All employees have the right to take statutory leave every year after working for 11 months. Such leave must be paid.

Management is obliged to carry out calculations and accrue vacation pay to employees. Such compensation is financial security for the employee during his absence from work. Vacation pay is calculated taking into account the following criteria:

- duration of vacation;

- estimated time;

- the average daily salary of an employee.

Is income tax calculated on vacation pay?

The most important thing is the employee’s income that he received during the pay period. When calculating, in addition to salary, allowances and bonuses are taken into account.

Vacation pay is accrued 3 days before the start of the vacation. Failure to comply with this procedure may be a good reason for a visit to the labor inspectorate with a complaint against the boss. Before vacation pay is accrued, personal income tax is deducted from them, as specified in the Tax Code of Russia.

What do you need to know?

Sometimes employers and employees themselves are not aware of whether personal income tax is paid on vacation pay. Such a payment is not considered a salary or bonus, but tax is still withheld from it.

Vacation pay is the employee's income and is therefore taxed. The same rule applies to payments for unused vacation days. The withholding of tax from such payments is approved by the Tax Code of Russia. The listed personal income tax must be included in accounting and tax reporting.

Personal income tax is always withheld from vacation pay

Important ! Vacation pay can be provided to the employee in cash or by transfer to a card or bank account.

When transferring funds, tax is withheld from them. Management assumes the role of tax agent and undertakes to follow all rules for the allocation of funds to the state budget.

Funds are transferred to the treasury at the time vacation pay is accrued or a transfer is made to the employee’s card. There is no need to carry out this procedure in advance.

The tax is transferred at the time the vacation pay is received. This is stated in Article 226 of the Tax Code of the Russian Federation.

Excerpt from Article 226 of the Tax Code of the Russian Federation

Personal income tax from additional payment to salary for vacation and sick leave

Some employers, when paying sick leave benefits or vacation pay, practice additional payment to their employees in the amount “before salary”. After all, payments in these cases are made based on the employee’s average earnings, so they are often less than the usual salary.

Any additional payment is income, so this amount is subject to personal income tax on a general basis. But by its structure, the additional payment is neither vacation pay nor sick leave.

The date of actual receipt of income, including in the form of additional payment to salary for benefits and vacation pay, is recognized as the day of actual payment of income to the taxpayer (letter of the Federal Tax Service of Russia dated August 1, 2016 No. BS-4-11 / [email protected] ).

At the same time, in accordance with the provisions of Article 226 of the Tax Code of the Russian Federation and clarifications of tax authorities, the timing of the transfer of personal income tax withheld from such an additional payment will differ from the timing of the transfer of tax on vacation pay or temporary disability benefits:

- Personal income tax from vacation pay and sick leave benefits is transferred to the budget on the last day of the month in which the employee received the money;

- Personal income tax from additional payment to salary is transferred on the day following the day of actual payment of the amount to the employee.

That is, if an employer pays employees extra, he will have to transfer personal income tax twice to avoid a fine.

Income tax

Income tax is a type of direct tax. It is collected from all individuals who have income. The Tax Code reflects some types of profit from which tax is not withheld. For example, they are not subject to benefits issued from the state budget.

The tax rate is 13%. In some cases it is equal to 9, 15, 30 and 35%. The rate depends on the type and status of profit that is due to working persons.

The tax base is based on income in full. It is worth considering that individuals have the right to count on a tax deduction.

Income tax is 13%

Income tax for employees with their salary is calculated by management, who is the tax agent and who is responsible for the correct execution of all transactions.

Personal Income Tax is an abbreviation for “personal income tax.” The tax is removed from all employed persons. It is collected from citizens of the Russian Federation, foreigners working in Russia and stateless people. This is the same as income tax

Important ! As a rule, taxpayers are not concerned about the deadlines for paying taxes. But if they have income that was not received for working in an organization, for example, for the sale of an apartment or car, then they need to transfer the information by filling out a declaration.

The reporting period for tax payments is 365 days

The tax reporting period is 365 calendar days. The declaration can be completed on paper or electronically. The deadline for its submission is April 30 of the following reporting year.

Features of personal income tax calculation

The object of taxation is the amount of vacation pay. This amount of money cannot be considered as part of the salary. In this regard, the tax on vacation pay is determined independently of the tax on wages.

