Accounting registers are needed to control the company's financial flows. With their help, information about an enterprise is first systematized and classified, then registered, and then stored for at least 4 years from the onset of the tax period. At the same time, compiling and registering statements is not a whim of Russian entrepreneurs, but a direct responsibility when carrying out commercial activities: for the lack of accounting documentation, the company and responsible persons are fined, and in the future this can lead to more serious consequences. In this regard, understanding what accounting registers are and why they are needed is important for business managers and their accountants. Details are in this article.

What are accounting registers and why are they needed?

The activities of enterprises, especially large ones, directly depend on competent control of financial flows, as well as on monitoring the final balance of the enterprise. This is exactly what accounting does: without its work, it would be extremely difficult for enterprises of all sizes to develop.

In addition, even if the head of an enterprise would like to do without such financial self-control, according to Federal Law No. 402 of December 6, 2011, legal entities are required to send data on balance sheets, debts, etc. to the Federal Tax Service. Taken together, this means that it is simply impossible to circumvent the accounting requirement, but this is also not unnecessary bureaucratization, because self-control contributes to the growth of the enterprise.

The answer to the main question - what are accounting registers in simple words - sounds like this: it is a means of systematizing accounting data . They look like counting tables, constructed in such a way that the existing balance sheet and sources of assets and liabilities are clear.

With the help of registers, the alienation of rights to any property in the company, the movement of financial resources and other processes are taken into account. Next, all these papers are sent to the Federal Tax Service (FTS). So all data about the company, its balance sheet, open deposits and loans is registered with government agencies.

Note: accounting registers are protected by trade secrets. This is easy to understand if you consider that the accounting registers used during registration are the code for the entire official income of the enterprise, its debts, recipients of deductions, employee salaries, etc. Anyone who had acquired such data before the amendment to Russian legislation could have used it as a means to undermine competitive businesses.

Accounting registers reflect all expenses and income of the enterprise, but this can be done in different ways depending on the convenience and goals pursued by the accountant. Therefore, there is a classification of registers that allows every entrepreneur to adapt to the current business situation.

How to approve registers for work

Let's figure out how to approve the selected forms. The procedure depends on what forms of documentation you decide to use in your work.

Option No. 1. We work according to unified forms.

It is permissible for public sector institutions to state in their accounting policies that for work they will use forms and unified forms approved by Order of the Ministry of Finance No. 52n. It is not necessary to attach samples; it is only permissible to list the names of the journals used for work, indicating their OKUD codes.

Option number 2. We use our own forms.

If an organization uses independently developed samples of accounting registers, then such documents must be listed in the text of the accounting policy, in the appropriate section. Then draw up each of the documents used as an appendix to the accounting policy. It also states which accounting registers must be printed.

IMPORTANT!

Even if the registers are compiled electronically and signed with digital signatures, it is necessary to approve the samples. During the inspection, controllers will request an order or instruction on approval of accounting registers (accounting policies and appendices thereto).

Classification of accounting registers

Depending on how the accounting department wants to structure data about the enterprise, registers are divided into:

- Systematic. This type of accounting register is intended for recording in an accounting account linked to an enterprise. This allows you to track the organization’s balance (the so-called balance sheet), overall balance, etc. An example of a systematic register is the general ledger of an enterprise;

- Chronological. The difference from the systematic type is that data is filled in in accordance with the measure of their receipt. In other words, all receipts and changes in accounting data are recorded without reference to an account, but indicating the date of the event. Example - journal, cash book, etc.;

- Synchronistic. They combine the characteristics of both previous groups: records are kept with reference to both the accounting account and the date of the event. The most common document with this type of register is a journal order.

In addition to the above types of accounting registers, maintaining a list for accounting policies is also classified according to the content and volume of records:

- Analytical. Registers of this kind allow you to systematize data according to any one characteristic (for example, sum up data on employee salaries). As a result, the manager and accounting department of the organization can analyze a specific component of the business;

- Synthetic. In this case, systematization occurs according to the principle of document homogeneity: all documents available in the organization that belong to any class of documents are accumulated in a separate group. They usually have a monetary equivalent. An example is the general ledger of an organization;

- Complex. They have characteristics of both analytical and synthetic registers and are used in most cases when filling out a journal order.

