment.

Collection on an additional account: what can be done and how to avoid a repeat situation

So, the Federal Tax Service issued a demand for tax payment, but the organization did not pay it on time. Next, the tax authorities review information on open accounts

legal entity or individual entrepreneur in all banks in Russia.

Information on opening and closing current accounts is provided to the Federal Tax Service

and is updated in a timely manner by financial institutions without the participation of the client himself.

If a company has only one account, there are no problems. The tax authorities send a decision to suspend transactions on the current account to the taxpayer-debtor, and a collection order to the bank. The solution looks like this:

The collection order is not sent to the legal entity (debtor) itself either by the Tax Service or by the bank

. That is, the taxpayer will not be notified about which account the money will be written off from.

The presence or absence of blocking on the account can be checked

on the website of the Federal Tax Service of Russia at this link. To check, you need to select the “Request for current decisions on suspension” type from the list provided, indicate the TIN of the legal entity and the BIC of the bank (any bank in which the company’s account is opened). The form looks like this:

A controversial situation arises if an enterprise or individual entrepreneur has several open current accounts. In this case, decisions to suspend operations

according to the current account are issued to all accounts, and collection - only to one bank.

And if the collection order was generated for an additional account in which there is no money or there is not enough money for payment on demand, then a controversial situation arises: what to do in this case?

It is worth noting that collection cannot be withdrawn by the tax authorities

, if payment has not been made.

There are only 3 possible solutions:

- contacting the Federal Tax Service to generate a new collection order;

- replenishment of an additional current account for the collection amount;

- payment of the amount of the enterprise's debt by the business owner or other legal entity.

In the future, to avoid such situations, it is better for the company to write an official letter in free form

, in which to indicate which current account of the legal entity is the main one and to which all possible collection orders must be issued. This document can be issued on the official letterhead of the enterprise, if available. The letter must be registered both with the company and with the tax authority, so it is issued in 2 options (one option remains with the Federal Tax Service, the second with a mark of acceptance - with the legal entity). The document is signed by the manager or an authorized person and stamped (if any).

Article875. Execution of collection order

But it is not confirmed in the legislation. Thus, according to clause 8.12 of the Regulation of the Central Bank of the Russian Federation N2-P, the executing bank must execute the order of the recipient of the funds no later than the business day following the day of receipt of the relevant document from the recipient (collector) of the funds, unless a different period is provided for in the bank account agreement. In accordance with paragraph 5 of Article 70 of the Law on Enforcement Proceedings, the bank fulfills the requirement of the writ of execution to collect funds from the debtor’s account within three days from the date of receipt of the writ of execution from the recoverer or bailiff. If the payment deadline is different, the executing bank must submit the documents immediately upon receipt of the collection order for acceptance, and before the expiration of the period specified in the collection order for payment. 6. Execution of collection orders means writing off funds from payers’ accounts in an indisputable manner. Banks do not consider the merits of payers' objections to debiting funds from their accounts. If there are funds in the payer’s account, they are written off on the basis of received collection orders (in some cases with attached executive documents) in an indisputable manner. In accordance with clause 12.10 of the Regulations of the Central Bank of the Russian Federation N2-P, banks suspend write-offs indisputably in the following cases: by decision of the body exercising control functions; if there is a judicial act on suspension of collection; on other grounds provided by law. When the write-off is resumed, the priority group and calendar order of receipt of documents are preserved. If there are no or insufficient funds to satisfy the claimant's demands in the payer's account (if the bank account agreement does not provide for crediting the payer's account), collection orders are placed in a file cabinet in off-balance sheet account N90902 "Settlement documents not paid on time" indicating the date of placement in the file cabinet. Payment for documents in the card index is carried out as funds are received into the payer’s account in the order prescribed by law. 7. The collection order is executed in full. Partial payment of a collection order is allowed in cases provided for by banking rules, or if there is special permission for this in the collection order. In accordance with clause 8.10 of the Regulations of the Central Bank of the Russian Federation N2-P, partial payment of collection orders located in file cabinet N90902 “Settlement documents not paid on time” is allowed in a manner similar to the procedure for partial payment of payment orders. 8. The amount of money debited from the payer’s account must be immediately transferred by the executing bank to the disposal of the issuing bank. Such a transfer is carried out by crediting funds to the correspondent account of the issuing bank if there is a correspondent relationship between them, or funds are credited to the correspondent account of the issuing bank with the Central Bank of the Russian Federation. The timing of banking operations must correspond to the deadlines provided for by law (Article 849 of the Civil Code). The general terms of all operations necessary for collection settlements are determined taking into account the specifics of collection operations. Thus, when determining the period within which the issuing bank is obliged to ensure the crediting of funds to the recipient’s account, the terms of transactions on accounts are taken into account (Article 849 of the Civil Code), the terms of travel of documents sent to the executing bank, as well as the deadlines established banking rules for the acceptance of these documents by the payer. Non-working days are not counted towards the deadline (clause 16 of Letter N39 of YOU). Therefore, such a period may exceed the general period for non-cash payments established by Article 80 of the Law on the Central Bank of the Russian Federation. The writ of execution, on the basis of which the penalty has been collected, is returned to the court or other authority that issued the document. The executing bank has the right to withhold from the collected amount the remuneration and reimbursement of expenses due to it, since collection is a banking service and is carried out at the expense of the client. Since the presentation of documents for payment does not always end with the transfer of funds, and the executing bank, before receiving a refusal, performs certain actions and incurs expenses, banks often enter into an agreement to pay for the services of the executing bank at the expense of the issuing bank. The latter, in turn, can recover its expenses from the payer on the basis of clause 1 of Article 874 of the Civil Code. 9. Execution of payment requests is carried out by analogy with the law according to the rules established for the execution of collection orders, if they do not contradict the specifics of settlements for payment requests. The rules on the execution of collection orders are applied by analogy when presenting collected checks for payment (Part 2, Clause 1, Article 882 of the Civil Code). Commentary on relations regarding payment of collected bills of exchange. the rules cannot be applied, since the bill of exchange is not a payment document and to transfer funds from one account to another, presenting the bill of exchange to the payer’s bank is not enough. Funds can be debited from the payer's account only on the basis of a settlement document (for example, a payer who is ready to pay a bill of exchange presented to his bank may issue a payment order to the bank, or payment of the bill may be provided for by the terms of the letter of credit).