Deadline for payment of personal income tax on vacation pay in 2021

The employer is obliged to withhold tax immediately upon actual payment of vacation pay to his employee

05/15/2018Russian tax portal

Author: Tatyana Sufiyanova (tax and duties consultant)

When to pay personal income tax in case of vacation pay? This question worries many accountants, and we decided to write an article devoted specifically to this issue. I would like to immediately draw your attention to the fact that you should not confuse such types of income as “vacation pay” and “salary”.

The fact is that the deadline for paying personal income tax to the budget depends on what type of income your company paid to its employee. If we are talking about wages, then the deadline for paying personal income tax will be “no later than the day following the day the income was paid,” and if the employee received vacation pay, the deadline for paying personal income tax will be “no later than the last day of the month in which payments were made.”

Let's give a simple example - I paid employee Ivanov I.A. salary for April 2021 May 10, 2021. And on May 14, 2021, vacation pay was paid to the same employee. How to properly pay personal income tax to the budget so that penalties are not charged later?

First, let's deal with the payment of wages - the date of receipt of income is May 10, which means that the withheld personal income tax should have been transferred to the employer either on the 10th or on May 11, 2021. If the accountant makes a payment order for the payment of personal income tax to the budget later, then there will be a “lateness” and penalties will be charged.

The second case is the payment of vacation pay . The payment was made on May 14, 2021, the tax was withheld from the amount of vacation pay immediately, but it should have been transferred to the budget either immediately on May 14, or throughout the month, but no later than May 31, 2021.

The question may arise - how does the tax inspector know about the type of income in order to charge penalties? It’s very simple - when an accountant creates a 6-NDFL report, all types of payments and their dates will be reflected, the deadlines for tax payment are indicated, and the inspectorate will be able to compare them with the dates of actual receipt of personal income tax into the budget.

As the Ministry of Finance writes in its letter dated March 28, 2018 No. 03-04-06/19804, on the basis of clause 4 of Art. 226 of the Tax Code of the Russian Federation, tax agents are required to withhold the calculated amount of tax directly from the taxpayer’s income upon their actual payment.

According to the second paragraph of clause 6 of Art. 226 of the Tax Code of the Russian Federation, when paying a taxpayer income in the form of temporary disability benefits (including benefits for caring for a sick child) and in the form of vacation pay, tax agents are required to transfer the amounts of calculated and withheld tax no later than the last day of the month in which such payments were made.

Consequently, the tax agent is obliged to calculate and withhold personal income tax on vacation amounts when they are actually paid, and transfer them to the budget no later than the last day of the month in which such payments were made.

Examples of calculating vacation payments

Post:

Comments

Object of taxation

The income that an individual has is subject to taxation. Vacation pay is issued to the employee before his vacation begins. They are the ones who are subject to personal income tax.

The formula for calculating vacation pay is as follows: duration of vacation (in days) * average daily earnings of the employee.

After which the resulting figure is * 13%.

The final number will reflect the amount of tax.

Vacation pay must be issued by the employer before the employee goes on vacation.

In this case, no action is required from the employee. All work falls on the management. He is responsible for the correctness of calculations and timely transfer of money to the treasury.

Deadline

In general, the tax agent is required to transfer personal income tax to the treasury up to and including the next day after payment of income. Meanwhile, a separate rule applies for the amounts of sick leave and vacation pay (clause 6 of Article 226 of the Tax Code of the Russian Federation): this must be done no later than the last day of the month in which such payments took place.

Sometimes it happens that the last day of the month is an official day off: Saturday, Sunday or a holiday according to the production calendar. For example, in 2021 this happened 4 times: in January, April, July and December. How then to fill out form 6-NDFL if the last day of the month is a day off ?

Also see “What dates are indicated in 6-NDFL”.

The legislative framework

The main regulatory act that controls the procedure for calculating vacation pay is the Labor Code of Russia. All issues regarding taxation are clarified in the Tax Code of the Russian Federation.

These main legal acts make it possible to count on receiving payments due to the employee and taxing them.

The Labor and Tax Codes provide information regarding vacation pay and tax withholding

Calculate personal income tax at the time of payment

Vacation pay must be paid to the employee three days before he goes on vacation. This is required by Article 136 of the Labor Code of the Russian Federation.

During a rolling vacation, the accountant is faced with a situation where the employee is paid income related to the future month. That is, for example, vacation pay is issued in August, and the vacation itself will take place in September. In this case, personal income tax must be withheld upon actual payment of vacation pay (subclause 1, clause 1, article 223, clause 4, article 226 of the Tax Code of the Russian Federation). That is, at the time of payment of vacation pay, the accountant should calculate personal income tax on the entire amount of vacation pay. This is confirmed by letter of the Ministry of Finance of Russia dated 06/06/2012 No. 03-04-08/8-139.