Accounting registers in accounting

All facts of the economic life of the institution must be confirmed by relevant primary documents.

It is unacceptable to enter business transactions and entries into accounting without a primary account. The information contained in the primary documentation is subject to special registration, generalization and accumulation in special journals, statements, books and accounting cards. Accounting registers are designed to reflect accounting entries and register primary documents. Information is systematized for further reflection on accounting accounts. Internal accounting documents are the basis for the formation of reliable accounting statements and separate reporting forms for management activities.

It is permissible to maintain accounting registers not only in paper form, but also in electronic form. For example, using specialized programs or websites. Electronic accounting documents are certified with the electronic signature of the responsible person (manager or chief accountant).

Use free access to ConsultantPlus to download current forms and find instructions on how to fill them out.

to read.

What form do registers have?

They are divided not only by appearance, but also by form of construction.

The form of construction is:

- Single-sided or double-sided. The data is filled in the journal according to the selected form (the most common is a two-sided form);

- Chess. In this case, the data is divided according to some criterion - for example, the assets and liabilities of the organization - and filled in cells at an angle to each other. As a rule, existing debits and credits are taken as separating data. Debits are plotted horizontally in the journal, and credits are plotted vertically.

In addition to the construction form, each register has a document specialized for its use. This is called the external form of the register.

- All kinds of cards. The accountant fills out certain data on a special form with a table. As of 2021, it is possible to separate account, multi-column and inventory cards - for example, a card for analytical accounting of enterprise expenses;

- Books. They look like graphed and stitched registers, usually numbering more than two hundred papers. Each page of the book is numbered and signed by the chief accountant. The most famous books in this area are the general ledger of the organization, the ledger for accounting of fixed assets, the cash book, and the registration journal;

- The so-called "free sheets" . Enlarged cards, whose functionality differs little from simple forms - a free sheet only gives a little more insight into the state of the company. Various statements are often printed on blank sheets;

- Machinegrams. The same as stated above. The difference is that these documents are compiled or printed using computers. At the moment, the number of documents filled out using technology is growing at such a rapid pace that machinograms can be approved by the Government of the Russian Federation as an outdated type of registers.

Forms of accounting registers

By appearance, registers are divided into:

- Books, the pages of which are necessarily laced, numbered, signed by the chief accountant and sealed with the seal of the organization.

- Cards. These are separate sheets, lined in the form of a table, which must be stitched together. They contain information on the names of accounting units, such as fixed assets, contractors, and goods. They are recorded in a special register.

- Magazines. Similar to books, but contain fewer pages and are not laced.

- Sheets. Individual documents are made in the form of a table or have a free form for text entries.

- Machine registers are only in electronic form, signed with a digital signature of the responsible person and stored on a computer or removable media. If necessary, it should be possible to print them at any time.

Journal

By Order of the Ministry of Finance No. 52n dated March 30, 2015, in accordance with budget laws, a list of registers for state enterprises was approved. They are often used not only by budgetary institutions, but also by commercial companies, including agricultural and construction companies.

Additional Information! All statements, cards and sheets must be filed in separate folders.

How are registers approved and filled out?

Until 2013, when amendments were introduced to Russian legislation regarding the preparation of accounting documents, all enterprises were required to record information on a unified form. Now it is permissible to use any document suitable for registration; You just need to provide the following information:

- the name of the document itself;

- legal name of the accounting company;

- time coverage of the document;

- form of registers and chosen classification order;

- an indication of all currencies and units of measurement given in the document;

- Full name and position of the person who does accounting.

The document must be approved by the person responsible for accounting (usually the chief accountant): the documentation must be signed and certified with the seal of the organization.

Please note: previously it was prohibited to make changes to the completed unified form. Now, starting in 2013, careful corrections in documentation have become acceptable.

Types and forms of accounting registers

Accounting registers differ in structure, purpose and other characteristics. Therefore, they are classified into the following groups: by appearance, by the nature of the records, the volume of content of the operations and by structure (Fig. 8.1).