Contacting the Federal Tax Service to generate a new collection order

As previously stated, the company will not know to which account the collection order was issued

until he notices that the account is blocked and funds (if any) are not debited.

If such a situation arises in practice, then the responsible person needs to call the local Federal Tax Service inspectorate (the telephone number is indicated in the decision to suspend account transactions or in the request for tax payment). Using the TIN of the legal entity, a tax specialist will announce to which bank the collection was sent

.

The tax authority may refuse to reissue a collection order, since tax legislation does not require it to do so.

Sometimes (in isolated cases)

) The Federal Tax Service agrees to issue a second collection to another bank or draw up a letter redirecting a previously issued order from one bank to another. For example:

- provided that this situation occurred for the first time;

- the tax authority has a letter containing the details of the main current account;

- the amount of the collection order is large and others.

It is worth noting that tax officials are “reluctant” to reissue instructions. Most often, they ask to pay the claim in person or to top up the current account to which the collection was issued. But still practice shows that this is possible

.

What is a collection order used for?

A collection order is issued in the following cases.

If funds must be written off to pay off debts to executive bodies in a legal and indisputable manner.

Example

The company did not pay taxes on time and did not pay off debts voluntarily at the request of the tax authorities. Then the inspectorate sends a collection to the bank and forcibly writes off the money to pay off the tax debt.

If the bank has the right to write off funds without acceptance based on agreements with the payer. Most often, this happens if the parties to the contract agree and transfer to the bank the conditions for direct debit on the part of the payer, subject to the fulfillment of certain conditions of the contract.

Example

An example is payment of utility bills.

These tips will help you work without penalties:

Replenishment of an additional current account for the collection amount

If the tax authority refuses to meet the debtor halfway (and formally the Federal Tax Service has the rights

!), then there is nothing left to do but replenish an additional current account. It can be done:

- by depositing cash into the account;

- by means of non-cash transfer from the main account (if available);

- issuing invoices to counterparties with other details.

But each of the above methods has its disadvantages. Deposit cash

only possible if they actually exist. If the company is in a difficult financial situation, then it is also necessary to find or collect this amount. To do this, proceeds can be withdrawn from the company’s cash desk (if any), or a loan or loan can be issued from the business owner or manager. If the amount of unpaid taxes is large, then it may take a long time to collect the amount to pay the tax. Applying for a loan to a legal entity is a long process. In addition, the company must have large turnover in the account for the previous year.