Levying tax on holiday pay

Vacation pay is subject to the only tax – personal income tax. For 2021, management's responsibility to pay and retain required funds has not changed. Minor adjustments affected the timing of tax transfers to the treasury. As already mentioned, personal income tax is transferred on the day the employee is paid.

Today the rules have changed. Management must transfer personal income tax before the end of the month in which the employee received vacation pay.

Personal income tax must be transferred by the employer before the end of the month

Important ! Such innovations are more beneficial for the employer. Now it is not necessary to accrue vacation pay to an employee and transfer tax to the budget on the same day, as well as enter transactions for the movement of funds in the appropriate documents.

Is personal income tax withheld from vacation pay on the last day of the month?

Finally, the issue of the deadline for paying personal income tax on vacation pay was closed by the current wording of clause 6 of Art. 226 Tax Code of the Russian Federation. Now it directly states that tax on vacation pay (and also personal income tax on sick leave) should be transferred until the end of the month in which they were paid.

Note! We are talking specifically about paying personal income tax, and not about withholding it from the amounts paid. Tax is withheld when paying money to an employee. But the payment can not be made immediately, but postponed until the last day of the month.

Let's look at an example.

The employee will go on leave from April 10, 2021. Lowering fees in the amount of 15,000 rubles. he was paid on April 6, 2021. On the same day, personal income tax was withheld from vacation pay in the amount of 1,950 rubles. (15,000 × 13%). The deadline for transferring tax to the budget is from April 6 to April 30, 2021. If you transfer personal income tax later than the 30th, the taxpayer will face a fine of 20% of the untimely transferred amount.

Vacation pay is indicated separately in section 2 of form 6-NDFL, because the terms rarely coincide with other payments. The amount of vacation pay in this case will be reflected in the report as follows:

Page 100 - date of actual receipt of vacation pay - 04/06/2020

Page 110 - tax withholding date - 04/06/2020

Page 120 - deadline for paying tax to the budget (regardless of the actual date of transfer) - 04/30/2020

Page 130 - amount of income - 15,000 rubles.

Page 140 - amount of personal income tax withheld - 1,950 rubles.

See also our example of filling out 6-NDFL for the 1st quarter of 2020 with vacation pay.

ConsultantPlus experts explained in detail how to reflect vacation pay on the 2-NDFL certificate. Get trial access to the system and use recommendations for free.

And more details about the deadline for transferring tax in the calculation of 6-NDFL are described in this article.

When to make tax payments?

Vacation pay is paid to the employee 3 days before the start of the vacation. At the same time, personal income tax is withheld under Art. 226 of the Tax Code of Russia. The time for transferring tax to the state budget depends on the choice of method of payment of vacation pay.

- Cash - on the day the money is credited or the next day. For example, if the money was transferred on Friday, then the tax is paid on that day or on Monday.

- When withdrawing money from a company account - on the same day. The tax must be transferred strictly on the day when vacation money is withdrawn from the company’s account, regardless of when the employee receives the funds.

- Crediting to a bank card or withdrawal from the organization’s account – on the day of crediting.

You cannot transfer personal income tax before the employee has been given vacation pay.

On a note! Most accountants transfer the tax before the holiday pay has been issued. Such actions are wrong.

What to do if the last day of the month falls on a weekend

In this case, the rule is that the deadline is the first working day of the next month.

For example, the last day of June - the 30th - falls on Saturday in 2021. Therefore, if you pay vacation pay to an employee on Friday, June 29, there is no need to rush to pay personal income tax on the same day. This can also be done on Monday, July 2, which becomes the deadline for paying personal income tax for June.

For 2021, the personal income tax payment schedule for vacation pay looks like this:

- January – until January 31 inclusive.

- February – until February 28 inclusive.

- March - until April 2 inclusive.

- April - until May 3 inclusive.

- May - until May 31 inclusive.

- June - until July 2 inclusive.

- July - until July 31 inclusive.

- August - until August 31 inclusive.

- September – until October 1 inclusive.

- October – until October 31 inclusive.

- November – until November 30 inclusive.

- December – until January 9, 2021 inclusive.

Payment of tax on compensation for unused vacation days

An employee has the right to go on vacation after working in the organization for at least six months. In the event of dismissal, if he did not take advantage of his vacation, he must be paid compensation.