According to their appearance (external form), registers are divided into ledgers, cards and free sheets. Accounting books are bound accounting tables (sheets of paper) designed to record transactions. It is impossible to remove sheets from books and replace them. Therefore, they are not suitable for mechanization and automation of records and complicate the division of labor of accounting workers. They are used to record inventories and other valuables at their storage locations, as well as to record certain types of calculations. All pages in the accounting book are numbered, and at the end of the book the signature of the chief accountant is placed and the number of pages is indicated.

The disadvantages of book registers include: the inability to group accounts opened in them in a different sequence; with a large volume of operations, books become bulky; in the books, excess consumption of sheets is allowed due to the need to reserve space in each book in case of opening new accounts. Cards and loose sheets are more convenient in this regard.

Cards are separate tables printed on separate sheets of thick paper or cardboard of a standard size. The cards are divided into the necessary sections (taking into account the nomenclature numbers of values, groups, stamps, etc.) in alphabetical or other order, for example, by codes or names of accounts, etc., which ensures that they are quickly found in the card index for recording or reconciling transactions and etc.

To register cards, a special register is created, where each card is assigned its own serial number. This makes it possible to check the availability of all cards. The use of cards contributes to the introduction of mechanization and automation of accounting processes, since entries in them, summing up and grouping of accounting data can be done not only manually, but also using computer technology.

Cards used in accounting practice are: current (have debit and credit columns); material (have columns for receipt, expense and balance, highlighting quantity and amount); multigraph (contain several columns).

Free sheets are tables containing a large number of details. They are stored in special folders (registers). Records of transactions on them can be kept by several accountants, since they can be retrieved from folders at any time for recording, counting, sampling, etc. Free sheets can be filled in using computer technology. Separate sheets are used in the form of journals, orders, statements and machine diagrams.

Based on the nature of the entries in them, accounting registers are divided into chronological, systematic and combined. Chronological registers are designed to reflect data on business transactions in calendar sequence as documents are received and processed, but without grouping them.

An example of chronological registers are business transaction logs, journals or registers for recording various documents. Their purpose is to ensure control over the safety of documents received by the accounting department, and they are also used for making inquiries, drawing up preliminary entries and checking them before posting transactions to accounting accounts.

Systematic registers are designed to record data from homogeneous business transactions, grouped according to their economic content according to accounting accounts, that is, by type of property and sources of economic funds. An example of a systematic register is the General Ledger, which is maintained in accounting to group transactions and summarize them into synthetic accounts.

Did not you find what you were looking for?

Teachers rush to help

Diploma

Tests

Coursework

Abstracts

Combined ledgers are ledgers in which transactions are recorded simultaneously in a chronological and systematic manner. They are used in simplified forms of accounting and in journal-order forms of accounting. These include the Journal - Main, accumulative statements, and order journals. Based on the volume of content of transactions or accounts, registers of synthetic and analytical accounting are distinguished.

Synthetic accounting registers are opened for maintaining synthetic accounts, that is, entries in synthetic registers are made in a generalized form in cost units of measurement. These include the General Ledger, Journal–Main, and journals—orders.

In analytical registers, data is recorded according to analytical accounts. Analytical registers indicate a summary of transactions and provide links to primary and summary documents on the basis of which entries were made. Accounting in analytical registers is carried out both in cost and in natural and labor units of measurement. This makes it possible to widely use analytical accounting data in the information system for control, analytical and management purposes.

According to the structure and form of graphing, accounting registers are divided into one-sided, two-sided, multi-graph, quantitative-total, quantitative, account-accountable, and chess.

One-sided registers are various cards for recording calculations and material assets, in which indicators are located on one side and separate columns of debit and credit entries are combined.

Double-sided registers are basically book-shaped registers where the account is opened on two unfolded pages - debit on the left side, credit on the right. They are used in synthetic and analytical accounting in the memorial-order form of accounting.

Multigraph registers are designed to record transactions, the amounts of which must be taken into account for individual elements, divisions, sections, warehouses, etc. Multigraph registers include registers of analytical accounting of production costs and material assets, etc.

For inventories, accounting is carried out simultaneously in physical and monetary terms. To do this, registers of quantitative and quantitative-sum forms are used. Quantitative accounting registers include warehouse accounting cards, a warehouse accounting book, and a book for recording the movement of livestock and poultry on the farm.

Quantitative-cumulative accounting registers include a book of accounting for product sales, a book of accounting for costs and output (release) of products, etc.