The second option is to transfer money from the main account

. Most often, if a company failed to pay a tax or fee on time, it means that it does not currently have this amount. Otherwise the tax would have been paid.

It is worth noting that when a decision is made to suspend operations on an account, the collection amount is blocked on all of the company’s accounts and debited from only one. That is, the organization has the right to manage money the amount of which exceeds the blocking.

Example: The Federal Tax Service has blocked transactions on current accounts. The collection amount is 50 thousand rubles. One of the company’s accounts contains 65 thousand rubles. What amount is the LLC entitled to use?

The enterprise has the right to dispose of only 15 thousand rubles, since 50 thousand will be blocked until the collection amount is debited from the current account to which the collection order was issued.

The last option is issuing invoices to counterparties with other details

for payment. The main disadvantages here are time and additional documents. The organization needs to notify the buyer that their details for payment for goods, works or services have changed in a separate letter, which is sent either immediately when the details are changed, or together with a posted invoice for payment.

If in the future the company wants to issue invoices to counterparties using the old details, then you will have to draw up a repeat letter

.

What is included in a collection order

Depending on the specific situation, the collection order must include:

- The number of the law on the basis of which the collection order was issued, as well as the corresponding number of the article of the law.

- Number and date of the writ of execution, name of the organization, case number in legal proceedings.

Important: if the collection was issued on the basis of a writ of execution, the original or a duplicate of the writ of execution must be attached to it.

- Agreement indicating the details and conditions on the basis of which the collection order was inserted

Payment of the company's debt by third parties

There is another possible course of action - payment of tax by another person. Moreover, it does not matter from whom the payment comes (from an individual or a legal entity). The main thing is that the purpose of the payment must indicate: “payment of tax... for (period) for Romashka LLC TIN/KPP...”.

Despite the fact that the payer will be another person, the Federal Tax Service will determine the payment based on the information specified in the “Purpose of payment” field.

If the taxpayer-debtor decides to take this option, then immediately after the payment has been made, contact the tax service and notify that the payment of the tax or fee was made by another person (name of the enterprise or last name, first name and patronymic, who made the payment, TIN and checkpoint if available). You can also send a payment order to the Federal Tax Service to confirm payment.

Russian legislation has made it possible to pay taxes and fees for third parties from the end of 2021

, when Part 1 of Article 45 of the Tax Code of Russia was changed. Payment can be made through the special service “Payment of taxes for third parties” on the Federal Tax Service website.

If the tax payment was made by third parties, you should pay attention to documentary evidence of this transaction. If this is gratuitous assistance from the owner, then an appropriate agreement must be drawn up. If the parent organization or an interdependent person paid, then the payment of tax must be reflected in the reporting in accordance with the rules of PBU. Otherwise, a number of questions may arise

from the Federal Tax Service specialists.

Features of this instruction for the tax authority

The tax office has the right to forcibly collect unpaid taxes in accordance with Article 46 of the Tax Code of the Russian Federation if the payer does not voluntarily fulfill his obligations within 2 months from the date of the demand.

Important: in this case, the authority issues a demand for payment of all arrears and blocks accounts until the debt is paid in full.

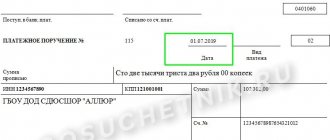

Collection order form with details.

Further events develop in the following direction:

- The bank writes off debts during the next business day after receiving collection if there is a debt;

- The company makes the payment itself and notifies the tax office before the accounts are blocked;

- If there is not enough money or there is no money, the claim is transferred to the bailiffs, who will seize and sell the debtor's property to pay off the debt.

Important: since 2021, all collection through the court has become much simpler; now only a single court decision is required without inviting the parties within 10 days.

Document processing

When processing a collection order, the bank is guided by Central Bank Regulation No. 383 P.

Important: execution of a collection order is mandatory from the moment it is received.

Revocation procedure

The territorial tax authority has the right to revoke a collection order previously issued by another similar authority, for example, by a successor after the reorganization of the authority.

A recall can occur for many reasons:

- Independent payment of debt by the debtor;

- The court's decision;

- Changing or canceling a previously made decision.

Important: this review can be in full or partial; for settlement checks, a partial version is not possible.

This action takes place on the basis of clause 2.17 of Appendix No2-P in accordance with the application submitted to the bank in 2 copies, containing in full all the necessary information and details for the revocation.

Both documents are certified by authorized persons, certified by a seal and transferred to the payer’s bank.