Compensation is due on the day of care. Tax is also paid along with this. Money is transferred to the treasury on the last day of the month. The compensation paid must be recorded in the appropriate document.

You can go on vacation after at least six months of work

When to pay personal income tax for vacation pay in 2021 if the vacation is transferable

In cases where vacation begins in one calendar month and ends in the next, nothing changes. According to the labor code, vacation pay must be paid before the employee goes on vacation. Vacation pay is paid in full on a specific date. This date will determine the deadline for paying personal income tax for vacation pay. This is the last day of the same calendar month or the first working day of the next according to the schedule given above.

Payment procedure

Income tax is charged only on the amount due to the employee. This matters when the employee has partially used vacation days. If two or more employees in an organization take vacation at once, the tax is transferred as a total amount.

As already mentioned, management now has the right to transfer money to the budget until the end of the month in which the employee has a vacation. The period for paying vacation pay this year according to the Labor Code of the Russian Federation is 3 days.

Personal income tax is withheld only from the amount that is currently due to the employee

Deadlines for payment and calculation of personal income tax on vacation money

For income that is subject to personal income tax, specific dates are established for the calculation of income tax, its withholding and further transfer to the Federal Tax Service of the Russian Federation. Such a tax payment is calculated and then transferred to the inspectorate no later than the last day of the month in which these payments were made.

Read also: Material costs

When transferring a certain amount of income tax for individuals, they take into account the fact in which month the day of payment of vacation money falls. This is also done when “rolling” annual leaves arise, which are opened in one specific month and closed in another.

On a note! Vacation pay for January 2021, which was transferred to the salary card in December 2021, was indicated in section 1 of the 6-NDFL calculation form for 2021. So, if vacation pay was paid to the employee on December 30, then in the calculation of 6-NDFL for the year this operation had to be indicated only in section 1. And in section 2 this payment is reflected when filling out the calculation for the first quarter of the current year. A similar procedure is in the letter of the Federal Tax Service dated 04/05/17 No. BS-4-11/ [email protected]

Order of the Federal Tax Service of Russia dated October 14, 2015 N ММВ [email protected] “On approval of the form for calculating the amounts of personal income tax calculated and withheld by the tax agent (Form 6-NDFL), the procedure for its completion and submission, as well as the format for presenting the calculation of tax amounts on the income of individuals calculated and withheld by a tax agent in electronic form"

Definition of payment

In tax and accounting reporting, tax must be displayed taking into account the following rules:

- the tax is entered as labor costs;

- if there is an insurance premium, they are classified as other expenses for core activities;

- expenses relate to the month in which they were incurred.

The tax is defined in the financial statements as labor costs

Income tax on maternity leave

Paragraph 1 of Article 217 of the Tax Code of the Russian Federation fully discloses the topic regarding the taxation of maternity leave. According to this article, the tax does not affect payments under the BiR. Payments under the BiR differ from standard sick leave, from which tax is supposed to be collected.

Girls who are not employed cannot take maternity leave. The only exceptions are those women who were forced to quit due to the closure of the enterprise. Like women who are on regular maternity leave, they are accrued all benefits without reduction by the amount of personal income tax.

Excerpt from Article 217 of the Tax Code of the Russian Federation

Also, women in this position are entitled to additional payments.

- One-time benefit. It is available to those who register with the antenatal clinic before 3 months of pregnancy. Its standard size is determined by law and is equal to 330 rubles. Indexation carried out on February 1, 2021 increased the benefit amount to 650 rubles.

- One-time payments for the birth of a baby. Their standard size is determined at the legislative level and is equal to 8 thousand rubles. Indexation also made it possible to increase the amount of payments by more than 2 times, and now they are equal to 17,500 rubles.

Important ! The amount of these benefits is also tax-free.

Various payments for a child are not subject to personal income tax

There are no changes regarding the calculation and taxation of maternity taxes this year. This means that no tax is charged on such payments. But the standard changes affected the amount, which depends on the minimum wage and the employee’s salary, which in turn is subject to income tax.

Taking into account these amounts from the beginning of 2021 for the amount of maternity benefits:

- the minimum amount as a result of the next increase in the minimum wage is 52 thousand rubles in the case of a normal birth;

- the minimum amount for childbirth with complications is 58 thousand rubles;

- the minimum amount for the birth of 2 or more children is 72 thousand rubles;

- the maximum size for normal childbirth is 301 thousand rubles;

- the maximum amount for childbirth with complications is 335 thousand rubles;

- the maximum amount for the birth of 2 or more children is 417 thousand rubles.