The contract form is a table, on the left side of which there are columns for the date, number and text of the entry (contents of the business transaction), on the right side there are columns for the amounts of debit and credit of accounts. Contract form registers are used to record settlements with debtors and creditors, with accountable persons, and to account for funds. In the contract form register, transactions are taken into account only in monetary terms.

Chess registers are used to reflect the amounts in the debit of one account and the credit of another account. Each amount is written in them in a checkerboard pattern, that is, at the intersection of a row and a column. An example of forms of chess registers are journals-orders, statements for them and the General Ledger in the journal-order form of accounting.

Nuances of making edits

The person maintaining the accounting records of an enterprise is directly responsible for reporting false information, concealing data and distorting it. Two points simultaneously follow from this: on the one hand, the desire to correct a document should be encouraged, on the other hand, it should be punished, since this introduces confusion into control over the organization.

Therefore, correction of errors is allowed, but only if the rules are followed. If at least one of them is violated, and the form is sent along with other documents to the Federal Tax Service or other authorities, the organization will be subject to penalties.

- The first method: you can cross out the erroneous information with one straight line, and write the correct information on top, above the erroneous information. Changes must be certified here with the signature of the person responsible for the company’s accounting;

- The second method, the so-called “reversal method”: without crossing out anything, you need to write an additional entry in red ink in the window where the error was made. In this case, the changes made must also be certified by a signature;

- Next to the correction you should indicate the date the changes were made;

- When correcting, use correctors, erasers, a blade, etc. It is highly not recommended: government authorities, when reading the document, should see the originally written data;

- In addition to all of the above, a brief and meaningful explanation of such corrections must be entered in the register where the error was made. For example: “When filling out the document, data on business income was mixed up with data on business expenses for the last quarter.”

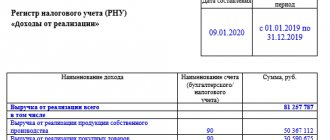

Tax accounting registers for income tax

To fill out a “profitable” declaration, you will need at least 2 NU registers: one for accounting for income, the other for expenses. Information about income received and expenses incurred, generated according to NU norms, will make it possible to determine profit - an object of taxation, without which the calculation of the income tax itself is impossible.

Read about what the tax base for different types of taxes may be in the article “Basic elements of taxation and their characteristics .

Additional registers will have to be drawn up in the case where the taxpayer has many types of activities, and also, in addition to standard business transactions, operations are carried out with special conditions for the transfer of ownership or for which a special procedure for forming the tax base is provided.

IMPORTANT! If the taxpayer cannot or does not want to develop tax accounting registers, but does not want to be punished under Art. 120 of the Tax Code of the Russian Federation for their absence, he has the right to use ready-made ones. Their forms can be found in the recommendations of the Ministry of Taxes of Russia “Tax accounting system recommended by the Ministry of Taxes of Russia for calculating profits in accordance with the norms of Chapter 25 of the Tax Code of the Russian Federation” dated December 19, 2001.

Example

Specialists of Ritm LLC reflect the information necessary for calculating income tax for the year in the following tax accounting registers (RNU):

- RNU "Income from sales" LLC "Rhythm";

- RNU "Expenses that reduce sales income" LLC "Rhythm";

- RNU "Non-operating income" LLC "Rhythm";

- RNU "Non-operating expenses" LLC "Rhythm".

Taking into account that during the specified period, Ritm LLC had no non-operating income and expenses, let us dwell in more detail on the preparation of tax registers for income received and expenses incurred for core activities.

ConsultantPlus experts spoke about the nuances of organizing tax accounting for income tax. Get trial access to the K+ system and move on to the Ready-made solution for free.

Storage order

Accounting documents should be stored in dry places, protected from direct sunlight; closed shelves, cabinets and safes are ideal for this.

Storage periods are regulated mainly by Art. 29 “On accounting” and paragraphs. 8 clause 1 of article 23 of the Tax Code of the Russian Federation. The first document specifies a period of at least 5 years after the reporting year, the second - for at least four years from the date of the tax period.

Such storage periods are established by the state due to the need in certain situations to access archival documents. Often, documents are requested in connection with some kind of litigation, and not necessarily directly related to the company - it could be a lawsuit against one of its employees, for example.