The amount of maternity leave depends on the employee’s salary

The Federal Tax Service explained how to fill out 6-NDFL if the deadline for transferring personal income tax falls on a weekend

Let us remind you that in section 2 of the 6-NDFL calculation for the corresponding reporting period, only those transactions that were made during the last three months of this period are reflected.

Line 100 “Date of actual receipt of income” is filled out taking into account the provisions of Article 223 of the Tax Code of the Russian Federation.

Line 110 “Date of tax withholding” - taking into account the provisions of paragraph 4 of Article 226 and paragraph 7 of Article 226.1 of the Tax Code of the Russian Federation.

Line 120 “Tax payment deadline” - taking into account the provisions of paragraph 6 of Article 226 and paragraph 9 of Article 226.1 of the Tax Code of the Russian Federation.

Line 030 “Amount of tax deductions” - according to the code values of the taxpayer’s types of deductions, approved by order of the Federal Tax Service of Russia dated September 10, 2015 No. ММВ-7-11/ [email protected]

The date of actual receipt of income in the form of wages is recognized as the last day of the month for which the taxpayer was accrued income for the performance of labor duties (clause 2 of Article 223 of the Tax Code of the Russian Federation). Tax agents are required to withhold the accrued amount of tax directly from the taxpayer’s income upon actual payment (Clause 4 of Article 226 of the Tax Code of the Russian Federation). In this case, the employer is obliged to transfer the tax no later than the day following the day the employee is paid income. When paying an employee benefits for temporary disability (including benefits for caring for a sick child) and vacation pay, personal income tax is transferred no later than the last day of the month in which such payments were made (clause 6 of Article 226 of the Tax Code of the Russian Federation).

An accountant who contacted the Ministry of Finance had a question: how to fill out line 120 of the 6-NDFL calculation “Tax transfer deadline” if the established deadline for personal income tax transfer falls on a weekend or holiday?

Federal Tax Service specialists responded that in such a situation one should be guided by paragraph 7 of Article 6.1 of the Tax Code of the Russian Federation. This rule states: in cases where the last day of the period falls on a day recognized in accordance with the legislation of the Russian Federation as a weekend and (or) a non-working holiday, the end of the period is considered to be the next working day following it. Accordingly, if the day the tax is transferred falls on a weekend, then in line 120 of the 6-NDFL calculation you need to indicate the nearest working day.

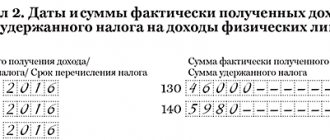

For clarity, the authors of the letter gave the following example. Vacation pay for January 2021 was paid on January 14, 2021. The personal income tax payment deadline (January 31) fell on Sunday. This means that in section 2 of the 6-NDFL calculation, this operation had to be reflected as follows:

- on line 100 “Date of actual receipt of income” - 01/14/2016;

- on line 110 “Date of tax withholding” - 01/14/2016;

- on line 120 “Tax payment deadline” - 02/01/2016 (taking into account paragraph 7 of Article 6.1 of the Tax Code of the Russian Federation);

- on lines 130 “Amount of income actually received” and 140 “Amount of tax withheld” - the corresponding total indicators.

Who pays maternity benefits and is it possible to collect income tax for individual entrepreneurs?

Responsibility for maternity payments lies entirely with the Social Insurance Fund of Russia, which allocates funds from insurance premiums for social insurance for incapacity and maternity. All employers are required to pay these contributions, regardless of whether they are individual entrepreneurs or legal entities. For the last two years, contributions are made not specifically to the fund, but to the Federal Tax Service. But the Social Insurance Fund is still responsible for the procedure for paying maternity benefits and makes decisions on reimbursement to their superiors.

Important ! In this case, the female employer may lose maternity benefits. She can count on them only if she has signed an agreement with the Social Insurance Fund on voluntary insurance and made a contribution 12 months before going on maternity leave.

The Social Insurance Fund is responsible for the procedure for paying maternity benefits.

For example, having entered into a contractual relationship with the Fund in 2021, a woman needs to pay contributions for all 12 months by December 31, 2018. Then the right to social insurance will be valid from January 1, 2020. If a girl works several jobs at once, she is entitled to maternity leave from all jobs. The boss at a non-main job must pay the B&R allowance in the same way as at the main job.

Income tax calculation

From the vacation pay received, you need to subtract:

- contributions to social and pension funds;

- medical deductions;

- contributions to the insurance fund in case of work injury or illness.

After all these deductions, the tax is calculated. The rate is 13%.

Contributions to the Pension Fund, compulsory medical insurance, etc. are also deducted from income.

Calculation of personal income tax from additional vacation days

The employee has the right to ask for additional vacation days at the expense of the organization. They are also subject to tax. For each vacation day, the average salary of the employee for 1 shift is calculated. For example, it is equal to 350 rubles. In this case, for 4 days of additional vacation, payments will be 1,400 rubles. To calculate the tax you need 1400*13%. Income tax = 182 rubles.

Personal income tax is also withheld from additional vacation days

Calculation example

Alexander Petrov took a vacation from September 21 to October 4, 2018. To begin with, the amount of vacation pay is determined, which depends on the amount of wages. Petrov receives 49,000 rubles. The average income per shift is 1650 rubles. In September he worked 10 shifts. His actual monthly income will be 24,500 rubles. The accountant makes the following calculations:

49,000 * 8 (number of months worked per year) + 1650 * 14 (number of vacation days) = 415,100 rubles.

1650 * 14 – 1400 (established deduction) = 21,700 rubles. The total is multiplied by 13%. Personal income tax is 2821 rubles.

The amount of income tax depends on the employee's salary

The procedure for calculating tax for unused vacation is identical.

Holiday pay accounting

When collecting personal income tax, the following transactions are used.

- Tax calculations (DT 68).

- Salary expenses (DT 70).

- KT 68 and 51 can be applied to the loan.

Examples

Employee Ivan Andreev has been taking 4 weeks leave since July 5, 2017. His income is 39,000 rubles. The money was transferred to the enterprise reserve account. There are no deductions from vacation pay. Their value is 5,000 rubles. In this case, the following wiring is used.

- DT 70 CT 68. Collection of a tax of 5 thousand rubles.

- DT 68 CT 51. Transfer of tax in the amount of 5 thousand rubles.

Employee Alexander Antonov goes on vacation. The salary is 30,000 rubles. The employee has the right to count on a tax deduction, which is 1,900 rubles. As a result, the amount of vacation pay is 3,650 rubles. The following wiring is used.

- DT 70 CT 68. Collection of income tax in the amount of 3,650 rubles.

- DT 68 CT 51. Transfer of funds to the state budget in the amount of 3,650 rubles.

Accountants must correctly report on vacation pay and personal income tax

Information entered into financial statements must be reflected in the primary documents.

Reflection of compensation for unused vacation in a certificate in 2-NDFL

When recording compensation in tax reporting, you must use a special code. There is no separate number for this type of payment. You can use the following notations.

| Designation | Definition |

| 4800 | Payment of compensation if an employee resigns. |

| 2000 | Salary payments. |

| 2012 | Payment of vacation pay. |

Help 2-NDFL

Main! According to the Tax Service, it is worth using code 2012. But the use of other codes will not constitute a serious violation.

Answers to frequently asked questions

Is personal income tax collected on vacation pay?

As stated in the legislation, all income that an individual has from an employer is subject to income tax. Vacation pay is also included in this number.

I was given vacation pay, from which personal income tax was taken away. But later I was recalled from vacation. As a result, vacation pay was deducted from subsequent salaries. Where does the tax go in such a situation?

It must be returned based on the written statement drawn up by the employee.

If the tax was deducted but the vacation was not used, it will be returned upon application to the employee

Does accounting have the right to calculate vacation pay and wages together and deduct personal income tax from the total amount?

According to the Labor Code of the Russian Federation as amended on December 20, 2001, Article 136, wages are paid no less frequently than every 15 days. A more precise date for calculating an employee’s salary is determined by the norms of the internal work code, a collective agreement or a work contract no later than 15 days from the end of the period for which it is due.

Vacation pay is accrued no later than 3 days before the start. If the dates coincide, salaries and vacation pay are issued together. Personal income tax is charged on both wages and vacation payments.

Salaries and vacation pay can be issued together; accordingly, tax is deducted from both payments

What is the amount of personal income tax??

Income tax is required to be withheld from vacation pay. This is provided for in paragraph 1 of Article 210 of the Tax Code. Tax collection occurs on the day vacation pay is calculated, i.e. the employee is paid funds from which income taxes have already been deducted.

The amount of tax depends on the employee's salary. It makes up 13% of income.