It should be remembered that some registers need to be stored longer than the periods indicated above. For example, salary records must be kept for at least 75 years from the date of their registration.

How to fill out the “expenditure” tax register

Taxpayers may experience certain difficulties filling out expense registers. This is due to the fact that the recognition of expenses in tax accounting does not always coincide with the reflection of similar expenses in accounting. So it is not always possible to use accounting registers without making additional adjustments to them.

For example, certain types of expenses are reflected in full in the accounting system, but are normalized in the accounting system (advertising, representative expenses, etc.). And tax legislation generally prohibits recognizing some types of expenses as expenses that form the taxable base for income tax.

Read about the nuances of recognizing other expenses associated with production and sales here.

Continuation of the example

A specialist from Ritm LLC formed a RNU “Expenses that reduce sales revenue”, which reflected the following types of expenses: costs for basic raw materials and supplies, wages along with accrued insurance premiums, depreciation of property of Ritm LLC, expenses for heat, water, electricity, etc.

The accountant took the information to fill out the register from accounting data (for accounts 20, 26, 44, 91, etc.). During the reporting period, the company did not incur expenses, the recognition of which in the financial accounting does not coincide with the accounting rules, so there was no need to adjust the accounting data.

You can also download a sample of a completed tax accounting register “Expenses that reduce sales revenue” on our website.

IMPORTANT! If tax expenses exceed tax revenues and there is no taxable base for profit in any of the periods (tax or reporting), a declaration must still be submitted to the tax authorities (clause 1 of Article 289 of the Tax Code of the Russian Federation).

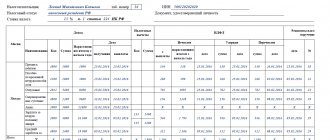

Accounting ledger example

One of the most common registers is the balance sheet. It is not only easy to fill out, but is also necessary for any commercial enterprise to fill out: in fact, it is this statement that reflects the current balance sheet of the enterprise, as well as its total capitalization.

Therefore, the balance sheet can be used as a sample. It looks quite simple: the content is divided into semantic blocks “How much was before accounting,” “During accounting,” and “By the end of the accounting period.” A table is compiled, divided into two subblocks under each column (the “Debit” and “Credit” blocks, the main ones in accounting).

It is not at all difficult for an experienced accountant to fill out such a table, especially in accounting. documentation, balance sheets are practically the simplest type of register. However, it does give a good initial understanding of what a register looks like and why it is needed, as well as how to fill it out.

Requirements for maintaining accounting registers

Business transactions must be reflected in the accounting registers in chronological order and grouped according to their respective accounts. The correct reflection of business transactions in accounting registers is ensured by the persons who compiled and signed them.

When stored, accounting registers must be protected from unauthorized corrections. The contents of accounting registers and internal financial statements are a commercial secret, and in cases provided for by the legislation of the Russian Federation, a state secret. Persons who have access to information contained in financial statements are required to maintain commercial and state secrets. For its disclosure they bear responsibility established by the legislation of the Russian Federation.

Entries in accounting registers are made in ink or a ballpoint pen (in cases where it is necessary to have several copies, copies are made, for example, when using calculating and writing machines, since the use of such means facilitates the work of accounting workers). Entries must be concise, clear, clear, legible, without erasures or erasures. You cannot make entries above or between lines. The method of recording in accounting registers can be linear-positional or chessboard.

The linear-positional recording method is used to account for settlements with buyers, suppliers and contractors, with accountable persons, etc. With this method, debit and credit turnovers are reflected in one position (line), which makes it possible to identify receivables or payables. For example, a journal order for account 71 “Settlements with accountable persons.”

In the case of a chess record form, a business transaction is recorded simultaneously in the debit and credit of accounts once. For example, in journal order No. 1 for account 50 “Cashier”, such an entry makes it possible to determine, control and analyze the completed business transaction through the correspondence of accounts.

After registering business transactions in the accounting registers, at the end of the month, results are summed up for each column. The final records of synthetic and analytical registers must be reconciled by comparing the turnover sheets, or in another way, and entered into the General Ledger.

After approval of the annual report, the accounting registers are grouped, bound and deposited in the current archive of the organization.