My husband is employed at PCH. When he took a vacation, personal income tax was withheld from his vacation pay. When the vacation ended and he returned to official duties, he was paid his salary without bonuses or other allowances. This is right? Since I was told that at some enterprises, after a vacation, additional accruals are paid in addition to the salary.

The employer must collect personal income tax from all salaries and transfer it to the state budget. The accrual of bonuses is reflected in the employment agreement and other local acts of the Labor Code. According to Art. 135, an employee’s salary is determined on the basis of an employment agreement, taking into account the remuneration system established by management.

Such a system exists along with the amount of tariff rates, official salary, bonuses and other accruals, including work with difficult or unhealthy conditions. All allowances, bonuses, compensation payments are agreed upon and reflected in the collective agreement, local regulations, taking into account the Labor Code of Russia and other acts that refer to labor standards.

Bonuses and other additional payments are specified in the employment contract

If management does not withhold tax on income and does not pay vacation pay at the same time, it argues that the tax rate is not deducted. Are there legal grounds for this?

The bosses have no right to refuse to pay vacation pay. All employees who have worked for at least six months have a legal entitlement to leave. This right is approved in Article 37 of the Russian Constitution, which additionally emphasizes that all officially employed citizens have such a right. According to Article 142 of the Labor Code, in Russia, management and responsible persons who are appointed by management, who delayed the payment of wages to employees or committed other violations of the employment contract, are required to bear responsibility, taking into account current legislation and regulations.

The employer has no right not to pay vacation pay

How does the income tax withholding process work? My situation is as follows: I worked for 2 weeks, part of my salary arrived, after which I went on a 2 -week vacation, of which only 10 days were paid as vacation pay. A 13% tax was withheld from the amount of vacation pay. I received my vacation pay 7 days before payday. I received vacation pay and salary in one total amount. Is this legal?

No, this is not considered legal. Personal income tax is taken into account only once and cannot be withdrawn again. In this case, it is appropriate to file a complaint with the labor inspectorate.

The individual entrepreneur did not withhold personal income tax from his salary; when it was time for vacation, they refused to give it to me, arguing that taxes had been paid for me for 12 months. Can an individual entrepreneur refuse leave?

In this case, you should contact your local prosecutor. According to Article 45 of the Civil Legal Code, the prosecutor must protect the rights of citizens in court if the rights and interests of citizens have not been respected.

A citizen can contact the prosecutor's office if his rights, enshrined in the Labor Code of the Russian Federation and the Constitution, are not fulfilled

So, since vacation pay is considered income of an individual, income tax (NDFL) is deducted from it. It is 13% of income.

Reflection of money for vacation in the calculation of 6 personal income taxes

Vacation pay is not considered salary or other monetary remuneration for work.

The date of receipt of such income is considered the day on which the worker is paid such money in fact - transferred to a card or given through a cash register (letter of the Ministry of Finance of the Russian Federation No. 2187 dated January 26, 2015, Article 223 of the Tax Code of the Russian Federation). At the same time, personal income tax is withheld from vacation money. This is done before the end of a certain month by paying a specific amount of vacation pay (Article 226 of the Tax Code of the Russian Federation).

When preparing a unified calculation of 6-NDFL in Section 1 of this document, the accrued specific amount of vacation pay is combined with other monthly income. In Section 2, money for vacation is separated from salaries (clause 4.2 of Appendix No. 2 from Order of the Federal Tax Service of the Russian Federation No. 450 of October 14, 2015). In this situation, additional lines are allocated and then filled in separately for each payment.

Vacation benefits are paid regardless of the date of payroll. This money is reflected in separate specific lines of Section 2 of form 6-NDFL. This is done for reasons:

- due to a discrepancy between the specific date of accrual of annual vacation pay and monthly salary;

- when applying a separate procedure for transferring income tax amounts from money for vacation on one of these days - the 28th, 30th or 31st of the month.

Money for annual leave is paid along with the monthly salary. This is done when specific calendar days coincide or, in particular, when paying annual leave with the subsequent dismissal of an employee.

Letter of the Ministry of Finance dated January 26, 2015 No. 03-04-06/2187 “On determining the date of receipt of income in the form of vacation pay for personal income tax purposes”

Read also: Compensation for unused vacation in 2021

Example

Money for vacation and salary was transferred to the worker’s salary card on March 31. The date of transfer of this money and the day of personal income tax deduction coincided.

In this situation, a specific amount of tax from the monthly salary is paid on working Monday or another next day, and money for vacation is issued on March 31. Then, in the unified form 6-NDFL, the payment period for a certain amount of vacation pay and wages is indicated in separate specific lines of Section 2.

How to fill out a payment order

Payment of personal income tax on vacation pay is indicated in a separate payment order. This document is filled out according to the rules from the order of the Ministry of Finance of the Russian Federation No. 107n dated November 12, 2013 and on the form according to form 0401060. In field 101 indicate code 02. In field 104 the following BCC is written - 182 1 0100 110.

Attention! The specific KBK code is found in the service from the Glavbukh System - on the website www.1gl.ru/about/.

Field 106 indicates the type of payment, and field 107 indicates the period for which personal income tax is paid. For example, when transferring to the tax office a specific amount of tax on vacation money for January 2021, the following entry is made in field 107 - MS.01.2021.

Fields 109 and 108 are filled with zeros. Field 110 is left blank.

Sample of filling out a payment order

Form 0401060

Order of the Ministry of Finance of Russia dated November 12, 2013 N 107n “On approval of the Rules for indicating information in the details of orders for the transfer of funds for payment of payments to the budget system of the Russian Federation”

How and where are carryover vacation pay reflected and their amounts after recalculation?

The 6-NDFL calculation reflects all types of annual vacation pay, including those that transfer to another specific month. This is done this way:

- First, vacation pay and the specific amount of personal income tax are calculated. This is done in accordance with certain dates for accrual and payment of this money in fact;

- The amounts received are recorded in Section 1 of the calculation;

- They reflect the payment of money for vacation in Section 2. In this place, indicate the date of transfer of this money and the deadline for paying a specific amount of personal income tax on it.

Recalculation of annual vacation pay is performed in 2 situations:

- when you provide incorrect information. In this situation, an updated (additional) 6-NDFL report is drawn up, in which reliable information on money for vacation is entered;

- upon dismissal or recall from annual leave, as well as upon untimely transfer of specific amounts of vacation pay. Changes in the amount of such payments and the tax on them are entered into specific calculation lines for the month in which the recalculation is made.

Important! According to the letter of the Federal Tax Service of Russia No. 9248 dated May 24, 2021, the amount of carryover vacation pay is indicated in form 6-NDFL upon the fact of their payment, and not according to the period in which they are accrued.

Letter of the Federal Tax Service dated May 24, 2021 No. BS-4-11/9248 “On the issue of filling out form 6-NDFL”

An example of form 6 personal income tax

Below is an example of how to correctly fill out the 6-NDFL calculation with vacation pay.

At Titan LLC, 2 workers were paid the following money for annual leave:

- August 15 - 17 thousand rubles. At the same time, personal income tax was charged in the amount of 2,210 rubles;

- August 22 - 23 thousand rubles. In this situation, income tax is 2990 rubles.

In 9 months paid 2 million rubles. salaries, applied deductions of 50 thousand rubles. Also, during this period, personal income tax was charged in the amount of 253,500 rubles, and withheld 230,500 rubles. tax

In this situation, in Section 1 of the unified form 6-NDFL, 2 workers entered vacation payments and the above salaries on line 020 (2 million rubles + 23 thousand rubles + 17 thousand rubles = 2 million 40 thousand rubles .).

Read also: Address of mass registration of legal entities

The amount of a certain accrued personal income tax was indicated on line 040 (2,990 rubles + 2,210 rubles + 253,500 rubles = 258,700 rubles), and the amount of such tax withheld was indicated on line 070 (2,990 rubles + 2,210 rubles. + 230,050 rub.) = 235,700 rub.).

In Section 2 of the report, the corresponding entries were made in the lines below:

- pp. 100, 130 - indicated the date of payment of annual vacation pay to workers (08/15/2016), and their amount (RUB 17,000);

- pp. 110, 140 - entered information about the day of withholding of accrued income tax (08/15/2016) and its amount (2210 rubles);

- page 120 - indicated the date of transfer of a certain amount of tax to the INFS (08/31/2016).

In the same way, fill out the lines for the second accrued specific personal income tax amount:

- pp. 100, 130 - indicated the date of payment of vacation money to the second employee (08/22/2016) and their amount (23,000 rubles);

- pp. 110, 140 - date of withholding (08/22/2016) and the amount of personal income tax (RUB 2990);

- page 120 - date of personal income tax payment (08/31/2016).

Attention! If the unified form 6-NDFL is correctly completed, the specific amount of vacation pay along with the monthly salary is prescribed in Section 1. In Section 2 of this document, vacation payments are separated from other various incomes.